Residential Real Estate Lending, Comptroller's Handbook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

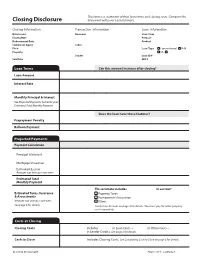

Closing Disclosure Document with Your Loan Estimate

This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term Closing Date Purpose Disbursement Date Product Settlement Agent Seller File # Loan Type Conventional FHA Property VA _____________ Lender Loan ID # Sale Price MIC # Loan Terms Can this amount increase after closing? Loan Amount Interest Rate Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty Balloon Payment Projected Payments Payment Calculation Principal & Interest Mortgage Insurance Estimated Escrow Amount can increase over time Estimated Total Monthly Payment This estimate includes In escrow? Estimated Taxes, Insurance Property Taxes & Assessments Homeowner’s Insurance Amount can increase over time Other: See page 4 for details See Escrow Account on page 4 for details. You must pay for other property costs separately. Costs at Closing Closing Costs Includes $5,877.00 in Loan Costs + $7,642.43 in Other Costs – $0 in Lender Credits. See page 2 for details. Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 3 for details. CLOSING DISCLOSURE PAGE 1 OF 5 • LOAN ID # 0000000000 This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term -

Real Estate Appraiser

REAL ESTATE APPRAISAL EXPERIENCE LOG Bureau of Professional Licensing Authority: 1980 PA 299 PO Box 30670 ● Lansing, MI 48909 Telephone: (517) 241-9288 www.michigan.gov/bpl [email protected] APPLICANT NAME: LICENSE #: Instructions: Copy as needed. Add entries in chronological order. The use of this form is not mandatory, but information requested must be provided to document appraisal experience as required by the Michigan Occupational Code, PA 299 Type of Check applicable description of work performed Total Hours Property Report S.R. 2- Complexity of 1980. ASSIGNMENT IDENTIFICATION Instructions: Under Property Type, indicate VL for Vacant Land, IND for by indicating A or S Requested Industrial or C1 for Single-Tenant Comm ercial Properties or CM for Multiple-Tenant Commercial Properties, R1 for Type 2 (a) (b) Single Family Residential & RM for 2-4 Family Residenti al Properties. All appraisal reports must indicate which tasks the Applicant (A) and Supervisor (S) completed. Separate experience logs shall be maintained/submitted for each supervising appraiser if applicable. on Date of Report & Number, if applicable Property Address, City, State, Zip Code Separate Page Other: Explain spection was Supervised Date Number In A S A S A S A S A S A S A S Supervisor Certification Total This Page: By signing the Supervisor Certification below I acknowledge that it is the joint responsibility of both the Supervisory Appraiser and the Applicant to ensure the experience log is accurate, current, and complies with all applicable laws, administrative rules, and applicable regulations for the appraiser profession. I certify that I have completed a course that, at a minimum, complies with the specifications for course content established by the TOTAL HOURS: AQB, which is specifically oriented to the requirements and responsibilities of Supervisory Appraisers and Trainee Appraisers. -

5/1 MOP Loan Program

GENERAL GUIDELINES 5/1 Maximum Loan-to-Value Ratio: Same as Standard MOP LTV Thresholds Fixed Rate Period: 5 Years ORTGAGE M Maximum Loan Term: 30 Years RIGINATION Qualifying Interest Rate: Initial 5/1 MOP Interest Rate O Minimum Interest Rate: 3.25% ROGRAM P Maximum Payment-to-Income Ratio: 40% Maximum Overall Debt-to-Income Ratio: 48% PROGRAM OVERVIEW 5/1 MOP Initial Interest Rate The 5/1 Mortgage Origination Program (5/1 MOP) loan is a fully-amortizing mortgage loan The initial fixed interest rate* in effect during the Fixed Rate that offers an initial fixed interest rate and payment for the first 5 years of the loan, after which Period of the loan is comprised of the following three (3) the loan converts to a 1-year adjustable rate mortgage (“Standard MOP”) for the remaining components: loan term. The maximum overall loan term is 30 years. All or any portion of the principal Index: 5-year Treasury Bond Yield balance may be prepaid without penalty at any time and there is no negative amortization associated with 5/1 MOP loans. For eligibility requirements, refer to the MOP Brochure. Spread: J.P. Morgan U.S. Liquid Index (JULI) Index Service Fee: .25% IMPORTANT CONSIDERATIONS: *The minimum 5/1 MOP Initial Interest Rate is 3.25% • The 5/1 MOP Initial Interest Rate may be higher or lower than the current Standard Rate offered for a Standard MOP loan. The current interest rate for each of these loan products is available at www.ucop.edu/loan-programs. QUESTIONS? • Fixed rate payments during the first 5 years of the loan provide a stable monthly payment Contact the local Campus Housing Programs to borrowers; however, there is potential for increased monthly payments when the Fixed Representative or the University of California Home Loan Rate Period ends. -

