MAR Cool Dry Season 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DM-No.-296-S.-2011.Pdf

RepLiirhcof the Dhrilpprnes Deparlmentof Edr-rcarron Regicr,u'ii, Centi-ai Visavas DlVl'-;11ryUF BU'J(JL Ctt1,lf TagSilara' October24 2011 DIVISIONMEMORANDUM NaZqGs aell TO FclucatronSupervisorslpSD.S Coor-djnatrng er.incipals/Eiementan, arrciSeourrriary School Hearts PLJBI.IC-PRIVATF PARTNERSHIP (PPP!PROGRAIU SITE APPRAISAL Oneof the actrvrtresof the prrbhc_pr.rvatepartnershrp {ppp)School Buildrng prcgram ts app,'atsa!cl lhe prcpcsedreopient schools. fhe slte site'apprarsalactrvrt,es are scheduledfor lhe wnoternonln ol November{tndu$ve}20.1 1 Thereare $x teams to condttctthe r;lro appralsalPFSED Manila freldrng three protect Fngineersrn addittcn lc cul"lhree {3) {3) DtvtsicnProiect Fngrne.ers and Divrsron physroal Slalito copeup $iltn lhe oeadirne Fac,lilres In thts reqardthe dtvtston offtce wtll prcvtrje the transportatron distrrcl facrlrtv'c io thedrstrrct office and the i^*llprcvrdelhe acccrnrncdaticn ct each tea,,n-vPr/rr('r'\''r Yorrrcoo'eratron on thrsactrvirv rsenicrnerl f.r thesuc-cess of the proqram Travelrng expensesof the DivtstonProtect Enqrneersarirj the DrvrsronFhysrcai slafl shall DrvrsrcnMooF Fund: sublecl r'r be ,.*T[il.,:nainst i;ruar,rr*;;; ,rot rli,t,ig ,uru,,no LORNAE MNCES,Ph.D..CESO V SchooisDivrsron Superrnlendent ;1 ITINERARYOF TRAVEL Nameoi DPE: ROMEOREX ALABA of Travel To conduct Site Appralsalfor PPP Purpose '-'.'.- - -t Name of School I Date i--- o*:ion i --- MuniiiPaiiry 1 REX loi;i ,Buerravista lBago !-s- , NOV*7 E;il F-elrt- -, -, ilsnqr'o;i - i4cryu!.li i:,::H*Ti"i" l lc$ur-11E$ -e lponot igrenavl-le i Nov - - ,anhn, jaG;t"i.i" lbimoui:ilFt i:-"-rqlBotrol i;ili iau.nuu'it' NOV-q l.grrnio*rr jCawag-.'::i-: E"r.,"fHnnnf Ductlavt3La :.: ff: -. -

PHL-OCHA-Bohol Barangay 19Oct2013

Philippines: Bohol Sag Cordoba Sagasa Lapu-Lapu City Banacon San Fernando Naga City Jagoliao Mahanay Mahanay Gaus Alumar Nasingin Pandanon Pinamgo Maomawan Handumon Busalian Jandayan Norte Suba Jandayan Sur Malingin Western Cabul-an San Francisco Butan Eastern Cabul-an Bagacay Tulang Poblacion Poblacion Puerto San Pedro Tugas Taytay Burgos Tanghaligue San Jose Lipata Saguise Salog Santo Niño Poblacion Carlos P. Garcia San Isidro San Jose San Pedro Tugas Saguise Nueva Estrella Tuboran Lapinig Corte Baud Cangmundo Balintawak Santo Niño San Carlos Poblacion Tilmobo Carcar Bonbonon Cuaming Bien Unido Mandawa Campao Occidental Rizal San Jose San Agustin Nueva Esperanza Campamanog San Vicente Tugnao Santo Rosario Villa Milagrosa Canmangao Bayog Buyog Sikatuna Jetafe Liberty Cruz Campao Oriental Zamora Pres. Carlos P. Garcia Kabangkalan Pangpang San Roque Aguining Asinan Cantores La Victoria Cabasakan Tagum Norte Bogo Poblacion Hunan Cambus-Oc Poblacion Bago Sweetland Basiao Bonotbonot Talibon San Vicente Tagum Sur Achila Mocaboc Island Hambongan Rufo Hill Bantuan Guinobatan Humayhumay Santo Niño Bato Magsaysay Mabuhay Cabigohan Sentinila Lawis Kinan-Oan Popoo Cambuhat Overland Lusong Bugang Cangawa Cantuba Soom Tapon Tapal Hinlayagan Ilaud Baud Camambugan Poblacion Bagongbanwa Baluarte Santo Tomas La Union San Isidro Ondol Fatima Dait Bugaong Fatima Lubang Catoogan Katarungan San Isidro Lapacan Sur Nueva Granada Hinlayagan Ilaya Union Merryland Cantomugcad Puting Bato Tuboran Casate Tipolo Saa Dait Sur Cawag Trinidad Banlasan Manuel M. Roxas -

