Glasgow Commonwealth Games

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2011 Annual Report

NEW ZEALAND OLYMPIC COMMITTEE 2011 100TH ANNUAL REPORT CONTENTS EXECUTIVE REPORTS President’s Report 2 Secretary General’s Report 4 GAMES REPORTS Games Time Planning 8 Commonwealth Youth Games – Isle of Man 9 PROMOTING THE OLYMPIC MOVEMENT Commercial and Marketing Activity 10 Events and Celebrations 14 Museum and Education 16 Athletes’ Commission 18 FINANCIAL REPORTS New Zealand Olympic Committee Financial Report 19 New Zealand Olympic Academy Financial Report 33 IOC and Olympic Solidarity Funding 40 New Zealand Olympic Committee Executive and Staff Lists 43 1 NEW ZEALAND OLYMPIC CoMMITTEE 2011 100TH ANNUAL REPORT PRESIDENt’s REPORT IN 2011 THE NEW ZEALAND Our relationships within the Olympic Movement have The ‘Making us Proud’ marketing campaign was OLYMPIC CoMMITTEE (NZOC) the potential to provide commercial as well as sporting launched in 2011 and has provided commercial partners CELEBRATED ITS CENTENARY AND benefits to New Zealand. Our international position with opportunities for returns on objectives as well was strengthened when it was confirmed that Barbara as ways for New Zealanders to be proud and inspire RECOGNISED THE CONTRIBUTION Kendall would again serve on the IOC. our Olympic team. The establishment of the NZOC’s OF THOSE WHO THROUGHOUT As part of the review of its constitution the NZOC will, President’s Council, which draws on the expertise THE DECADES HAVE WORKED for the first time, go to the public for applications for of some of New Zealand’s leading business and TIRELESSLY TO PROMOTE THE upcoming board positions. This will enable us to source community leaders, is an initiative to further strengthen OLYMPIC MOVEMENT IN NEW the very best candidates to steer our organisation into our financial position. -

World Record to Eileen Cikamatana Oceania

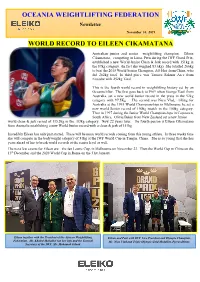

OCEANIA WEIGHTLIFTING FEDERATION Newsletter November 14, 2019 WORLD RECORD TO EILEEN CIKAMATANA Australian junior and senior weightlifting champion, Eileen Cikamatana, competing in Lima, Peru during the IWF Grand Prix, established a new World Junior Clean & Jerk record with 151kg in the 87kg category. (In fact she weighed 83.6kg) She totalled 266kg to beat the 2018 World Senior Champion, AO Hui from China, who did 262kg total. In third place was Tamara Salazar Arce from Ecuador with 252kg Total. This is the fourth world record in weightlifting history set by an Oceania lifter. The first goes back to 1969 when George Vasil from Australia, set a new world Junior record in the press in the 52kg category with 97.5Kg . The second was Nicu Vlad, lifting for Australia at the 1993 World Championships in Melbourne he set a new world Senior record of 190kg snatch in the 100kg category. Then in 1997 during the Junior World Championships in Capetown, South Africa, Olivia Baker from New Zealand set a new Junior world clean & jerk record of 115.5kg in the +83kg category. Now 22 years later, the fourth person is Eileen Cikamatana from Australia establishing a new World Junior record with a clean & jerk of 151kg. Incredibly Eileen has only just started. There will be more world records coming from this young athlete. In three weeks time she will compete in the bodyweight category of 81kg at the IWF World Cup in Tianjin, China. She is so young that she has years ahead of her to break world records at the senior level as well. -

Commonwealth Games INTRODUCTION the Next Commonwealth Games Are Going to Be Held in 2010 in New Delhi, the Capital of Our Country

