NSCC Important Notice

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Methodology of Comparison 2013

METHODOLOGY OF COMPARISON 2013 Comparative Analysis of Sustainability Performance Methodological Remarks Convinced that a comparison of environmental, social and governance performance is of interest, not only to the Company itself, but also to its stakeholders, certain comparisons between Terna’s results and those of other com- panies are included in the 2013 Sustainability Report, as was the case in the preceding three years. Listed below are the main criteria adopted in the analysis, as an introduction to the reading and interpretation of the comparisons of individual indicators in the Report: • three panels of companies were identified: an industry panel, composed of the European transmission system operators and the major extra-European operators in terms of kilometres of lines managed; and two multi- industry panels, the first relative to large Italian companies (the 40 companies of the FTSE-MIB at 18 December 2013) and the second relative to the best international performers (the 24 world Sustainability Industry Group Leaders, identified by the RobecoSAM sustainability rating agency and disclosed at the publishing of the Dow Jones Sustainability Index of September 2013). The purpose of the three panels is to guarantee, also relative to the type of indicator reviewed, a comparison between companies with the same operational characteristics, an Italian comparison, and a comparison with the top international performers. The Terna figures do not contribute to the calculation of the average in the case of the RobecoSAM – Supersector Leaders panel; • the companies considered from among those in the three panels were those which publicise the information necessary for comparisons either on their websites, through the Sustainability Report (even if not prepared following the GRI guidelines) or through other documentation (HSE Report, financial report, etc.). -

An Analysis of the Level of Qualitative Efficiency for the Equity Research Reports in the Italian Financial Market

http://ijba.sciedupress.com International Journal of Business Administration Vol. 9, No. 2; 2018 An Analysis of the Level of Qualitative Efficiency for the Equity Research Reports in the Italian Financial Market Paola Fandella1 1 Università Cattolica del Sacro Cuore, Italy Correspondence: Paola Fandella, Università Cattolica del Sacro Cuore, Italy. Received: January 15, 2018 Accepted: February 6, 2018 Online Published: February 8, 2018 doi:10.5430/ijba.v9n2p21 URL: https://doi.org/10.5430/ijba.v9n2p21 Abstract Corporate reports issued by various financial intermediaries play a major role in investment decisions. For this reason, it is particularly interesting to understand the accuracy of the forecasts, by carrying out an empirical analysis of the "equity research" system in Italy, identifying structural features, degree of reliability and incidence in the market. The choice of the analysis of the efficiency level information on the Italian market proposes to assess the interest of equity research of a niche market (339 listed companies in 2017) but with characteristics of potential growth such as having been acquired by LSEGroup in 2007, the 6th stock-exchange group at international level for the number of listed companies and the 4th for capitalization. The analysis was carried out on the reports issued on companies belonging to the Ftse Mib stock index during a period of 5 years. It aims to analyse the composition of the equity research system in Italy as well as the analysts' ability to properly evaluate the stocks' fair price, so as to test their degree of reliability and detect possible anomalies in recommendations to the investors. -

Of the Ftse-Mib Companies

DEPARTMENT OF BUSINESS AND MANAGEMENT DEPARTMENT OF ECONOMICS AND FINANCE MASTER’S DEGREE IN CORPORATE FINANCE INTERLOCKING DIRECTORATES IN ITALY: SOCIAL NETWORK ANALYSIS OF THE FTSE-MIB COMPANIES SUPERVISOR CANDIDATE Prof. Saverio Bozzolan Guido Biagio Sallemi SUPERVISOR Prof. Riccardo Tiscini ACADEMIC YEAR 2018-19 1 2 CONTENTS 1. Introduction ................................................................................................................................... 5 2. The interlocking literature ............................................................................................................ 9 2.1. Theory behind the interlocking directorates .......................................................................... 9 2.2. Relevant cases and findings in SNA Literature................................................................... 11 3. Methodological Section .............................................................................................................. 15 3.1. Social network Analysis ...................................................................................................... 15 3.2. Basic Graphs Taxonomy ..................................................................................................... 16 3.3. Vertex Degree and related metrics ...................................................................................... 19 3.4. Centrality measures ............................................................................................................. 20 3.5. Network Cohesion -

