Suntrusthome Developers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Conservatorship, Receivership and Liquidation Division

Republic of the Philippines Department of Finance INSURANCE COMMISSION l 071 United Nations Avenue Manila Conservatorship, Receivership and Liquidation Division A. Insurance Companies Under Conservatorship, Receivership and Liquidation As of 31 May 2020 NAME OF COMPANY DATE CEASE & APPOINTED ADDRESS CONTACT NUMBER DESIST CONSERVATOR/ ORDER (CDO) RECEIVER/ ISSUED LIQUIDATOR 1. AFISCO Insurance May 24, 1988 Atty. Rolando T. Devesa Block 136, Lot 14, Henry Ide St., 09178700414 Corp. Liquidator Katarungan Village Ph II Brgy. Poblacion Muntinlupa City 2. Algen Insurance Corp May 23, 2007 Insurance Commission Insurance Commission Bldg. 8523-8462 to 70 loc. 105 (formerly Acropolis By and thru Atty. John A. 1071 U. N. Avenue, Manila 8354-09-91 Central Guaranty Corp.) Apatan Ms. Irene S. Gaerlan Acting President 2nd flr 1250 bldg, 1250 Ex-Officio Liquidator North Edsa, Quezon City 3. BF Life Insurance July 20, 2015 Atty. Iris Sylvia Lucero BF Condominium A. Soriano Jr. 8527-4465 /86387618 Corporation Bonifacio Avenue Intramuros, Manila Liquidator 4. Bureau of Fire Jan. 4, 2018 Insurance Commission Insurance Commission Bldg. 8523-8462 to 70 Protection Mutual Aid and By and thru 1071 U. N. Avenue, Manila loc. 105 Beneficiary Association, Atty. Alwyn Franz P. Villaruel 8354-09-91 Inc. (“BFPMBAI) Ex-Officio Conservator 5. CAP General Insurance August 13, 2014 Atty. Rhodela Virginia V. Cap Building, 1 3rd Floor 126 Email: Corporation Garcia Amorsolo St., Legaspi Village Makati [email protected] Liquidator City 09178862000 6. CCC Insurance No CDO issued; Atty. Marilyn V. Gallanosa Unit 515, Pacific Century Tower 8990-3541 license not renewed Liquidator 1472-76 Quezon Avenue South since licensing year Triangle, Quezon City 2011-2012 7. -

