24September 2020 India Daily

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nominee List

NOMINEE LIST Best financial reporting (large cap) Cipla Hindalco Industries Hindustan Unilever Infosys Kotak Mahindra Bank Mahindra & Mahindra Piramal Enterprises Tata Steel Vedanta Best financial reporting (small to mid-cap) CEAT Everest Industries Hikal Hindustan Foods IIFL Holdings KEC International Minda Industries Raymond The Phoenix Mills Zensar Technologies Best investor meetings (large cap) Bharti Airtel Hindustan Unilever Infosys Lupin Mahindra & Mahindra Piramal Enterprises Best investor meetings (mid-cap) Balkrishna Industries IIFL Holdings Mindtree RPG Group Sterlite Technologies The Phoenix Mills NOMINEE LIST Best investor meetings (small cap) Amber Enterprises India Equitas Holdings Greenlam Industries Music Broadcast Navin Fluorine International NOCIL Raymond Zensar Technologies Best investor relations officer (large cap) Bharti Airtel Komal Sharan Bharti Airtel Aparna Vyas Garg Bharti Infratel Surabhi Chandna Cipla Naveen Bansal HDFC Conrad D'Souza Hindustan Unilever Suman Hegde Infosys Sandeep Mahindroo Kotak Mahindra Bank Nimesh Kampani Lupin Arvind Bothra Best investor relations officer (small to mid-cap) CEAT Pulkit Bhandari Jindal Steel & Power Nishant Baranwal Motilal Oswal Financial Services Rakesh Shinde PNB Housing Finance Deepika Gupta Padhi Raymond J Mukund RPG Group Pulkit Bhandari Schneider Electric Infrastructure Vineet Jain The Phoenix Mills Varun Parwal NOMINEE LIST Best investor relations team (large cap) Bharti Airtel Cipla Hindustan Unilever Infosys Kotak Mahindra Bank Larsen & Toubro Infotech Power -

Ultratech Corporate Dossier August

INDIA'S LARGEST CORPORATE CEMENT DOSSIER COMPANY Stock code: BSE: 532538 NSE: ULTRACEMCO Reuters: UTCL.NS Bloomberg: UTCEM IS / UTCEM LX Contents ADITYA BIRLA OPERATIONAL ECONOMIC INDIAN CEMENT ULTRATECH GROUP- AND FINANCIAL ENVIRONENT SECTOR LANDSCAPE OVERVIEW PERFORMANCE GLOSSARY Mnt – Million Metric tons Lmt – Lakhs Metric tons MTPA – Million Tons Per Annum MW – Mega Watts Q1 – April-June Q4 – January-March CY – Current year period LY – Corresponding Period last Year FY – Financial Year (April-March) ROCE – Return on Average Capital Employed ROIC – Return on Invested Capital 2 Note: The financial figures in this presentation have been rounded off to the nearest ` 1 cr. 1 US$ = ` 64.46 ADITYA BIRLA GROUP - OVERVIEW Aditya Birla Group – Overview Premium global US$ ~41 billion Corporation conglomerate In the League of Fortune 500 Operating in 36 countries with over 50% Group revenues from overseas Anchored by about 120,000 employees from 42 nationalities Ranked No. 1 corporate in the Nielsen’s Corporate Image Monitor FY15 # 1 cement player in India by Capacity A global metal powerhouse – 3rd biggest # 4 largest cement producers globally producers of primary aluminum in Asia (ex China) # 1 in viscose staple fibre in globally # 2 player in viscose filament yarn in India Globally 5th largest producer of acrylic Globally 4th largest producer of insulators fibre A leading player in life insurance and AM Indian Listed Entities Entities Listed Indian # 3 cellular operator in India Top fashion and lifestyle player in India Among top 2 supermarket chains in retail in India Our Values Integrity Commitment Passion Seamlessness Speed 4 UltraTech Cement India’s largest cement company No. -

Birla Group Holdings Private Limited: Rating Reaffirmed, Rated Amount Enhanced for Commercial Paper Programme

