The Use of Criminal Statutes to Regulate Financial Markets in the United States

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2015 U.S. Sentencing Guidelines Manual

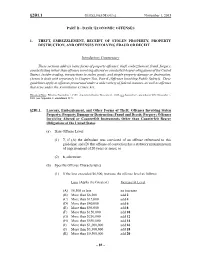

§2B1.1 GUIDELINES MANUAL November 1, 2015 PART B - BASIC ECONOMIC OFFENSES 1. THEFT, EMBEZZLEMENT, RECEIPT OF STOLEN PROPERTY, PROPERTY DESTRUCTION, AND OFFENSES INVOLVING FRAUD OR DECEIT Introductory Commentary These sections address basic forms of property offenses: theft, embezzlement, fraud, forgery, counterfeiting (other than offenses involving altered or counterfeit bearer obligations of the United States), insider trading, transactions in stolen goods, and simple property damage or destruction. (Arson is dealt with separately in Chapter Two, Part K (Offenses Involving Public Safety)). These guidelines apply to offenses prosecuted under a wide variety of federal statutes, as well as offenses that arise under the Assimilative Crimes Act. Historical Note: Effective November 1, 1987. Amended effective November 1, 1989 (see Appendix C, amendment 303); November 1, 2001 (see Appendix C, amendment 617). §2B1.1. Larceny, Embezzlement, and Other Forms of Theft; Offenses Involving Stolen Property; Property Damage or Destruction; Fraud and Deceit; Forgery; Offenses Involving Altered or Counterfeit Instruments Other than Counterfeit Bearer Obligations of the United States (a) Base Offense Level: (1) 7, if (A) the defendant was convicted of an offense referenced to this guideline; and (B) that offense of conviction has a statutory maximum term of imprisonment of 20 years or more; or (2) 6, otherwise. (b) Specific Offense Characteristics (1) If the loss exceeded $6,500, increase the offense level as follows: Loss (Apply the Greatest) Increase -

What Is Securities Fraud?

BUELL IN PRINTER PROOF 11/11/2011 5:38:12 PM Duke Law Journal VOLUME 61 DECEMBER 2011 NUMBER 3 WHAT IS SECURITIES FRAUD? SAMUEL W. BUELL† ABSTRACT As Rule 10b-5 approaches the age of seventy, deep familiarity with this supremely potent and consequential provision of American administrative law has obscured its lack of clear conceptual content. The rule, as written, interpreted, and enforced, is missing a fully developed connection to—of all things—fraud. Fraud is difficult to define. Several approaches are plausible. But the law of securities fraud, and much of the commentary about that body of law, has neither attempted such a definition nor acknowledged its necessity to the coherence and effectiveness of the doctrine. Securities fraud’s lack of mooring in a fully developed concept of fraud produces at least three costs: public and private actions are not brought on behalf of clearly specified regulatory objectives; the line between civil and criminal liability has become unacceptably blurred; and the law has come to provide at best a weak means of resolving vital public questions about wrongdoing in financial markets. The agenda of this Article is threefold. First, this Article illuminates and clarifies the relationship between securities fraud and fraud and structures a discussion of legal reform that more explicitly connects Copyright © 2011 by Samuel W. Buell. † Professor of Law, Duke University School of Law. I am grateful for the helpful questions and comments of Tom Baker, Sara Sun Beale, Stuart Benjamin, Ben Depoorter, Lisa Kern Griffin, Kim Krawiec, Dan Markel, James Park, and participants in workshops at Duke University School of Law, Willamette University College of Law, Notre Dame Law School, and Florida State University College of Law. -

Prosecuting Securities Fraud Under Section 17(A)(2)

Loyola University Chicago Law Journal Volume 50 Issue 3 Spring 2019 Article 11 2019 Prosecuting Securities Fraud Under Section 17(a)(2) Wendy Gerwick Couture Follow this and additional works at: https://lawecommons.luc.edu/luclj Part of the Law Commons Recommended Citation Wendy Gerwick Couture, Prosecuting Securities Fraud Under Section 17(a)(2), 50 Loy. U. Chi. L. J. 669 (). Available at: https://lawecommons.luc.edu/luclj/vol50/iss3/11 This Symposium Article is brought to you for free and open access by LAW eCommons. It has been accepted for inclusion in Loyola University Chicago Law Journal by an authorized editor of LAW eCommons. For more information, please contact [email protected]. Prosecuting Securities Fraud Under Section 17(a)(2) Wendy Gerwick Couture* INTRODUCTION ............................................................................. 669 I. STATUTES CRIMINALIZING VIOLATIONS OF SECTION 17(A)(2) AND RULE 10B-5 ........................................................................... 670 II. “IN THE OFFER OR SALE OF ANY SECURITIES” VERSUS “IN CONNECTION WITH THE PURCHASE OR SALE OF ANY SECURITY” ............................................................................ 673 III. “TO OBTAIN MONEY OR PROPERTY” ELEMENT ...................... 679 IV. “BY MEANS OF” VERSUS “MAKE” .......................................... 683 V. “WILLFULLY” VERSUS “WILLFULLY AND KNOWINGLY” ......... 684 VI. IMPLICATIONS OF PROSECUTING SECURITIES FRAUD UNDER SECTION 17(A)(2) ................................................................. -