CACHO Vice ~Tent for Finance and Corporate Information Officer

.. Empire- East July 10, 2013 Disclosure Department Philippine Stock Exchange, Inc. 3/F Tower One and Exchange Plaza Ayala Triangle, Ayala Avenue Makati Gty Attention: JANET A. ENCARNACION Head Gentlemen: We submit herewith the List of Top 100 Stockholders of Empire East Land Holdings, Inc. as ofJune 30,2013. Very truly yours, EVE Jhl~ CACHO Vice ~tent for Finance and Corporate Information Officer Empire East Land Holdings, Inc. 21 /F The World Centre, 330 Sen. Gil Puyat Avenue Extension, Mak.!ti City 1200, Philippines • Tels: (632) 867-8351 to 59 ·-------- ------------------ COMPANY NAME : EMPIRE EAST LAND HOLDINGS, INC. Page 1.00 LIST OF TOP 100 STOCKHOLDERS As Of June 30, 2013 OUTSTANDING & OUTSTANDING & TOTAL PERCENTAGE ISSUED SHARES ISSUED SHARES HOLDINGS TO STOCKHOLDER'S NAME (FULLY PAID) (PARTIALLY PAID)(SUBSCRIBED) TOTAL NATIONALITY ADDRESS MEGAWORLD CORPORATION 11,816,672,438.00 0.00 11,816,672,438.00 80 FILIPINO 28/F THE WORLD CENTRE 330 SEN. GIL PUYAT AVE., MAKATI CITY PCD NOMINEE CORPORATION (FILIPINO) 1,781,483,899.00 0.00 1,781,483,899.00 12 FILIPINO 37/F TOWER I, THE ENTERPRISE CENTER, 6766 AYALA AVE. COR. PASEO DE ROXAS, PCD NOMINEE CORPORATION (NON-FILIPINO) 646,214,491.00 0.00 646,214,491.00 4 NON-FILIPINO 37/F TOWER I, THE ENTERPRISE CENTER, 6766 AYALA AVE. COR. PASEO DE ROXAS, THE ANDRESONS GROUP INC. 138,133,820.00 0.00 138,133,820.00 1 FILIPINO 28/F THE WORLD CENTER 330 SEN GIL PUYAT AVE MAKATI CITY EMPIRE EAST LAND HOLDINGS, INC. 127,256,071.00 0.00 127,256,071.00 1 FILIPINO 21/F, THE WORLD CENTRE BUILDING 330 SEN. -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: March 7, 2016 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION ............................................................................................... 2 1.1 ALLOWED NATIONAL MARKS ....................................................................................................................................... 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: March 7, 2016 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application No. Filing Date Mark Applicant Nice class(es) Number 24 1 4/2010/00002075 February SPALDING SGG LISCO, LLC [US] 18 2010 19 CELEBRATIONS BY SHARON CUNETA- 2 4/2011/00011219 September 30 SHARON PANGILINAN [PH] 2011 28 August 3 4/2012/00010428 GRACE GRACE FOODS LIMITED [LC] 29; 30 and32 2012 28 DMCI PROJECT 4 4/2012/00012007 September TORRE DE MANILA 36 DEVELOPERS, INC. [PH] 2012 17 5 4/2012/00015244 December AFPRO ACS HOLDINGS B.V. [NL] 11; 24 and40 2012 1 October 29; 30; 31; 32 6 4/2012/00502545 JUJU FEELGOOD INC. [PH] 2012 and43 30 January FORBES TOWN MEGAWORLD 7 4/2013/00000997 36 and37 2013 CENTER CORPORATION [PH] 30 January GREENBELT PARK MEGAWORLD 8 4/2013/00000998 36 and37 2013 TOWER CORPORATION [PH] CHAMBER OF COSMETICS 18 March 9 4/2013/00002968 CCIP INDUSTRY OF THE PHILS., 45 2013 INC. [PH] 24 April SOCIÉTÉ DES PRODUITS 10 4/2013/00004732 30 2013 NESTLÉ S.A. -

1.1 Recordal of Change of Name/Address of Registrant

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < 20 October 2017 > Process/ Procedure Description Page 1 REGISTERED MARKS WITH PROCESSED REQUEST FOR RECORDAL (NATIONAL) 1.1 RECORDAL OF CHANGE OF NAME/ADDRESS OF REGISTRANT ......................................................................... 2 1.2 RECORDAL OF DEED OF ASSIGNMENT .................................................................................................................. 19 1.3 RECORDAL OF MERGER ............................................................................................................................................ 28 *Processed/Recorded as of September 2017 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date < 20 October 2017 > 1 REGISTERED MARKS WITH PROCESSED REQUEST FOR RECORDAL (NATIONAL) 1.1 RECORDAL OF CHANGE OF NAME/ADDRESS OF REGISTRANT Registration New Registrant Name / No. Mark Prior Registrant Name / Address Date of Recordal Number Address NACCO MATERIALS HANDLING HYSTER-YALE GROUP, INC. GROUP, INC. / 2902 N. E. [US] / 2902 N. E. CLACKAMAS 1 4/1960/00002848 HYSTER CLACKAMAS ST., 97208, 19 September 2017 ST., PORTLAND, OREGON, PORTLAND, 97208, United States of America United States of America FUJI JUKOGYO KABISHIKI KAISHA (ALSO TRADING AS SUBARU CORPORATION [JP] 2 4/1980/00039914 ROBIN FUJI HEAVY INDUSTRIES LTD. ) / 1-20-8, Ebisu, Shibuya-ku, 17 August 2017 / 1-20-8, Ebisu, Shibuya-ku, Tokyo, Japan Tokyo, Japan NEW BARBIZON FASHION, INC. NEW BARBIZON FASHION, / 401 VFP-MDC BLDG. 2, INC. [PH] / 2 Armela Compound 3 4/1981/00035291 MONA LISA VETERANS ROAD, VETERANS Road, Marcelo Green, 14 August 2017 CENTER , TAGUIG CITY, Parañaque, Metro Manila, Philippines Philippines NEW BARBIZON FASHION, INC. -

