Preliminary Prospectus to the Primary Offer of Series 2 Preferred Shares Dated 04 November 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

For Reel & Real

MAY 2016 CONFIDENTIAL Reigning Queens. Bb. Pilipinas International Kylie Versoza and Miss Universe Philippines Maxine Medina Maxine Medina is the new Pia Alonzo Wurtzbach MANILA - Reigning Miss Universe Pia Alonzo Wurtzbach relinquished the Bb. & Pilipinas-Universe crown to top model Maria Mika Maxine Medina at the Bb. Nadine Lustre Pilipinas 2016 Grand Coronation Night before a jam-packed crowd at the Smart Araneta Coliseum April 20. A stunning beauty from Quezon City, Medina, a 25-year-old, 5-foot-7 inte- rior designer and part-time model, was predicted to take the top title in this year’s Bb. PiIlipinas pageant, giving high hopes James Reid for a back-to-back Miss Universe crown. She had previously entered the com- FOR REEL & REAL petition in 2012 but backed out due to contract conflict issues. But the real star of the night was Wurtzbach who took a break from her hectic duties as Miss Universe to be in the country and crown her succes- MAXINE continued on page 25 Miss Philippines Canada 2016 Miss Philippines Canada 2015 Nathalie Ramos (CENTER) poses with the PCCF candidates for this year. Senator Tobias Enverga presents the cer- tificate of Recognition for Zenaida Guzman to her son Dr. Solon Guzman. Zenaida is currently in the Philippines. MAY 2016 MAY 2016 L. M. Confidential 1 2 L. M. Confidential MAY 2016 MAY 2016 KAPUSO STAR Tom This Is How Long Sex Usually Lasts We’re not saying you’ve peeked Rodriquez to star at through the blinds to see your neighbors doing the deed, but chances are you’ve wondered how your stamina stacks up against ev- Pinoy Fiesta eryone else. -

Railway Project Pipeline

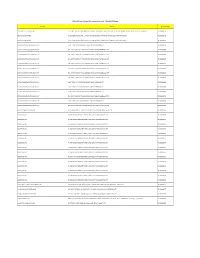

Asian Development Bank Southeast Asia Department Railway Project Pipeline Markus Roesner and Ruediger Zander Asian Development Bank Transport and Communications Division Southeast Asia Department Manila, Philippines Background Philippines is among the fastest growing economies in Southeast Asia • Gross Domestic Product (GDP) growth 6.4 % annually (2010–2018) • Aims to achieve upper middle-income country by 2022 Poor infrastructure hampers competitiveness and economic growth • GDP loss (0.8 %) and productivity loss ($18 billion per year) due to delays from road congestion in Metro Manila alone • Philippines is 97th out of 137 countries based on World Economic Forum Global Competitiveness Report), far behind Malaysia (22nd), Thailand (43rd) and Indonesia (52nd) • Nationwide 98 % of passenger transport and 55 % of freight transport are by road North–South Railway Project Clark–New Clark City Railway (18 km) ADB/JICA cofinancing (ADB pipeline for 2022) Malolos–Clark Railway Project (53 km) ADB/JICA cofinancing, 2 sections: ▪Malolos–Clark–Clark Int’l Airport ▪Solis - Blumentritt Tutuban – Malolos (37 km) JICA financing South Commuter Railway (55 km) Solis Blumentritt ADB/JICA cofinancing Tutuban (ADB pipeline for 2021) ▪Blumentritt – Calamba ▪Senate – FTI – Bicutan (tunnel connection to MMSP) Notes: JICA = Japan International Cooperation Agency MMSP = Metro Manila Subway Project Financing arrangements ADB – Asian Development Bank • Civil works (viaduct, bridges, stations, tunnel, depot) • Capacity development under Technical Assistance loan -

