Economics of Value Addition in Oleoresin: Implications for Access and Benefit Sharing of Byadagi Chilli in Karnataka

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

International Journal of Advanced Scientific and Technical Research

International Journal of Advanced Scientific and Technical Research Issue 3 volume 2, March-April 2013 Available online on http://www.rspublication.com/ijst/index.html ISSN 2249-9954 CAPSAICIN AND COLOUR EXTRACTION FROM DIFFERENT VERITIES OF GREEN AND RED CHILLI PEPPERS OF ANDHRAPRADESH DR. M. VIJAYA BHASKARA REDDY AND P. SASIKALA Corresponding author: Dr. M. Vijaya Bhaskara Reddy Study Investigator, Dept. of LPM, College of veterinary Science, Sri Venkateswara Veterinary University Tirupati-517502, Andhra Pradesh, India, Email: Cell: +91- 7396120530 Co- Author: P. Sasikala Dept. of LPM, College of veterinary Science, Sri Venkateswara Veterinary University, Tirupati-517502, Andhra Pradesh, India ______________________________________________________________________________ ABSTRACT Twelve different chilli varieties at three different stages (green, red ripe, red dry) were collected. The chillies were subjected for the estimation and extraction of capsaicin and colour. The estimation of capsaicin was done in the laboratory to determine the pungency for each chilli variety collected. The pungency level was given in Scoville units. The chilli sample which has the highest pungency was subjected for the extraction of capsaicin. From the pericarp of the chilli the colour was extracted and the colour intensity was found according to the ASTA (American Spice Trade Association) and CU (Colour Units). The large scale industrial extraction procedure for the extraction of capsaicin and colour was collected. Key words: Green and Red Chilli Samples, Capsaicin, Colour Oleoresin. ______________________________________________________________________________ INTRODUCTION In India, Pepper is an important agricultural crop, not only because of its economic importance, but also for the nutritional value of its fruits, mainly due to the fact that they are an excellent source of natural colors and antioxidant compounds (Nevarro et al., 2006). -

22/01/2021 Government of Karnataka Page:197

22/01/2021 GOVERNMENT OF KARNATAKA PAGE:197 DEPARTMENT OF PRE UNIVERSITY EDUCATION LIST OF PU COLLEGES IN HAVERI DISTRICT AS ON 22/01/2021 ******************************************************************************** SLNO COLCD NAME AND ADDRESS YEAR OF OPEN & COLL TYPE OPENING & AIDED GO NOS. WITH DATE ******************************************************************************** 2658 JH0031 GUDLEPPA HALLIKERI PU COL 63-64 BIFUR PU COL HAVERI DCE 59 MG 64 DT 16-03-1965 581110 -------------------------------------------------------------------------------- 2659 JH0032 GOVT SJJM PU COLLEGE GOVT PU COL BYADGI HAVERI DT 581106 -------------------------------------------------------------------------------- 2660 JH0033 GOVT MAJID PU COLLEGE 72-73 GOVT PU COL SAVANUR HAVERI DT 581118 -------------------------------------------------------------------------------- 2661 JH0034 RTES PU COLLEGE 66-67 BIFUR PU COL RANIBENNUR PB ROAD HAVERI DT 581115 -------------------------------------------------------------------------------- 2662 JH0035 HOSAMANI SIDDAPPA PU COL 72-73 AIDED PU COL RANIBENNUR AFL CR 103 71-72 DT 02-06-1972 HAVERI DT 581115 PUE/ACCTS/OAG/GIT/1973-74 22/02/74 -------------------------------------------------------------------------------- 2663 JH0036 MAHANTASWAMY PU COLLEGE 67-68 BIFUR PU COL HAUNSBHAVI HIREKERUR TQ HAVERI DT 581109 -------------------------------------------------------------------------------- 2664 JH0037 CES KH PATIL PU COLLEGE 72-73 AIDED PU COL HIREKERUR AFL CR 92 71-72 DT 03-06-1972 HAVERI DT 581111 PUE/ACCTS/0-11/GIA/72-73 -