IAC Ch 34, P.1 701—34.17(321,423) Repossession of a Vehicle. A

IAC Ch 34, p.1 701—34.17(321,423) Repossession of a vehicle. A vehicle may be taken from a purchaser by the holder of the security interest in the vehicle or someone acting on the holder’s interest, if the purchaser defaults on the terms of the purchase agreement. To be recognized as valid for use tax purposes, the repossession must be regulated under the terms of the Uniform Commercial Code and there must be a valid lien on the title of the vehicle. To be recognized as valid for use tax purposes, repossession of a vehicle can be made by dealers, by financial institutions, and by individuals. The taxable result of repossession depends on the identity of the person doing the repossessing and the manner in which the person doing the repossessing conducts the transaction. 34.17(1) Licensed vehicle dealer. If a licensed vehicle dealer repossesses a vehicle and anticipates reselling the vehicle, then the dealer can use the dealer’s resale exemption, and no use tax is due at the time of the registration of the vehicle by the dealer. 34.17(2) Financial institution or private individual. A financial institution or a private individual may be a licensed dealer entitled to receive an exemption from use tax based on the dealer’s license when registering a repossessed vehicle. Repossessions of vehicles that will be resold by a financial institution or an individual that does not have a dealer’s license can be effectuated using a foreclosure affidavit. Use tax liabilities which arise as a result of such affidavits are as follows: a. -

Underwriting, Mortgage Lending, and House Prices: 1996-2008

June 2009 Underwriting, Mortgage Lending, and House Prices: 1996-2008 James A. Wilcox University of California, Berkeley Abstract: Lowering of underwriting standards may have contributed much to the unprecedented recent rise and subsequent fall of mortgage volumes and house prices. Conventional data don’t satisfactorily measure aggregate underwriting standards over the past decade: The easing and then tightening of underwriting, inside and especially outside of banks, was likely much more extensive than they indicate. Given mortgage market developments since the mid 1990s, the method of principal components produces a superior indicator of mortgage underwriting standards. We show that the resulting indicator better fits the variation over time in the laxity and tightness of underwriting. Based on a VAR, we then show how conditions affected underwriting standards. The results also show that our new indicator of underwriting helps account for the behavior of mortgage volumes, house prices, and GDP during the recent boom in mortgage and housing markets. Keywords: Underwriting, standards, mortgages, house prices, LTV. 1 I. Introduction Underwriting standards for residential mortgages (henceforth: underwriting) are now generally regarded as having been unusually lax during the middle of the 2000s. Underwriting then tightened up again during the financial crisis that began in 2007. The laxity of underwriting and its ensuing tightness since the middle of the 1990s likely contributed considerably to the unprecedented rise and subsequent fall of mortgage volumes and house prices. Conventional data do not satisfactorily measure aggregate underwriting over the past decade: Easing of underwriting, inside and especially outside of banks, was likely much more extensive than they indicate. -

Consumer Guide to Vehicle Repossession

REQUIREMENTS FOR DOING REINSTATING A VEHICLE BUSINESS CONTRACT AFTER REPOSSESSION Repossession agencies and their employees must be The Bureau has no jurisdiction over whether or not licensed by the Bureau of Security and Investigative the vehicle’s legal owner will reinstate your contract. Services (Bureau or BSIS) to engage in business or If you obtain a reinstatement, you will need to accept employment to locate or recover vehicles that provide the repossession agency a release from are subject to a security agreement.2 the legal owner stating that you may redeem your vehicle and proof of having paid the administrative Note: In some cases, a bank, financial lender, or filing fee to the police or sheriff’s office, where the other legal owner will send their own employees to repossession was reported.8 recover the vehicle. Individuals employed directly by a bank, lender, or the legal owner of the vehicle are Please note that in some cases you may not get your not required to be licensed as repossession agency vehicle back after it has been repossessed. employees.3 HOW REPOSSESSIONS WORK When a person has violated a condition(s) of the lease CONSUMER or loan agreement (e.g. being past due on the vehicle loan or lease payments, failure to maintain insurance, etc.), and efforts to correct the violation fail, the GUIDE TO bank, financial lender, legal owner or their agents can contract with repossession agencies to locate 1 and repossess the vehicle subject to the security VEHICLE agreement that contains the repossession clause. Many of the activities carried out before, during, and REPOSSESSION after the repossession are regulated by State and federal laws. -