Yuva for All Session 3.11 TITLE : Looking forward to the Commonwealth Games INTRODUCTION The next Commonwealth Games are going to be held in 2010 in New Delhi, the capital of our country. This session ai ms at preparing students to be good hosts and volunteers during the Games. It aims at enhancing life skills such as Self Awareness, Creative and Critical Thinking, Empathy, Effective Communication and improving Inter-Personal Relationships with people from other countries. 1. Objectives : By the end of the session, the students will be able to Become aware about the Commonwealth and Commonwealth Games. Become aware about the importance of events such as the Commonwealth Games. Understand the importance of extending warmth, hospitality and cooperation to the guests from other countries who visit Delhi in relation with the Games. 2. Time : 70 Minutes (Two continuous periods) 3. Life Skills Being Used : Effective Communication, Decision Making, Empathy, Problem Solving, Critical Thinking 4. Advance Preparations : None 5. Linkages : Please see Contents 6. Methodology : Group Discussion, Role play 7. Process : Step 1: Please read the Fact Sheet carefully, and go through this session well in advance before you carry it out with the students. YUVA Help Line No. 1800116888 1 Step 2: Greet the class and state that we all know that Delhi is going to host the Commonwealth Games in 2010. All agencies are working fulltime to prepare for the Games. The roads are being widened, and venues for the games are being spruced up. A whole new setup for the stay of the athletes –the “Commonwealth Games Village” - is coming up near the Akshardham temple. -

2016 Owf Annual Report

2016 OWF ANNUAL REPORT Eileen Cikamatana - Fiji Ele Opeloge - Samoa Kiana Elliott - Australia Oceania Weightlifting Federation PB 333, Noumea Cedex 98845 NEW CALEDONIA Telephone: +687 467640 or +687 948756 • Mobile: +61 457 778900 Email: [email protected] or [email protected] Website: www.oceaniaweightlifting.com OCEANIA WEIGHTLIFTING FEDERATION 2016 ANNUAL REPORT PREAMBLE What a year 2016 was for the OWF. After eight long years of waiting, Ele Opeloge was awarded the silver medal which she rightfully deserved from the 2008 Beijing Olympic Games. The first World Youth Champion from the region was Eileen Cikamatana from Fiji winning gold in the 69kg in the clean & jerk in Penang. Silver medal went to Kiana Elliot from Australia with a world class performance at the World Junior Championships in Georgia – our 15 lifters from 11 countries did a great job at the Rio Olympic Games. The performance in Rio by our two 62kg category lifters – Morea Baru from PNG and Nevo Ioane from Samoa – was brilliant. These are only some of the achievements of the OWF during 2016: The magnificent technical seminar held in Suva, upgraded 16 technical officials from the Pacific Islands to international category two level. The outstanding Oceania Championships and Olympic Qualification event was held in Suva, Fiji. And also the extraordinarily successful OTIP program and subsequent OTIP training camp in New Caledonia. It gives us immense pride and satisfaction in highlighting the OWF achievements for this year: FEBRUARY 2016 – EMAIL PACIFIC ISLANDS TOURNAMENT The 2016 Pacific Islands Email tournament turned out to be another great success. This tournament is producing some excellent results every year and it is good for the island nations as it kick starts their year of competition. -

Olympic Weightlifting

Olympic Weightlifting Olympic weightlifting, or weightlifting, is an athletic discipline in the modern Olympic programme in which the athlete attempts a maximum-weight single lift of a barbell loaded with weight plates. Qualifying – the road to Rio Qualification is based on the results of the 2014 and 2015 International Weightlifting Federation (IWF) World Championships and the 2016 Continental Championships. No more than six men and four women can qualify per country, with a maximum of two athletes per event. Brazil, as host country, is guaranteed five quota places, three for men and two for women. No New Zealand weightlifters have qualified for Rio as yet. The best chance for qualification for our weightlifters is via the Oceania qualifying event being held in Fiji in early 2016. At this event qualifying is based on team results, not individuals. Teams must place in the top three for women to gain one Olympic spot, and men must place in the top four to gain a spot. A women’s team has seven members and a men’s team has eight. If the New Zealand teams are successful at this qualification event in gaining places at the Rio Games, then our selectors will choose one male weightlifter and one female weightlifter to go (in agreement with the NZOC). Rio 2016 Weightlifting When: Competition will take place over 10 days from 7-14 August 2016 (with no competition on 15 August). Where: Riocentro – Pavilion 2. Men will compete in eight events based on athlete weight categories, from under 56kg to the super- heavyweights at over 105kg. -