Design of 24X7 Water Supply System for Ranebennur Town

ISSN(Online): 2319-8753 ISSN (Print): 2347-6710 International Journal of Innovative Research in Science, Engineering and Technology (An ISO 3297: 2007 Certified Organization) Vol. 5, Issue 6, June 2016 Design of 24x7 Water Supply System for Ranebennur Town Mallikarjun S K 1, Jyothi D O 2, Manjureddy K H 3, Sandhya H B 4, Anand S Amaravati 5, U.G. Students, Department of Civil Engineering, STJIT Engineering College, Ranebennur, Karnataka, India1234 Assistant Professor, Department of Civil Engineering, STJIT Engineering College, Ranebennur, Karnataka, India5 ABSTRACT: The project highlights the work carried out on the population forecast, water requirement and water supply to the Ranebennur town, Haveri district, Karnataka,-India. The Current project has been carried out on design a 24x7 water supply scheme for a Ranebennur town for domestic use. It also includes the provision of design of intake structure, water treatment work, for the area in order to supply the treated water to the publics. Providing distribution networks, pipe appurtenances, and water meters, to save water. Quality and quantity of water supplied should be satisfactory. KEYWORDS: Water, Surface Water, Water Quality, Water Supply, Water Treatment Scheme I. INTRODUCTION Water is one of the most basic amenities required for every living being. Apart from using the water for domestic needs, water resources have been the most widely exploited natural system since man occupied this earth. The other beneficial uses of water includes, for industries, generation of electric power, -

Red Chilli Prices to Decline Marginally During Harvest India Is the Largest

Tamil Nadu Agricultural University Coimbatore – 641 003 Dr. Ravi Kumar Theodore, Ph.D., Phone: 0422 - 6611302 Public Relations Officer & Fax: 0422 – 2431821 Professor (Agrl. Extension) E-mail: [email protected] To Date: 5-11-2012 The Editor, Sir, I request that the following matter may kindly be published in your esteemed daily: Red Chilli Prices to Decline Marginally During Harvest India is the largest producer, consumer and exporter of chili, which contributes to 25% of total world production. India has produced about 12.50 lakh tonnes of chilli during 2011-12. Next to India, China is the major producer of chilli in the world. During 2010, Chinese chilli production declined sharply because of unfavorable weather conditions which became an advantage for Indian chilli exporters. In India, chillies are grown in almost all the states. Andhra Pradesh is the largest producer of chilli in India contributing to about 30% to the total area under chilli, followed by Karnataka (20%), Orissa (9%), Tamil Nadu (8%), Maharashtra (1%), and other States contributing 18 %. Chillies grown in India have many special features. The Byadagi and Guntur sannam varieties are known for its natural colour. Mizoram and some areas of Manipur chilli are famous for their spiciness. Byadagi chilli is used for extracting oil. 10-15% of total domestic production is meant for exports with domestic consumption of 85-90%. India exports chilli in various processed forms like chilli powder, dried chillies, chilly pickles, chilli paste, flaked chilli, etc., and it is mainly exported to Sri Lanka, USA, Nepal, Mexico, Malaysia, Bangladesh, UAE, Indonesia and China. -

Effect of Drying Methods on Seed Quality of Byadagi Chilli

Bulletin of Environment, Pharmacology and Life Sciences Bull. Env. Pharmacol. Life Sci., Vol 7 [4] April 2018 : 27-29 ©2018 Academy for Environment and Life Sciences, India Online ISSN 2277-1808 Journal’s URL:http://www.bepls.com CODEN: BEPLAD Global Impact Factor 0.876 Universal Impact Factor 0.9804 NAAS Rating 4.95 ORIGINAL ARTICLE OPEN ACCESS Effect of Drying Methods on Seed Quality of Byadagi Chilli Krishna D. Kurubetta *, M. H. Tatagar, T. B. Allolli, R. K. Mesta, M. Abdul Kareem and K. Sweta * Assistant Professor of Agronomy, Horticulture Research and Extension Station, Devihosur- 581110, Haveri , Karnataka . e-mail: [email protected] ABSTRACT The pooled results of the two year experimentation revealed that, among the different methods of drying chilli, significantly highest per cent (85%) of germination was noticed with treatment (T6) drying on surface washed with dung slurry and field emergence(77%) with drying on cement concrete floor and drying on polythene tarpaulin sheet. The high temperature during drying period will affect the seed quality parameters. Key words : Drying methods, Seed quality, Chilli Seed, Bydagi Chilli Received 11.02.2018 Revised 02.03.2018 Accepted 26.04.2018 INTRODUCTION Drying is one of the essential unit operations performed to increase the shelf life of agricultural / horticultural produce and it is one of the most practical methods of preserving food and the quality of horticultural produce. If the drying process is not completed fast enough, growth of microorganisms will take place as a result of the high relative humidity [1-2]. This often leads to severe deterioration of the quality of the product. -

