Scotland Residential

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Edinburgh PDF Map Citywide Website Small

EDINBURGH North One grid square on the map represents approximately Citywide 30 minutes walk. WATER R EAK B W R U R TE H O A A B W R R AK B A E O R B U H R N R U V O O B I T R E N A W A H R R N G Y E A T E S W W E D V A O DRI R HESP B BOUR S R E W A R U H U H S R N C E A ER R P R T O B S S S E SW E O W H U A R Y R E T P L A HE B A C D E To find out more To travel around Other maps SP ERU W S C Royal Forth K T R OS A E S D WA E OA E Y PORT OF LEITH R Yacht Club R E E R R B C O T H A S S ST N L W E T P R U E N while you are in the Edinburgh and go are available to N T E E T GRANTON S S V V A I E A E R H HARBOUR H C D W R E W A N E V ST H N A I city centre: further afield: download: R S BO AND U P R CH RO IP AD O E ROYAL YACHT BRITANNIA L R IMPERIAL DOCK R Gypsy Brae O A Recreation Ground NEWHAVEN D E HARBOUR D Debenhams A NUE TON ROAD N AVE AN A ONT R M PL RFR G PIE EL SI L ES ATE T R PLA V ER WES W S LOWE CE R KNO E R G O RAN S G T E 12 D W R ON D A A NEWHAVEN MAIN RO N AD STREET R Ocean R E TO RIN K RO IV O G N T IT BAN E SH Granton RA R Y TAR T NT O C R S Victoria Terminal S O A ES O E N D E Silverknowes Crescent VIE OCEAN DRIV C W W Primary School E Starbank A N Golf Course D Park B LIN R OSWALL R D IV DRI 12 OAD Park SA E RINE VE CENT 13 L Y A ES P A M N CR RIMR R O O V O RAN T SE BA NEWHAVEN A G E NK RO D AD R C ALE O Forthquarter Park R RNV PORT OF LEITH & A O CK WTH 14 ALBERT DOCK I HA THE SHORE G B P GRANTON H D A A I O LT A Come aboard a floating royal N R W N L O T O O B K D L A W T A O C O R residence or visit the dockside bars Scottish N R N T A N R E E R R Y R S SC I E A EST E D L G W N O R D T D O N N C D D and bistros; steeped in maritime S A L A T E A E I S I A A Government DRI Edinburgh College I A A M K W R L D T P E R R O D PA L O Y D history and strong local identity. -

![Covering Colinton, Longstone & Slateford]](https://docslib.b-cdn.net/cover/3961/covering-colinton-longstone-slateford-53961.webp)

Covering Colinton, Longstone & Slateford]

Edinburgh’s Great War Roll of Honour Colinton District Great War Roll of Honour: Restricted [Covering Colinton, Longstone & Slateford] This portion of the Edinburgh Great War Roll of Honour is part of a much larger work that will be published over a period of time. It should also be noted that this particular roll is also a restricted one of Great War casualties giving basic details of each casualty: Name, Rank, Battalion/Ship/Squadron, Regiment/Service, Number. Special awards. Cause and date of death. Age. Place commemorated or buried. Birthplace. District of Edinburgh’s Great War Roll of Honour name is recorded in. The reason this roll is presently restricted is that we would like to invite and give the greater community the opportunity to fill out the story of each casualty, even helping identify casualties that appear on local memorials that cannot be clearly identified or have some details missing. These latter casualties appear in red with some having question marks in the area that needs to be clarified. It is also worth noting at this point that the names of some casualties appear on more than one district. The larger Roll of Honour [RoH] will also include information about those who served and survived and again the hope is that the wider community will come forward and share the story of their ancestors’ who served in the Great War, whether a casualty or survivor. The larger RoH will contain information such as: Name. Rank, Battalion/Ship/Squadron, Regiment/Service. Born when and where? Parent’s names and address. -