May 27, 2021 Birla Group Holdings Private Limited: Rating reaffirmed, rated amount enhanced for Commercial Paper Programme Summary of rating action Previous Rated Current Rated Instrument* Amount Amount Rating Action (Rs. crore) (Rs. crore) Commercial Paper (CP) Programme 3,500 4,000 [ICRA]A1+; assigned / reaffirmed Non-convertible debentures programme 500 0 [ICRA]AA- (stable); reaffirmed and withdrawn Non-convertible debentures programme 1,000 1,000 [ICRA]AA- (stable); reaffirmed Total 5,000 5,000 *Instrument details are provided in Annexure-1 Rationale The ratings factor in the position of Birla Group Holdings Private Limited (BGHPL) as one of the main holding companies of the Aditya Birla Group. The ratings factor in the company’s equity ownership of listed Group entities including Grasim Industries Limited (rated [ICRA]AAA(Stable)/A1+), Aditya Birla Capital Limited (rated [ICRA]AAA(Stable)/A1+), Aditya Birla Fashion and Retail Limited (rated [ICRA]AA(Stable) /A1+) and Hindalco Industries Limited. The ratings also factor in the company’s adequate liquidity position backed by the market value of its holdings in listed Group entities and its strategic holdings in non-listed Group companies (including other Group holding companies). Further, ICRA expects the Group to extend capital support to BGHPL, as and when required. The ratings are constrained by the standalone financials of the company and the negative net worth on its balance sheet. The outlook is Stable for the company. ICRA has reaffirmed and withdrawn the rating outstanding on non-convertible debenture programmes of BGHPL aggregating Rs. 500 crore in line with request received from the company. -

Hindalco Industries Launches India's First All-Aluminium Freight Trailer

ADITYA BIRLA HINDALCO December 4, 2019 BY PORTAL BSE Limited National Stock Exchange of India Phiroze Jeejeebhoy Towers Limited Dalal Street Exchange Plaza, 5th Floor Mumbai: 400 001 Plot No. C/1, G Block Bandra Kurla Complex Scrip Code: 500440 Bandra (East), Mumbai - 400 051 Scrip Symbol: HINDALCO Banque Internationale A Luxembourg SocieteAnonyme 69, Route Esch L-2953; Luxembourg Fax No. 00352 4590 2010 Tel. 00 352 4590-1 Dear Sirs, Sub: Press Release — Hindalco Industries launches India's first All-Aluminium Freight Trailer Ref: Regulation 30 of Securities Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 We enclosed herewith a press release dated December 04, 2019 on the above subject, which is self- explanatory. This is for the information of your members and all concerned. Thanking you, Yours faithfully, For indalco Industries Limited r tvevmw C) to Anil ik President & Company Secretary Encl: as above Hindalco Industries Limited. 6th "lth & / Floor, Birla Centurion, Pandurang Budhkar Marg, Worli, Mumbai — 400030, India T:+91 22 66626666/62610555 I F:+912262610400/62610500 I W: www.hindalco.com Registered Office : Ahura Centre, 1st Floor, B wing, Mahakali Caves Road, Andheri (East), Mumbai — 400093, India Corporate ID No: L27020MH1958PLC011238 Hindalco Industries Limited launches India’s first All-Aluminium freight trailer Jaipur, 04 December 2019: Hindalco Industries Limited, a global leader in aluminium and copper, launched India’s’ first all-aluminium freight trailer in Jaipur, Rajasthan. Shri Udai Lal Anjana, Honourable Minister of Co-operative and IGNP, and Shri Pratap Singh Khachariyawas, Honourable Minister of Transport, Govt. of Rajasthan, along with Mr. -

