Powerpoint Print Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Hyperlinks of Merchant Websites Will Bring to You to Another Website on the Internet, Which Is Published and Operated by a Third Party

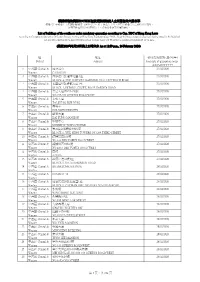

The hyperlinks of merchant websites will bring to you to another website on the Internet, which is published and operated by a third party. Such links are only provided on our website for the convenience of the Client and Standard Chartered Bank does not control or endorse such websites, and is not responsible for their contents. The use of such websites is also subject to the terms of use and other terms and guidelines, if any, contained within each such website. In the event that any of the terms contained herein conflict with the terms of use or other terms and guidelines contained within any such websites, then the terms of use and other terms and guidelines for such website shall prevail. Offers are applicable for Standard Chartered Visa Credit Card Offers are applicable for Standard Chartered Mastercard Offers are applicable for Standard Chartered UnionPay Dual Currency Platinum Credit Card Offers are applicable for Standard Chartered WorldMiles Card Merchants Offers Details and Merchant's Additional Terms and Conditions Contact Details (852) 2833 0128 BEE CHENG HIANG SHOP NO.1 GROUND FLOOR, YING KONG MANSION, NO. 2-6 10% off on regular-priced meat products upon spending of HK$300 or above YEE WO STREET, CAUSEWAY BAY Promotion period is from 1 Jan to 31 Dec 2017. (852) 2730 8390 SHOP C, G/F, DAILY HOUSE, Merchant website: http://www.bch.hk NO.35-37 HAIPHONG ROAD, TSIM SHA TSUI (852) 2411 0808 SHOP NO.2 GROUND FLOOR,NO. 60 SAI YEUNG CHOI STREET SOUTH, MONGKOK (852) 3514 4018 SHOP NO.B02-36, LANGHAM PLACE,NO.8 ARGYLE STREET, MONGKOK (852) 2362 0823 SHOP NO.E5,HUNG HOM STATION,HUNG HOM (852) 2357 077 SHOP NO.KWT 20 ,KWUN TONG STATION, KWUN TONG (852) 2365 2228 Shop B12, Basement 1, Site 5,(Aeon Dept Store)Whampoa Garden, Hung Hom, Kowloon (852) 2698 8310 SHOP NO. -

DDC Location Plan Apr-2015 Quarry Bay MTR Station Exit a Nam Cheong MTR Station Exit Training / Day Off Training / Day

WWF - DDC Location Plan Apr-2015 Mon Tue Wed Thu Fri Sat Sun 1 2 3 4 5 Team A Quarry Bay MTR Station Exit A Nam Cheong MTR Station Exit Training / Day Off Training / Day Off Training / Day Off Cheung Sha Wan Road, Lai Chi Kok Team B Yun Ping Road,Causeway Bay Training / Day Off Training / Day Off Training / Day Off (near Cheung Sha Wan Plaza) Wan Chai Pedestrian Footbridge Great George Street, Team C Citimall, Yuen Long Great George Street, Causeway Bay Great George Street, Causeway Bay (near Immigration Tower) Causeway Bay Wan Chai Pedestrian Footbridge Kornhill Road, Quarry Bay Team D Mei Foo MTR Station Exit A Mei Foo MTR Station Exit A Mei Foo MTR Station Exit A (near Immigration Tower) (near Jusco) Kornhill Road, Quarry Bay Tat Tung Road, Tung Chung Team E Tai Wai MTR Station Exit C Tai Wai MTR Station Exit C Tai Wai MTR Station Exit C (near Jusco) (near Bus Terminal) Tat Tung Road, Tung Chung Team F Long Ping MTR Station Exit B2 Long Ping MTR Station Exit B2 Long Ping MTR Station Exit B2 (near Bus Terminal) 6 7 8 9 10 11 12 Nathan Road, Prince Edward Ngau Tau Kok Road, Ngau Tau Kok Nathan Road, Tsim Sha Tsui Team A Training / Day Off Training / Day Off Great George Street, Causeway Bay (near Pioneer Centre) (near Municipal Services Building) (near St. Andrew Church) Kwai Fu Road, Kwai Chung Wai Man Road, Sai Kung Team B Training / Day Off Training / Day Off Kennedy Town MTR Station Exit C Quarry Bay MTR Station Exit A (near Kwai Chung Plaza) (near Bus Terminal) Connaught Place, Central Connaught Place, Central Connaught Place, Central -

Mon Tue Wed Thu Fri Sat Sun 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