Australian Olympians 2014

AUSTRALIAN OLYMPIANS 2014 - THIS ISSUE - SOCHI 2014 / NANJING 2014 / ROAD TO RIO CHAMPIONS OF THE WORLD / ATHLETE TRANSITION / REUNIONS NOW Australian Olympians — 2014 FINDING SOMETHING THAT MORE Australian Olympians — 2014 16 HALL OF FAME Australian Olympians were celebrated and recognised at the Annual Sport Australia Hall of Fame awards. 10 JOHN COATES AC CHAMPIONS OF THE WORLD President, Australian Olympic Committee Australian Olympians triumph taking on the world’s best. Vice President, International Olympic Committee 32 The greatest honour in sport is to be called an Australian Olympian. This year we have seen a number of reunions take place celebrating significant milestones of ROAD TO RIO Olympic Games. Whether you are still competing or retired, I encourage you to keep sharing the Olympic spirit amongst your Team mates and in your communities. In 2016, Rio de Janeiro will host the XXXI Olympic Games and they I was most pleased to see the competitive drive and camaraderie amongst our 60 promise to be spectacular. Olympians in Sochi, where for the first time in Australia’s Olympic history we saw 43 more women (31) than men (29) competing. Congratulations to all Olympians for your collective effort and outstanding results. INSIDE Contributing to a At the Youth Olympic Games in Nanjing, China, the spirit exhibited by the 89 Youth better world Olympians in our Australian Team epitomised what the Olympic Movement strives for. 23 through sport In November 2014 the AOC Executive resolved to recognise our Australian Indigenous heritage in the AOC’s Constitution. I was delighted to announce this with Cathy SOCHI 2014 Freeman and I look forward to the AOC offering practical support to Indigenous Australians through sport in the years to come. -

Glasgow Wins the Race! How the Bid Was Won | What Comes Next | Pune Update

ISSUE 8 WINTER 2007/2008 Glasgow wins the race! How the bid was won | What comes next | Pune update THE COMMONWEALTH GAMES COUNCIL FOR SCOTLAND NEWSLETTER The magic monent Message from the Queen I send my warm congratulations to everyone involved in Glasgow’s successful bid to hold the 2014 Commonwealth Games: the third time that a Scottish city has been chosen as the venue for the Games. My good wishes go to you all, and to the people of Glasgow, as you celebrate this impressive achievement. Glasgow wins race for 2014 Games ELIZABETH R. “The host for the 2014 Commonwealth Games will be Glasgow!” These were the words of Mike Fennell, the Scottish Athletes’ Commission. The For the presentation party and the Chairman of the Commonwealth Games Commission played a key role in many Glasgow 2014 delegation, who had been Federation and the ones which hundreds aspects of the Bid plans including the allowed to squeeze into the back of the of thousands of Scots who had given village and venues and they took an room for the voting, it was a very long their backing to the Bid were waiting to active part in both the outward and eight minutes whilst the votes were hear. inward visits. Jamie had delegates counted. When the moment finally captivated as he recalled his own athlete arrived it was announced that Glasgow After a tense but exciting week in story and the importance of the support had beaten Abuja by 47 votes to 24 with Colombo for the Bid Team and its of family and friends when achieving the all 71 countries taking part in the vote. -

Impacts of the Commonwealth Games 2014 on Young People in the East End of Glasgow

Briefing Paper 27 GoWell is a collaborative partnership between the Glasgow Centre for Population Health, and Urban Studies and the MRC/CSO Social and Public Health Sciences Unit at the University of Glasgow, sponsored by Glasgow Housing Association, the Scottish Government, NHS Health Scotland and NHS Greater Glasgow and Clyde. Impacts of the Commonwealth Games 2014 on young people in the East End of Glasgow October 2016 GoWell is a planned ten-year research and learning programme that aims to investigate the impact of investment in housing, regeneration and neighbourhood renewal on the health and wellbeing of individuals, families and communities. It commenced in February 2006 and has several research components. This paper is part of a series of Briefing Papers which the GoWell team has developed in order to summarise key findings and policy and practice recommendations from the research. Further information on the GoWell Programme and the full series of Briefing Papers is available from the GoWell website at: www.gowellonline.com INTRODUCTIONKey findings • A longitudinal qualitative study was undertaken with young people living in the Glasgow 2014 Commonwealth Games (CWG) core hosting zone to examine legacy impacts with regard to changes in their social and spatial horizons up to one year after the Games. Expanded horizons is associated with altered aspirations and improved life chances for young people. • Drawing on official legacy documentation and known legacy projects, a hypothetical Logic Model identified four mechanisms considered most likely to impact on young people’s horizons: Place Transformation; Education & Learning; Engagement & Participation; and Inspiration. • Of these, place transformation was the most salient, with recent physical changes viewed positively by young people and directly attributed to the CWG. -

