Bitcoin Protocol Main Threats

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

YEUNG-DOCUMENT-2019.Pdf (478.1Kb)

Useful Computation on the Block Chain The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters Citation Yeung, Fuk. 2019. Useful Computation on the Block Chain. Master's thesis, Harvard Extension School. Citable link https://nrs.harvard.edu/URN-3:HUL.INSTREPOS:37364565 Terms of Use This article was downloaded from Harvard University’s DASH repository, and is made available under the terms and conditions applicable to Other Posted Material, as set forth at http:// nrs.harvard.edu/urn-3:HUL.InstRepos:dash.current.terms-of- use#LAA 111 Useful Computation on the Block Chain Fuk Yeung A Thesis in the Field of Information Technology for the Degree of Master of Liberal Arts in Extension Studies Harvard University November 2019 Copyright 2019 [Fuk Yeung] Abstract The recent growth of blockchain technology and its usage has increased the size of cryptocurrency networks. However, this increase has come at the cost of high energy consumption due to the processing power needed to maintain large cryptocurrency networks. In the largest networks, this processing power is attributed to wasted computations centered around solving a Proof of Work algorithm. There have been several attempts to address this problem and it is an area of continuing improvement. We will present a summary of proposed solutions as well as an in-depth look at a promising alternative algorithm known as Proof of Useful Work. This solution will redirect wasted computation towards useful work. We will show that this is a viable alternative to Proof of Work. Dedication Thank you to everyone who has supported me throughout the process of writing this piece. -

Smart Contracts: Building Blocks for Digital Markets

1/25/2018 Nick Szabo -- Smart Contracts: Building Blocks for Digital Markets Smart Contracts: Building Blocks for Digital Markets Copyright (c) 1996 by Nick Szabo permission to redistribute without alteration hereby granted Glossary (This is a partial rewrite of the article which appeared in Extropy #16) Introduction The contract, a set of promises agreed to in a "meeting of the minds", is the traditional way to formalize a relationship. While contracts are primarily used in business relationships (the focus of this article), they can also involve personal relationships such as marraiges. Contracts are also important in politics, not only because of "social contract" theories but also because contract enforcement has traditionally been considered a basic function of capitalist governments. Whether enforced by a government, or otherwise, the contract is the basic building block of a free market economy. Over many centuries of cultural evolution has emerged both the concept of contract and principles related to it, encoded into common law. Algorithmic information theory suggests that such evolved structures are often prohibitively costly to recompute. If we started from scratch, using reason and experience, it could take many centuries to redevelop sophisticated ideas like property rights that make the modern free market work [Hayek]. The success of the common law of contracts, combined with the high cost of replacing it, makes it worthwhile to both preserve and to make use of these principles where appropriate. Yet, the digital revolution is radically changing the kinds of relationships we can have. What parts of our hard-won legal tradition will still be valuable in the cyberspace era? What is the best way to apply these common law principles to the design of our on-line relationships? Computers make possible the running of algorithms heretofore prohibitively costly, and networks the quicker transmission of larger and more sophsiticated messages. -

Piecework: Generalized Outsourcing Control for Proofs of Work

(Short Paper): PieceWork: Generalized Outsourcing Control for Proofs of Work Philip Daian1, Ittay Eyal1, Ari Juels2, and Emin G¨unSirer1 1 Department of Computer Science, Cornell University, [email protected],[email protected],[email protected] 2 Jacobs Technion-Cornell Institute, Cornell Tech [email protected] Abstract. Most prominent cryptocurrencies utilize proof of work (PoW) to secure their operation, yet PoW suffers from two key undesirable prop- erties. First, the work done is generally wasted, not useful for anything but the gleaned security of the cryptocurrency. Second, PoW is natu- rally outsourceable, leading to inegalitarian concentration of power in the hands of few so-called pools that command large portions of the system's computation power. We introduce a general approach to constructing PoW called PieceWork that tackles both issues. In essence, PieceWork allows for a configurable fraction of PoW computation to be outsourced to workers. Its controlled outsourcing allows for reusing the work towards additional goals such as spam prevention and DoS mitigation, thereby reducing PoW waste. Meanwhile, PieceWork can be tuned to prevent excessive outsourcing. Doing so causes pool operation to be significantly more costly than today. This disincentivizes aggregation of work in mining pools. 1 Introduction Distributed cryptocurrencies such as Bitcoin [18] rely on the equivalence \com- putation = money." To generate a batch of coins, clients in a distributed cryp- tocurrency system perform an operation called mining. Mining requires solving a computationally intensive problem involving repeated cryptographic hashing. Such problem and its solution is called a Proof of Work (PoW) [11]. As currently designed, nearly all PoWs suffer from one of two drawbacks (or both, as in Bitcoin). -