Contestable Customers As of March 2016 1 PHILIPPINE ECONOMIC ZONE AUTHORITY 2 14-678 PROPERTY HOLDINGS, INC

Contestable Customers as of March 2016 1 PHILIPPINE ECONOMIC ZONE AUTHORITY 2 14-678 PROPERTY HOLDINGS, INC. 3 18-2 PROPERTY HOLDINGS, INC 4 19-1 PROPERTY HOLDINGS, INC. 5 20-12 PROPERTY HOLDINGS, INC. 6 20-34 PROPERTY HOLDINGS. INC. 7 21ST CENTURY STEEL MILLS, INC 8 3-J PLASTICWORLD & MANUFACTURING CORP. 9 557 DRESSING PLANT/557 FEATHER MEAL CORP. 10 6-24 PROPERTY HOLDINGS, INC. 11 6-3 PROPERTY HOLDINGS, INC. 12 6776 AYALA AVENUE CONDOMINIUM CORPORATION 13 A. D. GOTHONG MANUFACTURING. CORP. 14 ABC DEVELOPMENT CORPORATION 15 ABS-CBN CORPORATION 16 ABS-CBN CORPORATION 17 ABSOLUT CHEMICALS 18 ACBEL POLYTECH(PHILIPPINES)INC 19 ACCUPRINT INCORPORATED 20 ACES AMC I.P.P.C/ MAGNOLIA 21 ACESITE (PHILS.) HOTEL CORPORATION 22 ACP TEST COMPANY, INC. 23 ADEBE REALTY COMPANY, INC. 24 ADEBE REALTY COMPANY, INC. 25 ADRIATICO CONSORTIUM, INC. 26 AEGIS PEOPLE SUPPORT REALTY CORPORATION 27 AFC FERTILIZER AND CHEMICALS, INC. 28 AFP GEH HQTRS SERV GRP 29 AFP HNDF PHIL ARMY 30 AGC FLAT GLASS PHILIPPINES, INC. 31 AICHI FORGING CO. OF ASIA, INC. 32 AIKAWA PHILIPPINES INC. 33 AIR EDUCATION AND TRAINING COMMAND-FAB 34 AIR LIQUIDE PHILIPPINES, INC. 35 AIR LIQUIDE PIPELINE UTILITIES 36 AIR LIQUIDE PIPELINE UTILITIES SERVICES, INC. 37 AIR LIQUIDE PIPELINE UTILITIES SERVICES, INC. 38 AIR TRANSPORTATION OFFICE (ILOILO INTERNATIONAL AIRPORT) 39 AJINOMOTO PHILIPPINES FLAVOR FOOD INC. 40 ALABANG COMMERCIAL CORPORATION 41 ALABANG COMMERCIAL CORPORATION 42 ALASCO VINYL CORPORATION 43 ALASKA MILK CORPORATION 44 ALBAY AGRO-INDUSTRIAL DEVELOPMENT CORPORATION 45 ALI MAKATI HOTEL PROPERTY, INC. 46 ALI/TONGCO, MA. CLAVEL G. 47 ALI-CII DEVELOPMENT CORPORATION 48 ALLEGRO MICROSYSTEMS PHILIPPINES,INC. -