The Corporate and Criminal Fraud Accountability Act of 2002

Calendar No. 366 107TH CONGRESS REPORT "! 2d Session SENATE 107–146 THE CORPORATE AND CRIMINAL FRAUD ACCOUNTABILITY ACT OF 2002 MAY 6, 2002.—Ordered to be printed Mr. LEAHY, from the Committee on the Judiciary, submitted the following R E P O R T together with ADDITIONAL VIEWS [Including the cost estimate of the Congressional Budget Office] [To accompany S. 2010] The Committee on the Judiciary, to which was referred the bill (S. 2010) to provide for criminal prosecution of persons who alter or destroy evidence in certain Federal investigations or defraud in- vestors of publicly traded securities, to disallow debts incurred in violation of securities fraud laws from being discharged in bank- ruptcy, to protect whistleblowers against retaliation by their em- ployers, and for other purposes, having considered the same, re- ports favorably thereon, with an amendment in the nature of a substitute, and recommends that the bill, as amended, do pass. CONTENTS Page I. Purpose ........................................................................................................... 2 II. Background and need for the legislation ..................................................... 2 III. Section-by-section analysis and discussion .................................................. 11 IV. Committee consideration ............................................................................... 21 V. Votes of the Committee ................................................................................. 21 VI. Congressional Budget Office cost estimate -

Applying the Fraud-Exclusion Provision Under D&O

APPLYING THE FRAUD-EXCLUSION PROVISION UNDER D&O INSURANCE POLICIES: “ADJUDICATION” OR “IN FACT” – WHICH IS BETTER? Fang Liu* TABLE OF CONTENTS I. INTRODUCTION ................................................................. 248 II. BACKGROUND .................................................................. 249 III. STRUCTURE OF A D&O INSURANCE POLICY ....... 252 IV. ANALYSIS OF D&O INSURANCE POLICY PROVISIONS ............................................................................ 252 V. EXCLUSION PROVISIONS .............................................. 254 A. Deliberate-Fraud Exclusion ........................................ 254 B. Alstrin: Problematic Reasoning and Holding .............. 257 C. AT & T: Adjudication or Settlement ............................ 259 D. PMI: An Ambiguous “Some-Evidentiary-Proof” Standard ........................................................................... 261 E. Which Approach Should Be Applied? .......................... 262 VI. CONCLUSION ................................................................... 263 * Fang Liu is an associate with Dickinson Wright PLLC in Ann Arbor, Michigan. She graduated from Peking University School of Law with an LL.B. degree in 1999. Ms. Liu was a corporate attorney with nine years of legal experience in China before she came to the United States. Ms. Liu received her J.D. degree, magna cum laude, from Western Michigan University Cooley Law School and an LL.M. degree with a business-law certificate from University of California, Berkeley, School of Law. Ms. -

Investor Alert: Social Media and Investing – Avoiding Fraud

Investor Alert: Social Media and Investing - Avoiding Fraud The SEC’s Office of Investor Education and Advocacy What You Can Do To Protect Yourself - is issuing this Investor Alert to help investors be Tips to Help Avoid Fraud Online better aware of fraudulent investment schemes that may involve social media. U.S. retail investors So, what can individual investors do to use social are increasingly turning to social media, including media, while at the same time protecting themselves? Facebook,YouTube,Twitter, LinkedIn and other The key to avoiding investment fraud on the Internet is online networks for information about investing. to be an educated investor. Below are five tips to help Whether it be for research on particular stocks, you avoid investment fraud on the Internet: background information on a broker-dealer or investment adviser, guidance on an overall investing strategy, up-to-date news, or to simply discuss the Be Wary of Unsolicited Offers to markets with others, social media has become a key Invest tool for U.S. investors. Investment fraud criminals look for victims on While social media can provide many benefits for social media sites, chat rooms, and bulletin boards. If you see a new post on your wall, a tweet investors, it also presents opportunities for fraudsters. mentioning you, a direct message, an e-mail, or Social media, and the Internet generally, offer a any other unsolicited – meaning you didn’t ask for number of attributes criminals may find attractive. it and don’t know the sender – communication Social media lets fraudsters contact many different regarding a so-called investment opportunity, you people at a relatively low cost. -