26The Performing Arts

TICKETS AVILABLE AT ALL TICKETWORLD OUTLETS AND ONLINE AT HTTP://TICKETWORLD.COM.PH/MANILASCOPE CONTENTSJUNE2017 8 TOYCON PH BRITNEY SPEARS Global Pop Superstar finally 10 coming to Manila FATHEr’S DAY 15 Tribute TECH REVIEW 20 featuring Samsung S8 Series 24 HOT SPOTS THE PERFORMING ARTS 26 are Alive in Metro Manila 29 TICKETBOOTH.PH 4 june2017issue | manilascope.com june2017issue | manilascope.com 5 EDITor’s NoTE h yes it is June, officially the start of the rainy season in the Philippines. OI’m still in disbelief that summer has waived goodbye so soon. And along with summer’s departure, we also bid adieu to the extremely hot weather it brought. Many would think that there will be less exciting events and happenings now that school year is about to start. Let me tell you that the fun is just starting here in Manilascope. I guarantee you that you are about to be blown away with the massive line up of hottest events that we have for you in this issue. We are in a super treat that the phenomenal icon and world superstar Britney Spears will rock the stage of MOA Arena on June 15th. Yes, it’s her very first time in Manila so I hope you were able to buy your tickets already because it’s fast selling, if not, sold out. No one else other than the pop princess Britney Spears deserves our June cover. Thanks to Wilbros Live for bringing her in our motherland. Watch out for Monty Python’s Spamalot play opening on July by Upstart Productions. -

DOLE-NCR for Release AEP Transactions As of 7-16-2020 12.05Pm

DOLE-NCR For Release AEP Transactions as of 7-16-2020 12.05pm Company Address Transaction No. 3M SERVICE CENTER APAC, INC. 17TH, 18TH, 19TH FLOORS, BONIFACIO STOPOVER CORPORATE CENTER, 31ST STREET COR., 2ND AVENUE, BONIFACIO GLOBAL CITY, TAGUIG CITY TNCR20000756 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000178 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000283 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000536 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000554 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000569 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000607 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000617 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000632 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000633 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000638 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000680 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY -

Order Received to Supply 240 Train Cars for Philippines' Metro Manila Subway

Press Release December 21, 2020 Sumitomo Corporation Japan Transport Engineering Company Order Received to Supply 240 Train Cars for Philippines’ Metro Manila Subway First Subway Project in the Philippines Sumitomo Corporation (Head Office: Chiyoda-ku, Tokyo; Representative Director, President and Chief Executive Officer: Masayuki Hyodo) and Japan Transport Engineering Company (Head Office: Yokohama-shi, Kanagawa Prefecture; President and Representative Director: Takao Nishiyama; hereinafter, “J-TREC”) have received an order from the Department of Transportation (DOTr) of the Republic of the Philippines to supply 240 train cars for the contract package CP107 of the country’s Metro Manila Subway Project Phase 1 (between Quezon City in the north and Parañaque City in the south). The CP107 contract was signed on December 15, 2020. Sumitomo Corporation and J-TREC received this order following the order to supply 104 train cars for the North-South Commuter Railway Project in July 2019. In the Metropolitan Manila area, where the population continues to grow due to rapid economic growth, population concentration is causing traffic congestion and air pollution that are becoming more serious year by year. Building efficient and economical public transportation networks is a pressing issue. To fully develop its infrastructure, the Philippines government is promoting a large-scale infrastructure development plan called “Build Build Build,” in which the Metro Manila Subway Project is considered a core project. The CP107 project is to be undertaken as part of the Official Development Assistance (ODA) program of Japan based on a loan aid agreement between the Japan International Cooperation Agency (JICA) and the Philippines government. The Philippines’ first subway project (a total of 17 stations, including 13 underground stations, and covering approximately 36 kilometers) aims to connect the northern city of Quezon to the southern city of Parañaque in the Metropolitan Manila area. -