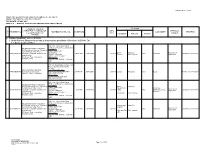

A. MINING TENEMENT APPLICATIONS 1. Under Process (Returned Pursuant to the Pertinent Provisions of Section 4 of EO No

ANNEX B Page 1 of 105 MINES AND GEOSCIENCES BUREAU REGIONAL OFFICE NO. VII MINING TENEMENTS STATISTICS REPORT FOR MONTH OF MAY, 2017 ANNEX B - MINERAL PRODUCTION SHARING AGREEMENT (MPSA) TENEMENT HOLDER/ LOCATION line PRESIDENT/ CHAIRMAN OF AREA PREVIOUS TENEMENT NO. ADDRESS/FAX/TEL. NO. DATE FILED COMMODITY REMARKS no. THE BOARD/CONTACT (has.) Barangay/s Mun./City Province HOLDER PERSON A. MINING TENEMENT APPLICATIONS 1. Under Process (Returned pursuant to the pertinent provisions of Section 4 of EO No. 79) 1.1. By the Regional Office 25th Floor, Petron Mega Plaza 358 Sen. Gil Puyat Ave., Makati City Apo Land and Quarry Corporation Cebu Office: Mr. Paul Vincent Arcenas - President Tinaan, Naga, Cebu Contact Person: Atty. Elvira C. Contact Nos.: Bairan Naga City Apo Cement 1 APSA000011VII Oquendo - Corporate Secretary and 06/03/1991 10/02/2009 240.0116 Cebu Limestone Returned on 03/31/2016 (032)273-3300 to 09 Tananas San Fernando Corporation Legal Director FAX No. - (032)273-9372 Mr. Gery L. Rota - Operations Manila Office: Manager (Cebu) (632)849-3754; FAX No. - (632)849- 3580 6th Floor, Quad Alpha Centrum, 125 Pioneer St., Mandaluyong City Tel. Nos. Atlas Consolidated Mining & Cebu Office (Mine Site): 2 APSA000013VII Development Corporation (032) 325-2215/(032) 467-1408 06/14/1991 01/11/2008 287.6172 Camp-8 Minglanilla Cebu Basalt Returned on 03/31/2016 Alfredo C. Ramos - President FAX - (032) 467-1288 Manila Office: (02)635-2387/(02)635-4495 FAX - (02) 635-4495 25th Floor, Petron Mega Plaza 358 Sen. Gil Puyat Ave., Makati City Apo Land and Quarry Corporation Cebu Office: Mr. -

DM-No.-098-S.-2020.Pdf

Bt*nhtic st tle Sllilf$$i$e$ &slisrtr$s$t sf Sbu*stisn itegi*n tr'Il * {.'}-XT-{{A{, \:lS.{\'-{$ scHosls sruIsl&f{ oF B0}N0r- Office of the Schools Division $uperintendent February 24,20?,* D31)"ISIOIT I?IEM{}NAIS SUM $*.q-f8' s. 2o2o fB*Til BIIILDI1YG ACTIIIT?T {ffi*atal l{*altb S*nagcment Frotoeel-GAl} Cosnpoaent} TO " : fiilIIHP F8O.TECT OWETR SDI'CATIT}H FBOGRAS SI'FER\NSOII IIT EI}IDAIIrCE ASD VAI,I'ES EtrT}CILTIOS DAXS rOCAt pEBS(}IT ffiE$TCAL $;rETCEB DrllIsxs$ 03' StlHoL Rs{tr$"rE8tD omsAfiss so$xsEr,olt,s IS? Coor*iastsr-In*ba*g* ISf$e $choal trEst-f 1, e, S FS*$e, ELEHEII"*5I? and $ECOI$B.*.RY B*HSOL &I}HUTIS?XA?GRS 1. ?his Olfice announces the conduct of the Team-Building Aetivities in the pilot implements.tion of Mental Heatth Ma:ragement Protoeol {MHMP} ?CI20 on the follouring schedules: Mareh 5-7. ?S20 {Thurxd*y-$aturday}- Ubay I I}istrict Participants lv€arch 1S-21, 2*20 {Thursday-satr"uday} IJbay Distriet ? Farticipants March26*?8, 202C {?hursda-v-Saturday} Ubay 3 District Pa.rticipants Venue: BPS?EA Br:ildizrg, Tagbilaran Citj' 2. Particip*nis to this three-day Team-Brlilding activities &re the following: Vakres and Guida:rce Education Program Suprviscr Pmject Orruner Division *f Bahol Register+d Guidance Caunseior* {R0Cs}-Faci[ilatsrs ' PSDSslActing PSDSs in th* districts Eleme*tar-y and Secondary Schcol Administrators in the t}ree districts andomly $ele*ted Elemente.4r arrd $eccndary $choal Teachers as Pilct Implementers of tlre Prograra. -