Corporate Scienter and Securities Fraud Liability

© Practising Law Institute CORPORATE LAW AND PRACTICE Course Handbook Series Number B-2165 Securities Litigation 2015: From Investigation to Trial Co-Chairs Lyle Roberts Jonathan K. Youngwood To order this book, call (800) 260-4PLI or fax us at (800) 321-0093. Ask our Customer Service Department for PLI Order Number 58858, Dept. BAV5. Practising Law Institute 1177 Avenue of the Americas New York, New York 10036 © Practising Law Institute 7 Being of One Mind: Corporate Scienter and Securities Fraud Liability Lyle Roberts Cooley LLP If you find this article helpful, you can learn more about the subject by going to www.pli.edu to view the on demand program or segment for which it was written. 207 © Practising Law Institute 208 © Practising Law Institute If a corporate official makes a statement to investors and another corpo- rate official knows the statement is false, can the company be liable for securities fraud? Federal appellate courts have struggled with this ques- tion in assessing what must be plead and/or proven to establish the requisite scienter (or fraudulent intent) for a corporate defendant facing claims brought under Section 10(b) of the Securities Exchange Act and Rule 10b-5 promulgated thereunder. Recent Supreme Court jurispru- dence, however, strongly suggests that only the scienter of corporate officials who “made” the alleged false statements should be imputed to the company. BACKGROUND Rule 10b–5 prohibits the “mak[ing] any untrue statement of a material fact” in connection with the purchase or sale of securities. 17 CFR 240.10b-5(b) (2010).1 It is the most common basis for federal securities fraud claims brought against publicly-traded companies. -

GAO-11-664 Securities Fraud Liability of Secondary Actors

United States Government Accountability Office Washington, DC 20548 B-321063 July 21, 2011 The Honorable Tim Johnson Chairman The Honorable Richard C. Shelby Ranking Member Committee on Banking, Housing, and Urban Affairs United States Senate The Honorable Spencer Bachus Chairman The Honorable Barney Frank Ranking Member Committee on Financial Services House of Representatives Subject: Securities Fraud Liability of Secondary Actors Since the 1930s, publicly traded companies that commit fraud in the issuance or sale of their securities have been liable to private investors under the U.S. securities laws, as well as subject to government enforcement of these laws. Entities commonly referred to as “secondary actors”—such as banks, brokers, accountants, and lawyers, who play important but generally lesser roles in securities transactions1—may also be liable to investors and to the government for certain securities law violations, but as of 1994, such entities are liable only to the government, not to investors, for substantially assisting— or “aiding and abetting”—securities fraud under section 10(b) of the Securities Exchange Act of 1934 (1934 Act).2 Before 1994, courts had interpreted section 10(b), as implemented by the Securities and Exchange Commission’s (the 1 In general, “secondary actors” are persons charged with “secondary liability” because they do not directly commit violations of the anti-fraud provisions but instead are alleged to provide substantial assistance to fraudulent conduct. Because transactions subject to the federal securities laws are often complex and involve multiple entities, it can be difficult to determine, at the time a violation occurs, who should be subject to primary versus secondary liability. -

Principles for State Prosecution of Securities Crime in a Dual-Regulatory, Multi-Enforcer Regime

PRINCIPLES FOR STATE PROSECUTION OF SECURITIES CRIME IN A DUAL-REGULATORY, MULTI-ENFORCER REGIME Wendy Gerwick Couture* ABSTRACT This article proposes principles for the exercise of prosecutorial discretion when prosecuting securities crime under state law. Securities transactions in the United States are subject to a dual-regulatory, multi- enforcer regime. Securities are dually regulated by the federal government and the states, with each regulatory scheme including both civil and criminal enforcement provisions. Those laws are multi-enforced at each level by a regulator, private parties, and prosecutors. And yet, the role of state prosecution of securities crime within this regime is undertheorized, and there is little guidance for state prosecutors about how their prosecutorial decisions affect this regime. This article, drawing from the goals of prosecuting securities crime and the implications of this complex regime, provides guidance on states’ exercise of prosecutorial discretion therein. I. INTRODUCTION......................................................................................... 31 II. STATE PROSECUTION OF SECURITIES CRIME WITHIN A DUAL- REGULATORY, MULTI-ENFORCER REGIME...................................... 34 A. Dual Federal-State Regulation .................................................. 34 B. Scope of State Securities Crimes .............................................. 36 1. Definition of “Security” ...................................................... 37 2. Mental State About Unregistered, Non-Exempt Status...... -

Securities Fraud and the Tax Loss Deduction: the Rise and (Perhaps) Fall of the Stockbroker Exclusion

