Lancashire Holdings Limited 2010 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UNIVERSITY of CENTRAL LANCA S HIRE PARTNERSHIP POLICING

UNIVERSITY oF CENTRAL LANCA S HIRE PARTNERSHIP POLICING BY PC 970 IAIN ASHER UNIVERSITY POLICE OFFICER PRESTON POLICE STATION LAWSON STREET PRESTON LANCASHIRE PR1 2RJ TEL: 01772 209157 FAX: 01772 209146 Lancashire Constabuary Summary Title. University of Central Lancashire Partnership Policing. The University of Central Lancashire is located within Central Division close to the centre of Preston, Lancashire. In 1997, the Division moved towards a geographic style of policing and I took ownership of the policing problems of the University. It was apparent that the main volume crime issues facing the area were crimes against property. This was a problem which affected both students and the university organisation_ Scanning and analysis quickly indicated that a large proportion of these crimes could t have been avoided had basic security and crime prevention measures been adhered to. The issue was, therefore, largely one of education. Education of the community to prevent students and staff becoming victims of crime and education of the University organisation to help it to improve the way in which it addressed its crime problems. The University is an autonomous organisation which can resemble a distinct community. It has its own physical boundaries, hierarchy, discipline structure and policing systems. As an organisation they had many of the resources and structures to deal with their crime problems, but needed help to work more efficiently. The response to the problem was, therefore, to develop partnerships within the University to help them to address their crime problems. This approach was beneficial to the police as it has a positive influence not only on crime figures, but also on demands upon police time. -

Lancashire Historic Town Survey Programme

LANCASHIRE HISTORIC TOWN SURVEY PROGRAMME BURNLEY HISTORIC TOWN ASSESSMENT REPORT MAY 2005 Lancashire County Council and Egerton Lea Consultancy with the support of English Heritage and Burnley Borough Council Lancashire Historic Town Survey Burnley The Lancashire Historic Town Survey Programme was carried out between 2000 and 2006 by Lancashire County Council and Egerton Lea Consultancy with the support of English Heritage. This document has been prepared by Lesley Mitchell and Suzanne Hartley of the Lancashire County Archaeology Service, and is based on an original report written by Richard Newman and Caron Newman, who undertook the documentary research and field study. The illustrations were prepared and processed by Caron Newman, Lesley Mitchell, Suzanne Hartley, Nik Bruce and Peter Iles. Copyright © Lancashire County Council 2005 Contact: Lancashire County Archaeology Service Environment Directorate Lancashire County Council Guild House Cross Street Preston PR1 8RD Mapping in this volume is based upon the Ordnance Survey mapping with the permission of the Controller of Her Majesty’s Stationery Office. © Crown copyright. Unauthorised reproduction infringes Crown copyright and may lead to prosecution or civil proceedings. Lancashire County Council Licence No. 100023320 ACKNOWLEDGEMENTS Lancashire County Council would like to acknowledge the advice and assistance provided by Graham Fairclough, Jennie Stopford, Andrew Davison, Roger Thomas, Judith Nelson and Darren Ratcliffe at English Heritage, Paul Mason, John Trippier, and all the staff at Lancashire County Council, in particular Nik Bruce, Jenny Hayward, Jo Clark, Peter Iles, Peter McCrone and Lynda Sutton. Egerton Lea Consultancy Ltd wishes to thank the staff of the Lancashire Record Office, particularly Sue Goodwin, for all their assistance during the course of this study. -