Franklin India Fund LU1212701376 31 August 2021

Franklin Templeton Investment Funds India Equity Franklin India Fund LU1212701376 31 August 2021 Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund USD Performance over 5 Years in Share Class Currency (%) Total Net Assets (USD) 1,44 billion Franklin India Fund A (acc) EUR-H1 MSCI India Index-NR in USD Fund Inception Date 25.10.2005 190 Number of Issuers 45 170 Benchmark MSCI India Index-NR 150 Morningstar Category™ Other Equity 130 Summary of Investment Objective The Fund aims to achieve long-term capital appreciation by 110 principally investing in equity securities of companies of any size located or performing business predominately in India. 90 Fund Management 70 Sukumar Rajah: Singapore 50 08/16 02/17 08/17 02/18 08/18 02/19 08/19 02/20 08/20 02/21 08/21 Asset Allocation Discrete Annual Performance in Share Class Currency (%) 08/20 08/19 08/18 08/17 08/16 08/21 08/20 08/19 08/18 08/17 A (acc) EUR-H1 50,51 -1,01 -13,58 -3,55 9,44 Benchmark in USD 53,15 3,00 -7,64 7,12 17,46 % Performance in Share Class Currency (%) Equity 103,05 Cumulative Annualised Cash & Cash Equivalents -3,05 Since Since 1 Mth 3 Mths 6 Mths 1 Yr 3 Yrs 5 Yrs Incept 3 Yrs 5 Yrs Incept A (acc) EUR-H1 7,78 9,87 19,92 50,51 28,75 35,90 46,91 8,79 6,33 6,24 Benchmark in USD 10,94 11,12 22,35 53,15 45,68 83,30 84,41 13,36 12,89 10,11 Calendar Year Performance in Share Class Currency (%) 2020 2019 2018 2017 2016 A (acc) EUR-H1 9,54 4,01 -17,74 34,53 0,74 Benchmark in USD 15,55 7,58 -7,31 38,76 -1,43 Past performance is not an indicator or a guarantee of future performance. -

Grasim Industries Standalone Profitability Comes Under Pressure Stock Update Stock

Grasim Industries Standalone profitability comes under pressure Stock Update Stock Sector: Diversified Grasim Industries Limited’s (Grasim) adjusted standalone net profit declined by 35.5% y-o-y to Rs. 526.5 crore on account of weak Result Update operating profit margin (OPM) in both viscose and chemical divisions. The VSF division was affected by global capacity overhang, elevated Change further by U.S.-China trade war. Caustic soda also performed poorly on the operational front owing to increased domestic capacity and weak Reco: Hold demand. Exit prices for both VSF and caustic soda are lower, which is CMP: Rs. 734 expected to put pressure on its standalone operations. Going ahead, with its capacity expansion plans in both verticals, the company expects Price Target: Rs. 803 to see gradual improvement in profitability. On the other hand, the key overhang on Grasim related to the funding of Vodafone Idea remains, as á Upgrade No change â Downgrade management would consider fund infusion at the time it arises. We have lowered our standalone estimates for FY2020-FY2021, factoring weak profitability in the VSF and chemical divisions. On account of increasing Company details losses in Vodafone Idea, its rising funding requirements and little clarity Market cap: Rs. 48,293 cr emerging from Grasim’s management on funding Vodafone Idea, we continue to maintain our Hold rating on the stock with an unchanged 52-week high/low: Rs. 959/636 SOTP-based price target (PT) of Rs. 803. Key Positives NSE volume: (No of 19.0 lakh shares) Lower pulp prices benefits to be visible in VSF profitability in the coming quarters. -

Annual-Report-Utcl-2019-20.Pdf

The Chairman’s Letter to Shareholders Dear Shareholder, COVID-19 and the associated lockdowns across countries have triggered a once-in-a-century crisis for the society and the economy in 2020. January now seems like a month of a bygone era – such has been the enormity of change. This is a defining period in human and business history: one that will test the resilience of individuals, societies, corporations, and nations. Given the fog of uncertainty all around, it is hard to be prescient in these times. But there is little doubt on one reality: companies with quality leadership, sound business fundamentals, and a track record of winning in turbulent times, will emerge as champions in the new global order. Mr. Aditya Vikram Birla Global Economy It has been several months since the pandemic engulfed the world and yet there is a lot of uncertainty We live by his values. with respect to the extent of the economic contraction due to this Integrity, Commitment, crisis, and the subsequent pace of Passion, Seamlessness recovery. This year will see an economic and Speed. contraction, but this 2020 recession is turning out very different from the past recessions. It has been too 01-35 Corporate Overview 2 36-133 Statutory Reports 3 134-320 Financial Statements UltraTech Cement Limited Annual Report 2019-20 confidence. Some sectors, like airlines and zones during the lockdown, where economic strengthening its business relationships. hospitality, will take time to recover fully. activity remained severely constrained. The Aditya Birla Group is also closely And some supply chain disruption effects Correspondingly, India’s GDP is likely to examining the evolving changes in the will linger. -