Coaching Conference 2015 Coaching

COACHING CONFERENCE 2015 EMIRATES ARENA, GLASGOW 26 & 27 SEPT 2015 COACHING CONFERENCE 26 & 27 September 2015 SATURDAY 26 SEPTEMBER 2015 TIME DETAILS LOCATION 09:00 Registration and Tea & Coffee 09:30 - 09:45 Welcome and Introduction to weekend: Rodger Harkins / Mark Munro Sports Hall 09:45 - 10:45 Keynote 1: Boo Schexnayder - COACHING PLAYGROUND TO PODIUM - Sports Hall Lessons learned through my coaching journey 10:45 - 11:00 Comfort Break Sports Hall 11:00 - 12.30 Breakout 1 BREAKOUT 1 CHOICE Practical Workshops 1) Vesteinn Hafsteinsson - Conditioning for Throws Seminar 2) Jonas Tawiah - Dodoo - My Philosophy on Coaching Speed Sports Hall 3) Mick Woods - Developing an Endurance Powerhouse Club NGB Room 1 4) Susan Moncrieff - My Approach to Coaching through my Lessons as an Athlete NGB Room 2 12:30 - 13:30 Lunch Sports Hall 13:30 - 15.00 Breakout 2 BREAKOUT 2 CHOICE Practical Workshops 5) Vesteinn Hafsteinsson - Coaching the Discus 6) Mike McNeill - Competencies for Throwing Javelin 7) Jared Deacon - Practical Application of Speed Drills for the Club Coach 8) Boo Schexnayder - Plyometric Conditioning for the Power Athlete Seminar 9) Pierre-Jean Vazel - My Approach to Successfully Coaching Athletes from Youth NGB Room 1 through to Senior Level 10) Ron Morrison & Don Macgregor - Planning for the Marathon NGBRoom2 15:00 - 15:30 Refreshment Break Sports Hall 15:30 - 17.00 Breakout 3 BREAKOUT 3 CHOICE Practical Workshops 11) Jonas Tawiah - Dodoo - Sprinting Attractors for Acceleration and High Speed Running 12) Mick Jones - Hammer Coaching -

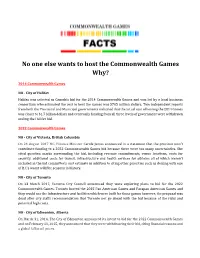

No One Else Wants to Host the Commonwealth Games Why?

No one else wants to host the Commonwealth Games Why? 2014 Commonwealth Games NO - City of Halifax Halifax was selected as Canada’s bid for the 2014 Commonwealth Games and was led by a local business consortium who estimated the cost to host the Games was $785 million dollars. Two independent reports from both the Provincial and Municipal governments indicated that the actual cost of hosting the 2014 Games was closer to $1.7 billion dollars and eventually funding from all three levels of government were withdrawn ending the Halifax bid. 2022 Commonwealth Games NO - City of Victoria, British Columbia On 24 August 2017 B.C. Finance Minister Carole James announced in a statement that the province won't contribute funding to a 2022 Commonwealth Games bid because there were too many uncertainties. She cited question marks surrounding the bid, including revenue commitments, venue locations, costs for security, additional costs for transit, infrastructure and health services for athletes all of which weren’t included in the bid committee’s cost estimate in addition to citing other priorities such as dealing with one of B.C’s worst wildfire seasons in history. NO - City of Toronto On 23 March 2017, Toronto City Council announced they were exploring plans to bid for the 2022 Commonwealth Games. Toronto hosted the 2015 Pan American Games and Parapan American Games and they would use the infrastructure and facilities which were built for those games however, the proposal was dead after city staffs recommendation that Toronto not go ahead with the bid because of the risks and potential high costs. -

