Alectra Inc. 2018 Consolidated Financial Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Discovering the Possibilities About Our Sustainability Report

2019 Annual Sustainability Report Discovering the possibilities About our sustainability report The Alectra Inc. 2019 Annual Sustainability Report provides details about Alectra’s social, environmental and economic impact, as well as issues that are of material interest to our stakeholders as validated through a third-party materiality assessment and a variety of engagement activities. Material issues include: Health and Safety/ Public Health and Safety; Infrastructure Modernization; Community Engagement; Climate Change; Customer Services; Energy Affordability; Waste and Material Management; Diversity and Inclusion; Employee Well-Being, Engagement and Development; Energy Efficiency; and Financial Performance. Commitment Our sustainability commitment As a sustainable company, Alectra is committed to meeting today’s needs and the needs of future generations by empowering our customers, communities and employees, protecting the environment, and embracing innovation. Our vision is to be Canada’s leading distribution and integrated energy solutions provider, creating a future where people, businesses and communities will benefit from energy’s full potential. Our mission is to provide customers with smart and simple energy choices, while creating sustainable value for our shareholders, customers, communities and employees. Our values are safety, respect, customer focus, excellence, and innovation. CONTENTS 2 Corporate profile 10 People 3 2019 Achievements 20 Planet 4 Message to our stakeholders 26 Performance 6 A new energy future 32 Corporate governance 8 The Alectra GRE&T Centre Corporate Profile As one of Canada’s Sustainability leading energy companies, at Alectra Alectra Inc. is shaping the Our sustainability future of energy. framework – AlectraCARES We provide safe, reliable and innovative We have embedded sustainability energy solutions to families and About Alectra principles into our core business businesses across the 17 communities strategy and operations in order to in our service territory, while maintaining Alectra Inc. -

Download the 2018 Annual Sustainability Report

SUSTAINABLE POWER Discovering the possibilities 2018 Annual Sustainability Report Sustainable power balances social responsibility and environmental accountability with economic efficiency – People, Planet and Performance. It is power that embraces innovation to improve our quality of life by providing safe and reliable energy solutions that help deliver value to our homes, workplaces and communities. Alectra is committed to helping customers and the communities we serve discover the possibilities of a new energy future for our people and our planet through our sustainable performance. This is Alectra’s second Annual Sustainability Report which highlights our achievements in 2018. Alectra’s Vision, Mission and Values Our Vision To be Canada’s leading electricity distribution and integrated energy solutions provider, creating a future where people, businesses and communities will benefit from energy’s full potential. Our Mission To provide customers with smart and simple energy choices, while creating sustainable value for our shareholders, customers, communities and employees. Our Values Our core values are safety, respect, customer focus, excellence and innovation. 2 Corporate Profile 4 Message to Stakeholders 6 Corporate Governance 8 Sustainability at Alectra 10 Stakeholder Engagement 12 Sustainability Leadership 14 People 22 Planet 30 Performance Alectra Inc. 2018 Annual Sustainability Report 1 Corporate Profile About Alectra Alectra Inc. (Alectra) is an investment holding customers, we deliver approximately company with a head office in Mississauga, 22 per cent of Ontario’s electricity. In Ontario, that owns 100 per cent of the addition to our electricity distribution common shares of each of: Alectra Utilities business, Alectra Utilities Corporation Corporation (Alectra Utilities), Alectra Energy has a non-regulated commercial rooftop Solutions Inc. -