Alternative Mining Puzzles

Cryptocurrency Technologies Alternative Mining Puzzles Alternative Mining Puzzles • Essential Puzzle Requirements • ASIC-Resistant Puzzles • Proof-of-Useful-Work • Non-outsourceable Puzzles • Proof-of-Stake “Virtual Mining” Puzzles (recap) Incentive system steers participants Basic features of Bitcoin’s puzzle The puzzle is difficult to solve, so attacks are costly … but not too hard, so honest miners are compensated Q: What other features could a puzzle have? 1 Cryptocurrency Technologies Alternative Mining Puzzles On today’s menu . Alternative puzzle designs Used in practice, and speculative Variety of possible goals ASIC resistance, pool resistance, intrinsic benefits, etc. Essential security requirements Alternative Mining Puzzles • Essential Puzzle Requirements • ASIC-Resistant Puzzles • Proof-of-Useful-Work • Non-outsourceable Puzzles • Proof-of-Stake “Virtual Mining” 2 Cryptocurrency Technologies Alternative Mining Puzzles Puzzle Requirements A puzzle should ... – be cheap to verify – have adjustable difficulty – <other requirements> – have a chance of winning that is proportional to hashpower • Large player get only proportional advantage • Even small players get proportional compensation Bad Puzzle: a sequential Puzzle Consider a puzzle that takes N steps to solve a “Sequential” Proof of Work N Solution Found! 3 Cryptocurrency Technologies Alternative Mining Puzzles Bad Puzzle: a sequential Puzzle Problem: fastest miner always wins the race! Solution Found! Good Puzzle => Weighted Sample This property is sometimes called progress free. 4 Cryptocurrency Technologies Alternative Mining Puzzles Alternative Mining Puzzles • Essential Puzzle Requirements • ASIC-Resistant Puzzles • Proof-of-Useful-Work • Non-outsourceable Puzzles • Proof-of-Stake “Virtual Mining” ASIC Resistance – Why?! Goal: Ordinary people with idle laptops, PCs, or even mobile phones can mine! Lower barrier to entry! Approach: Reduce the gap between custom hardware and general purpose equipment. -

Read the Report Brief

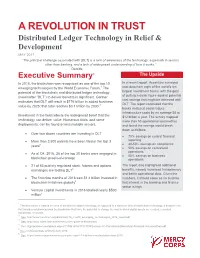

A REVOLUTION IN TRUST Distributed Ledger Technology in Relief & Development MAY 2017 “The principal challenge associated with [DLT] is a lack of awareness of the technology, especially in sectors other than banking, and a lack of widespread understanding of how it works.” - Deloitte Executive Summary1 The Upside In 2016, the blockchain was recognized as one of the top 10 In a recent report, Accenture surveyed emerging technologies by the World Economic Forum.2 The cost data from eight of the world’s ten potential of the blockchain and distributed ledger technology largest investment banks, with the goal of putting a dollar figure against potential (hereinafter “DLT”) to deliver benefits is significant. Gartner cost savings that might be achieved with estimates that DLT will result in $176 billion in added business DLT. The report concluded that the value by 2025; that total reaches $3.1 trillion by 2030.3 banks analyzed could reduce infrastructure costs by an average $8 to Investment in the field reflects the widespread belief that the $12 billion a year. The survey mapped technology can deliver value. Numerous trials, and some more than 50 operational cost metrics deployments, can be found across multiple sectors. and found the savings would break down as follows: Over two dozen countries are investing in DLT 70% savings on central financial More than 2,500 patents have been filed in the last 3 reporting 4 30-50% savings on compliance years 50% savings on centralized operations As of Q4, 2016, 28 of the top 30 banks were engaged in 50% savings on business blockchain proofs-of-concept operations. -