Preston, Lancashire, UK PR1 2HE Tel: +44

ATM Barrier controlled road ATM BikeBarrier Hub controlled road 123 Bus number Bike Hub For up-to-date bus time and route information 123 BusBus routesnumber see stagecoachbus.com Forand up-to-date prestonbus.co.uk bus time and route information BusBus stopsroutes see stagecoachbus.com and prestonbus.co.uk DP CycleBus stops compounds / lockers DP CycleCycle rackscompounds / lockers DC DentalCycle racks Clinic UCLan Sports Arena 125 N 40 DC - by bus V DP Dental Clinic UCLan Sports Arena DP 41125 Disabled parking N 40 - by bus V DP DP Disabled parking 23 41 WC Disabled toilets 23 WC Disabled toilets eat@UCLan eat@UCLan Ri Electric vehicle charging point Ri Electric vehicle charging point PC Entrance to buildings WC DP Hawkins Street PC Entrance to buildings WC DP Hawkins Street DP ER WC EC Eye Clinic HW Dw DP WC ER EC HW Dw Eye Clinic IW WC Gender neutral toilets IWGordon Street WC Gender neutral toilets WC DP V WC Gordon Street V S 31 DP DP SC Hearing loop 24 S V Greenbank Street 31 DrDP SC V Hearing loop 44 24 WC Greenbank Street Dr EC WC 44 WC EC WC Mailroom WC WC DP DP WC DP Mailroom 9 DP WC 9 V V DC DC MainMain receptionreception DP Victoria Street DP DP 26Victoria Street26 DP WrWr MC Medical Centre DP DP MC Medical Centre UCLan SportsUCLan Arena Sports & Arena & Westleigh - byWestleigh car (2 miles) - by car (2 miles) Pn MotorcycleMotorcycle shelters (covered)(covered) Pn DP V V DP WC WC DP DP ParentingParenting room 53º 53º PHPH Pharmacy WC Pharmacy WC DP DP WC WC WC WC V WC PC Physiotherapy Clinic V WC PC Physiotherapy Clinic DP -

Code of Practice CCTV Blackburn with Darwen Borough Council And

Code of Practice CCTV of Blackburn with Darwen Borough Council and Pennine Lancashire CCTV Hub 3 May 2019 1 Certificate of Agreement The contents of this Code of Practice are hereby approved by the signatories on behalf of Blackburn with Darwen Borough Council, Preston City Council, Burnley Borough Council, Hyndburn Borough Council, Pendle Borough Council and Rossendale Borough Council. The Code will be followed by Blackburn with Darwen Council in its management and operation of the Hub and, where applicable, by the signatories. By signing this document the organisations below accept and will adopt the statements included in this Code of Practice and agree to maintain the specified standards where applicable. The principles in this Code are also applicable to Blackburn Borough Council’s ‘Other Cameras’ as defined within the Code. The terms of the Code are also agreed and signed by Lancashire Constabulary as regular users of the information gathered by the Hub. Signed for and on behalf of: Blackburn with Darwen Borough Council of [insert address]: Signature……………………………………… Name………………………………………. Position Held …………………………………………………………………………………. Dated the………………………………………day of………………………………….201 Signed for and on behalf of: Preston City Council of Town Hall, Preston, PR1 2RL: Signature……………………………………… Name………………………………………. Position Held …………………………………………………………………………………. Dated the………………………………………day of………………………………….201 Signed for and on behalf of: Burnley Borough Council of Parker Lane Offices, Burnley BB11 2BY: Signature……………………………………… Name………………………………………. Position Held …………………………………………………………………………………. Dated the………………………………………day of………………………………….201 2 Signed below for and on behalf of: Hyndburn Borough Council of Scaitcliffe House, Ormerod Street. Accrington BB5 OPF Signature……………………………………… Name………………………………………. Position Held …………………………………………………………………………………. Dated the………………………………………day of………………………………….201 Signed below for and on behalf of: Pendle Borough Council of Market Street, Nelson, BB9 7LG Signature……………………………………… Name………………………………………. -

Investor Presentation

Investor Presentation www.lancashiregroup.com Safe harbour statements NOTE REGARDING FORWARD-LOOKING STATEMENTS: CERTAIN STATEMENTS AND INDICATIVE PROJECTIONS (WHICH MAY INCLUDE MODELLED LOSS SCENARIOS) MADE IN THIS RELEASE OR OTHERWISE THAT ARE NOT BASED ON CURRENT OR HISTORICAL FACTS ARE FORWARD-LOOKING IN NATURE INCLUDING, WITHOUT LIMITATION, STATEMENTS CONTAINING THE WORDS “BELIEVES”, “ANTICIPATES”, “PLANS”, “PROJECTS”, “FORECASTS”, “GUIDANCE”, “INTENDS”, “EXPECTS”, “ESTIMATES”, “PREDICTS”, “MAY”, “CAN”, “LIKELY”, “WILL”, “SEEKS”, “SHOULD”, OR, IN EACH CASE, THEIR NEGATIVE OR COMPARABLE TERMINOLOGY. ALL SUCH STATEMENTS OTHER THAN STATEMENTS OF HISTORICAL FACTS INCLUDING, WITHOUT LIMITATION, THE FINANCIAL POSITION OF THE COMPANY AND ITS SUBSIDIARIES (THE “GROUP”), THE GROUP’S TAX RESIDENCY, LIQUIDITY, RESULTS OF OPERATIONS, PROSPECTS, GROWTH, CAPITAL MANAGEMENT PLANS AND EFFICIENCIES, ABILITY TO CREATE VALUE, DIVIDEND POLICY, OPERATIONAL FLEXIBILITY, COMPOSITION OF MANAGEMENT, BUSINESS STRATEGY, PLANS AND OBJECTIVES OF MANAGEMENT FOR FUTURE OPERATIONS (INCLUDING DEVELOPMENT PLANS AND OBJECTIVES RELATING TO THE GROUP’S INSURANCE BUSINESS) ARE FORWARD-LOOKING STATEMENTS. SUCH FORWARD-LOOKING STATEMENTS INVOLVE KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER IMPORTANT FACTORS THAT COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE GROUP TO BE MATERIALLY DIFFERENT FROM FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. THESE FACTORS INCLUDE, BUT ARE NOT LIMITED TO: THE ACTUAL -