Alectra Inc. 16X9

Exploring PSBN in Electric Utilities 1 March 26, 2019 Keith Hemingway, Manager Operational Technology Services Who We Are 2 Together we’re better • Enersource, Horizon Utilities and PowerStream merged to become Alectra Inc. on January 31, 2017; The company acquired Hydro One Brampton on February 28, and merged with Guelph Hydro on January 1, 2019. • The consolidation of the four utilities created the second largest municipally-owned electric utility by customer base in North America (second only to Los Angeles Department of Water and Power) • Alectra Inc. is the holding company for several subsidiaries including Alectra Utilities and Alectra Energy Solutions 3 Alectra’s family of companies • Alectra’s family of energy companies distributes electricity to nearly one million customers in Ontario’s Greater Golden Horseshoe area and provides innovative energy solutions to these and thousands more all across Ontario. Our employees are allies in helping customers discover the possibilities of energy conservation and new technologies for enhancing their quality of life. We create sustainable value for our customers, communities and shareholders. 4 Alectra’s family of companies 5 Our name & signature line • The Greek meaning of the name Alectra means brilliant. Our name also conveys energy... the energy of our people and the millions of customers we serve. • Alectra identifies us with the energy sector today and for the future—and sends the message that we are the customer’s ally. • Our signature line, ‘Discover the Possibilities’ is an invitation—to our customers, employees and communities—to come with us on this journey. It says we aspire to something bold for the future, but we’re also about practical choices that improve daily life. -

Alectra Utilities (“Alectra”) Serves Over One Million Customers Across 1,800 Sq

February 13, 2020 IESO Engagement Independent Electricity System Operator 1600–120 Adelaide Street West Toronto, ON M5H 1T1 To Whom it May Concern: Re: Exploring Expanded DER Participation in the IESO-Administered Markets Part 2: Options and Considerations for Enabling DER Participation On October 17, 2019 the Independent Electricity System Operator (“IESO”) released the first in its series of white papers (the “Paper”) on exploring expanded Distributed Energy Resource (“DER”) participation in the IESO Administered Markets (“IAMs”). The Paper overviewed the ways in which DERs currently participate in the IAM, concluding that only directly participating generators, Demand Response (“DR”) and aggregated non-dispatchable DR are currently able to fully participate. The Paper also examined several barriers that prevent DERs from other types or forms of participation. On January 30, 2020, the IESO hosted a webinar to provide an overview of the next DER white paper and to introduce some of its high-level ideas and options to enhance DER participation that may be explored in the next Paper. The intention of the next Paper will be to include more detailed examination of participation models and options to address barriers identified in the first Paper. The IESO is seeking feedback from stakeholders on the options presented in the webinar in order to determine or guide which should be explored further. Alectra Utilities (“Alectra”) serves over one million customers across 1,800 sq. km of service territory, spanning 17 communities in Ontario, including Alliston, Aurora, Barrie, Beeton, Brampton, Bradford, Guelph, Hamilton, Markham, Mississauga, Penetanguishene, Richmond Hill, Rockford, St. Catharines, Thornton, Tottenham and Vaughan. -

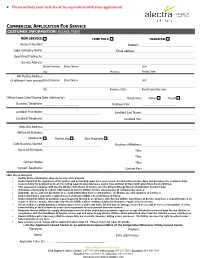

Commercial Application Form

* Please include your Articles of Incorporation with your application. COMMERCIAL APPLICATION FOR SERVICE CUSTOMER INFORMATION: PLEASE PRINT NEW SERVICE: TEMP POLE: TRANSFER: Account Number: Deposit: Legal Company Name: Email address: Operating/Trading As: Service Address: Street Number Street Name Unit City Province Postal Code Bill Mailing Address: (if different from service) Street Number Street Name Unit City Province/State Postal Code/Zip Code Official Lease Date/Closing Date (dd/mm/yy): Check One: Owner Tenant Business Telephone: Business Fax: Landlord First Name: Landlord Last Name: Landlord Telephone: Landlord Fax: Web Site Address: Nature of Business: Corporation Partnership Sole Proprietor Date Business Started: Business Affiliations: Name of Principals: Title: Title: Contact Name: Title: Contact Telephone: Contact Fax: I/We, the undersigned Certify all the information above to be true and complete; Understand that the signatures of the parties will be binding upon their successors. Vacating this premise does not discharge the customer from responsibility for payment up to and including legal closing date/lease expiry date, without written notification from Alectra Utilities; This agreement complies with Alectra Utilities Conditions of Service and the Ontario Energy Boards Distribution System Code; Authorize a third party to submit information to Alectra Utilities for the sole purpose of commencing service; Authorize the receipt and provision of account information from credit grantors, credit bureaus and suppliers of services; Understand that a deposit is required based on Alectra Utilities Security Deposit Policy. Understand that failure to maintain a good payment history in accordance with Alectra Utilities Conditions of Service may have a deposit invoiced as required. Service may be interrupted by Alectra Utilities when customer payments for power supplied are in arrears; Alectra Utilities cannot guarantee uninterrupted service and is not liable for any loss or damage incurred as a result of service interruption. -