Processing of Byadgi Chilli

PROCESSING OF BYADGI CHILLI 1 INTRODUCTION ❑ Byadgi or Byadagi chilli is a famous variety of chilli in Karnataka state. ❑ It is a long (12-15 cm) and thin variety of chilli. The fruits have characteristic red colour and wrinkles on the surface. ❑ This variety of chilli is extensively grown and marketed in Byadgi, a town in the Haveri district of Karnataka state. Hence, the name of the variety is Byadgi chilli 2 GENERAL CHARACTERISTICS OF BYADGI CHILLI ❑ Byadgi chillies are famous for its aroma and deep red colour. ➢ Colour: 150000 - 250000 CU (Colour Units) or 80 - 130 ASTA ❑ Bydagi chillies have mild pungency and moderate seed content. ➢ The capsaicin content: 0.8 - 1.3%, Oleoresin: 12 – 15% ➢ Pungency: 8000 - 15000 SHU (Scoville Heat Units). ❑ Byadgi chillies are the Geographical Indication product of Karnataka. ❑ Grown in Dharwad, Gadag, Haveri , Bellary, Raichur and Gulbarga districts of Karnamataka and Karnool and Adhoni districts of Andhra Pradesh ➢ Yield: 0.5-1.25 MT/ha (rain-fed), 3.75-5.00 MT/ha (Irrigated) 3 VARIETIES OF BYADGI CHILLI Byadgi Kaddi Byadgi Dabbi Other varieties Dyavanur Delux Noolvi Dabbi Kubhsi Dabbi Antur Bentur Dabbi 4 CULTIVATION OF BYADGI CHILLIES ❑ Soil ➢ Well drained loamy soils ➢ Black and red lateritic soils rich in potash having a pH of 5.5-6.5 ❑ Climate ➢ 20-38ºC with warm humid conditions during the growth of plant ➢ Dry weather conditions during maturity of fruits. ❑ Sowing : May-June month ➢ Transplanting 30-45 days old seedlings on raised beds of 1 m width. ➢ Seed rate: 1.0 - 1.25 kg/ha, 40 - 45 days seedlings ❑ Harvesting ➢ November - January months ➢ Fruits are picked when they turn bright red colour. -

Department of Animal Husbandry and Veterinary Services

Department of Animal Husbandry and Veterinary services Details of Hospital Co-ordinates to be submitted to AH&VS Helpline District name : Haveri Name of the SL.NO Taluk Name Name of the Hospital (VH, VD, PVC) Contact Number Doctor Dr.Santosh 1 Hangal V D Kusanur 7411108998 Malagund https://goo.gl/maps/SSRQUc5a4Fa32Ypt9 Dr.Santosh 2 Hangal V D Belagalpet Malagund 7411108998 (incharge) https://goo.gl/maps/Z3oGx9cUdvNu1sLD9 Dr.Suresh 3 Hangal V D Adur Magod 9986546509 (incharge) https://goo.gl/maps/BbohjuLagXxXYYyV9 Dr.Suresh 4 Hangal V D Shiragod Magod 9986546509 (incharge) https://goo.gl/maps/dqzRRQdjJ2tCg51h9 Dr.Santosh 5 Hangal V D Araleshwara Malagund 7411108998 (incharge) https://goo.gl/maps/AGCX4yiNNnn3HfQi7 Dr.Santosh 6 Hangal V D Shyadaguppi Malagund 7411108998 (incharge) https://goo.gl/maps/nNupo8wQ6eWzcAwo7 Dr.Santosh 7 Hangal V D Kanchinegalur Malagund 7411108998 (incharge) https://goo.gl/maps/pdghFsE5bzH26nhX6 Dr.Suresh 8 Hangal V D Herur Magod 9986546509 (incharge) https://goo.gl/maps/XZctoC8JocdSowHx9 Dr.Girish 9 Hangal PVC Somasagar Radder 9901118508 (incharge) https://goo.gl/maps/z3uuMLCrzqXyMXpr8 Dr.Santosh 10 Hangal V H Bommanahalli Malagund 7411108998 (incharge) https://goo.gl/maps/i3naV4Pwm21RLxzM9 Dr.Girish 11 Hangal V H Hangal Radder 9901118508 (incharge) https://goo.gl/maps/VNK31yw7afHPygJFA Dr.Girish 12 Hangal V D Akkivalli 9901118508 Radder https://goo.gl/maps/dx4JTzoLAF4Vy3Vt8 Dr.Suresh 13 Hangal V D Chikkoushihosur Magod 9986546509 (incharge) https://goo.gl/maps/U9eHgBGrFZA2q7qm6 Dr.Suresh 14 Hangal V D Hirehullal -