Postal Code Province City Barangay Amti Bao-Yan Danac East Danac West

Postal Code Province City Barangay Amti Bao-Yan Danac East Danac West 2815 Dao-Angan Boliney Dumagas Kilong-Olao Poblacion (Boliney) Abang Bangbangcag Bangcagan Banglolao Bugbog Calao Dugong Labon Layugan Madalipay North Poblacion 2805 Bucay Pagala Pakiling Palaquio Patoc Quimloong Salnec San Miguel Siblong South Poblacion Tabiog Ducligan Labaan 2817 Bucloc Lamao Lingay Ableg Cabaruyan 2816 Pikek Daguioman Tui Abaquid Cabaruan Caupasan Danglas 2825 Danglas Nagaparan Padangitan Pangal Bayaan Cabaroan Calumbaya Cardona Isit Kimmalaba Libtec Lub-Lubba 2801 Dolores Mudiit Namit-Ingan Pacac Poblacion Salucag Talogtog Taping Benben (Bonbon) Bulbulala Buli Canan (Gapan) Liguis Malabbaga 2826 La Paz Mudeng Pidipid Poblacion San Gregorio Toon Udangan Bacag Buneg Guinguinabang 2821 Lacub Lan-Ag Pacoc Poblacion (Talampac) Aguet Bacooc Balais Cayapa Dalaguisen Laang Lagben Laguiben Nagtipulan 2802 Nagtupacan Lagangilang Paganao Pawa Poblacion Presentar San Isidro Tagodtod Taping Ba-I Collago Pang-Ot 2824 Lagayan Poblacion Pulot Baac Dalayap (Nalaas) Mabungtot 2807 Malapaao Langiden Poblacion Quillat Bonglo (Patagui) Bulbulala Cawayan Domenglay Lenneng Mapisla 2819 Mogao Nalbuan Licuan-Baay (Licuan) Poblacion Subagan Tumalip Ampalioc Barit Gayaman Lul-Luno 2813 Abra Luba Luzong Nagbukel-Tuquipa Poblacion Sabnangan Bayabas Binasaran Buanao Dulao Duldulao Gacab 2820 Lat-Ey Malibcong Malibcong Mataragan Pacgued Taripan Umnap Ayyeng Catacdegan Nuevo Catacdegan Viejo Luzong San Jose Norte San Jose Sur 2810 Manabo San Juan Norte San Juan Sur San Ramon East -

Spectrum Management Principles, Challenges and Issues Related to Dynamic Access to Frequency Bands by Means of Radio Systems Employing Cognitive Capabilities