Poblacion, Makati : Trending Now Partners

manilascope MAY 2018 .com 10TH SECRETARIES AND ADMINSTRATIVE PROFESSIONALS SUMMIT MOTHER’S DAY DATE IDEAS DOWNLOAD YOUR MAGAZINE FOR LIVE IN STA. ROSA LAGUNA MAY 31, 7:30 PM DO NOT FREE REMOVE 10 PERFECT LABOR DAY FROM VACATIONS THIS 2018 PREMISES Poblacion, Makati : Trending Now partners 2 manilascope.com | MAY 2018 Inside Manila CONTENTs MAY 2018 Top 10 Perfect Labor Day Vacations this 2018 6 Healthy Food in Manila, Anyone? 11 Editor’s Picks 13 Events Calendar 15 Hobbies That Help Spark Your Inner Creativity 17 Mother’s Day Ideas 22 Hot Spots 25 Trendy Poblacion! 28 4 manilascope.com | MAY 2018 Editor’s About Us Note MAY 2018 Ahoy! At last, after a couple of months of hibernating, we are PUBLISHER by Enlightened Entertainment finally bringing back this monthly issue of the Manilascope under the license of Wittygekko Inc. Magazine! For the past few days, we had a lot of things in our plate that we must finish and prioritize. Thus, we had to set this magazine aside for the time being. Now that we have EDITOR-IN-CHIEF Carol Thor organized our group and we can better provide everyone with fresh content of the latest happenings in the Metro, it is time CONSULTANT Antony Thor for a rebound! CONTRIBUTORS For everyone’s reference, Manilascope is a platform for all events and happenings across Metro Manila. You can find all Erin Joan Yang content in our website (www.manilascope.com). Go ahead Faye Martinez and take a look of upcoming events and, who knows, you Czarina Pinlac might discover an occasion that will happen near you! In Martin Santos addition, we have a newsletter, a mobile app that you can download for free (available in both Android and iOS), a blog section in which you are reading right now, and a monthly PHOTOGRAPH/VIDEO Janjan Capili magazine that summarizes most major happenings of the current month! DESIGN Vinna Vinz Now, without further ado, let us present to you what’s in store for this issue. -

Sec 17-A Fy 2018

12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports); Yes [ X ] No [ ] (b) has been subject to such filing requirements for the past ninety (90) days. Yes [ X ] No [ ] 13. State the aggregate market value of the voting stock held by non-affiliates of the registrant. P1,931,103,029 as of December 31, 2018 APPLICABLE ONLY TO ISSUERS INVOLVED IN INSOLVENCY/SUSPENSION OF PAYMENTS PROCEEDINGS DURING THE PRECEDING FIVE YEARS: 14. Check whether the issuer has filed all documents and reports required to be filed by Section 17 of the Code subsequent to the distribution of securities under a plan confirmed by a court or the Commission. Yes [ ] No [X] DOCUMENTS INCORPORATED BY REFERENCE 15. If any of the following documents are incorporated by reference, briefly describe them and identify the part of SEC Form 17-A into which the document is incorporated: Consolidated Financial Statements as of and for year ended December 31, 2018 (Incorporated as reference for Item 7 to 12 of SEC Form 17-A) ________________________________________________________________________ CENTURY PROPERTIES GROUP INC. Page 2 of 84 SEC Form 17-A TABLE OF CONTENTS PART I. BUSINESS AND GENERAL INFORMATION 4 Item 1 Business……………………………………………………………………………………………... 4 Item 1.1 Overview…………………………………………………………………………. -

Metro Manila Market Update Q1 2017

RESEARCH METRO MANILA MARKET UPDATE Q1 2017 METRO MANILA REAL ESTATE SECTOR REVIEW METRO MANILA AND THE THREAT OF EMERGING CITIES The attractiveness of Metro Manila for real estate developers and investors continues to exist. Although highly congested and vacancy rates are constantly dwindling, it is still the best location for business and investment activities. Considering that the seat of government, head offices of key companies, and the most reputable universities and institutions are located in Metro Manila, demand is perceived to always be buoyant and pervasive. The real challenge is innovation and the creation of new stock to cater to the limitless demand. The Philippine National Economic and Development Authority defines Philippine Emerging Cities as cities, relative to Manila, that are rapidly catching up in terms of business activities, innovation and ability to attract people. A few of the notable emerging cities in the Philippines are Angeles (Clark), Cebu, Davao, Iloilo and Zamboanga. Cebu, Davao and Iloilo are top 5, 6 and 8, respectively, among the Philippine Highly Urbanized Cities (HUC) of the country. Angeles City’s makings is supplemented by the much- awaited Clark Green City. Zamboanga City was identified as one of the emerging cities when it comes to information technology Source: Wikipedia operations. The city has the propensity to flourish being the third major gateway and transshipment important transportation networks, largest city in the Philippines in hub in Northern Mindanao, it will increase access to jobs and terms of land area. Furthermore, continue to be a key educational services by people in smaller Bacolod, Bohol, Leyte, Naga, center in the region. -