Comparison Methodology

COMPARISON METHODOLOGY Comparative Analysis of Sustainability Performance Convinced that a comparison of environmental, social and governance performance is of interest, not only to the Company itself, but also to its stakeholders, certain comparisons between Terna’s results and those of other companies are included in the 2015 Sustainability Report, as was the case in previous years. The comparative sustainability indicators regard the following themes: CO2 emissions, SF6 leakage incidence rate, hours of training per capita provided to employees and the turnover rate on termination of personnel. Listed below are the main criteria adopted in the analysis, as an introduction to the reading and interpretation of the comparisons of individual indicators in the Report: • three panels of companies were identified: the first was composed of the European transmission system operators and the major non-European operators in terms of kilometres of lines managed; the second, multi-sectoral in nature, is made up of large Italian companies (the 40 listed companies of the FTSE MIB at 31/12/2015); the third formed by the best international performers in the “Electric Utilities - ELC” sector (identified by the RobecoSAM sustainability rating agency and included in the Dow Jones Sustainability World Index of September 2015). The purpose of the three panels is to guarantee, also relative to the type of indicator reviewed, a comparison between companies with the same operational characteristics, an Italian comparison, and a comparison with top international performers in the same sector; • the companies considered from among those in the three panels were those which publicise the information necessary for comparisons either on their websites, through the Sustainability Report (even if not prepared following the GRI guidelines) or through other documentation (HSE Report, Financial Report, etc.). -

Relazione Del Consiglio Di Amministrazione

Report on Corporate Governance and ownership structure pursuant to article 123 bis of Legislative Decree February 24, 1998 no. 58 as amended referring to the year ended December 31, 2020 MARCH 25, 2021 Buzzi Unicem SpA Registered Office: Casale Monferrato (AL) - via Luigi Buzzi n. 6 Share capital: euro 123,636,658.80 fully paid up Chamber of Commerce of Alessandria: 00930290044 Website: www.buzziunicem.com REPORT ON CORPORATE GOVERNANCE AND OWNERSHIP STRUCTURE Introduction This report contains the information on the corporate governance and ownership structure of Buzzi Unicem SpA (“Buzzi Unicem” or “Company”) pursuant to article 123 bis of Legislative Decree February 24, 1988 no. 58 as amended (hereinafter referred to as “TUF”), also in compliance with the Corporate Governance Code of listed companies approved in July 2018 by the Corporate Governance Committee and promoted by Borsa Italiana S.p.A, Ania, Assogestioni, Assonime and Confindustria (“Corporate Governance Code” or “Code”) to which Buzzi Unicem adheres under the terms reported in this report. The above Corporate Governance Code to which Buzzi Unicem adheres is available to the public on the Corporate Governance Committee’s website (https://www.borsaitaliana.it/comitato-corporate-governance/codice/codiceeng2018.en.pdf). During the 2021 financial year, the company will evaluate the implementation of the new Corporate Governance Code approved by the Corporate Governance Committee in January 2020, providing information on the subscription to the Code in the report on corporate governance to be published in 2022. Part I – General description of Buzzi Unicem SpA organizational structure Buzzi Unicem SpA’s organizational structure consists, currently, of the following main corporate bodies: - Shareholders’ meeting; - Board of directors; - Chairman of the board of directors; - two Managing Directors; - Statutory auditors’ committee. -