View Corporate Brochure

next | contents GREENER STRONGER SMARTER previous | next | contents Contents The Materials that Build the Future 02 Customers as Business Partners 04 The Hindalco Growth Story & Metals Flagship of a Global Conglomerate 05 Local & Global Advantages 07 Hindalco Aluminium : Manufacturing Excellence 09 Robust Growth in Flat Rolled & Extruded Products 16 Major Aluminium Brands 17 Novelis Aluminium 18 Hindalco in Speciality Alumina 20 Hindalco Copper 26 Sustainability Framework 32 Research & Development 36 People at the Core 42 Reaching out to Communities 46 From islands of Excellence to a World of Excellence 54 Offices 55 Growing Worldwide Presence — India Map I — World Map II Across the Metals Value Chain — The Making of Aluminium III Across the Metals Value Chain — The Making of Copper IV previous | next GREENER STRONGER SMARTER THE MATERIALS THAT BUILD THE FUTURE Hindalco produces materials that create a The metals from Hindalco, namely, aluminium greener, stronger, smarter, world. Its products and copper are green in more ways than one. sustain the environment, power the global Their use in electric vehicles or solar panels economy and offer smart solutions for today contribute to a sustainable planet. and the future. From mining to manufacturing, Hindalco cares From infrastructure to aeronautics to seafaring for the environment at every stage. Combining vessels, Hindalco products find applications advantages of lightweight and strength, across land, sea and air. From new generation recyclability and manufacturing excellence, automobiles to aerospace and bullet trains, strong research and development capability to innovations like tempered glass for the and a global talent pool, Hindalco today is transformational mobile communication big in your life. -

Aban Offshore ABG Shipyard ACC Limited Adani Group Aditya Birla

A . Aban Offshore . Amul[8] . ABG Shipyard . Andhra Bank . ACC Limited . Apollo Hospitals[9] . Adani Group . Apollo Tyres[10] . Aditya Birla Group.[2] . Archies Greetings & Gifts Ltd[11] . Ador Powertron Limited[3] . Aptech . Aftek . Arvind Mills . Air India[4] and subsidiary Air-India Express[5] . Ashok Leyland[12] . Air Sahara[6] . Asia Motor Works . Ajanta Group . Asian Paints[13][14] . Alang Ship Recycling Yard[7] . Axis Bank . Allahabad Bank . Ambuja Cements . Amrutanjan Healthcare [edit]B . Bajaj Auto[15] . Bhushan Steel . Balaji Telefilms[16] . Biocon . Bank of India[15] . BMR Advisors[21] . Bank of Baroda[17] . Bombay Dyeing[22] . Bharat Aluminium Company[18] . BPL group[23] . Bharat Electronics Limited[19] . Ballarpur Industries Limited[24] . Bharat Forge[20] . Bharat Earth Movers Limited . Bharat Heavy Electricals Limited[15] . Britannia Industries[25] . Bharat Petroleum[15] . BirlaSoft . Bharat Sanchar Nigam Limited . Bharati Shipyard . Bharti Airtel [edit]C . Camlin Ltd. Coal India Limited[31] . CMC Limited[26] . Container Corporation of India . Canara Bank[15] . Crest Animation Studios[32] . Cellebrum Technologies Limited[27] . Crompton Greaves . Central Bank of India . Cadila Healthcare[33] . CESC . Coromandel International[34] . CPCL . Catholic Syrian Bank . Cipla[28] . Cosmic Circuits . Club Mahindra Holidays[29] . Covansys India Limited[30] [edit]D . Dabur India Limited[35] . Dr. Reddy's . Damodar Valley Corporation[36] Laboratories[40] . Deccan Aviation Pvt. Ltd.[37][38] is an aviation company that operates Air . DLF Universal Limited Deccan . Directi . Delhi Metro Rail Corporation Limited[39] [edit]E . Educomp Solutions . Essar Group[44] . Eicher Motors[41] . Eureka Forbes . Engineers India Limited[42] . EID Parry . English Indian Clays Limited[43] . Evalueserve[45] . Escorts Group . -