TIAA-Real Estate 03.31.2021-10Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2021. OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from__________to __________ Commission file number: 33-92990; 333-237134 TIAA REAL ESTATE ACCOUNT (Exact name of registrant as specified in its charter) New York (State or other jurisdiction of incorporation or organization) NOT APPLICABLE (I.R.S. Employer Identification No.) C/O TEACHERS INSURANCE AND ANNUITY ASSOCIATION OF AMERICA 730 Third Avenue New York, New York 10017-3206 (Address of principal executive offices, including zip code) Registrant’s telephone number, including area code: (212) 490-9000 (Former name, former address and former fiscal year, if changed since last report) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). -

Agency Guideline Revisions Note: Suntrust Mortgage Specific Overlays Are Underlined

Agency Guideline Revisions Note: SunTrust Mortgage specific overlays are underlined. Impacted Revised Guidelines Topic Impacted Products Current Guidelines Document Effective Immediately for NEW AND EXISTING Loan Applications ON OR After May 26, 2017 Appraisal Correspondent HomeReady® Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Requirements Section 1.07 Mortgage / Accessory Appraisal- (non-AUS & Non-AUS Non-AUS Units Guideline DU) Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Home guidelines from this section remain the same. guidelines from this section remain the same. Possible® Accessory Units Accessory Units Mortgage Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an (LPA) additional living area independent of the primary dwelling unit, and includes a fully functioning additional living area independent of the primary dwelling unit, and includes a fully functioning kitchen and bathroom. Some examples may include a living area over a garage and basement units. kitchen and bathroom. Some examples may include a living area over a garage and basement units. Whether a property is defined as a one-unit property with an accessory unit or a two-unit property Whether a property is defined as a one-unit property with an accessory unit or a two-unit property will be based on the characteristics of the property, which may include, but are not limited to, the will be based on the characteristics of the property, which may include, but are not limited to, the existence of separate utilities, a unique postal address, and whether the unit is rented. -

Accelerated Resolution of Financial Distress

Washington University Law Review Volume 76 Issue 4 January 1998 Accelerated Resolution of Financial Distress Barry E. Adler New York University Follow this and additional works at: https://openscholarship.wustl.edu/law_lawreview Part of the Bankruptcy Law Commons Recommended Citation Barry E. Adler, Accelerated Resolution of Financial Distress, 76 WASH. U. L. Q. 1169 (1998). Available at: https://openscholarship.wustl.edu/law_lawreview/vol76/iss4/1 This Article is brought to you for free and open access by the Law School at Washington University Open Scholarship. It has been accepted for inclusion in Washington University Law Review by an authorized administrator of Washington University Open Scholarship. For more information, please contact [email protected]. Washington University Law Quarterly VOLUME 76 NUMBER4 1998 ACCELERATED RESOLUTION OF FINANCIAL DISTRESS BARRY E. ADLER* In principle, debt can bond afirm's management to diligence and wise investment of corporate assets. In practice, however, management can escape the ties of this bond through new capital infusion prior to financial collapse. When management pursues this tactic, insolvent corporationsmay enter bankruptcy too late, after an unnecessary economic decline. To address this problem, a beneficial modification of bankruptcy's voidablepreference rules would permit a trustee to invalidate loan termsfavorable to a creditoron any loan made while a debtor is insolvent if that loan is used to repay an earlier claim. This modification would deprive an insolvent firm of resources its managers can now use to stave off bankruptcy supervision. As a result of this modification, corporate bankruptcy would occur earlierin the financial distress of a firm, before managers could unduly dissipate the firm's value. -

Uniform Residential Loan Application Interactive (Form 1003)

Uniform Residential Loan Application ___________________________________________________________________________________________________________________________________________________________________ This application is designed to be completed by the applicant(s) with the Lender’s assistance. Applicants should complete this form as “Borrower” or “Co-Borrower,” as applicable. Co-Borrower information must also be provided (and the appropriate box checked) when the income or assets of a person other than the Borrower (including the Borrower’s spouse) will be used as a basis for loan qualification or the income or assets of the Borrower’s spouse or other person who has community property rights pursuant to state law will not be used as a basis for loan qualification, but his or her liabilities must be considered because the spouse or other person has community property rights pursuant to applicable law and Borrower resides in a community property state, the security property is located in a community property state, or the Borrower is relying on other property located in a community property state as a basis for repayment of the loan. If this is an application for joint credit, Borrower and Co-Borrower each agree that we intend to apply for joint credit (sign below): _________________________________________ _________________________________________ Borrower Co-Borrower I. TYPE OF MORTGAGE AND TERMS OF LOAN Mortgage VA Conventional Other (explain): Agency Case Number Lender Case Number Applied for: FHA USDA/Rural Housing Service Amount Interest Rate No. of Months Amortization Type: Fixed Rate Other (explain): $ % GPM ARM (type): II. PROPERTY INFORMATION AND PURPOSE OF LOAN Subject Property Address (street, city, state & ZIP) No. of Units Legal Description of Subject Property (attach description if necessary) Year Built Purpose of Loan Purchase Construction Other (explain): Property will be: Refinance Construction-Permanent Primary Residence Secondary Residence Investment Complete this line if construction or construction-permanent loan. -