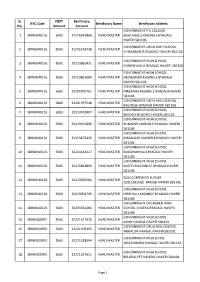

Sl. No. IFSC Code NEFT Amount Benificiary Account Benificiary

Sl. NEFT Benificiary IFSC Code Benificiary Name Benificiary Address No. Amount Account GOVERNMENT P U COLLEGE 1 SBIN0040126 5000 31216042866 HEAD MASTER BISALAHALLI KAGINELE BYADAGI HAVERI 581106 GOVERNMENT URDU HIGH SCHOOL 2 SBIN0040126 5000 31216199238 HEAD MASTER CHIKKABASUR BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 3 SBIN0040126 5000 31213865431 HEAD MASTER GUNDENHALLI BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 4 SBIN0040126 5000 31213861684 HEAD MASTER HEDIGONDA KAGINELE BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 5 SBIN0040126 5000 31202000761 HEAD MASTER HIREANAJI KAGINELE BYADAGI HAVERI 581106 GOVERNMENT URDU HIGH SCHOOL 6 SBIN0040126 5000 31201997540 HEAD MASTER KAGINELE BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 7 SBIN0040126 5000 31213902407 HEAD MASTER KERVADI BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 8 SBIN0040126 5000 31213916806 HEAD MASTER KUMMUR KAGINELE BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 9 SBIN0040126 5000 31213872426 HEAD MASTER MASANAGI KAGINELE BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 10 SBIN0040126 5000 31214444127 HEAD MASTER BUDAPANHALLI BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 11 SBIN0040126 5000 31215863894 HEAD MASTER MUTTUR KAGINELE BYADAGI HAVERI 581106 SJJM COMPOSITE JUNIOR 12 SBIN0040126 5000 31213920084 HEAD MASTER COLLEGELEGE BYADGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 13 SBIN0040126 5000 31213904743 HEAD MASTER HIREHALLI KAGINELE BYADAGI HAVERI 581106 GOVERNMENT UPGRADED HIGH 14 SBIN0040126 5000 31303362184 HEAD MASTER SCHOOL CHATRA BYADAGI HAVERI 581106 GOVERNMENT HIGH SCHOOL 15 SBIN0000991 5000 31221311925 HEAD MASTER ADUR HANGAL HAVERI 581101 GOVERNMENT URDU HIGH SCHOOL 16 SBIN0000991 5000 31221309165 HEAD MASTER AKKIALUR HANGAL HAVERI 581102 GOVERNMENT HIGH SCHOL 17 SBIN0000991 5000 31221328394 HEAD MASTER ARLESHWARA HANGAL HAVERI 581110 GOVERNMENT HIGH SCHOOL 18 SBIN0000991 5000 31221327651 HEAD MASTER BELAGALPET HANGAL HAVERI 581104 Page 1 Sl. -

