Embracer Group

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Contributors

gems_ch001_fm.qxp 2/23/2004 11:13 AM Page xxxiii Contributors Curtis Beeson, NVIDIA Curtis Beeson moved from SGI to NVIDIA’s Demo Team more than five years ago; he focuses on the art path, the object model, and the DirectX ren- derer of the NVIDIA demo engine. He began working in 3D while attending Carnegie Mellon University, where he generated environments for playback on head-mounted displays at resolutions that left users legally blind. Curtis spe- cializes in the art path and object model of the NVIDIA Demo Team’s scene- graph API—while fighting the urge to succumb to the dark offerings of management in marketing. Kevin Bjorke, NVIDIA Kevin Bjorke works in the Developer Technology group developing and promoting next-generation art tools and entertainments, with a particular eye toward the possibilities inherent in programmable shading hardware. Before joining NVIDIA, he worked extensively in the film, television, and game industries, supervising development and imagery for Final Fantasy: The Spirits Within and The Animatrix; performing numerous technical director and layout animation duties on Toy Story and A Bug’s Life; developing games on just about every commercial platform; producing theme park rides; animating too many TV com- mercials; and booking daytime TV talk shows. He attended several colleges, eventually graduat- ing from the California Institute of the Arts film school. Kevin has been a regular speaker at SIGGRAPH, GDC, and similar events for the past decade. Rod Bogart, Industrial Light & Magic Rod Bogart came to Industrial Light & Magic (ILM) in 1995 after spend- ing three years as a software engineer at Pacific Data Images. -

Redeye-Gaming-Guide-2020.Pdf

REDEYE GAMING GUIDE 2020 GAMING GUIDE 2020 Senior REDEYE Redeye is the next generation equity research and investment banking company, specialized in life science and technology. We are the leading providers of corporate broking and corporate finance in these sectors. Our clients are innovative growth companies in the nordics and we use a unique rating model built on a value based investment philosophy. Redeye was founded 1999 in Stockholm and is regulated by the swedish financial authority (finansinspektionen). THE GAMING TEAM Johan Ekström Tomas Otterbeck Kristoffer Lindström Jonas Amnesten Head of Digital Senior Analyst Senior Analyst Analyst Entertainment Johan has a MSc in finance Tomas Otterbeck gained a Kristoffer Lindström has both Jonas Amnesten is an equity from Stockholm School of Master’s degree in Business a BSc and an MSc in Finance. analyst within Redeye’s tech- Economic and has studied and Economics at Stockholm He has previously worked as a nology team, with focus on e-commerce and marketing University. He also studied financial advisor, stockbroker the online gambling industry. at MBA Haas School of Busi- Computing and Systems and equity analyst at Swed- He holds a Master’s degree ness, University of California, Science at the KTH Royal bank. Kristoffer started to in Finance from Stockholm Berkeley. Johan has worked Institute of Technology. work for Redeye in early 2014, University, School of Business. as analyst and portfolio Tomas was previously respon- and today works as an equity He has more than 6 years’ manager at Swedbank Robur, sible for Redeye’s website for analyst covering companies experience from the online equity PM at Alfa Bank and six years, during which time in the tech sector with a focus gambling industry, working Gazprombank in Moscow he developed its blog and on the Gaming and Gambling in both Sweden and Malta as and as hedge fund PM at community and was editor industry. -

OPERATIONAL EBIT INCREASED 217% to SEK 396 MILLION

THQ NORDIC AB (PUBL) REG NO.: 556582-6558 EXTENDED FINANCIAL YEAR REPORT • 1 JAN 2018 – 31 MAR 2019 OPERATIONAL EBIT INCREASED 217% to SEK 396 MILLION JANUARY–MARCH 2019 JANUARY 2018–MARCH 2019, 15 MONTHS (Compared to January–March 2018) (Compared to full year 2017) > Net sales increased 158% to SEK 1,630.5 m > Net sales increased to SEK 5,754.1 m (507.5). (632.9). > EBITDA increased to SEK 1,592.6 m (272.6), > EBITDA increased 174% to SEK 618.6 m (225.9), corresponding to an EBITDA margin of 28%. corresponding to an EBITDA margin of 38%. > Operational EBIT increased to SEK 897.1 m > Operational EBIT increased 217% to SEK 395.9 m (202.3) corresponding to an Operational EBIT (124.9) corresponding to an Operational EBIT margin of 16%. margin of 24%. > Cash flow from operating activities amounted > Cash flow from operating activities amounted to SEK 1,356.4 m (179.1). to SEK 777.2 m (699.8). > Earnings per share was SEK 4.68 (1.88). > Earnings per share was SEK 1.10 (1.02). > As of 31 March 2019, cash and cash equivalents were SEK 2,929.1 m. Available cash including credit facilities was SEK 4,521.1 m. KEY PERFORMANCE INDICATORS, Jan-Mar Jan-Mar Jan 2018- Jan-Dec GROUP 2019 2018 Mar 2019 2017 Net sales, SEK m 1,630.5 632.9 5,754.1 507.5 EBITDA, SEK m 618.6 225.9 1,592.6 272.6 Operational EBIT, SEK m 395.9 124.9 897.1 202.3 EBIT, SEK m 172.0 107.3 574.6 188.2 Profit after tax , SEK m 103.0 81.1 396.8 139.2 Cash flow from operating activities, SEK m 777.2 699.8 1,356.4 179.1 Sales growth, % 158 673 1,034 68 EBITDA margin, % 38 36 28 54 Operational EBIT margin, % 24 20 16 40 Throughout this report, the extended financial year 1 January 2018 – 31 March 2019 is compared with the financial year 1 January – 31 December 2017. -