Introduction of “Split Payment” Regulations for RCC Service Invoices

Market Notice 11 August 2017 MN_61/2017 Introduction of “Split Payment” regulations for RCC service invoices For the attention of: Intermediaries Priority: High Re: Invoicing of RCC charges Dear Client, Please note that following the publication of the Ministry of Economy and Finance Decree of 13 July 2017 in Official Gazette No. 171 of 24 July 2017, which amends the implementing regulations for the splitting of payments for VAT purposes (Article 17-ter, Presidential Decree No. 633/1972) in invoices payable as of 1 July 2017, the RCC fees invoicing application for issuer companies included in the list of listed companies in the FTSE MIB Index published by the Ministry of Economy and Finance (link) must be adapted to the new provisions. The Monte Titoli application is currently in the process of modification and therefore data indicated in the invoicing documentation issued by intermediaries to the issuers concerned (see the list below) in the period 1 July - 10 August is not consistent with the instructions in the Decree. Pending the adaption of the application, and in order to avoid issuing incorrect documents, the invoice request function has been temporarily suspended exclusively for sums due from Issuers to which the aforementioned Decree applies. It should be recalled that the RCC application allows the recovery of sums in suspension without time limits. Monte Titoli shall promptly inform clients by means of Market Notice when the application has been adapted. 1 Market Notice 11 August 2017 MN_61/2017 We apologise for this temporary inconvenience. Our operating offices are available for any clarifications or operating requirements. -

London Stock Exchange's Low Latency Performance Channels Service

News Release 26 November 2012 Borsa Italiana S.p.A. Piazza degli Affari, 6 20123 Milano www.borsaitaliana.it ITALIAN EQUITY ROADSHOW 2012: BORSA ITALIANA COMPANIES IN NORTH AMERICA - Events New York, Boston and Toronto from 26-28 November 2012 - More than 180 meetings planned From 26 to 28 November, Borsa Italiana will host 2012’s North American Italian Equity Roadshow, in which representatives from some of the most well-known listed Italian companies will meet with American and Canadian investors. As well as events in New York and Toronto, this year will also see Boston included on the tour’s schedule for the first time. Management teams from participating Italian firms will attend over 180 meetings with around 80 international investors, from 60 investment houses, confirming Borsa Italiana’s position as a key part of the international financing network. The aim of the meetings is to strengthen relations with American shareholders, who represent about 35 per cent of the institutional investment in leading Italian companies. The meetings are also intended to attract interest from new international investors, to the benefit of Italian companies, financial markets, and Italy’s economy as a whole. Massimiliano Lagreca, Head of Large Caps, Borsa Italiana said: “We are delighted with the high level of participation and interest we have received in our North American Roadshow again this year. Borsa Italiana has always been committed to a strategy which promotes its listed Media Relations: T +39 02 72426.360 F +39 02 72426.260 [email protected] News Release companies on a global stage, and engaging with international investors is crucial, given 90 per cent of institutional investment on the FTSE MIB comes from overseas, and 35 per cent comes from the US. -

FTSE MIB Quarterly Rebalancing Changes 15 March 2021 FTSE MIB

FTSE MIB Quarterly Rebalancing Changes 15 March 2021 FTSE Russell announces the new shares number and Investability Weighting Factors for the FTSE MIB Index effective after the close of business on Friday, 19 March 2021, i.e. on Monday, 22 March 2021. According to the FTSE MIB Ground Rules art. 7.4 and Appendix C, FTSE publishes share in issue & IWF figures updated at the cut-off date, where needed adjusted for capping based on capitalisation calculated with closing prices of five trading days before the rebalancing. The share in issue figure excludes all treasury shares and the Investability Weighting is computed with reference to shares in issue net of treasury shares. The new index divisor will be published after close of business on Friday, 19 March 2021. FTSE MIB Ribilanciamento trimestrale 15 marzo 2021 FTSE Russell comunica il nuovo numero di azioni e i pesi di investibilità per l'Indice FTSE MIB che saranno effettivi dopo la chiusura delle contrattazioni di venerdì 19 marzo 2021 (vale a dire da lunedì 22 marzo 2021). Secondo le Regole di base del FTSE MIB art. 7.4 e l'Appendice C, sono indicati i valori del numero di azioni e peso di investibilità aggiornati alla data del cut-off, eventualmente soggetti alla correzione del capping applicata con riferimento alle capitalizzazioni calcolate con i prezzi di chiusura di cinque giorni di negoziazione prima della data di ribilanciamento. Il numero di azioni esclude tutte le azioni proprie e la percentuale di flottante è calcolata con riferimento al numero di azioni al netto delle azioni proprie. -