Domestic Branch Directory BANKING SCHEDULE

Domestic Branch Directory BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays cor Gen. Araneta St. and Aurora Blvd., Cubao, Quezon 1 Q.C.-Cubao Main 911-2916 / 912-1938 9:00 AM – 4:00 PM City 912-3070 / 912-2577 / SRMC Bldg., 901 Aurora Blvd. cor Harvard & Stanford 2 Q.C.-Cubao-Harvard 913-1068 / 912-2571 / 9:00 AM – 4:00 PM Sts., Cubao, Quezon City 913-4503 (fax) 332-3014 / 332-3067 / 3 Q.C.-EDSA Roosevelt 1024 Global Trade Center Bldg., EDSA, Quezon City 9:00 AM – 4:00 PM 332-4446 G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 4 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Elliptical Road cor. Kalayaan Avenue, Diliman, Quezon 920-3353 / 924-2660 / 5 Q.C.-Elliptical Road 9:00 AM – 4:00 PM City 924-2663 Aurora Blvd., near PSBA, Brgy. Loyola Heights, 421-2331 / 421-2330 / 6 Q.C.-Katipunan-Aurora Blvd. 9:00 AM – 4:00 PM Quezon City 421-2329 (fax) 335 Agcor Bldg., Katipunan Ave., Loyola Heights, 929-8814 / 433-2021 / 7 Q.C.-Katipunan-Loyola Heights 9:00 AM – 4:00 PM Quezon City 433-2022 February 07, 2014 : G/F, Linear Building, 142 8 Q.C.-Katipunan-St. Ignatius 912-8077 / 912-8078 9:00 AM – 4:00 PM Katipunan Road, Quezon City 920-7158 / 920-7165 / 9 Q.C.-Matalino 21 Tempus Bldg., Matalino St., Diliman, Quezon City 9:00 AM – 4:00 PM 924-8919 (fax) MWSS Compound, Katipunan Road, Balara, Quezon 927-5443 / 922-3765 / 10 Q.C.-MWSS 9:00 AM – 4:00 PM City 922-3764 SRA Building, Brgy. -

CPGI Bond Prospectus | February 9, 2021

Century Properties Group Inc. (incorporated in the Republic of the Philippines) ₱2,000,000,000 with an Oversubscription Option of up to ₱1,000,000,000 Fixed Rate 3-Year Bonds due 2024 at 4.8467% p.a. Issue Price: 100% of Face Value Sole Issue Manager, Sole Lead Underwriter and Sole Bookrunner The date of this Prospectus is February 9, 2021. THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS ACCURATE OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE AND SHOULD BE REPORTED IMMEDIATELY TO THE SECURITIES AND EXCHANGE COMMISSION. Office Address Contact Numbers Century Properties Group Inc. Trunkline (+632) 7793-5500 21st Floor Pacific Star Building, Cellphone (+63917) 555-5274 Sen. Gil Puyat Avenue corner Makati Avenue, www.century-properties.com Makati City 1200 Century Properties Group Inc. (the “Issuer” or the “Company” or “CPGI” or the “Group”) is offering Unsecured Peso-denominated Fixed-Rate Retail Bonds (the “Bonds”) with an aggregate principal amount of ₱2,000,000,000, with an Oversubscription Option of up to ₱1,000,000,000. The Bonds are comprised of 4.8467% p.a. three-year bonds. The Bonds will be issued by the Company pursuant to the terms and conditions of the Bonds on March 1, 2021 (the "Issue Date"). Interest on the Bonds will be payable quarterly in arrears; commencing on June 1, 2021 for the first Interest Payment Date and on March 1, June 1, September 1 and December 1 of each year for each Interest Payment Date at which the Bonds are outstanding, or the subsequent Business Day without adjustment if such Interest Payment Date is not a Business Day. -