REVIEWS Vis Et Virtus

IGN Entertainment Games: IGN | GameSpy | FilePlanet | TeamXbox | CCG | GameStats | Direct2Drive | What They Play | Battlefield Heroes IGN Entertainment Games: IGN | GameSpy | FilePlanet | TeamXbox | CCG | GameStats | Direct2Drive | What They Play | Battlefield Heroes Skins: NWN2 | NWN Welcome, The Web The Site Search Pailith St.. Profile | Logout Neverwinter Vault New | Pending List | Full Listings | Request Review | Reviewer Awards | Search Site Front Page REVIEWS Current News Archive Old News Archive NWN2 Community RATINGS News Vis et Virtus - Chapter 8 NWN Community News Gameplay : 8 Reviewers Forum Voting FAQ Created by Pailith Studios RP/Storytelling : 10 Reviewed by QSW Work to Do Action : 8.5 RSS Feeds Review Posted on 2009-10-03 Visuals : 9.5 Contacts Staff Quick Pros: Sound : 9 Help Replayability : 8 Buy NWN2 Amazing cut scenes, vivacious companions and gripping story. Download Full Games Polish : 6.5 My Profile Quick Cons: Solo : 8 Features Multiplayer : NA Some polish and debugging issues. Fun : 8.5 Neverwinter Nights 2 NWN2 Files Summary (No Spoilers) FINAL SCORE : 8.44 NWN2 Game Info Number of Players: 1 NWN2 Resources Hours of Game Play: 12 AWARDS NWN2 Community Character: Seiji Master of the Way Monk. Start Level: Master of the Way 38/Shadowdancer 1. Neverwinter Nights End Level: Master of the Way 39/Shadowdancer 1. NWN2 NWN NWN Files Hak Size: 325.07MB compressed. Death: Final (reload) unless raised by henchman. NWN Game Info Resting: Limited to every 4 in game hours. SCREENSHOTS NWN Resources Requires: (SoU & HoTU) NWN Community PNP conversion: No HOF NWN2 Original Hakpaks Vault Network Vis et Virtus is a saga of epic proportions acted out via the NWN1 game platform. -

THQ Nordic Fast Comment

Equity Research - 14 August 2019 07:09 CET THQ Nordic Fast comment Shows strength despite limited new releases Company-sponsored research: Not rated Sales of SEK 1,142m, +12.0% vs. ABGSCe… Share price (SEK) 13/08/2019 222.4 …Operational EBIT of SEK 206m, +17.1% vs. ABGSCe Technology Hardware & Equipment, Sweden Two new acquisitions strengthen games segment THQNb.ST/THQNb.ST Estimate beat driven by back catalog and digital sales MCap (SEKm) 20,906 THQ reported its Q1’19/20 figures today, which beat our estimates for MCap (EURm) 1,955.3 what was set up to become a somewhat weak quarter. Sales came in at Net debt (EURm) -212 SEK 1,142m, which was 12.0% above our estimate of SEK 1,020m. driven by strong back catalog sales (82%), where Metro Exodus No. of shares (m) 94.0 continued to perform well as Deep Silver saw sales of SEK 373m, Free float (%) 48.2 +24.3% vs ABGSCe. Coffee Stain Studios also showed another strong Av. daily volume (k) 493.6 quarter with sales of SEK 83m, as was mainly expected, with sales being driven by the promotion of Satisfactory by Epic Games Store. THQ also offered an earnings beat, where higher than usual digital sales contributed (71% of total net sales). EBITDA came in at SEK 389m, beating our estimate of SEK 299m by 30.3%. Operational EBIT, was SEK 206m, beating our estimate of SEK 176m by 17.1%. All in all the estimate beats show that THQ can rely on its back catalog to transition strongly through quarters with no new major releases. -