FTSE MIB Quarterly Rebalancing Changes 16 September 2019 FTSE

FTSE MIB Quarterly Rebalancing Changes 16 September 2019 FTSE announces the new shares number and Investability Weighting Factors for the FTSE MIB Index effective after the close of business on Friday, 20 September 2019, i.e. on Monday, 23 September 2019. According to the FTSE MIB Ground Rules art. 7.4 and Appendix C, FTSE publishes share in issue & IWF figures updated at the cut-off date, where needed adjusted for capping based on capitalisation calculated with closing prices of five trading days before the rebalancing. The share in issue figure excludes all treasury shares and the Investability Weighting is computed with reference to shares in issue net of treasury shares. The new index divisor will be published after close of business on Friday, 20 September 2019. FTSE MIB Ribilanciamento trimestrale 16 settembre 2019 FTSE comunica il nuovo numero di azioni e i pesi di investibilità per l'Indice FTSE MIB che saranno effettivi dopo la chiusura delle contrattazioni di venerdì 20 settembre 2019 (vale a dire da lunedì 23 settembre 2019). Secondo le Regole di base del FTSE MIB art. 7.4 e l'Appendice C, sono indicati i valori del numero di azioni e peso di investibilità aggiornati alla data del cut-off, eventualmente soggetti alla correzione del capping applicata con riferimento alle capitalizzazioni calcolate con i prezzi di chiusura di cinque giorni di negoziazione prima della data di ribilanciamento. Il numero di azioni esclude tutte le azioni proprie e la percentuale di flottante è calcolata con riferimento al numero di azioni al netto delle azioni proprie. Il nuovo divisor per il FTSE MIB sarà reso disponibile dopo la chiusura delle contrattazioni di venerdì 20 settembre 2019. -

The Effect of Csr Reporting on Stock Prices in European Markets

THE EFFECT OF CSR REPORTING ON STOCK PRICES IN EUROPEAN MARKETS Giorgio Muchacho Dissertation written under the supervision of Ricardo Ferreira Reis Dissertation submitted in partial fulfilment of requirements for the International MSc in Management, at the Universidade Católica Portuguesa, 31/07/2017. 1 The effect of CSR reporting on stock prices in European markets Giorgio Muchacho Prof. Ricardo Ferreira Reis Abstract CSR economic implications have been studied from various points of view. However, we think literature so far has failed to address some issues we aim to study in this research. We focus on the effects of disclosure of sustainability information, which is meant to increase the firm’s level of transparency with stakeholders, reduce information asymmetry and signal the company’s social accountability. There are two issues this thesis strives to understand; the first one is the empirical effect of the initiation of voluntary CSR disclosure on a firm’s market value, as measured by the stock price. The second issue is the hypothesis that CSR information can be used as a tool to greenwash financial information. Our findings suggest that CSR disclosure per se is not sufficient to raise a firm’s stock price, and that companies do not intentionally use CSR for greenwashing. Resumo As implicações económicas da responsabilidade social das empresas foram estudadas de diversos pontos de vista. Contudo, consideramos que a literature não foi capaz abordar algunas questões que queremos analisar nesta investigação. Vamos concentrar-nos nos efeitos da divulgação de informações sobre a sustentabilidade, que destina-se a aumentar o nível de transparência com os stakeholders, a reduzir a assimetria da informação e a sinalizar a responsibilidade social da empresa. -

Transition Effects from the Initial Adoption of IFRS 9 by Italian and German Blue Chip Companies