Discovering the Possibilities

Discovering the possibilities 2020 Annual Sustainability Report About our sustainability report The Alectra Inc. 2020 Annual Sustainability Report provides details about Alectra’s social, environmental, and economic impact, as well as issues that are of significant interest to our stakeholders as validated through a third-party assessment and a variety of engagement activities. Significant issues include: Health and Safety/Public Health and Safety; Infrastructure Modernization; Community Engagement; Climate Change; Customer Services; Energy Affordability; Waste and Materials Management; Equity, Diversity and Inclusion; Employee Well-Being, Engagement and Development; Energy Efficiency; and Financial Performance. Many of these issues were brought into sharper focus as the COVID-19 pandemic affected all aspects of the corporation and the communities we serve. This report discusses the impact of these issues in detail. This is Alectra’s fourth Annual Sustainability Report. Transparently sharing our performance and progress is one way of demonstrating our commitment to the three pillars of sustainability – people, planet, and performance. Our sustainability commitment As a sustainable company, Alectra is committed to meeting the needs of current and future generations by empowering our customers, communities, and employees, protecting the environment, and embracing innovation. Our vision is to be Canada’s leading distribution and integrated energy solutions provider, creating a future where people, businesses, and communities will benefit from energy’s full potential. Our mission is to provide customers with smart and simple energy choices, while creating sustainable value for our shareholders, customers, communities, and employees. Our values are safety, respect, customer focus, excellence, and innovation. CONTENTS 2 Corporate Profile 4 2020 Highlights 6 Message to our Stakeholders 8 Response to COVID-19 10 People 18 Planet 26 Performance 36 Corporate Governance 38 Alectra Fast Facts CORPORATE PROFILE As one of Canada’s leading energy companies, Alectra Inc. -

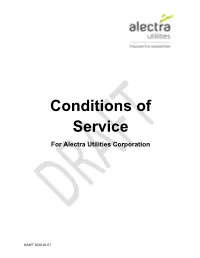

Conditions of Service for Alectra Utilities Corporation

Conditions of Service For Alectra Utilities Corporation DRAFT 2020.01.07 PREFACE CONDITIONS OF SERVICE Alectra Utilities’ Conditions of Service contains three major sections: Section 1 (Introduction): contains references to the legislation that covers the Conditions of Service, the rights of the Customer and of Alectra, and the dispute resolution process. Section 2 (General Distribution Activities): contains references to services and requirements that are common to all the Customer classes. This section covers items such as Capital Contribution, Billing, Hours of Work, Emergency Response, Power Quality and Availability Voltages. Section 3 (Customer Specific): contains references to services and requirements specific to the respective Customer class. This section covers items such as Service Entrance Requirements, Delineation of Ownership, Special Contracts, and Metering etc. Other sections include the Glossary of Terms (Section 4), and Appendices (Section 5). 2 Table of Contents 1. INTRODUCTION .............................................................................................................................. 10 1.1 IDENTIFICATION OF DISTRIBUTOR AND SERVICE AREA ......................................... 10 1.2 RELATED CODES, AND GOVERNING LAWS ................................................................. 10 1.3 INTERPRETATION ................................................................................................................. 11 1.4 AMENDMENTS AND CHANGES ........................................................................................ -