Close Brothers Group Plc (Incorporated with Limited Liability in England and Wales with Registered Number 00520241)

PROSPECTUS DATED 8 JUNE 2021 Close Brothers Group plc (incorporated with limited liability in England and Wales with registered number 00520241) £200,000,000 2.00% Subordinated Tier 2 Notes Issue price: 99.531 per cent. The £200,000,000 2.00% Subordinated Tier 2 Notes (the “Notes”) will be issued by Close Brothers Group plc (the “Issuer”) on or about 11 June 2021 (the “Issue Date”). The terms and conditions of the Notes are set out herein in “Terms and Conditions of the Notes” below (the “Conditions”, and references to a numbered “Condition” shall be construed accordingly). The Notes will bear interest on their outstanding principal amount from (and including) the Issue Date to (but excluding) 11 September 2026 (the “Reset Date”), at a rate of 2.00 per cent. per annum and thereafter at the Reset Interest Rate as provided in Condition 5. Interest will be payable on the Notes semi-annually in arrear on each Interest Payment Date, commencing on 11 September 2021 (with a short first Interest Period from (and including) the Issue Date to (but excluding) 11 September 2021). Unless previously redeemed or purchased and cancelled, or (pursuant to Condition 7(f)) substituted, the Notes will mature on 11 September 2031 and shall be redeemed at their principal amount, together with any accrued and unpaid interest on such date. The Noteholders will have no right to require the Issuer to redeem or purchase the Notes at any time. The Issuer may, in its discretion but subject to Regulatory Approval, elect to (a) redeem all (but not some only) of the -

FTSE Factsheet

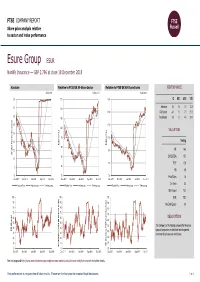

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 18 December 2018 Esure Group ESUR Nonlife Insurance — GBP 2.796 at close 18 December 2018 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 18-Dec-2018 18-Dec-2018 18-Dec-2018 2.8 115 130 1D WTD MTD YTD Absolute 0.0 0.0 0.1 12.5 2.7 110 120 Rel.Sector -0.1 1.0 7.1 21.2 2.6 105 Rel.Market 0.8 1.9 4.5 29.7 2.5 110 100 VALUATION 2.4 (local currency) (local 95 100 2.3 Trailing Relative Price Relative Price 90 2.2 90 PE 14.6 Absolute Price Price Absolute 85 EV/EBITDA 10.7 2.1 80 PCF 12.8 2 80 PB 3.9 1.9 75 70 Price/Sales 1.5 Dec-2017 Mar-2018 Jun-2018 Sep-2018 Dec-2018 Dec-2017 Mar-2018 Jun-2018 Sep-2018 Dec-2018 Dec-2017 Mar-2018 Jun-2018 Sep-2018 Dec-2018 Div Yield 3.4 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Div Payout 70.1 100 100 100 ROE 28.2 90 90 90 Net Debt/Equity 0.4 80 80 80 70 70 70 60 60 DESCRIPTION 60 50 50 50 The Company is the holding company for the esure 40 40 RSI (Absolute) RSI 40 group of companies, established to write general 30 30 insurance for private cars and homes. -