Journal of Modern Accounting and Auditing, November 2020, Vol. 16, No.11, 467-483 doi: 10.17265/1548-6583/2020.11.001 D DAVID PUBLISHING Transition Effects from the Initial Adoption of IFRS 9 by Italian and German Blue Chip Companies Knut Henkel University of Applied Sciences, Emden/Leer, Emden, Germany Marvin Bürger NORD/LB Norddeutsche Landesbank - Girozentrale -, Hanover, Germany For the financial years from 2018, the new standard for accounting of financial instruments, IFRS 9, was applicable for the first time. Various questions arose in connection with the transition. For example, how high would the resulting transition effect be on equity? Another aspect related to the question of the extent to which the fair value measurement (through profit or loss) would increase. It is also of interest whether the previously presented IFRS 9 changes are classifiable as being material. Through the analysis of the financial statements of FTSE MIB and DAX 30 companies that were prepared for the first time in accordance with IFRS 9 in the year 2018, answers are given in this article to the aforementioned questions and a comparison is made regarding the extent to which national differences or commonalities existed. In the overall view of the absolute change in equity, for the FTSE MIB companies, a mean value of € - 3.03 million was calculated and for the DAX 30 companies, € - 34.29 million. The equity ratio (median), however, only declined marginally in percentage points with the FTSE MIB companies (-0.07), as well as with the DAX 30 companies (-0.02). With regard to the migration of financial assets, it has been shown that the accounting and measurement of more than 90% of financial assets of the FTSE MIB and DAX 30 companies have not changed. -

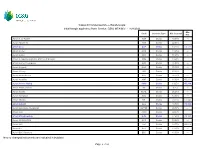

Cassa Di Compensazione E Garanzia Spa Initial Margin Applied to Share Section GEM, MTA/MIV - 16/8/2021 Min

Cassa di Compensazione e Garanzia spa Initial Margin applied to Share Section GEM, MTA/MIV - 16/8/2021 Min. Code Contract Type Mar. Interval Mar. Azioni A. S. ROMA ASR Stocks 49.00% --- Azioni Abitare IN ABT Stocks 22.00% --- Azioni Acea ACE Stocks 13.25% €0.122 Azioni Acotel ACO Stocks 41.25% --- Azioni Aedes AED Stocks 51.25% --- Azioni Aeroporto Guglielmo Marconi di Bologna ADB Stocks 18.25% --- Azioni Alerion Cleanpower ARN Stocks 25.00% --- Azioni Algowatt ALW Stocks 30.75% --- Azioni Alkemy ALK Stocks 25.00% --- Azioni Ambienthesis ATH Stocks 26.75% --- Azioni Amplifon AMP Stocks 13.00% €0.260 Azioni Anima Holding ANIM Stocks 19.25% €0.038 Azioni Antares Vision AV Stocks 9.25% --- Azioni Aquafil ECNL Stocks 26.25% --- Azioni Ascopiave ASC Stocks 13.00% --- Azioni Atlantia ATL Stocks 23.75% €0.146 Azioni Autogrill AGL Stocks 33.50% €0.082 Azioni Autostrade Meridionali AUTME Stocks 26.50% --- Azioni Avio AVIO Stocks 22.50% --- Azioni Azimut Holding AZM Stocks 17.50% €0.182 Azioni ACSM AGAM ACS Stocks 19.00% --- Azioni A2A A2A Stocks 14.75% €0.012 Azioni B.F. BFG Stocks 13.50% --- Azioni B&C Speakers BEC Stocks 13.00% --- New or changed instruments are indicated in boldface Page 1 of 16 Cassa di Compensazione e Garanzia spa Initial Margin applied to Share Section GEM, MTA/MIV - 16/8/2021 Min. Code Contract Type Mar. Interval Mar. Azioni Banca Carige CRG Stocks 97.50% --- Azioni Banca Carige Rnc CRGR Stocks 96.50% --- Azioni Banca Farmafactoring BFF Stocks 17.25% --- Azioni Banca Finnat BFE Stocks 16.75% --- Azioni Banca Generali BGN