Report ITU-R SM.2405-0 (06/2017) Spectrum management principles, challenges and issues related to dynamic access to frequency bands by means of radio systems employing cognitive capabilities SM Series Spectrum management ii Rep. ITU-R SM.2405-0 Foreword The role of the Radiocommunication Sector is to ensure the rational, equitable, efficient and economical use of the radio- frequency spectrum by all radiocommunication services, including satellite services, and carry out studies without limit of frequency range on the basis of which Recommendations are adopted. The regulatory and policy functions of the Radiocommunication Sector are performed by World and Regional Radiocommunication Conferences and Radiocommunication Assemblies supported by Study Groups. Policy on Intellectual Property Right (IPR) ITU-R policy on IPR is described in the Common Patent Policy for ITU-T/ITU-R/ISO/IEC referenced in Annex 1 of Resolution ITU-R 1. Forms to be used for the submission of patent statements and licensing declarations by patent holders are available from http://www.itu.int/ITU-R/go/patents/en where the Guidelines for Implementation of the Common Patent Policy for ITU-T/ITU-R/ISO/IEC and the ITU-R patent information database can also be found. Series of ITU-R Reports (Also available online at http://www.itu.int/publ/R-REP/en) Series Title BO Satellite delivery BR Recording for production, archival and play-out; film for television BS Broadcasting service (sound) BT Broadcasting service (television) F Fixed service M Mobile, radiodetermination, amateur and related satellite services P Radiowave propagation RA Radio astronomy RS Remote sensing systems S Fixed-satellite service SA Space applications and meteorology SF Frequency sharing and coordination between fixed-satellite and fixed service systems SM Spectrum management Note: This ITU-R Report was approved in English by the Study Group under the procedure detailed in Resolution ITU-R 1. -

World Bank Document

Document of The World Bank FOR uFFICIAL USE ONLY Public Disclosure Authorized ReportNo. 7948 PROJECT COMPLETION REPORT Public Disclosure Authorized PHILIPPINES RURAL INFRASTRUCTURE PROJECT (CREDIT 790-PH) JUNE 30, 1989 Public Disclosure Authorized Adra-hure Operations Division CouintryDepartment II Public Disclosure Authorized Asia Regional Office This document has a restricted distribution and mat be used by recipients only in the performance of their official luties. Its contents may not otherwise be disclosed without World Bank authorizstion. CURRENCYEQUIVALENTS Currency unit - Philippines Peso (O) P 1 - US$0.135 US$1 - 1 7.40 WEIGHTSAND MEASURES 1 ha - 2.47 acres 1 km - 0.62 miles 1 sq km - 0.386 sq mile 1 m - 3.28 ft 1 sq m = 10.76 sq ft 1 cu m - 35.31 cu ft 1 M cu m 3 810.7 ac ft 1 mm 00.039 in 1 kg - 2.2 lb 1 cavan = 50 kg 20 cavans = 1 m ton ABBREVIATIONS ADB - Asian Development Bank AID - Agency for International Development BAE - Bureau of Agricultural Extension BBR - Bureau of Barangay Roads BHS - Barangay health Station BPI - Bureau of Plant Industry BPW - Bureau of Public Works CCC - Cabinet Coordinating Committee on Rural Development CP - Cooperative Program CPO - Central Project Organization DAR - Department of Agrarian Reforms DLGCD - Department of Local Government and Community Development DOH - Department of Health DPH - Departmont of Public Highways DPWTC - Department of Public Works, Transportation and Communications FAO - Food and Agriculture Organization FSDC - Farm Systems Development Corporation ISA - Irrigation -

Province, City, Municipality Total and Barangay Population BOHOL 1,255,128 ALBURQUERQUE 9,921 Bahi 787 Basacdacu 759 Cantiguib 5

2010 Census of Population and Housing Bohol Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population BOHOL 1,255,128 ALBURQUERQUE 9,921 Bahi 787 Basacdacu 759 Cantiguib 555 Dangay 798 East Poblacion 1,829 Ponong 1,121 San Agustin 526 Santa Filomena 911 Tagbuane 888 Toril 706 West Poblacion 1,041 ALICIA 22,285 Cabatang 675 Cagongcagong 423 Cambaol 1,087 Cayacay 1,713 Del Monte 806 Katipunan 2,230 La Hacienda 3,710 Mahayag 687 Napo 1,255 Pagahat 586 Poblacion (Calingganay) 4,064 Progreso 1,019 Putlongcam 1,578 Sudlon (Omhor) 648 Untaga 1,804 ANDA 16,909 Almaria 392 Bacong 2,289 Badiang 1,277 National Statistics Office 1 2010 Census of Population and Housing Bohol Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population Buenasuerte 398 Candabong 2,297 Casica 406 Katipunan 503 Linawan 987 Lundag 1,029 Poblacion 1,295 Santa Cruz 1,123 Suba 1,125 Talisay 1,048 Tanod 487 Tawid 825 Virgen 1,428 ANTEQUERA 14,481 Angilan 1,012 Bantolinao 1,226 Bicahan 783 Bitaugan 591 Bungahan 744 Canlaas 736 Cansibuan 512 Can-omay 721 Celing 671 Danao 453 Danicop 576 Mag-aso 434 Poblacion 1,332 Quinapon-an 278 Santo Rosario 475 Tabuan 584 Tagubaas 386 Tupas 935 Ubojan 529 Viga 614 Villa Aurora (Canoc-oc) 889 National Statistics Office 2 2010 Census of Population and Housing Bohol Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and -