Kirkliston to Cramond

Kirkliston to Cramond Last leg of a 4-part route down the full length of the valley of the River Almond. Starts Kirkliston. Quarter hourly bus (38) from Edinburgh. Also buses 63 and 600. Varied walk: banks of R. Almond, beside the airport runway; woods, estate; coast. Distance: 14 km Walk begins at bus stop on Kirkliston High St. adjacent to The Square beside the old Parish Church. Find a narrow snicket, behind black safety railings, next to a whitewashed cottage (2 doors right of the cottage with the ‘Amulree’ wall plaque). Follow the snicket as it doglegs left and the right towards the river. You emerge from Cobblers Close onto Wellflats Rd. Bear right. After a few paces go straight over the old railway path. After a few more paces, at the Y-junction, take the right-hand road straight ahead with a neat, brown fence on the right. The road looks to be ending but keep straight ahead along a really narrow pathway between houses, with a high fence on the right. This alleyway leads to the river bank. Carry on along a most pleasant stretch of river bank until you come to a bridge. Cross over. Turn sharp left to follow reasonably close to the riverside. Keep to the thin footpath on the low levee, rather than the field edge. Soon you come to the strange set of buildings of Hallyards. Walk straight ahead, keeping to the left of buildings. There are all sorts of strange containers, old vehicles and trucks. Keep going until your way appears to be blocked, or partially blocked. -

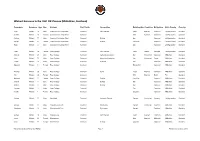

1851 Census (Midlothian).Xlsx

Wishart Surname in the 1851 UK Census (Midlothian, Scotland) Forename Surname Age Sex Address Civil Parish Occupation Relationship Condition Birthplace Birth County Country Hugh Wishart 33 Male Cramond Park Lodge West Cramond Farm Servant Head Married Cramond Linlithgowshire Scotland Isabella Wishart 32 Female Cramond Park Lodge West Cramond Wife Married Cramond Linlithgowshire Scotland Andrew Wishart 11 Male Cramond Park Lodge West Cramond Scholar Son Cramond Linlithgowshire Scotland Cecilia Wishart 6 Female Cramond Park Lodge West Cramond Scholar Daughter Cramond Linlithgowshire Scotland Hugh Wishart 4 Male Cramond Park Lodge West Cramond Son Cramond Linlithgowshire Scotland Janet Wishart 50 Female Rose Cottage Cramond Farm Servant Head Widow Bathgate Linlithgowshire Scotland Andrew Wishart 21 Male Rose Cottage Cramond Agricultural Labourer Son Unmarried Cramond Midlothian Scotland John Wishart 19 Male Rose Cottage Cramond Agricultural Labourer Son Unmarried Currie Midlothian Scotland James Wishart 13 Male Rose Cottage Cramond At Home Son Cramond Midlothian Scotland Margaret Wishart 3 Female Rose Cottage Cramond Grandchild Cramond Midlothian Scotland Thomas Wishart 36 Male Rose Cottage Cramond Carter Head Married Cramond Midlothian Scotland Ann Wishart 36 Female Rose Cottage Cramond Wife Married Beath Fife Scotland Margaret Wishart 11 Female Rose Cottage Cramond Scholar Daughter Cramond Midlothian Scotland Andrew Wishart 9 Male Rose Cottage Cramond Scholar Son Cramond Midlothian Scotland William Wishart 6 Male Rose Cottage Cramond Scholar -