(Cpd) Council for Physicians List of Accredited Providers As of September 26, 2018

CONTINUING PROFESSIONAL DEVELOPMENT (CPD) COUNCIL FOR PHYSICIANS LIST OF ACCREDITED PROVIDERS AS OF SEPTEMBER 26, 2018 ACCREDITATION E-MAIL ADDRESS TELEPHONE NO. NO. NAME OF PROVIDER ADDRESS FAX NO. DATE OF EXPIRATION Philippine Medical Association PMA Bldg., North Avenue, Quezon [email protected] / 929-6366 1 2012-001 (PMA) City www.philippinemedicalassociation.org Fax: 929-6951 13-Feb-21 College of Medicine, University of 547 Pedro Gil St., Ermita, Manila, 2 2012-002 the Philippines Philippines, 1000 [email protected] 0918-905-0862 18-Apr-20 Rm. 2007 Medical Arts Bldg., UST 749-9707 Fax No. 740- 3 2012-003 Dementia Society of the Philippines Hospital, España, Manila www.dementia.org.ph 9725 14-Feb-15 [email protected] / Unit 25 Facilities Centre, #548 [email protected]/ (632) 531-1278/ 534- 4 2012-004 Diabetes Philippines Shaw Blvd., Mandaluyong City www.diabetesphil.org 9559 12-Jul-20 Unit 205 The Garden Heights [email protected] / Condominium 268 E. Rodriguez Sr. [email protected] / 584-2700 5 2012-005 Pain Society of the Philippines, Inc. Avenue, Quezon city www.painsociety.ph Cel: 0917-6213705 13-Mar-20 Unit 4 Metro Square Townehomes, 374-1855 Pediatric Infectious Disease No. 35 Scout Tuazon cor. Scout de [email protected]/ Fax No. 412-6998 6 2012-006 Society of the Philippines (PIDSP) Guia, Quezon City www.pidsphil.org Cel: 0917-834-9837 13-Feb-21 Room 403 PPS Building, #52 Perinatal Association of the Kalayaan Avenue, Brgy. Malaya, [email protected]/ 925-3538 7 2012-007 Philippines, Inc. Quezon City www.perinatphil.org.ph Cel: 0920-945-3513 13-Feb-21 516-2900 / 405-0140 Philippine Academy of Family [email protected] / Fax: 254-5646 8 2012-008 Physicians, Inc. -

Sec 17-A Fy 2019

SECURITIES AND EXCHANGE COMMISSION ANNUAL REPORT PURSUANT TO SECTION 17 SEC FORM 17-A OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended: December 31, 2019 2. SEC Identification Number: 60566 3. BIR Tax Identification No.: 004-504-281-000 4. Exact name of issuer as specified in its charter: CENTURY PROPERTIES GROUP INC. 5. Province, Country or other jurisdiction of incorporation or organization: Philippines 6. Industry Classification Code: (SEC Use Only) 7. Address of principal office/Postal Code: 21st Floor, Pacific Star Building, Sen Gil Puyat Avenue corner Makati Avenue, Makati City 8. Issuer's telephone number, including area code: (632) 7938905 9. Former name, former address, and former fiscal year, if changed since last report: 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sec. 4 and 8 of the RSA: Title of Each Class No. of Shares of Common Stock Outstanding and as Issued of December 31, 2018 COMMON 11,599,600,690 shares of stock outstanding 100,123,000 treasury shares PREFERRED 3,000,0000,000 11. Are any or all of these securities listed on a Stock Exchange. Yes [ X ] 11,699,723,690 common shares No [ ] If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange, Inc. Common Shares 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports); Yes [ X ] No [ ] (b) has been subject to such filing requirements for the past ninety (90) days.