Downloadable Annual Report Yes

CR02058-2016 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended Dec 31, 2015 2. SEC Identification Number 167423 3. BIR Tax Identification No. 000-477-103 4. Exact name of issuer as specified in its charter MEGAWORLD CORPORATION 5. Province, country or other jurisdiction of incorporation or organization Metro Manila 6. Industry Classification Code(SEC Use Only) 7. Address of principal office 28th Floor, The World Centre, 330 Sen. Gil Puyat Avenue, Makati City Postal Code 1227 8. Issuer's telephone number, including area code (632) 8678826 to 40 9. Former name or former address, and former fiscal year, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 32,239,445,872 Preferred 6,000,000,000 11. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange, Common Shares 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports) Yes No (b) has been subject to such filing requirements for the past ninety (90) days Yes No 13. -

Sec Form 17-C

http://edge.pse.com.ph/downloadHtml.do?file_id=112583 C00929-2015 SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2(c) THEREUNDER 1. Date of Report (Date of earliest event reported) Feb 27, 2015 2. SEC Identification Number 167423 3. BIR Tax Identification No. 000-477-103 4. Exact name of issuer as specified in its charter MEGAWORLD CORPORATION 5. Province, country or other jurisdiction of incorporation Metro Manila 6. Industry Classification Code(SEC Use Only) 7. Address of principal office 28th Floor, The World Centre, 330 Sen. Gil Puyat Avenue, Makati City, Philippines Postal Code 1227 8. Issuer's telephone number, including area code (632) 8678826 to 40 9. Former name or former address, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 32,231,457,948 Preferred 6,000,000,000 11. Indicate the item numbers reported herein Item 9(b) The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporat disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly t the Corporate Information Officer of the disclosing party. 1 of 2 2/27/2015 10:57 AM -

GIS-2015.Pdf

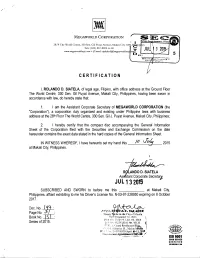

.. MEGAWORLD CORPORATION ' I ~. ~£~ 28/F The World Centre, 330 Sen. Gil Puyat Avenue, Makati City 120 , ~pp" es ~ Tels: (632) 867-8826 to 40 JU 3 201 ;pww.mq;aworldcop.com • E-maiL· iqf:>desk@mq;aworldcotp. >?mT S D .,-.---"~-.....::::;--J CERTIFICATION I, ROLANDO D. SIATELA, of legal age, Filipino, with office address at the Ground Floor The World Centre, 330 Sen. Gil Puyat Avenue, Makati City, Philippines, having been sworn in accordance with law, do hereby state that: 1. I am the Assistant Corporate Secretary of MEGA WORLD CORPORATION (the "Corporation"), a corporation duly organized and existing under Philippine laws with business address at the 28th Floor The World Centre, 330 Sen. Gil J. Puyat Avenue, Makati City, Philippines; 2. I hereby certify that the compact disc accompanying the General Information Sheet of the Corporation filed with the Securities and Exchange Commission on the date hereunder contains the exact data stated in the hard copies of the General Information Sheet. IN WITNESS WHEREOF, I have hereunto set my hand this __/_O_W_u--.::::~~-2015 at Makati City, Philippines. R ANDO D. SIATELA As tant Corporate Secreta~ JUL 13 2015 SUBSCRIBED AND SWORN to before me this at Makati City, Philippines, affiant exhibiting to me his Driver's License No. N-03-97-228950 expiring on 8 October 2017. Doc.No.J£; Page No. ; ll.lotmy !' blic in the City of Manila Book No. ; ffnl!• December Jl, ?.015 f"TR f·lrt B~Bi:1fi I hn. 05. 2015 . Series of 2015. l)'!' ~h '1!)25RVRoil No. 43135 ~ ''·' Fi. ~<; (hand Residc;1ce~ Bf4,g. -