On Trade-Offs of Applying Block Chains for Electronic Voting Bulletin

On Trade-offs of Applying Block Chains for Electronic Voting Bulletin Boards Sven Heiberg1, Ivo Kubjas1, Janno Siim3;4, and Jan Willemson2;3 1 Smartmatic-Cybernetica Centre of Excellence for Internet Voting Ulikooli¨ 2, 51003 Tartu, Estonia fsven,[email protected] 2 Cybernetica AS, Ulikooli¨ 2, 51003 Tartu, Estonia [email protected] 3 Software Technology and Applications Competence Center Ulikooli¨ 2, 51003 Tartu, Estonia 4 Institute of Computer Science, University of Tartu Ulikooli¨ 18, 50090 Tartu, Estonia [email protected] Abstract. This paper takes a critical look at the recent trend of building electronic voting systems on top of block chain technology. Even though being very appealing from the election integrity perspective, block chains have numerous technical, economical and even political drawbacks that need to be taken into account. Selecting a good trade-off between de- sirable properties and restrictions imposed by different block chain im- plementations is a highly non-trivial task. This paper aims at bringing some clarity into performing this task. We will mostly be concentrating on public permissionless block chains and their applications as bulletin board implementations as these are the favourite choices in majority of the recent block chain based voting protocol proposals. 1 Introduction In virtually all of the modern democratic societies, democracy (translated from Greek roughly as rule of the people) is implemented via some sort of public opinion polling e.g. voting on the elections of representative bodies. Regrettably, the process of public polling is very fragile. Many things can go wrong, and have gone wrong in the history of elections. To address the his- torically experienced problems, many requirements have been put forward and many measures have been developed to meet them. -

Smart Contracts and Distributed Ledger Technology: a Lawyer’S Guide

Smart Contracts and Distributed Ledger Technology: A Lawyer’s Guide Presented by: Ken Moyle Clear Law Institute | 4601 N. Fairfax Dr., Ste 1200 | Arlington | VA | 22203 www.clearlawinstitute.com Questions? Please call us at 703-372-0550 or email us at [email protected] All-Access Membership Program ● Earn continuing education credit (CLE, CPE, SHRM, HRCI, etc.) in all states at no additional cost ● Access courses on a computer, tablet, or smartphone ● Access more than 75 liVe webinars each month ● Access more than 750 on-demand courses Register within 7 days after the webinar using promo code “7member” to receive a $200 discount off the $799 base price. Learn more and register here: http://clearlawinstitute.com/member Clear Law Institute, © 2018 Smart Contracts and Distributed Ledger Technology A Lawyer’s Guide Agenda Smart Contracts: Theory and Reality Concepts and Confusion • Legal vs. Technical viewpoints The Lexicon • Common Accord • Distributed Ledger Initial Coin Offerings and SAFTs • Blockchain Regulatory Developments • Cryptocurrency • State blockchain statutes • Smart Contracts • Delaware Resources www.ClearLawInstitute.com (703) 372-0550 Clear Law Institute, © 2018 “ The digital revolution is radically changing the kinds of relationships we can have. What parts of our hard- won legal tradition will still be valuable in the cyberspace era? ” - Nick Szabo, 1996 “What is the best way to apply these common law principles to the design of our on-line relationships?” Integrity of record Trust in the Enforceability outcome -

Cryptocurrency and the Blockchain: Technical Overview and Potential Impact on Commercial Child Sexual Exploitation