WWF - DDC Location Plan May-2018 Mon Tue Wed Thu Fri Sat Sun 1 2 3 4 5 6 Team A Day-Off Tsuen Wan Plaza Diamond Hill MTR Exit A2 Lau Sin Street, Tin Hau King Man Street, Sai Kung (Near Sai Kung Library) Day-Off Hang Seng Bank Head Office, Central New Jade Shopping Centre, Chai Wan New Jade Shopping Centre, Chai Wan Team B Shatin Plaza Shatin Plaza Shatin Plaza (Near Footbridge) (Near Footbridge) (Near Footbridge) Hang Seng Bank Head Office, Central New Jade Shopping Centre, Chai Wan Team C Canal Road East Bridge, Causeway Bay Hong Kong MTR Station Yuen Long MTR Station Yuen Long MTR Station (Near Footbridge) (Near Footbridge) Hang Seng Bank Head Office, Central Team D Wu Kai Sha MTR Station Exit B Canal Road East Bridge, Causeway Bay Yuen Long MTR Station Tsuen Wan Plaza (Near Footbridge) Tsuen Wan Plaza (Near Footbridge) (Near Footbridge) World Wide House, Central World Wide House, Central Team E Tuen Mun MTR Station Wu Kai Sha MTR Station Exit B Canal Road East Bridge, Causeway Bay Tsuen Wan Plaza (Near Footbridge) (Near Footbridge) (Near Footbridge) World Wide House, Central Team F Causeway Bay Plaza 1 (Near Footbridge) Tuen Mun MTR Station Wu Kai Sha MTR Station Exit B Chai Wan MTR Station Chai Wan MTR Station (Near Footbridge) Team G Admiralty MTR Station Exit A Causeway Bay Plaza 1 (Near Footbridge) Tuen Mun MTR Station Chai Wan MTR Station Austin MTR Station Exit B (Near Footbridge) Austin MTR Station Exit B (Near Footbridge) Team H Tai Wai MTR Station Exit D Admiralty MTR Station Exit A Causeway Bay Plaza 1 (Near Footbridge) Austin -

繪drawing A-1 A/Yl/259

°Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 19.2.2020 §e (Extract from Applicant's Further A/YL/259 A-1 Information Submitted on 19.2.2020) °Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 21.4.2020 §e (Extract from Applicant's Further A/YL/259 A-2 Information Submitted on 21.4.2020) °Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 2.12.2019 §e (Extract from Applicant's Further A/YL/259 A-3 Information Submitted on 2.12.2019) °Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 27.3.2020 §e (Extract from Applicant's Further A/YL/259 A-4 Information Submitted on 27.3.2020) °Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 27.3.2020 §e (Extract from Applicant's Further A/YL/259 A-5 Information Submitted on 27.3.2020) °Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 2.12.2019 §e (Extract from Applicant's Further A/YL/259 A-6 Information Submitted on 2.12.2019) °Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 2.12.2019 §e (Extract from Applicant's Further A/YL/259 A-7 Information Submitted on 2.12.2019) °Ñ¦Ò REFERENCE No. ø DRAWING (ºK¿ý¦Û¥Ó½Ð¤H©ó 2.12.2019 §e (Extract from Applicant's Further A/YL/259 A-8 Information Submitted on 2.12.2019) °Ñ¦Ò REFERENCE No. -

REGULATION Compulsory Testing No

G.N. (E.) 15 of 2021 PREVENTION AND CONTROL OF DISEASE (COMPULSORY TESTING FOR CERTAIN PERSONS) REGULATION Compulsory Testing Notice I hereby exercise the power conferred on me by section 10(1) of the Prevention and Control of Disease (Compulsory Testing for Certain Persons) Regulation (the Regulation) (Chapter 599, sub. leg. J) to:— Category of Persons (I) specify the following category of persons:— (a) any person who had been present on any of the following premises in any capacity (including but not limited to residents, visitors and workers) for more than 2 hours at any time during the period from 27 December 2020 to 9 January 2021:— (1) Block 3 of Sun Yuen Long Centre, 8 Long Yat Road, Yuen Long, New Territories, Hong Kong; (2) King Lai House of Shan King Estate, 1 Ming Kum Road, Tuen Mun, New Territories, Hong Kong; (b) any person who had been engaged to work or had been present for more than 2 hours at the construction sites for contract number HY/2018/08—Central Kowloon Route— Central Tunnel at any time during the period from 3 January to 9 January 2021; Requirements and Procedure for the Test (II) require every person who falls within the above category [Note 1] to undergo a polymerase chain reaction-based nucleic acid test for the coronavirus disease 2019 (the Specified Test) in compliance with the requirements and procedure set out below:— (a) for a test at mobile specimen collection stations:— (i) attend one of the mobile specimen collection stations [Note 2] set up by the Government on or before 12 January 2021; (ii) undergo -