Ncsoft (036570) Korea – Equity Research

NCsoft (036570) Korea – Equity Research Visit to NCsoft West: Earnings, target price under review Internet Buy Oct. performance may warrant revision of TP 30 Sep 2009 We maintain our Buy call and target price of W280,000, as we keep our 2009F EPS of Bloomberg: 036570 KS W9,098 intact. If sales and servers for Aion continue to increase in Oct., we will likely Target Price (12M, W): 280,000 raise our earnings estimates and target price. Share Price (09/29/09, W): 166,000 Expected Return (%): 68.7 After visiting NCsoft West and game stores like Gamestop and Best Buy in US and Sector: Internet Software and Services Europe, we feel confident that sales of Aion in those regions in 3Q09 will exceed our Sector Rating: Overweight expectation of 520k boxes. EPS Growth (09F, %): 582.0 The commercial launch of Aion began in Europe (Germany, France, Britain) on Sep. 25. Market EPS Growth (09F, %): 53.0 However, the gameÊs launch has not gone smoothly as pre-sales of Aion boxes far P/E (X): 18.2 exceeded the companyÊs expectations and server capacity. In Germany, about 40,000 Market P/E (09/29/09F, X): 15.4 gamers were on the waiting list after Aion boxes were sold out. NCsoft is gradually Market Cap (Wbn): 3,601 deploying servers to address this issue, Shares Outstanding (mn): 22 Avg Trading Volume (60D, '000): 638 Aion was introduced through game websites, as well as through major press such as The Avg Trading Value (60D, Wbn): 90 New York Times in US and The Times of England. -

Zalman ZM-M190 19 Inch Trimon 2D/3D LCD Monitor

1 3D Game We would like to explain what kinds of games supporting 3D and what you should do before you play 3D games. And here are some comments on our 3D monitor. 「I did not know how exciting it was until I played PC games in 3D. But once I played PC Games in 3D, I defi- nitely know the difference between 2D and 3D. And I would never ever satisfied with 2D Games now」 「When I play shooting games, the bullet seems like to come through the monitor. So the 3D gives me some tense and the tense make me exciting」 For example, you can play these very famous PC games in 3D!! You can find out what kind of games make you crazy and what you should do before playing 3D games in [3D Game List] and [How to enjoy 3D game] as below. 2 3D Game List Age of Empires 3 Half-Life 2 - Episode 2 Age of Empires 3 - Asian Dynasties Half-Life 2 - Portal Age of Empires III - The War Chiefs Half-Life 2 - Team Fortress 2 Age of Mythology Harry Potter and the Order of the Phoenix Age of Mythology - Titans Heroes of Might and Magic 5 Assault Heroes Loki Bee Movie the Game Lord of the Rings Battle for Middle Earth I Beowulf Lord of the Rings Battle for Middle Earth II BioShock Madden 2008 Blazing Angels 2 - Secret missions of WWII Maelstrom Call of Duty 4 Meet the Robinsons Call of Juarez Medieval 2 - Total War Civilization 4 Mage Night - Apocalypse Command and Conquer 3 - Tiberiam Wars Medal of Honor Pacific Assault Crysis Monster Jam CSI: Hard Evidence MotoGP URT 3 Dead Reefs NBA Live 07 Driver Parallel Lines NBA Live 08 Empire Earth 3 Need for Speed Carbon F.E.A.R. -

THQ Nordic (THQNO.ST)