Typical Small Borrower Ownership

Apartment Property Typical small borrower ownership Single Asset Entity 2530 Borrower 2530 Shell General Partner 1% Owner of SAE 2530 Key Sponsor Principal 99% Limited Partner of SAE REO 100% owner of Shell GP Apartment Property Typical large borrower entity 2530 Single Asset Entity Borrower Shell Managing 2530 2530 Member Limited Equity Partner 10% Owner of SAE & 90% Member of SAE Principal Principal 2530 Developer & Sponsor 2530 Key 2530 Large Investor Fund Principal 100% owner of JV Entity Fund Investors 90+% owners of REO Key Large Investor Fund Principal REO Fund Sponsor Less than 10% investor in Large Investor Fund 2530 ABC Partners, LLC Regional Borrower v1 XYZ Partners, LLC 2530 Manager (Shell Entity) 2530 XYZ Group, LLC Manager of XYZ Partner Key Sam Smith, Manager Principal REO Project Name Investors, LLC Project Name Investments, LLC Company Investments 2530 21.379% 17.85% 60.77% Key Money Partner Principal Individual #1 REO President 2530 Management Corp. Individual #1 Individual #2 Individual #3 Individual #4 .99% 24.907% 24.698% 24.698% 24.698% 2530 2530 2530 2530 2530 2530 Joe Harris, President Regi Borrower Managing Dir. Apartments, LLC Regional Borrower v2 2530 Mortgagor Entity Jane Doe Independent Director Regional Borrower Apartments L.P. 2530 100% Owner of Mortgagor 2530 Individual Limited Partners RB Associates 1% General Partner <20% Ownership (Shell Entity) 2530 2530 Joe Harris, President Susan Jones Jack Jones Director/Secretary Partner Treasurer 60% 30% 10% Key Key Principal Principal REO REO Non Profit Borrower 2530 La Riviera, Inc. Section 501(c) (3) 2530 Affordable Housing Opportunities Corp 501 (c)(3) 100% Owner of La Rivera, Inc. -

Integra Realty Resources Phoenix Appraisal of Real Property 26.57

Integra Realty Resources Phoenix Appraisal of Real Property 26.57 Acres Vacant Land Vacant Land Southeast side of State Route 66, Northwest of the Burlington Northern Santa Fe Railroad Unincorporated, Mohave County, Arizona 86401 Client Reference: TO‐21‐023 Project: M697501X; ADOT Parcel L‐K‐038C Prepared For: ADOT Right of Way Operations Effective Date of the Appraisal: November 16, 2020 Report Format: Appraisal Report – Comprehensive Format IRR ‐ Phoenix File Number: 132‐20‐301 I 0.48 Acres vacant Land Southeast side of State Route 66, Northwest of the Burlington Northern Santa Fe Railroad Unincorporated, Arizona Integra Realty Resources 2999 North 44th Street T 602.266.5599 Phoenix Suite 512 F 602.266.1515 Phoenix, AZ 85018 www.irr.com November 30, 2020 Mr. Timothy F. O'Connell, Jr. Appraisal Section Supervisor ADOT Right of Way Operations ADOT Mail Room, 1655 W. Jackson Street Phoenix, AZ 85007 SUBJECT: Market Value Appraisal 0.48 Acres vacant Land Southeast side of State Route 66, Northwest of the Burlington Northern Santa Fe Railroad Unincorporated, Mohave County, Arizona 86401 Client Reference: TO‐21‐023 Project: M697501X IRR ‐ Phoenix File No. 132‐20‐301ADOT Parcel L‐K‐038B Dear Mr. O'Connell: Integra Realty Resources – Phoenix is pleased to submit the accompanying appraisal of the referenced property. The purpose of the appraisal is to develop an opinion of the market value of the fee simple interest in the property. The client for the assignment is ADOT Right of Way Operations, and the intended use is for property disposition purposes. The subject is a parcel of vacant land containing an area of 0.48 acres or 20,844 square feet.