Yuen Long Centre

Environmental Central Facility Air Ventilation Assessment study Institute for the Environment Sun Yuen Long Centre Air Ventilation Assessment Study Sun Yuen Long Centre Site Environmental Central Facility/Institute for the Environment Page 1 HKUST Environmental Central Facility Air Ventilation Assessment study Institute for the Environment Sun Yuen Long Centre Table of Content 1. INTRODUCTION ...........................................................................................................3 1.1 Background and Objectives ................................................................................3 1.2 Site Environs .......................................................................................................3 1.3 General Features Affecting the Wind Environment ............................................4 2. DESIGN SCHEME UNDER DETAILED STUDY........................................................4 2.1 Design Scheme....................................................................................................4 3. ASSESSMENT APPROACH..........................................................................................5 3.1 General ................................................................................................................5 4. SUMMARY OF RESULTS AND DISCUSSION...........................................................6 5. Future Prospect ................................................................................................................7 6. Disclaimer........................................................................................................................8 -

Review of Operations

Review of Operations 21 Property Sales 64 Property Related Businesses 22 Hong Kong Property Business 71 Telecommunications and Information Technology 22 Land Bank 72 Transportation, Infrastructure and Logistics 24 Property Development 34 Property Investment 75 Corporate Finance 44 Mainland Property Business 76 Customer Service 44 Land Bank 46 Property Development 60 Property Investment The Group’s International Commerce Centre and International Finance Centre form a magnificent Victoria Harbour Gateway SUN HUNG KAI PROPERTIES LIMITED 20 Annual Report 2009/10 Property Sales The Group sold or pre-sold an attributable HK$23,218 million worth of properties in the third quarter of 2010, mainly from Hong Kong of properties in the year under review, compared to last year’s properties including Lime Stardom in Kowloon and Larvotto in HK$25,674 million. A number of projects in Hong Kong and on the Island South. Nearly 95 per cent of the units in these two projects mainland were put on the market over the past year and produced have been sold. highly encouraging sales. The Group will continue offering new developments for sale as Sales of Hong Kong properties amounted to HK$20,562 million, planned. Major residential projects in Hong Kong to go on sale in mostly from YOHO Midtown in Yuen Long, Aria and The Latitude the rest of the current financial year include luxury town houses in Kowloon and The Cullinan at Kowloon Station. The remaining Valais at Beas River, Avignon on Castle Peak Road, Park Nara and a HK$2,656 million was from mainland and Singapore properties, project on Po Yip Street in Yuen Long and the residential towers including Lake Dragon in Guangzhou and Orchard Residences in at the integrated landmark development at Tseung Kwan O Singapore. -

Building List 20200301.Xlsx

根據香港法例第599C章正在接受強制檢疫人士所居住的大廈名單 根據《若干到港人士強制檢疫規例》(第599C章),除了豁免人士外,所有在到港當日之前的14日期間, 曾在內地逗留任何時間的人士,必須接受14天的強制檢疫。 List of buildings of the confinees under mandatory quarantine according to Cap. 599C of Hong Kong Laws According to Compulsory Quarantine of Certain Persons Arriving at Hong Kong Regulation (Cap. 599C), except for those exempted, all persons having stayed in the Mainland for any period during the 14 days preceding arrival in Hong Kong will be subject to compulsory quarantine for 14 days. (截至2020年2月26日晚上11時59分 As at 11:59 p.m., 26 February 2020) 區 地址 檢疫最後日期 (日/月/年) District Address End date of quarantine order (DD/MM/YYYY) 1 中西區 Central & 加多近山 27/02/2020 Western CADOGAN 2 中西區 Central & 西摩道11號福澤花園A座 27/02/2020 Western BLOCK A, THE FORTUNE GARDENS, NO.11 SEYMOUR ROAD 3 中西區 Central & 花園道55號愛都大廈3座 27/02/2020 Western BLOCK 3, ESTORIL COURT, NO.55 GARDEN ROAD 4 中西區 Central & 皇后大道西355-359號 27/02/2020 Western NO.355-359 QUEEN'S ROAD WEST 5 中西區 Central & 泰成大廈 27/02/2020 Western TAI SHING BUILDING 6 中西區 Central & 高雲臺 27/02/2020 Western GOLDWIN HEIGHTS 7 中西區 Central & 啟豐大廈 27/02/2020 Western KAI FUNG MANSION 8 中西區 Central & 堅城中心 27/02/2020 Western KENNEDY TOWN CENTRE 9 中西區 Central & 第三街208號毓明閣1座 27/02/2020 Western BLOCK 1, YUK MING TOWERS, NO.208 THIRD STREET 10 中西區 Central & 德輔道西333號 27/02/2020 Western NO.333 DES VOEUX ROAD WEST 11 中西區 Central & 德輔道西408A號 27/02/2020 Western NO.408A DES VOEUX ROAD WEST 12 中西區 Central & 蔚然 27/02/2020 Western AZURA 13 中西區 Central & 羅便臣道74號1座 27/02/2020 Western BLOCK 1, NO.74 ROBINSON ROAD 14 中西區 Central & BRANKSOME -