COMPANY ANALYSIS 1 March 2018 Summary THQ Nordic (THQNO.ST) List: Power-up! Market Cap: 11,190 MSEK The company had an immense release schedule with loads of Industry: Gaming new content during the quarter. The reported numbers beat CEO: Lars Wingefors Chairman: Kicki Wallje-Lund our estimates. Even though that THQ Nordic produced a record quarter, the thing stole the spotlight was the announcement of the acquisition of Koch Media; we get into OMXS 30 THQ Nordic detail about the acquired company in this research update. 160 The acquisition is a prime example of THQ Nordic’s 140 acquisition strategy. We believe that the market is yet to fully 120 100 grasp the underlying value and cash flow generating 80 capabilities of THQ Nordic’s growing IP portfolio, which was 60 enhanced significantly by the acquirement. 40 20 We raised our Base-case valuation to 140 SEK per share 0 28-Feb 29-May 27-Aug 25-Nov 23-Feb based on a Back-Of-The-Envelope assessment on the same day as the acquisition. Following a more in-depth analysis, we increase our fair value estimate further to 168 SEK per share. We argue that the new addition to the Group was acquired at a low price and that the long-term possibilities following the purchase are vast. Redeye Rating (0 – 10 points) Management Ownership Profit outlook Profitability Financial strength 8.0 points 9.0 points 7.0 points 6.0 points 8.0 points Key Financials 2016 2017 2018E 2019E 2020E Share information Revenue, MSEK 302 508 3,666 3,909 4,300 Share price (SEK) 141.0 Growth 42% 68% 622% 7% 10% Number of shares (m) 79.4 EBITDA 132 273 929 1,009 1,212 Market Cap (MSEK) 11,190 EBITDA margin 44% 54% 25% 26% 28% Net cash (MSEK) 255 EBIT 95 188 616 696 849 Free float (%) 50 % EBIT margin 31% 37% 17% 18% 20% Daily turnover (’000) 60 Pre-tax earnings 93 182 616 696 849 Net earnings 72 139 480 543 662 Net margin 24% 27% 13% 14% 15% Analysts: Kristoffer Lindstrom 2016 2017 2018E 2019E 2020E [email protected] Dividend/Share 0.00 0.00 0.00 0.00 2.50 2016 2017 2018E 2019E 2020E EPS adj. -

19/20 Interim Report 2 Reg No

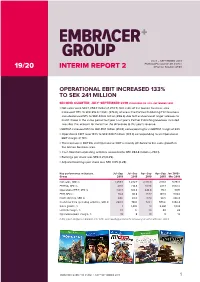

JULY – SEPTEMBER 2019 EMBRACER GROUP AB (PUBL) 19/20 INTERIM REPORT 2 REG NO. 556582-6558 OPERATIONAL EBIT INCREASED 133% TO SEK 241 MILLION SECOND QUARTER, JULY–SEPTEMBER 2019 (COMPARED TO JULY–SEPTEMBER 2018) > Net sales were SEK 1,259.7 million (1,272.7). Net sales of the Games business area increased 117% to SEK 816.0 million (376.0), whereas the Partner Publishing/Film business area decreased 51% to SEK 443.6 million (896.6) due to the absence of larger releases to match those in the same period last year. Last year’s Partner Publishing revenues included two titles that account for more than the difference to this year’s revenue. > EBITDA increased 95% to SEK 418.1 million (214.8), corresponding to an EBITDA margin of 33%. > Operational EBIT rose 133% to SEK 240.7 million (103.4) corresponding to an Operational EBIT margin of 19%. > The increase in EBITDA and Operational EBIT is mainly attributed to the sales growth in the Games business area. > Cash flow from operating activities amounted to SEK 284.8 million (–740.1). > Earnings per share was SEK 0.21 (0.25). > Adjusted earnings per share was SEK 0.65 (0.28). Key performance indicators, Jul–Sep Jul–Sep Apr–Sep Apr–Sep Jan 2018– Group 2019 2018 2019 2018 Mar 2019 Net sales, SEK m 1,259.7 1,272.7 2,401.8 2,110.1 5,754.1 EBITDA, SEK m 418.1 214.8 807.6 421.7 1,592.6 Operational EBIT, SEK m 240.7 103.4 444.8 173.1 897.1 EBIT, SEK m 76.4 90.8 157.7 143.3 574.6 Profit after tax, SEK m 64.6 65.0 117.4 98.5 396.8 Cash flow from operating activities, SEK m 284.8 –740.1 723.1 –575.6 1,356.4 Sales growth, % –1 1,403 14 2,281 1,034 EBITDA margin, % 33 17 34 20 28 Operational EBIT margin, % 19 8 19 8 16 In this report, all figures in brackets refer to the corresponding period of the previous year, unless otherwise stated. -