SECURITIES FRAUD AND THE TAX LOSS DEDUCTION: THE RISE AND (PERHAPS) FALL OF THE STOCKBROKER EXCLUSION ∗Brian Elzweig, J.D., LL.M. ∗∗Valrie Chambers, CPA, Ph.D. I. INTRODUCTION Recent financial frauds, and in particular Ponzi schemes, have prompted new tax clarifications to the theft loss rules. A revenue ruling and complementary revenue procedure (both issued in 2009) make deducting thefts from such recognized schemes on federal individual tax returns easier. These new rules are in contrast with the recent court decisions where a theft loss was denied, in part because the plaintiff had given his money to a broker to buy stock, rather than to the executives actually committing the fraud. The case law has stated that there is a need for direct privity between the person who is being defrauded and the person committing the fraud for a theft loss to be allowable. The new rules are silent on whether using an intermediary as an agent will disqualify a taxpayer from taking a theft loss. This article explores the genesis of the judicially created rule that direct privity is needed. The privity requirement essentially eliminates the possibility of a theft loss deduction for any brokered securities transaction. Because most securities transactions involve an intermediary, there is often no recovery for these victims. Use of an intermediary does not make one less defrauded than one who was to purchase a security directly from an issuer. This article then shows that the need for direct privity should be eliminated so that more victims of security fraud would be able to avail themselves of a theft loss deduction. -

Criminal Division/Fraud Section, Year in Review 2019

Fraud Section Year In Review | 2019 United States Department of Justice | Criminal Division | Fraud Section 1 Welcome to the Fraud Section The Fraud Section is a national leader in the Department of Justice’s fight against economic crime. As the Department’s office with the largest number of white-collar prosecutors, the Fraud Section focuses on the prosecution of complex and sophisticated securities, commodities, and other financial fraud cases; foreign bribery offenses; and complex, multi-jurisdictional health care fraud, Anti-Kickback Statute, and opioid cases in federal courts around the country, routinely charging and resolving cases of both national and international significance and prominence. Located in Washington, D.C., the Fraud Section employs over 150 prosecutors and has over 120 federal and contract support staff. The Fraud Section has three litigating units: FCPA Foreign Corrupt Practices Act Unit MIMF1 HCF Market Integrity Health Care and Major Fraud Unit Frauds Unit http://www.justice.gov/criminal-fraud 1 In October 2019, the Fraud Section announced that the Securities and Financial Fraud (SFF) Unit would be renamed the Market Integrity and Major Frauds (MIMF) Unit to more accurately reflect the diversity of the MIMF Unit’s concentrations: (1) commodities; (2) consumer, regulatory, and investment fraud; (3) financial institutions; (4) government procurement fraud and bribery; and (5) securities. For ease of reference, the term MIMF Unit in this document will refer to both the SFF Unit and the MIMF Unit. Cover Photo - “Bond Building - Washington, D.C." by AgnosticPreachersKid is licensed under CC BY 3.0 / Desaturated and watercolored from original. 2 The Foreign Corrupt Practices Act (FCPA) Unit has primary jurisdiction among the Department components in prosecuting FCPA matters. -

In the Supreme Court of the United States ______

No. 20-306 In the Supreme Court of the United States ____________________ ROBERT OLAN and THEODORE HUBER, Petitioners, v. UNITED STATES OF AMERICA, Respondent. ____________________ On Petition for a Writ of Certiorari to the Court of Appeals for the Second Circuit ____________________ BRIEF OF LAW PROFESSORS AS AMICI CURIAE IN SUPPORT OF PETITIONERS ____________________ Anton Metlitsky Michael R. Dreeben O’MELVENY & MYERS LLP Counsel of Record Times Square Tower Kendall Turner 7 Times Square O’MELVENY & MYERS LLP New York NY 10036 1625 Eye Street NW Washington, DC 20006 (202) 383-5400 [email protected] i QUESTION PRESENTED Amici curiae will address the following question: Whether this Court’s holding in Dirks v. SEC, 463 U.S. 646 (1983), requiring proof of “personal benefit” to establish insider-trading fraud, applies to Title 18 statutes that proscribe fraud in language virtually identical to the Title 15 anti-fraud provisions at issue in Dirks. ii TABLE OF CONTENTS Page INTERESTS OF AMICI CURIAE ............................ 1 INTRODUCTION ..................................................... 3 STATEMENT ............................................................ 5 ARGUMENT ............................................................. 8 I. GRANTING THE PETITION IS ESSENTIAL TO RESTORE COHERENCE TO INSIDER- TRADING LAW ................................................... 8 A. Trading On Inside Information Is Fraudulent Only If The Insider Acts For Personal Benefit ............................................. 9 B. The Second Circuit Erred