Congressional District 2 List of Grade V Teachers for English Proficiency Test 6 11

Republic of the Philippines Department of Education Region VII, Central Visayas DIVISION OF BOHOL CONGRESSIONAL DISTRICT 2 LIST OF GRADE V TEACHERS FOR ENGLISH PROFICIENCY TEST ROOM 1 (A.M.)- San Roque NHS, Alburquerque No. Name District 1 Abarre MariaImaG. TugasES,Getafe 2 Abad JesseC. CPGCES Theresa Ubay1CES 3 Abapo > 4 Abapo Welenda VillaMilagrosaES,CPG 5 Abella AvelineD. GetafeCES Abregana Jonalyn SanMiguelES,Dagohoy 6 , 7 Aclao Lucile SaguiseES,CPG 8 Alcazar AntonietteV. Talibon 1 9 Amba CrisdtinaA. Talibon 1 Amorin UrsulaT. Buenavista 10 , 11 Ampo Ruel VillaTeresitaES,Ubay3 12 Anana VeronicaE. Buenavista 13 Anto QueenieE. Buenavista 14 Anzano WilmaP. HandumonES,Getafe 15 Aparece CitoA. Buenavista Aparece DoreenC. Buenavista 16 , 17 Aparri Veronica DagohoyCES 18 Aranzado UnaM. GarciaES,SanMiguel 19 Artiaga ServeniaF. Talibon 1 Aurestila Margie DiisES,Trinidad 20 i Autentico Juliet LaVictoriaES,Trinidad 21 / 22 Auxtero ElvanaT. CabatuanES,Danao Avenido Ma.Lolete TrinidadCES 23 i 24 Ayento Donato0. SanCarlosES,Danao 25 Baay BernadethC. CorazonES,SanMiguel 26 Bacante NelmaS. JagoliaoES,Getafe 27 Bagot MescilM. Buenavista 28 Baja Melisa SinandiganES,Ubay2 29 Balabat CindyC. Talibon 1 Baliientos MariaNilLBuenavista 30 i (Note for the EXAMINEES) brings pencils (lead No. 2 bring snacks clean sheet of paper & sharpener must know the school ID his/her respective school CONGRESSIONAL DISTRICT 2 LIST OF GRADE V TEACHERS FOR ENGLISH PROFICIENCY TEST ROOM2(A.M.)-SanRoqueNHS, Alburquerque 1 3alonga MeriamE. t Talibon 1 2 3amba ChristopherS. t Ubay1CES 3 Bantono Anjo i Talibon 1 4 Batiller LynnE. / 3uenavista 5 3autiata Prisco / Talibon 1 6 3autista JaniceC. / 3uenavista 7 Belga AnalynT. i CangmundoES,Getafe 8 Belida MarianitoV. / SanVicenteES,CPG 9 Bendanillo Analie Pag-asaES,Ubay3 10 Bentulan Helen TipoloEs,Ubay2 11 3ernales Marissa BenliwES,Ubay2 12 Besira Esterlita i Talibon 1 13 Betaizar CecileGraceE. -

A Comprehensive Assessment of the Agricultural Extension System in the Philippines: Case Study of LGU Extension in Ubay, Bohol

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Saz, Efren B. Working Paper A Comprehensive Assessment of the Agricultural Extension System in the Philippines: Case Study of LGU Extension in Ubay, Bohol PIDS Discussion Paper Series, No. 2007-02 Provided in Cooperation with: Philippine Institute for Development Studies (PIDS), Philippines Suggested Citation: Saz, Efren B. (2007) : A Comprehensive Assessment of the Agricultural Extension System in the Philippines: Case Study of LGU Extension in Ubay, Bohol, PIDS Discussion Paper Series, No. 2007-02, Philippine Institute for Development Studies (PIDS), Makati City This Version is available at: http://hdl.handle.net/10419/127938 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu Philippine Institute for Development Studies Surian sa mga Pag-aaral Pangkaunlaran ng Pilipinas A Comprehensive Assessment of the Agricultural Extension System in the Philippines: Case Study of LGU Extension in Ubay, Bohol Efren B. -