Securities and Exchange Commission Sec Form 20-Is Information Statement Pursuant to Section 20 of the Securities Regulation Code

SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ ] Preliminary Information Statement [/] Definitive Information Statement 2. Name of Registrant as specified in its charter: SUNTRUST HOME DEVELOPERS, INC. 3. Province, country or other jurisdiction of incorporation or organization: METRO MANILA, PHILIPPINES 4. SEC Identification Number: 10683 5. BIR Tax Identification Code: 000-141-166-000 6. Address of Principal Office: 6th Floor, The World Centre Building, 330 Sen. Gil Puyat Avenue, Makati City, Metro Manila, Philippines 7. Registrant’s telephone number, including area code: (+632) 867-8826 to 40 8. Date, time and place of the meeting of security holders: 27 October 2015, 9:00 AM Eastwood Richmonde Hotel, Grand Ballroom Eastwood City, Bagumbayan, Quezon City, Metro Manila, Philippines 9. Approximate date on which the Information Statement is first to be sent or given to security holders: 06 October 2015 10. Securities registered pursuant to Sections 8 and 12 of the Code or Sections 4 and 8 of the RSA (information on number of shares and amount of debt is applicable only to corporate registrants): Title of Each Class Number of Shares of Common Stock Outstanding Common stock 2,250,000,000 11. Are any or all of registrant's securities listed in a Stock Exchange? Yes Disclose the name of such Stock Exchange: Philippine Stock Exchange WE ARE NOT ASKING YOU FOR A PROXY AND YOU ARE NOT REQUESTED TO SEND US A PROXY SAMPLE PROXY ONLY The undersigned shareholder(s) of SUNTRUST HOME DEVELOPERS, INC. -

2015 Annual Report/Suntrust Home Developers, Inc

1 0 6 8 3 S U N T R U S T H O M E D E V E L O P E R S , I N C . 6 T H F L O O R , T H E W O R L D C E N T R E , 3 3 0 S E N . G I L P U Y A T A V E N U E M A K A T I C I T Y , M E T R O M A N I L A 17- A S E C N/A (632) 867-8826 to 40 N/A 1,613 OCTOBER/LAST TUESDAY DECEMBER/31 [email protected] ROLANDO D. SIATELA 867-8826 22ND FLOOR, THE WORLD CENTRE, 330 SEN. GIL PUYAT AVENUE, MAKATI CITY, METRO MANILA 2015 ANNUAL REPORT/SUNTRUST HOME DEVELOPERS, INC. Page 1 of 24 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE 1. For the fiscal year ended 31 December 2015 2. SEC Identification Number: 10683 3. BIR Tax Identification No.: 000-141-166-000 4. SUNTRUST HOME DEVELOPERS, INC. Exact name of issuer as specified in its charter 5. Metro Manila Province, Country or other jurisdiction of incorporation or organization 6. (SEC Use Only) Industry Classification Code 7. 6th Floor, The World Center Bldg. 330 Sen. Gil J. Puyat Avenue Makati City, Philippines 1227 Address of principal office 8. (632) 867-8826 to 40 Issuer’s telephone number, including area code 9. -