Scorecard - Alectra Utilities Corporation 10/21/2020

Scorecard - Alectra Utilities Corporation 10/21/2020 Target Performance Outcomes Performance Categories Measures 2015 2016 2017 2018 2019 Trend Industry Distributor Customer Focus New Residential/Small Business Services Connected 99.47% 99.59% 97.02% 94.57% 92.59% 90.00% Service Quality on Time Services are provided in a Scheduled Appointments Met On Time 95.97% 99.47% 99.31% 99.31% 98.75% 90.00% manner that responds to Telephone Calls Answered On Time 80.73% 80.61% 79.52% 77.67% 75.78% 65.00% identified customer preferences. First Contact Resolution 82.76% 80.86% 81.73% 86.18% 85.1% Customer Satisfaction Billing Accuracy 99.54% 99.56% 99.64% 99.59% 99.58% 98.00% Customer Satisfaction Survey Results 91.13% 90.76% 88.05% 90.89% 93% Operational Effectiveness Level of Public Awareness 78.60% 78.59% 81.27% 81.27% 82.00% 1 Safety Level of Compliance with Ontario Regulation 22/04 C C C C C C Continuous improvement in Serious Electrical Number of General Public Incidents 8 6 9 13 20 6 productivity and cost Incident Index Rate per 10, 100, 1000 km of line 0.388 0.289 0.429 0.621 0.950 0.283 performance is achieved; and Average Number of Hours that Power to a Customer is distributors deliver on system 1.00 0.83 0.80 1.04 1.07 0.91 System Reliability Interrupted 2 reliability and quality objectives. Average Number of Times that Power to a Customer is 1.23 1.09 1.11 1.33 1.26 1.26 Interrupted 2 Asset Management Distribution System Plan Implementation Progress 108.28% 96.16% 95.82% 89.01% 114% Efficiency Assessment 3 3 3 3 3 Cost Control Total Cost -

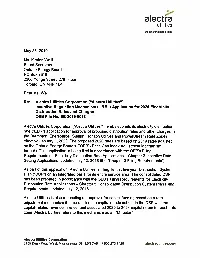

Alectra Utilities

, alectra utilities Discover the possibilities May 28, 2019 Ms. Kirsten Walli Board Secretary Ontario Energy Board PO Box 2319 2300 Yonge Street, 27th Floor Toronto, ON M4P 1E4 Dear Ms. Walli: Re: Alectra Utilities Corporation ("Alectra Utilities") Incentive Regulation Mechanism ("IRM") Application for 2020 Electricity Distribution Rates and Charges OEB File No. EB-2019-0018 Alectra Utilities Corporation ("Alectra Utilities") hereby submits its electricity distribution rate ("EDR") application for approval of proposed distribution rates and other charges in the Brampton, Enersource, Guelph, Horizon Utilities and PowerStream Rate Zones effective January 1, 2020. The proposed 2020 rates are based on 2019 rates adjusted by the Ontario Energy Board's ("OEB") Price Cap Index Adjustment Mechanism formula. This application is being filed in accordance with the OEB's Filing Requirements for Electricity Distribution Rate Applications — Chapter 3 Incentive Rate- Setting Applications, updated July 12, 2018 (the "Chapter 3 Filing Requirements"). As part of this application, Alectra Utilities is filling its first five-year Distribution System Plan ("DSP") on an integrated basis for its entire service area. The consolidated DSP has been prepared in accordance with the OEB's Filing Requirements for Electricity Distribution Rate Applications — Chapter 5 Consolidated Distribution System Plan Filing Requirements, updated July 12, 2018. Alectra Utilities is also requesting an approval for capital funding based on a rate- adjustment mechanism that reconciles -

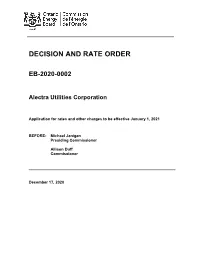

Decision and Rate Order for Alectra 2021

DECISION AND RATE ORDER EB-2020-0002 Alectra Utilities Corporation Application for rates and other charges to be effective January 1, 2021 BEFORE: Michael Janigan Presiding Commissioner Allison Duff Commissioner December 17, 2020 Table of Contents 1 INTRODUCTION AND SUMMARY ................................................................................ 1 2 THE PROCESS .............................................................................................................. 3 3 ORGANIZATION OF THE DECISION ............................................................................ 4 4 PRICE CAP ADJUSTMENT ........................................................................................... 5 5 RETAIL TRANSMISSION SERVICE RATES ................................................................. 7 6 GROUP 1 DEFERRAL AND VARIANCE ACCOUNTS .................................................. 9 7 LOST REVENUE ADJUSTMENT MECHIANSM VARIANCE ACCOUNT BALANCE ..35 8 RENEWABLE GENERATION CONNECTION RATE PROTECTION ...........................39 9 HORIZON RZ – EARNINGS SHARING MECHANISM .................................................43 10 HORIZON RZ – CAPITAL INVESTMENT VARIANCE ACCOUNT ...............................47 11 CAPITALIZATION DEFERRAL ACCOUNTS ...............................................................50 12 INCREMENTAL CAPITAL MODULE ............................................................................53 13 IMPLEMENTATION AND ORDER ................................................................................64 Ontario -