2014 Commonwealth Games Statistics – Women's 400M

2014 Commonwealth Games Statistics – Women’s 400m (440y before 1970) All time performance list at the Commonwealth Games Performance Performer Time Name Nat Pos Venue Year 1 1 50.10 Amantle Montsho BOT 1 Delhi 2010 2 2 50.17 Sandie Richards JAM 1 Kuala Lumpur 1998 3 3 50.28 Christine Ohuruogu ENG 1 Melbourne 2006 4 4 50.38 Cathy Freeman AUS 1 Victoria 1994 5 5 50.53 Fatima Yusuf NGR 2 Victoria 1994 6 50.65 Sandie Richards 1sf2 Kuala Lumpur 1998 7 50.69 Sandie Richards 3 Victoria 1994 8 6 50.71 Allison Curbishley SCO 2 Kuala Lumpur 1998 9 7 50.76 Tonique Williams-Darling BAH 2 Melbourne 2006 10 50.80 Amantle Montsho 1sf1 Delhi 2010 11 8 50.85 Donna Fraser ENG 2sf2 Kuala Lumpur 1998 12 50.87 Christine Ohuruogu 1sf3 Melbourne 2006 13 50.97 Tonique Williams-Darling 2sf3 Melbourne 2006 14 51.01 Donna Fraser 3 Kuala Lumpur 1998 15 9 51.02 Marilyn Neufville JAM 1 Edinburgh 1970 16 10 51.03 Novlene Williams JAM 1sf1 Melbourne 2006 17 11 51.06 Damayanthi Darsha SRI 4 Kuala Lumpur 1998 18 51.08 Fatima Yusuf 1 Auckland 1990 19 12 51.12 Charity Opara NGR 1h2 Auckland 1990 19 51.12 Novlene Williams 3 Melbourne 2006 21 51.23 Sandie Richards 1sf1 Victoria 1994 22 13 51.26 Raelene Boyle AUS 1 Brisbane 1982 23 14 51.29 Debbie Flintoff-King AUS 1 Edinburgh 1986 23 14 51.29 Lee McConnell SCO 1sf2 Manchester 2002 25 16 51.34 Aliann Pompey GUY 2sf2 Manchester 2002 26 17 51.36 Catherine Murphy WAL 3sf2 Manchester 2002 26 17 51.36 Christine Amertil BAH 1sf2 Melbourne 2006 28 51.38 Christine Amertil 1sf1 Manchester 2002 29 19 51.40 June Griffith GUY 1sf1 Edmonton -

Glasgow 2014 Commonwealth Games Case Study

Glasgow 2014 Commonwealth Games Case Study The 2014 Commonwealth Games in Glasgow was held from 23 July to 3 August and was the largest multi-sport event ever held in Scotland. Around 4,950 athletes from 71 different nations and territories competed in 18 different sports across seven sites. In a joint venture with Field & Lawn Limited, GL events UK became Official Overlay and Temporary Structures Provider to build temporary structures at seven venues in Glasgow including at the Commonwealth Games Village that spanned 25.2sqkm. With seven sites across the city the challenge for this project was to complete the build not only in time for the start of the games but also without causing too much disruption across the city. With a team of forty-one on site, the build had to be completed on the 5th July 2014 allowing seventeen days before the start of the summer sporting event on the 23rd July, 2014. GL events UK created over 33,000 square metres of space created at seven Games venues including the Emirates Arena and adjoining Sir Chris Hoy Velodrome, Tollcross International Swimming Centre and a temporary squash showcourt at Scotstoun Sports Campus, complete with a 2,400-seater grandstand. This included responsibility for the Polyclinic enclosure in the Athletes’ Village, operating 24 hours a day and providing medical services from emergency dental care to physiotherapy and sports massage services to athletes and team officials throughout the Games. GL events UK also created a temporary outdoor broadcast suite for the regional reporters covering the Glasgow 2014 Commonwealth Games.