Annexure 1B 18416

Annexure 1 B List of taxpayers allotted to State having turnover of more than or equal to 1.5 Crore Sl.No Taxpayers Name GSTIN 1 BROTHERS OF ST.GABRIEL EDUCATION SOCIETY 36AAAAB0175C1ZE 2 BALAJI BEEDI PRODUCERS PRODUCTIVE INDUSTRIAL COOPERATIVE SOCIETY LIMITED 36AAAAB7475M1ZC 3 CENTRAL POWER RESEARCH INSTITUTE 36AAAAC0268P1ZK 4 CO OPERATIVE ELECTRIC SUPPLY SOCIETY LTD 36AAAAC0346G1Z8 5 CENTRE FOR MATERIALS FOR ELECTRONIC TECHNOLOGY 36AAAAC0801E1ZK 6 CYBER SPAZIO OWNERS WELFARE ASSOCIATION 36AAAAC5706G1Z2 7 DHANALAXMI DHANYA VITHANA RAITHU PARASPARA SAHAKARA PARIMITHA SANGHAM 36AAAAD2220N1ZZ 8 DSRB ASSOCIATES 36AAAAD7272Q1Z7 9 D S R EDUCATIONAL SOCIETY 36AAAAD7497D1ZN 10 DIRECTOR SAINIK WELFARE 36AAAAD9115E1Z2 11 GIRIJAN PRIMARY COOPE MARKETING SOCIETY LIMITED ADILABAD 36AAAAG4299E1ZO 12 GIRIJAN PRIMARY CO OP MARKETING SOCIETY LTD UTNOOR 36AAAAG4426D1Z5 13 GIRIJANA PRIMARY CO-OPERATIVE MARKETING SOCIETY LIMITED VENKATAPURAM 36AAAAG5461E1ZY 14 GANGA HITECH CITY 2 SOCIETY 36AAAAG6290R1Z2 15 GSK - VISHWA (JV) 36AAAAG8669E1ZI 16 HASSAN CO OPERATIVE MILK PRODUCERS SOCIETIES UNION LTD 36AAAAH0229B1ZF 17 HCC SEW MEIL JOINT VENTURE 36AAAAH3286Q1Z5 18 INDIAN FARMERS FERTILISER COOPERATIVE LIMITED 36AAAAI0050M1ZW 19 INDU FORTUNE FIELDS GARDENIA APARTMENT OWNERS ASSOCIATION 36AAAAI4338L1ZJ 20 INDUR INTIDEEPAM MUTUAL AIDED CO-OP THRIFT/CREDIT SOC FEDERATION LIMITED 36AAAAI5080P1ZA 21 INSURANCE INFORMATION BUREAU OF INDIA 36AAAAI6771M1Z8 22 INSTITUTE OF DEFENCE SCIENTISTS AND TECHNOLOGISTS 36AAAAI7233A1Z6 23 KARNATAKA CO-OPERATIVE MILK PRODUCER\S FEDERATION -