Regulated Price Plan Pilot – Dynamic Pricing Final Report

Regulated Price Plan Pilot – Dynamic Pricing Final Report Submitted to the Ontario Energy Board Alectra Utilities with its partner BEworks January, 2021 CONTRIBUTORS About Alectra Alectra Alectra’s family of energy companies distributes electricity to more than one TEAM MEMBERS million homes and businesses in Ontario’s Neetika Sathe Greater Golden Horseshoe area and provides VP, GRE&T Centre innovative energy solutions to these and Daniel Carr thousands more across Ontario. The Alectra Head, Smart Cities family of companies includes Alectra Inc., Shirley Liu Alectra Utilities Corporation and Alectra Analyst, Smart Cities Energy Solutions. Learn more about Alectra at alectrautilities.com. i CONTRIBUTORS About BEworks BEworks Founded in 2010, BEworks is an unconventional management consulting firm that applies scientific thinking to transform the economy TEAM MEMBERS and society. BEworks’ team of experts in Kelly Peters cognitive and social psychology, neuroscience, CEO and marketing answer clients' most complex Dave Thomson business questions, execute disruptive growth Director, Experimentation strategies, and accelerate innovation. Sarah M. Carpentier Associate Part of the kyu collective of companies since Leigh Christopher January 2017, the firm's client list includes Associate Fortune 1000 companies, not-for-profit Nathaniel Whittingham organizations and government agencies. Behavioural Data Scientist BEworks was co-founded by Dan Ariely, Jesse Van Patter renowned behavioural scientist, Kelly Peters, Data Analyst the firm's CEO and BE pioneer, and top Matthew O’Brien marketing scholar Nina Mažar. Data Analyst For more information, please visit www.BEworks.com, @BEworksInc or https://www.linkedin.com/company/bework s/ ii Executive Summary In 2016, the Ontario Energy Board (OEB), through its Regulated Price Plan (RPP) Pilots, sought to examine the impact of alternative pricing schemes and non-price interventions on conservation and demand management behaviours among utility customers. -

Barrie Power Outage: Alectra Crews Working to Repair Power Lines Damaged by High Winds

For Immediate Release July 15, 2021 Barrie power outage: Alectra crews working to repair power lines damaged by high winds Barrie, ON – A significant weather event including wind gusts and a suspected tornado is impacting power to 2,700 homes and businesses in Barrie today. These strong gusts caused substantial damage to overhead powerlines that supply electricity to parts of Southeast Barrie. Alectra Utilities crews are currently investigating and assessing the damage and will continue to work until all power has been restored. Additional crews have been called in to assist with restoration efforts. Many customers are expected to have power restored overnight, but some customers may be without power until tomorrow afternoon. Alectra is reminding everyone to stay safe: • Areas with trees located near wires should take extra precaution as fallen limbs that contact power lines could cause extended outages in affected areas • In the event of downed power lines, stay at least 10 metres away (the length of a school bus), and call 911 immediately. To report outages, Alectra Utilities’ customers should call 1-833- ALECTRA (1-833-253-2872) Alectra’s System Control Centre continuously monitors weather forecasts and storm models, and mitigation strategies are being made to prepare line crews and additional field and communications staff to respond in the event the situation evolves. If you experience a power outage, you can find frequent updates through our Twitter channel @AlectraNews or by visiting the outage map on our website. Alectra Utilities reminds all customers of the importance of having mobile phones and laptop computers charged and preparing an emergency kit in the event of a sustained power outage.