Geospatial Analysis of Pediatric Tuberculosis in Bohol, Philippines: Disease Clusters and Access to Care

The Texas Medical Center Library DigitalCommons@TMC UT School of Public Health Dissertations (Open Access) School of Public Health Spring 5-2019 GEOSPATIAL ANALYSIS OF PEDIATRIC TUBERCULOSIS IN BOHOL, PHILIPPINES: DISEASE CLUSTERS AND ACCESS TO CARE LAUREN M. LEINING UTHealth School of Public Health Follow this and additional works at: https://digitalcommons.library.tmc.edu/uthsph_dissertsopen Part of the Community Psychology Commons, Health Psychology Commons, and the Public Health Commons Recommended Citation LEINING, LAUREN M., "GEOSPATIAL ANALYSIS OF PEDIATRIC TUBERCULOSIS IN BOHOL, PHILIPPINES: DISEASE CLUSTERS AND ACCESS TO CARE" (2019). UT School of Public Health Dissertations (Open Access). 67. https://digitalcommons.library.tmc.edu/uthsph_dissertsopen/67 This is brought to you for free and open access by the School of Public Health at DigitalCommons@TMC. It has been accepted for inclusion in UT School of Public Health Dissertations (Open Access) by an authorized administrator of DigitalCommons@TMC. For more information, please contact [email protected]. GEOSPATIAL ANALYSIS OF PEDIATRIC TUBERCULOSIS IN BOHOL, PHILIPPINES: DISEASE CLUSTERS AND ACCESS TO CARE by LAUREN M. LEINING, B.A. APPROVED: JOESPH B. MCCORMICK, MD KRISTY O. MURRAY, DVM, PHD LU-YU HWANG, MD SARAH M. GUNTER, PHD, MPH Copyright by Lauren M. Leining, BA, MPH 2019 DEDICATION To our Bohol research team and the families who participated in this study. GEOSPATIAL ANALYSIS OF PEDIATRIC TUBERCULOSIS IN BOHOL, PHILIPPINES: DISEASE CLUSTERS AND ACCESS TO CARE by LAUREN M. LEINING BACHELOR OF ARTS, St. Edwards University, 2013 Presented to the Faculty of The University of Texas School of Public Health in Partial Fulfillment of the Requirements for the Degree of MASTER OF PUBLIC HEALTH THE UNIVERSITY OF TEXAS SCHOOL OF PUBLIC HEALTH Houston, Texas May 2019 ACKNOWLEDGEMENTS Thank you to my dedicated supervisors, mentor, co-workers, and peers who have supported me through this project. -

TV White Space Technologies

TV White Space Technologies! Super Wi-Fi, Weightless! From a Wasted Resource Into a Tool fro Public Service & National Development! The Philippine Internet Landscape The Philippine Internet Landscape The Philippine Internet Landscape Based on DepEd Study! The Philippine Internet Landscape Based on DepEd Study! The Philippine Internet Landscape Based on DepEd Study! The Philippine Internet Landscape Based on DepEd Study! Based on DepEd Study! The Philippine Internet Landscape Based on DepEd Study! Based on DepEd Study! The Philippine Internet Landscape TVWS Area Connected w Internet w/out Internet Based on DepEd Study! The Philippine Internet Landscape The Philippine “Connectivity”! 55.42% cities and municipalities have broadband access (fixed or wireless) which is more often than not limited to the immediate vicinity of a municipality’s center.! 35% or 33.6M out of 95.9M Filipinos use the Internet! 20% of households! have computers! The Philippine Internet Landscape The Philippine “Connectivity”! 94.2 Cellular Mobile! Million Telephone Service! active! 98.52% mobile phones! of municipalities! 2 messages! 99% Billion! handled daily! population (CY2011)! The Philippine Internet Landscape ICT Situation of Public Schools! Elementary Schools High Schools 38,659 7,750 86% 53% 17% public elementary are in an area public high schools schools use use available 4% with an ISP available use a wired connectivity connectivity connection Cost Per Elementary School P1,026.60 is equal to the lowest household ISP subscription. TV White Space TV White Space CH3CH3 CH6 CH8 CH10 CH12 “Guard Band” There many unused TV channels are channels possibly due TV White intentionally kept Space refers between active ones to to insufficient to the unused distinguish signals commercial TV channels clearly.