Permits and Clearances Issued Fy 2014 Hazwaste Id

PERMITS AND CLEARANCES ISSUED FY 2014 HAZWASTE ID DATE OF APPLICATION/S NO NAME OF FIRM ADDRESS DATE APPROVED / ISSUED RECEIVED 1 SCT Electro - Component Corporation 584 Shaw Boulevard, Mandaluyong City November 27, 2013 January 9, 2014 Lot 2 & 3, Block 1, B.V. Romero Boulevard, 2 Mama Tina Pasta Company, Inc. Manila Harbour Center , Radial Road - 10, October 16, 2013 January 9, 2014 Vitas, Tondo, Manila Banawe Street cor. Del Monte Avenue, 3 5 Storey Commercial Building (SMI Development Corporation) October 9, 2013 December 16, 2013 Manresa, Quezon City Km 21 West Service Road, Buli, Muntinlupa 4 Rema Tiptop Philippines, Inc. October 14, 2013 December 3, 2013 City Paseo de Roxas corner Makati Avenue, 5 Zuelig Building August 14, 2013 January 24, 2014 Urdaneta, Makati City 3F, 1006 San Luis Building, T.M. Kalaw cor. 6 Helplabs Medical and Diagnostic Center, Inc. October 16, 2013 January 24, 2014 Ma. Orosa St., Ermita, Manila Room 402 Stanisco Towers, 999 Pedro Gil 7 Alcomed Diagnostic & Medical Center Inc. November 14, 2013 January 3, 2014 cor, Agoncillo Sts., Ermita, Manila Building 2, Tatalon Street, Ugong, 8 One Cypress Agri-Solution, Inc. December 6, 2013 January 30, 2014 Valenzuela City 9 Brent Oil Corporation 469 Paseo de Blas, Valenzuela City December 23, 2013 January 30, 2014 10 Bright Star Plastic Recycling 8 I. Cabral Street, Maysan, Valenzuela City December 5, 2013 January 30, 2014 ITC Road, ITC Compound, Canumay, 11 Rostech Foundry and Forging, Inc. December 13, 2013 January 30, 2014 Valenzuela City 12 Snack and Enjoy Corporation 8 Galas Street, Bignay, Valenzuela City October 4, 2013 February 7, 2014 13 Xinyuan Recycling Corporation 73 Maysan Road, Maysan, Valenzuela City September 27, 2013 February 7, 2014 GF GBT Building, Maysan Road cor. -

Name Establishment Location/Address Date of Accreditation YEAR JGC Phil

Name Establishment Location/Address Date of Accreditation YEAR JGC Phil. Bldg., 2109 Prime St. Madrigal Business Park, Ayala JAY R. KABAMALAN JGC Philippines, Inc. 5th day of January 2012 Alabang, Muntinlupa City ANTONIO FRANCIS G. CHUA Energy Development Corporation-Laboratory Energy Center, Merritt Road, Fort Bonifacio, Taguig City 5th day of January 2012 MANUEL L. EMBERGA Symphony Industrial Corporation 354 F. San Diego St., Viente Reales, Valenzuela City 5th day of January 2012 Quezon Institute Compound, Eulogio Rodriguez Avenue (España LUISITO A. ASIÑAS Philippine Tuberculosis Society, Inc. 5th day of January 2012 Ext.), Quezon City FERDIE P. DE LUNA Pascual Laboratories, Inc. 817 EDSA, South Triangle, Quezon City 5th day of January 2012 TOMAS T. BALISI Ann Francis Mother & Child Hospital 606 Quirino Hi-way, Novaliches, Quezon City 5th day of January 2012 RODOLFO M. REYES Green Earth Treatment Solutions, Inc. Elena Drive cor. Marcos Alvarez Avenue, Talon 5, Las Piñas City 5th day of January 2012 ALANE BLYTHE C. DY United Diagnostic Laboratory G/F UDL Medical Bldg., 1440 Taft Ave., Ermita, Manila 5th day of January 2012 JINARD A. MODINA Cargohaus, Inc. (CHI) 4F Cargohaus Bldg., Brgy. Vitalez, NAIA Complex, Parañaque City 5th day of January 2012 Blue Sapphire and Sapphire Residences Condo MICHAEL E. COSTELO, JR. 2nd Ave. cor. 30th St., Fort Bonifacio Global City, Taguig City 5th day of January 2012 Corporation First Medical Team Healthcare Specialist PAUL M. TEVES 4/F San Luis Terraces Bldg., 638 T.M. Kalaw St., Ermita, Manila 5th day of January 2012 Group ELMA P. REYES One Pacific Place Condominium 147 H.V.