List of Radio Dealer (Unrestricted) Licensees (As at 16/08/2021)

List of Radio Dealer (Unrestricted) Licensees 無線電商(放寬限制)持牌商名單 ( As at 16/09/2021) (截至 16/09/2021) Licensee Address Telephone Licence No. (Ex-Licence No.) 持牌商 地址 電話 牌照號碼 (原有牌照號碼) RM. G87, G/F, SINCERE PODIUM, , MONG KOK 1 + 1 九龍旺角先達廣場地下G87號舖 55926692 RU00231996-RU 188 TELECOM GROUP LIMITED RU00119316-RU 188 電訊集團有限公司 G/F, 188 APLIU ST, SHAM SHUI PO 35860072 (11931) 188 TELECOM O/B 188 TELECOM GROUP LIMITED 188電訊 O/B 188電訊集團有限公司 G/F, 209 APLIU ST, SHAM SHUI PO 23207788 RU00180442-RU 2626 LIMITED RM. /FLAT 1, 5/F, BLK A, HOI LUEN INDUSTRIAL CENTRE, 55 HOI YUEN ROAD, KWUN TONG 97804506 RU00158065-RU 28 FOOD (HK) LIMITED G/F, 204 FA YUEN STREET, MONG KOK 易發食品(香港)有限公司 九龍旺角花園街204號地下 26939008 RU00222985-RU 2DEEP INTERNATIONAL LIMITED 泰森國際貿易有限公司 RM. /FLAT A, 12/F, ZJ 300, 300 LOCKHART ROAD, WAN CHAI 51731646 RU00230817-RU 360 KIDS GUARD CO. LIMITED 2/F, YAU TAK BUILDING, 167 LOCKHART ROAD, WAN CHAI 21563920 RU00216069-RU 365 DAYS FREIGHT SERVICES (HK) LIMITED 5/F, BLK F, COMFORT BUILDING, 86-88A NATHAN ROAD, TSIM SHA TSUI +852 62213657 RU00220056-RU 3M HONG KONG LTD RU00132097-RU 三M香港有限公司 38/F, MANHATTAN PLACE, 23 WANG TAI ROAD, KOWLOON BAY 28066111 (13209) 4&6 TELECOM LIMITED RM. /FLAT 01, 11/F, HANG SENG CASTLE PEAK RD BLDG, 339 CASTLE PEAK RD, CHEUNG SHA WAN +852 66493320 RU00202666-RU 409 SHOP RU00128365-RU 409專門店 RM. /FLAT D-E, 11/F, FLOURISH FOOD MFY CTR, 18 TAI LEE STREET, YUEN LONG 35860967 (12836) 4PX EXPRESS CO., LIMITED RU00129432-RU 遞四方速遞有限公司 G/F, 167-169 HOI BUN ROAD, KWUN TONG 29772988 (12943) 5 CELL RM. -