19/20 Full Year Report Reg No

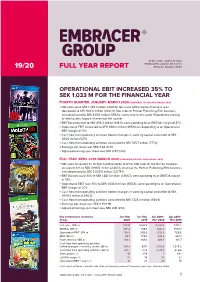

APRIL 2019 – MARCH 2020 EMBRACER GROUP AB (PUBL) 19/20 FULL YEAR REPORT REG NO. 556582-6558 OPERATIONAL EBIT INCREASED 35% TO SEK 1,033 M FOR THE FINANCIAL YEAR FOURTH QUARTER, JANUARY–MARCH 2020 (COMPARED TO JANUARY–MARCH 2019) > Net sales were SEK 1,339.1 million (1,630.5). Net sales of the Games business area decreased to SEK 903.5 million (1,034.9). Net sales of Partner Publishing/Film business area decreased to SEK 435.6 million (595.6), mainly due to the covid-19 pandemic closing of retail outlets towards the end of the quarter. > EBITDA amounted to SEK 495.2 million (618.6), corresponding to an EBITDA margin of 37%. > Operational EBIT amounted to SEK 286.0 million (395.9) corresponding to an Operational EBIT margin of 21%. > Cash flow from operating activities before changes in working capital amounted to SEK 384.6 million (527.1). > Cash flow from operating activities amounted to SEK 765.7 million (777.2). > Earnings per share was SEK 0.42 (0.37). > Adjusted earnings per share was SEK 0.97 (1.00). FULL YEAR, APRIL 2019–MARCH 2020 (COMPARED TO APRIL 2018–MARCH 2019) > Net sales increased 3% to SEK 5,249.4 million (5,121.2). Net sales of the Games business area grew 31% to SEK 3,196.5 million (2,447.1), whereas the Partner Publishing/Film business area decreased to SEK 2,052.9 million (2,674,1). > EBITDA increased 33% to SEK 1,821.3 million (1,366.7), corresponding to an EBITDA margin of 35%. -

THQ Nordic Acquires the German Game Developer and Publisher Handygames

Press release Karlstad, Sweden, July 9, 2018 THQ Nordic acquires the German game developer and publisher HandyGames THQ Nordic GmbH today announced the acquisition of the game developer and publisher HandyGames, headquartered in Giebelstadt, Germany. THQ Nordic GmbH is acquiring 100% of the shares for a total cash consideration of 1 million euro. In addition, the parties have agreed a potential performance based earnout of up to 1.5 million euro. Founded in 2000, HandyGames has released more than 150 games on a multitude of platforms, utilizing a wide range of technologies. Current game development is focused on iOS, Android, Oculus Rift, Samsung Gear VR, HTC Vive, tablet computers, Android TV, Wearables as well as digital-only releases on next generation consoles. The company currently has about 50 employees. HandyGames will continue operating as a developer and publisher for value-priced projects under the management of THQ Nordic GmbH in Vienna. For more information about HandyGames, please visit https://www.handy-games.com/en/ For additional information, please contact: Lars Wingefors, Group CEO Tel: +46 708 471 978 E-mail: [email protected] About THQ Nordic THQ Nordic acquires, develops and publishes PC and console games for the global games market. The company is a major player within game and partner publishing with an extensive catalogue of over 100 owned franchises, such as Saints Row, Dead Island, Homefront, Darksiders, Metro (exclusive license), Titan Quest, MX vs ATV, Red Faction, Delta Force, Destroy All Humans, ELEX, Biomutant, Jagged Alliance, SpellForce, The Guild amongst others. THQ Nordic has a global publishing reach within marketing, sales and distribution, both online and offline. -

Stubbs the Zombie: Rebel Without 21 Starship Troopers PC Continues to Set the Standard for Both Technology and Advancements in Gameplay

Issue 07 THE WAY It’s Meant To Be Played Peter Jackson’s King Kong Age Of Empires III Serious Sam 2 Blockbusters Enjoy the season’s hottest games on the hottest gaming platform Chronicles Of Narnia: The Lion, The Witch City Of Villains F.E.A.R And The Wardrobe NNVM07.p01usVM07.p01us 1 119/9/059/9/05 33:57:57:57:57 ppmm The way it’s meant to be played 3 6 7 8 Welcome Welcome to Issue 7 of The Way It’s Meant 12 13 to be Played, the magazine that showcases the very best of the latest PC games. All the 30 titles featured in this issue are participants in NVIDIA’s The Way It’s Meant To Be Played program, a campaign designed to deliver the best interactive entertainment experience. Development teams taking part in 14 19 the program are given access to NVIDIA’s hardware, with NVIDIA’s developer technology engineers on hand to help them get the very best graphics and effects into their new games. The games are then rigorously tested by NVIDIA for compatibility, stability and reliability to ensure that customers can buy any game with the TWIMTBP logo on the box and feel confident that the game will deliver the ultimate install- and-play experience when played with an Contents NVIDIA GeForce-based graphics card. Game developers today like to use 3 NVIDIA news 14 Chronicles Of Narnia: The Lion, Shader Model 3.0 technology for stunning, The Witch And The Wardrobe complex cinematic effects – a technology TWIMTBP games 15 Peter Jackson’s King Kong fully supported by all the latest NVIDIA 4 Vietcong 2 16 F.E.A.R.