Hot Chili Chili Tool Oa., Styrke & Scoville – 3 – Rev

Hot Chili Chili tool oa., Styrke & Scoville – 3 – rev. 1.2 Stor liste med relativ styrke og Scoville værdi (..eller den lille gruppe oversigt med kendte chili) Styrke Navne Scoville Noter ▪ Ren Capsaicin 16,000,000 12 ▪ Carolina Reaper 2,200,000 ▪ Trinidad Moruga Scorpion 2,009,231 ▪ ▪ 7 Pot Douglah 1,853,396 10++++ til 12 ▪ Trinidad Scorpion Butch T 1,463,700 ▪ Naga Viper Pepper 1,382,118 ▪ 7 Pot Barrackpore 1,300,000 ▪ 7 Pot Jonah 1,200,000 ▪ 7 Pot Primo 1,200,000 ▪ New Mexico Scorpion 1,191,595 ▪ Infinity Chili 1,176,182 ▪ Bedfordshire Super Naga 1,120,000 ▪ ▪ Dorset Naga chili 1,100,000 ▪ Naga Jolokia 1,100,000 ▪ Naga Morich 1,100,000 ▪ Spanish Naga Chili 1,086,844 ▪ 7 Pot Madballz 1,066,882 ▪ Bhut Jolokia chili 1,041,427 ▪ Chocolate Bhut Jolokia 1,001,304 ▪ 7 Pot Brain Strain 1,000,000 ▪ Bhut Jolokia Indian Carbon 1,000,000 ▪ Trinidad Scorpion 1,000,000 ▪ Raja Mirch 900,000 ▪ Habanaga chili 800,000 ▪ Nagabon Jolokia 800,000 ▪ Red Savina Habanero 580,000 10++++ Chili Home Side 1/12 Hot Chili Chili tool oa., Styrke & Scoville – 3 – rev. 1.2 10+++ og 10++++ ▪ Fatalii 500,000 10++++ ▪ Aji Chombo 500,000 ▪ Pingo de Ouro 500,000 ▪ Aribibi Gusano 470,000 ▪ Caribbean Red Habanero 400,000 ▪ Chocolate Habanero 350,000 10++++ ▪ Datil chili 350,000 10++++ ▪ Habanero 350,000 ▪ Jamaican Hot chili 350,000 ▪ Madame Jeanette chili 350,000 ▪ Rocoto chili 350,000 ▪ Scotch Bonnet 350,000 10+++ ▪ Zimbabwe Bird Chili 350,000 ▪ Adjuma 350,000 ▪ Guyana Wiri Wiri 350,000 10+++ ▪ Tiger Paw 348,634 ▪ Big Sun Habanero 325,000 ▪ Orange Habanero 325,000 9 og 10+++ ▪ Mustard Habanero 300,000 ▪ Devil’s Tongue 300,000 10++++ ▪ Orange Rocoto chili 300,000 10++ ▪ Paper Lantern Habanero 300,000 ▪ Piri Piri 300,000 8-10 ▪ Red Cheese 300,000 ▪ Red Rocoto 300,000 10++ ▪ Tepin chili 300,000 ▪ Thai Burapa 300,000 ▪ White Habanero 300,000 9-10 ▪ Yellow Habanero 300,000 ▪ Texas Chiltepin 265,000 ▪ Pimenta de Neyde 250,000 ▪ Maori 240,000 ▪ Quintisho 240,000 Chili Home Side 2/12 Hot Chili Chili tool oa., Styrke & Scoville – 3 – rev. -

Haveri District Karnataka West Graduates Constituency in the State

75°0'0"E 75°10'0"E 75°20'0"E 75°30'0"E 75°40'0"E 75°50'0"E N N " " 0 0 ' ' 0 0 2 2 ° ° 5 5 1 Haveri District 1 Karnataka West Graduates Constituency in the State of Karnataka-2020 µ N N " " 0 0 ' ' 0 0 1 1 ° ° 5 5 1 Dharwad District 1 Muthalli Tadas Attigeri Basanal Kamalanagar Muthalli Thimmapur Panigatti Shisuvinal Kunnur Belwalakoppa Adavisomapur Neeralgi Hirebendigeri Chikbendigeri Hulgur Kadahalli Kyalkond Gudageri Surapgatti G Kunnur Belagali Gonala Shyadambi a Madapur d Mamadapur Hulsogi Kabanur Jekenakatti Chowdala a Hiremanakatti (Manakatti) Yelavigi g KengapurJekenakatti Maruthipura Huvinshigli Kunnur Madli Dhundshi Bisatikoppa Bannur D 96 Gotagodi Mugali Karadagi Bujruk Basapur Bannikoppa is Hesarur Sheelvant Somapur Wanahalli Hiremallur Chillur Badni Paramawadi Basavankoppa tr Kamanahalli Ganjigatti Honikop i N Jondalgatti Aratal c N " Makapur Chikmallur t " 0 0 ' Mantrodi Naikerur ' 0 Yattinahalli Shiggaon (TMC) Chillur Allipura 0 ° Shirabadgi ° SHIGGAON Kankanwad 5 95 Vadnikoppa Siddapur 5 1 95A 1 Hanumarahalli Gundur Shevalalpur Jakkankatti Motalli Bevinahalli BasavanakoppaHosur Kaliwal Shivapur Hosa Neeralgi-M-Karadgi (New) Kadakola Kerikop Chakapur 93 Khursapur Savanur (TMC) Bhairapur Gudisalkoppa Bhadrapur KonankeriNeeralakatti Chiknellur Savanur (RURAL) SAVANUR Hunshikatti Bisanhalli Teggihalli Kalalkond Ichangi MeundiTaredahalli Hottur Jallapur Bailmadapura Chandapur Kalyan NandihalliMannur Hattimattur Krishnapur Gudur Munavalli Mulkeri Nidagundi 94 Halagi Neeralagi-M-Guttal Ibrahimpur Mavoor (Mahur) Hiremaralihalli -