Investor Presentation H1 2021 Update Safe Harbor Statements

Investor Presentation H1 2021 Update www.lancashiregroup.com Safe harbor statements NOTE REGARDING FORWARD-LOOKING STATEMENTS: CERTAIN STATEMENTS AND INDICATIVE PROJECTIONS (WHICH MAY INCLUDE MODELLED LOSS SCENARIOS) MADE IN THIS PRESENTATION OR OTHERWISE THAT ARE NOT BASED ON CURRENT OR HISTORICAL FACTS ARE FORWARD-LOOKING IN NATURE INCLUDING, WITHOUT LIMITATION, STATEMENTS CONTAINING THE WORDS “BELIEVES”, “AIMS”, “ANTICIPATES”, “PLANS”, “PROJECTS”, “FORECASTS”, “GUIDANCE”, “INTENDS”, “EXPECTS”, “ESTIMATES”, “PREDICTS”, “MAY”, “CAN”, “LIKELY”, “WILL”, “SEEKS”, “SHOULD”, OR, IN EACH CASE, THEIR NEGATIVE OR COMPARABLE TERMINOLOGY. SUCH FORWARD-LOOKING STATEMENTS INVOLVE KNOWN AND UNKNOWN RISKS, UNCERTAINTIES AND OTHER IMPORTANT FACTORS THAT COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE GROUP TO BE MATERIALLY DIFFERENT FROM FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS EXPRESSED OR IMPLIED BY SUCH FORWARD-LOOKING STATEMENTS. FOR A DESCRIPTION OF SOME OF THESE FACTORS, SEE THE GROUP’S ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER 2020. ALL FORWARD-LOOKING STATEMENTS IN THIS PRESENTATION OR OTHERWISE SPEAK ONLY AS AT THE DATE OF PUBLICATION. LANCASHIRE EXPRESSLY DISCLAIMS ANY OBLIGATION OR UNDERTAKING (SAVE AS REQUIRED TO COMPLY WITH ANY LEGAL OR REGULATORY OBLIGATIONS INCLUDING THE RULES OF THE LONDON STOCK EXCHANGE) TO DISSEMINATE ANY UPDATES OR REVISIONS TO ANY FORWARD-LOOKING STATEMENT TO REFLECT ANY CHANGES IN THE GROUP’S EXPECTATIONS OR CIRCUMSTANCES ON WHICH ANY SUCH STATEMENT IS BASED. ALL SUBSEQUENT WRITTEN AND ORAL FORWARD-LOOKING STATEMENTS ATTRIBUTABLE TO THE GROUP OR INDIVIDUALS ACTING ON BEHALF OF THE GROUP ARE EXPRESSLY QUALIFIED IN THEIR ENTIRETY BY THIS NOTE. PROSPECTIVE INVESTORS SHOULD SPECIFICALLY CONSIDER THE FACTORS IDENTIFIED IN THIS PRESENTATION WHICH COULD CAUSE ACTUAL RESULTS TO DIFFER BEFORE MAKING AN INVESTMENT DECISION. -

Health Behaviours District Summary for Burnley

Burnley summary This local summary forms part of the joint strategic needs assessment for health behaviours in Lancashire.1 It provides an overview of the health behaviours questionnaire and the secondary data analysis, providing a bespoke view of health behaviours in the district. The intention is for this report to be used to aid commissioning decisions in local areas in conjunction with the recommendations of the health behaviours JSNA. For a wide range of data, intelligence and analysis, and summary reports for other local authorities please see the health behaviours webpage. Please direct all queries to [email protected] The questionnaire covered a wide range of topics around health behaviours and incorporated the 'healthy foundations' segmentation tool. Segmentation tools can be used to inform bespoke local health improvement activities. They provide insight for social marketing around health policies, campaigns and targeted interventions. This allows us to identify the motivation levels and the potential for behaviour change among In Burnley more respondents are classed as the different groups and can be used when 'balanced compensators', and 'live for todays', although fewer are 'health-conscious considering the recommendations below in realists' when compared to Lancashire. There relation to the health status, lifestyle behaviours are similar rates for 'hedonistic immortals', and wellbeing of Burnley's residents. and 'unconfident fatalists'. Recommendations for Burnley Strategies which address specific health behaviours may have a positive effect on improving health overall within the district. Whilst there are distinct recommendations for Burnley based on the questionnaire and secondary data analysis, there are overarching priorities and recommendations. -