Cryptocurrency and the BlockChain: Technical Overview and Potential Impact on Commercial Child Sexual Exploitation Prepared for the Financial Coalition Against Child Pornography (FCACP) and the International Centre for Missing & Exploited Children (ICMEC) by Eric Olson and Jonathan Tomek, May 2017 Foreword The International Centre for Missing & Exploited Children (ICMEC) advocates, trains and collaborates to eradicate child abduction, sexual abuse and exploitation around the globe. Collaboration – one of the pillars of our work – is uniquely demonstrated by the Financial Coalition Against Child Pornography (FCACP), which was launched in 2006 by ICMEC and the National Center for Missing & Exploited Children. The FCACP was created when it became evident that people were using their credit cards to buy images of children being sexually abused online. Working alongside law enforcement, the FCACP followed the money to disrupt the economics of the child pornography business, resulting in the virtual elimination of the use of credit cards in the United States for the purchase of child sexual abuse content online. And while that is a stunning accomplishment, ICMEC and the FCACP are mindful of the need to stay vigilant and continue to fight those who seek to profit from the sexual exploitation of children. It is with this in mind that we sought to research cryptocurrencies and the role they play in commercial sexual exploitation of children. This paper examines several cryptocurrencies, including Bitcoin, and the Blockchain architecture that supports them. It provides a summary of the underground and illicit uses of the currencies, as well as the ramifications for law enforcement and industry. ICMEC is extremely grateful to the authors of this paper – Eric Olson and Jonathan Tomek of LookingGlass Cyber Solutions. -

Introducing Ethereum and Solidity Foundations of Cryptocurrency and Blockchain Programming for Beginners — Chris Dannen Introducing Ethereum and Solidity

Introducing Ethereum and Solidity Foundations of Cryptocurrency and Blockchain Programming for Beginners — Chris Dannen Introducing Ethereum and Solidity Foundations of Cryptocurrency and Blockchain Programming for Beginners Chris Dannen Introducing Ethereum and Solidity: Foundations of Cryptocurrency and Blockchain Programming for Beginners Chris Dannen Brooklyn, New York, USA ISBN-13 (pbk): 978-1-4842-2534-9 ISBN-13 (electronic): 978-1-4842-2535-6 DOI 10.1007/978-1-4842-2535-6 Library of Congress Control Number: 2017936045 Copyright © 2017 by Chris Dannen This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmission or information storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. Trademarked names, logos, and images may appear in this book. Rather than use a trademark symbol with every occurrence of a trademarked name, logo, or image, we use the names, logos, and images only in an editorial fashion and to the benefit of the trademark owner, with no intention of infringement of the trademark. The use in this publication of trade names, trademarks, service marks, and similar terms, even if they are not identified as such, is not to be taken as an expression of opinion as to whether or not they are subject to proprietary rights. While the advice and information in this book are believed to be true and accurate at the date of publication, neither the authors nor the editors nor the publisher can accept any legal responsibility for any errors or omissions that may be made. -

Survey on Surging Technology: Cryptocurrency

International Journal of Engineering &Technology, 7 (3.12) (2018) 296-299 International Journal of Engineering & Technology Website: www.sciencepubco.com/index.php/IJET Research paper Survey on Surging Technology: Cryptocurrency Swathi Singh1, Suguna R2, Divya Satish3, Ranjith Kumar MV4 1Research Scholar, 2, 3Professor, 4Assistant Professor 1,2,3,4Department of Computer Science and Engineering, 1,3SKR Engineering College, Chennai, India, 2Vel Tech Rangarajan Dr.Sagunthala Institute of Science and Technology, Chennai, India 4SRM Institute of Science and Technology, Kattankulathur, Chennai. *Corresponding Author Email: [email protected] Abstract The paper gives an insight on cryptography within digital money used in electronic commerce. The combination of digital currencies with cryptography is named as cryptocurrencies or cryptocoins. Though this technique came into existence years ago, it is bound to have a great future due to its flexibility and very less or nil transaction costs. The concept of cryptocurrency is not new in digital world and is already gaining subtle importance in electronic commerce market. This technology can bring down various risks that may have occurred in usage of physical currencies. The transaction of cryptocurrencies are protected with strong cryptographic hash functions that ensure the safe sending and receiving of assets within the transaction chain or blockchain in a Peer-to-Peer network. The paper discusses the merits and demerits of this technology with a wide range of applications that use cryptocurrency. Index Terms: Blockchain, Cryptocurrency. However, the first implementation of Bitcoin protocol routed 1. Introduction many other cryptocurrencies to exist. Bitcoin is a self-regulatory system that is not supported by government or any organization. -