NSE Symbol NSE 6 Month Avg Total Market

Average Market Cap of 200 listed companies on BSE & NSE for the six months ended 30 June 2021 BSE 6 month Avg NSE 6 month Avg Average of BSE and NSE 6 Total Market Cap Total Market Cap month Avg Total Market Cap S.No. Company Name ISIN BSE SYMBOL (Rs. In Crs.) NSE Symbol (Rs. In Crs.) (Rs. in Crs.) 1 Reliance Industries Ltd INE002A01018 RELIANCE 1338017.01 RELIANCE 1355067.509 1346542.26 Tata Consultancy Services 2 Ltd. INE467B01029 TCS 1169783.56 TCS 1173068.166 1171425.86 3 HDFC Bank Ltd. INE040A01034 HDFCBANK 819037.95 HDFCBANK 818713.671 818875.81 4 Infosys Ltd INE009A01021 INFY 579784.19 INFY 579697.3885 579740.79 5 Hindustan Unilever Ltd., INE030A01027 HINDUNILVR 549336.78 HINDUNILVR 549358.908 549347.84 Housing Development 6 Finance Corp.Lt INE001A01036 HDFC 462288.58 HDFC 461373.1089 461830.84 7 ICICI Bank Ltd. INE090A01021 ICICIBANK 416645.51 ICICIBANK 416389.0234 416517.27 8 Kotak Mahindra Bank Ltd. INE237A01028 KOTAKBANK 361640.52 KOTAKBANK 361438.6361 361539.58 9 State Bank Of India, INE062A01020 SBIN 329767.32 SBIN 329789.268 329778.29 10 Bajaj Finance Limited INE296A01024 BAJFINANCE 324996.53 BAJFINANCE 324843.5005 324920.02 11 Bharti Airtel Ltd. INE397D01024 BHARTIARTL 299981.36 BHARTIARTL 299955.7729 299968.57 12 HCL Technologies Ltd INE860A01027 HCLTECH 261400.46 HCLTECH 261392.0109 261396.24 13 Wipro Ltd., INE075A01022 WIPRO 258617.45 WIPRO 261102.3994 259859.92 14 ITC Ltd INE154A01025 ITC 259423.16 ITC 259396.0648 259409.61 15 Asian Paints Ltd. INE021A01026 ASIANPAINT 253487.28 ASIANPAINT 253454.4536 253470.87 16 AXIS Bank Ltd. -

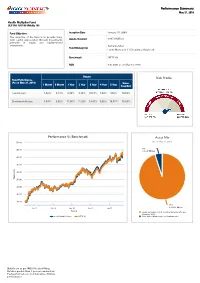

Risk Profile Performance Vs Benchmark Asset Mix Performance

Performance Summary May 31, 2019 Health Multiplier Fund ULIF 058 15/01/09 HMultip 105 Fund Objective: Inception Date January 15, 2009 The objective of the fund is to provide long- ₹ term capital appreciation through investments Assets Invested 687.4 Million primarily in equity and equity-related instruments. Sumanta Khan Fund Manager(s) Funds Managed: 11 (9 Equity, 2 Balanced) Benchmark NIFTY 50 NAV ₹ 42.0495 as on May 31, 2019 Return Risk Profile Fund Performance (As on May 31, 2019 ) Since 1 Month 6 Month 1 Year 2 Year 3 Year 4 Year 5 Year Inception Fund Return 1.82% 8.13% 6.74% 8.18% 10.67% 7.64% 10.6% 14.84% Benchmark Return 1.49% 9.62% 11.05% 11.32% 13.47% 9.02% 10.51% 15.24% Performance Vs Benchmark Asset Mix (As on May 31, 2019) 50.00 5% 45.00 ₹ 37.41 Million 40.00 35.00 ) ₹ 30.00 V in ( NA 25.00 20.00 15.00 10.00 95% Jan 10 Jan 12 Jan 14 Jan 16 Jan 18 ₹ 650.01 Million Period Equity and Equity related securities Minimum 80% and Maximum 100% Health Multiplier Fund NIFTY 50 Debt, Money Market and Cash Maximum 20% Details are as per IRDAI Product Filing. Returns greater than 1 year are annualized. Past performance is not indicative of future performance. Performance Summary May 31, 2019 % of Invested Top 10 Sectors * Assets Financial and insurance activities 24.30% Computer programming consultancy and related activities 13.52% Manufacture of coke and refined petroleum products 10.25% Infrastructure 8.57% Manufacture of chemicals and chemical products 6.35% Manufacture of tobacco products 5.72% Manufacture of Basic Metals 1.85% Manufacture of motor vehicles trailers and semi-trailers 1.73% Manufacture of pharmaceuticalsmedicinal chemical and botanical 1.60% products Manufacture of other non-metallic mineral products 1.57% OTHERS 24.54% *As per IRDAI NIC industry classification Details are as per IRDAI Product Filing.