Dwfitness Club & Smyths Toys Unit

DW FITNESS CLUB & SMYTHS TOYS UNIT VICARAGE LANE, BLACKPOOL, LANCASHIRE, FY4 4NB SECURE, LONG LET LEISURE AND RETAIL WAREHOUSE INVESTMENT WITH FIXED UPLIFTS DW FITNESS CLUB & SMYTHS TOYS UNIT VICARAGE LANE, BLACKPOOL, LANCASHIRE, FY4 4NB SECURE, LONG LET LEISURE AND RETAIL WAREHOUSE INVESTMENT WITH FIXED UPLIFTS INVESTMENT CONSIDERATIONS ■ City Fringe Gym Investment and Retail Warehouse ■ Total area of 54,857 sqft (5,096.2 sq m) ■ Site area of 4.3 acres (1.74 hectares) Investment situated on the busy Vicarage Lane ■ Fully let to the strong covenants of Dave Whelan ■ The vendor is seeking offers in excess of£4,750,000 within close proximity to Blackpool city centre Sports Limited and Smyths Toys UK Limited (Four Million Seven Hundred and Fifty Thousand ■ The town has an extensive catchment population ■ Attractive average weighted unexpired lease term Pounds) subject to contract and exclusive of VAT. and benefits fromexcellent accessibility with the of 14.4 years (12.8 years to break) Based on this level of pricing, the net initial yield A583 & A5230 linking Blackpool to the M55 and reflects 7.5%, assuming standard purchasers costs. ■ A584 coast road, which connects the city to the Producing a total rent of £377,257 pa, equating affluent Lytham St. Anne’s. to a low passing rent of £6.88 psf YIELD PROFILE ■ Freehold April 2021 8.57% April 2026 9.87% ■ Benefits from on-site car parking for approximately 200 cars. *based on forecast RPI at 2.5% Pen rose Av e D A O R E E R T Y R R E H DW FITNESS CLUB & SMYTHS TOYS UNIT VICARAGE LANE, BLACKPOOL, -

Blackburn with Darwen Employment and Skills Strategy 2017 - 2040

Blackburn with Darwen Employment and Skills Strategy 2017 - 2040 Blackburn with Darwen Skills Strategy | 1 Introduction Blackburn with Darwen’s Employment and Skills Strategy aims to get more local people into work by delivering a skills system that meets the needs of both employers and residents of the borough. Why is it needed? We have too few people of working age in work – one of the lowest rates in the region. A significant number of employers raise skills, or the lack of, as a recruitment issue. They report concern about the impact this has on their continued productivity and growth of their business. This can be related to workforce development needs or an inability to recruit new talent, particularly from the local area. In addition to this, skills are not just important for regional, national and global competitiveness; they have the potential to transform life chances and to drive social mobility. We need to ensure that Blackburn with Darwen’s education system has the infrastructure and framework in place to capitalise on what the Government sees as the skill needs for the future as set out in the Industrial Strategy White Paper published in November 2017. The Lancashire Enterprise Partnership (LEP) already has a Skills and Employment Strategic Framework and will be producing its own ‘Industrial Strategy’ in response to the White Paper. The Borough needs to be well placed to shape and influence this to ensure it reflects the needs of Blackburn with Darwen. There are lots of organisations and sectors across the borough and wider Lancashire area who wish to address skills issues and improve outcomes. -

Great Britain and King Cotton: the Lancashire Cotton

GREAT BRITAIN AND KING COTTON: THE LANCASHIRE COTTON FAMINE AND THE AMERICAN CIVIL WAR RYAN D KELL The Colorado College Department of History-Political Science Copyright © by Ryan D. Kell 2015 GREAT BRITAIN AND KING COTTON: THE LANCASHIRE COTTON FAMINE AND THE AMERICAN CIVIL WAR by RYAN D KELL THESIS Presented to the Faculty of the Undergraduate School of The Colorado College In Partial Fulfillment of the Requirements for the Degree of HISTORY-POLITICAL SCIENCE Department of History-Political Science THE COLORADO COLLEGE 2015 Acknowledgments I cannot express enough thanks to my thesis advisor, Lindsey Flewelling, Visiting Professor of History at Colorado College. Lindsey Was alWays Willing to help me With this project, Whether it Was With research or editing, while working a busy schedule of her own. I am extremely grateful for all the assistance she provided, and I could not have completed this task Without her. I would also like to thank David Hendrickson, Professor of Political Science at Colorado College. David helped me to polish my final product, making sure that I Was accurate and as persuasive With my argument as possible. My completion of this project Would not have been possible Without the help of my tWo academic advisors, Bryant “Tip” Ragan and Peter Blasenheim, both Professors of History at Colorado College. Tip, as my primary academic advisor, helped me navigate my four years of college and I Would not have been in position to graduate without him. Peter, my major advisor, has helped me to complete both my thesis and all my major requirements, always willing to give his honest opinion.