Acrobat Document

As at 15 March 2021 Service Boundary of Integrated Home Care Services Teams (Ordinary Cases) in Central & Western District No. Agency Service Unit Address Phone / Fax Service Boundary 1 St. James’ Central & Western 11/F., Sheung Wan 2805 1256, Admiralty, Central, Sheung Wan, Mid-levels,Sai Ying Pun Settlement Integrated Home Care Municipal Bldg., 345 2805 1257 / (Connaught Road West all numbers, Des Voeux Road West from Services Team Queen’s Road Central , 2851 6557 number 1 to 408 ),Centre Street (all odd numbers, even numbers Hong Kong. from 2 to 40),Queen’s Road West (odd numbers from 1 to 451 even numbers from 2 to 290), Western Street (even numbers from 2 to 22), Water Street (numbers from 1 to 3), First Street (odd numbers from 1 to 55, even numbers from 2 to 60), Second Street (odd numbers from 1 to 55, even numbers from 2 to 32), Third Street (odd numbers from 1 to 61, even numbers from 2 to 54), High Street (odd numbers from 1 to 51, even numbers from 2 to 44), Mid-levels (Boham Road odd numbers from 1 to 31, all even numbers), Caine Road (all numbers) 1 As at 15 March 2021 No. Agency Service Unit Address Phone / Fax Service Boundary 2 Hong Kong Family i) Sheung Wan Service i) G/F, Low Block, Grand 2546 3332 / Sai Ying Pun, Centre Street (even numbers from 42 to 62), Queen Welfare Society Centre Millennium Plaza, 181 to 2167 8987 Road West (odd numbers from 453 onwards, even numbers 183 Queen’s Road from 292 to 504), Hing Hon Road (all numbers) Central, Hong Kong Western Street (all odd numbers, even numbers from 24 to 52) Water -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of buildings with confirmed / probable cases of COVID-19 List of residential buildings in which confirmed / probable cases have resided (Note: The buildings will remain on the list for 14 days since the reported date) Related confirmed / probable District Building name case number Yuen Long Yan Sau Wai 455 Kwun Tong Sau Wah House, Sau Mau Ping Estate 458 Yau Tsim Mong Shining Heights 459 Sai Kung Tower 9, Metro City Phase 2 460 Islands Twilight Court, Peninsula Village 461 Kwun Tong Block A, Hyde Towers 462 Southern Block B, Abba House 463 Central & Western Scholastic Garden 464 Central & Western 8 Kennedy Road 465 Yuen Long Block 4, Sun Yuen Long Centre 466 Wan Chai Block A, Elm Tree Towers 467 Central & Western Block 2, Villas Sorrento 468 Wan Chai OZO Wesley Hong Kong 469 Yau Tsim Mong YMCA 470 Tuen Mun Block 2, Sun Tuen Mun Centre 471 Tai Po Tower 2, Solaria 472 Yau Tsim Mong 392 Reclamation Street 473 Yau Tsim Mong The Luxe Manor 474 Sai Kung The Palisades 475 Southern 57 South Bay Road 476 Wan Chai Yick Shing Mansion 477 Sai Kung 5B, Wings At Sea, Lohas Park 478 Tsuen Wan Hoi Tsui Mansion, Riviera Gardens 480 Eastern 33 Kam Wa Street 481 Kwun Tong Dorsett Kwun Tong 482 Sha Tin Scenery Garden 483 Wong Tai Sin Ching Ming House, Tsz Ching Estate 484 1 Related confirmed / probable District Building name case number Southern L’ Hotel Island South 485 Sha Tin Courtyard by Marriott Hong Kong Sha Tin 486 Wan Chai OZO Wesley Hong Kong 487 Kwun Tong Hiu Tin House, Hiu Lai Court 488 Kwun Tong Hiu Tin House, Hiu Lai Court 489 Yuen Long -

Essential Public Infrastructure Works for the Yuen Long Section – Remaining Works

For discussion PWSC(1999-2000)82 on 5 January 2000 ITEM FOR PUBLIC WORKS SUBCOMMITTEE OF FINANCE COMMITTEE HEAD 706 - HIGHWAYS Transport – Roads 37TR - West Rail (phase 1) - essential public infrastructure works for the Yuen Long section – remaining works Members are invited to recommend to Finance Committee the upgrading of 37TR, entitled “West Rail (phase 1) - essential public infrastructure works for the Yuen Long section – remaining works” to Category A at an estimated cost of $32.0 million in money-of-the-day prices. PROBLEM The existing Long Yat Road and its junction with Castle Peak Road will not be able to cope with the future traffic demand upon the commissioning of the Yuen Long (YUL) Station of the West Rail (phase 1) in 2003 and the planned developments in the vicinity of the YUL Station. PROPOSAL 2. The Director of Highways (DHy), with the support of the Secretary for Transport, proposes to upgrade 37TR to Category A at an estimated cost of $32.0 million in money-of-the-day (MOD) prices for the construction of the essential public infrastructure works (EPIW) around the YUL Station of the Kowloon-Canton Railway Corporation (KCRC)’s West Rail (phase 1) project. / PROJECT ..... PWSC(1999-2000)82 Page 2 PROJECT SCOPE AND NATURE 3. The proposed scope of 37TR comprises - (a) widening of a section of Long Yat Road (east of the Sun Yuen Long Centre) from a 7.3-metre wide two- lane one-way southbound road to a 15-metre wide four-lane two-way road (3 southbound and 1 northbound lanes) and modification of the road junction of Long Yat Road/Castle Peak Road; and (b) indirect mitigation measures in the form of window insulation and air-conditioners for the Sun Yuen Long Centre, Block 5 dwellings with facades facing the roadworks in item (a) above.