A Survey on Consensus Mechanisms and Mining Strategy Management

1 A Survey on Consensus Mechanisms and Mining Strategy Management in Blockchain Networks Wenbo Wang, Member, IEEE, Dinh Thai Hoang, Member, IEEE, Peizhao Hu, Member, IEEE, Zehui Xiong, Student Member, IEEE, Dusit Niyato, Fellow, IEEE, Ping Wang, Senior Member, IEEE Yonggang Wen, Senior Member, IEEE and Dong In Kim, Fellow, IEEE Abstract—The past decade has witnessed the rapid evolution digital tokens between Peer-to-Peer (P2P) users. Blockchain in blockchain technologies, which has attracted tremendous networks, especially those adopting open-access policies, are interests from both the research communities and industries. The distinguished by their inherent characteristics of disinterme- blockchain network was originated from the Internet financial sector as a decentralized, immutable ledger system for transac- diation, public accessibility of network functionalities (e.g., tional data ordering. Nowadays, it is envisioned as a powerful data transparency) and tamper-resilience [2]. Therefore, they backbone/framework for decentralized data processing and data- have been hailed as the foundation of various spotlight Fin- driven self-organization in flat, open-access networks. In partic- Tech applications that impose critical requirement on data ular, the plausible characteristics of decentralization, immutabil- security and integrity (e.g., cryptocurrencies [3], [4]). Further- ity and self-organization are primarily owing to the unique decentralized consensus mechanisms introduced by blockchain more, with the distributed consensus provided by blockchain networks. This survey is motivated by the lack of a comprehensive networks, blockchains are fundamental to orchestrating the literature review on the development of decentralized consensus global state machine1 for general-purpose bytecode execution. mechanisms in blockchain networks. In this survey, we provide a Therefore, blockchains are also envisaged as the backbone systematic vision of the organization of blockchain networks. -

Books and Papers

APPENDIX A Books and Papers Books Economics Economics in One Lesson, Henry Hazlitt, ISBN-13: 978-0517548233 Basic Economics, Thomas Sowell, ISBN-13: 978-0465060733 Crashed: How a Decade of Financial Crises Changed the World, Adam Tooze, ISBN-13: 978-0670024933 The Ascent of Money, Niall Ferguson, ISBN-13: 978-0143116172 The Ethics of Money Production, Jörg Guido Hülsmann, ASIN: B003NX6Z3W Denationalisation of Money, F. A. Hayek, ASIN: B005DTKORM Society The Sovereign Individual, James Dale Davidson and Lord William Rees-Mogg, ISBN-13: 978-0684832722 Exit, Voice, and Loyalty, Albert O. Hirschman, ASIN: 0674276604 © Harris Brakmić 2019 349 H. Brakmić, Bitcoin and Lightning Network on Raspberry Pi, https://doi.org/10.1007/978-1-4842-5522-3 APPENDIX A BOOKS and PaPERS Technology Mastering Bitcoin 2nd Edition, Andreas Antonopoulos, ASIN: B071K7FCD4 Programming Bitcoin, Jimmy Song, ISBN-13: 978-1492031499 A Dissection of Bitcoin, Paul Huang, ASIN: B0198LXI5K Bitcoin Internals, Chris Clark, ASIN: B00DG8EPT0 Applied Cryptography, Bruce Schneier, ISBN-13: 978-1119096726 Essays and Papers Bitcoin: A Peer-to-Peer Electronic Cash System, Satoshi Nakamoto, https://bitcoin.org/en/bitcoin-paper Bitcoin’s Academic Pedigree, Arvind Narayanan and Jeremy Clark, https://queue.acm.org/detail.cfm?id=3136559 Blockchain Proof-of-Work is a Decentralized Clock, Gregory Trubetskoy, https://grisha.org/blog/2018/01/23/explaining-proof- of-work/ Shelling Out: The Origins of Money, Nick Szabo, https://nakamoto institute.org/shelling-out/ Money, Blockchains, and