Hot Pepper (Capsicum Spp.) – Important Crop on Guam

Food Plant Production June 2017 FPP-05 Hot Pepper (Capsicum spp.) – Important Crop on Guam Joe Tuquero, R. Gerard Chargualaf and Mari Marutani, Cooperative Extension & Outreach College of Natural & Applied Sciences, University of Guam Most Capsicum peppers are known for their spicy heat. Some varieties have little to no spice such as paprika, banana peppers, and bell peppers. The spice heat of Capsicum peppers are measured and reported as Scoville Heat Units (SHU). In 1912, American pharmacist, Wilbur Scoville, developed a test known as the, Scoville Organoleptic Test, which was used to measure pungency (spice heat) of Capsicum peppers. Since the 1980s, pungency has been more accurately measured by high-performance liquid chromatography Source: https://phys.org/news/2009-06-domestication- (HPLC). HPLC tests result in American Spice Trade capsicum-annuum-chile-pepper.html Association (ASTA) pungency units. ASTA pungency Introduction units can be converted to SHU. Table 2 displays Sco- Hot pepper, also known as chili, chilli, or chile pepper, ville Heat Units of various popular Capsicum peppers is a widely cultivated vegetable crop that originates (Wikipedia, 2017). from Central and South America. Hot peppers belong to the genus Capsicum. There are over 20 species under the genus Capsicum. There are five major domesticated species of peppers that are commercially cultivated (Table 1), and there are more than 50,000 varieties. Fig. 1 depicts a unqiue, citrus-flavored variety of Capsicum baccatum hot pepper, known as Lemon Drop (aji-type), popular for seasoning in Peru (Wikipedia, 2017). Table 1. The five major domesticated Capsicum species of pepper with examples of commonly known types of pepper. -

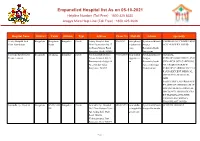

Empanelled Hospital List As on 02-09-2021

Empanelled Hospital list As on 05-10-2021 Helpline Number (Toll Free) : 1800 425 8330 Arogya Mitra Help Line (Toll Free) : 1800 425 2646 Hospital Name District Taluk Division Type Address Phone No Mail-ID Scheme Speciality Trinity Hospital And Bengaluru Bengaluru Bangalore Private Trinity Hospital And 41503434 trinityhospit Ayushman Bharat - CARDIOLOGY,CARDIOTHOR Heart Foundation South Heart Foundation No 27 al@hotmail. Arogya ACIC SURGERY,COVID Sri Rama Mandir Road com Karnataka,Jyothi Bangalore South 560004 Sanjeevini Narayana Hrudayalaya Bengaluru ANEKAL Bangalore Private Narayana Hrudayalaya 9980528300 samconhblr Ayushman Bharat - GENERAL Private Limited Private Limited 258 A @gmail.co Arogya SURGERY,OBSTETRICS AND Bommasandra Industrial m Karnataka,Jyothi GYNAECOLOGY,CARDIOLO Area Anekal Taluk Sanjeevini,Organ GY,CARDIOTHORACIC Bangalore 560099 Transplantion SURGERY,CARDIOVASCULA R SURGERY,ENT,MEDICAL ONCOLOGY,NEONATAL AND PAEDIATRICS,NEUROSURGE RY,ORTHOPAEDICS,RADIAT ION ONCOLOGY,SURGICAL ONCOLOGY,UROLOGY,HEA RT TRANSPLANT,LIVER TRANSPLANT,KIDNEY TRANSPLANT,COVID Samrudhi Eye Hospital Bengaluru BANGALO Bangalore Private Samrudhi Eye Hospital 8042075944 samruddhie Ayushman Bharat - OPHTHALMOLOGY RE No 2 Near Fortuna Vista yehospital@ Arogya Karnataka Apt Kodigehalli Main gmail.com Road Thindlu Vidyaranyapura Post Bangalore West 560097 Page 1 Empanelled Hospital list As on 05-10-2021 Helpline Number (Toll Free) : 1800 425 8330 Arogya Mitra Help Line (Toll Free) : 1800 425 2646 Hospital Name District Taluk Division Type Address Phone