5 Ravelston Court, Edinburgh, EH12 6HQ an Attractive First Floor Flat with Open Outlook to the Front

5 Ravelston Court, Edinburgh, EH12 6HQ An attractive first floor flat with open outlook to the front. An attractive first floor flat with open outlook to the front. It is a light filled, spacious property with private parking and garage. Located in the highly sought after residential area of Ravelston this first floor flat forms part of a desirable development surrounded by well maintained garden grounds. It lies within easy reach of the City Centre and West End. The property benefits from a single garage, secure entry phone system and lift access. Internally the property is bright and well proportioned but could benefit from some upgrading and decoration to fulfil it’s potential as a fantastic home. It benefits from electric central heating and double glazing. A pleasing feature of the property is the large lounge/dining room which has a dual aspect with large patio doors to the front looking over a Juliet balcony. ACCOMMODATION Hall, Sitting/Diningroom, three Bedrooms, Kitchen,Bathroom and Shower room. There is a single garage and private parking. 5 Ravelston Court, Ravelston Dykes, LOCATION Edinburgh, Ravelston is a prestigious residential area situated Midlothian, EH12 6HQ approximately 2 miles west of the city centre. There is a good range of local shops, bars and restaurants in nearby Roseburn, and Craigleith Approx. Gross Internal Area Retail Park is a short car journey away offering 1237 Sq Ft - 114.92 Sq M a number of larger retail shops including a For identification only. Not to scale. © SquareFoot 2018 Sainsbury’s supermarket, Marks and Spencer and Boots. A gentle stroll along the Water of Leith Walkway takes you to the cafes and boutiques of Stockbridge, the Gallery of Modern Art and the West End. -

Granton Waterfront Regeneration: Consultation Responses Summary Report Stage 1: Tell Us More About Granton Waterfront November 2018

Granton Waterfront Regeneration: Consultation Responses Summary Report Stage 1: Tell us more about Granton Waterfront November 2018 Key themes and the questions asked 01 Place & Identity Question 3: What would attract you to live / work / visit Granton Waterfront? Question 4: There are a number of features in Granton Waterfront which make the area unique including Granton Station building, Madelvic Car Factory, Granton Castle Walled Gardens, Waterfront Promenade, Gasometer and Forthquarter Park. Do you have any ideas of ways in which these could be used in the future? Question 5: What additional space/services do you think the Granton Waterfront area needs in addition to new homes, school and medical centre? 02 Being Outdoors Question 6: Granton Waterfront has a number of outdoor and natural assets including the beach, Forthquarter Park and the Waterfront Promenade. In the future of Granton Waterfront how would you like to see these used and improved? Question 7: Which of the following outdoor projects would you like to see developed in the Granton Waterfront area? 03 Moving Around Question 8: Are there particular barriers in Granton Waterfront that make it difficult for you to get around by foot, bike, car or bus etc? Question 9: What do you think would make getting to and around Granton Waterfront easier? 04 Being Sustainable Question 10: Which of the following do you think should be prioritised to make Granton Waterfront a more environmentally sustainable area? 05 Learning, Work & Local Economy Question 11: Which of the following do you think the local economy needs most? Question 12: What new learning opportunities do you think the area needs most? This survey was live on the consultation hub from 2nd November 2018 to 22nd November 2018. -

Edinburgh City Cycleways Innertube and Little France Park

Edinburgh City Cycleways Innertube 50 51 49 52 LINDSAY RD CRAMOND VILLAGE MARINE DR HAWTHORNVALE WEST HARBOUR RD (FOR OCEAN TERMINAL) CRAIGHALL RD WEST SHORE RD 25 VICTORIA PARK / NEWHAVEN RD and Little France Park Map CRAMOND 2 WEST SHORE RD (FOR THE SHORE) FERRY RD SANDPORT PL CLARK RD LOWER GRANTON RD TRINITY CRES 472 SALTIRE SQ GOSFORD PL 48 TRINITY RD SOUT CONNAUGHT PL WARDIE RD H WATERFRONT AVE BOSWALL TER STEDFASTGATE WEST BOWLING COBURG ST 24 EAST PILTON FERRY RD ST MARKʼS PARK GREEN ST / (FOR GREAT 4 MACDONALD RD PILRIG PARK JUNCTION ST) (FOR BROUGHTON RD / LEITH WALK) DALMENY PARK CRAMOND BRIG WHITEHOUSE RD CRAMONDDAVIDSONʼS RD SOUTH MAINS / PARK WEST PILTON DR / WARRISTON RD SILVERKNOWES RD EAST / GRANTON RD SEAFIELD RD SILVERKNOWES ESPLANADE / / CRAMOND FORESHORE EILDON ST WARRISTON GDNS 26 TO SOUTH QUEENSFERRY WEST LINKS PL / & FORTH BRIDGES GRANTON LEITH LINKS SEAFIELD PL HOUSE Oʼ HILL AVE ACCESS INVERLEITH PARK 1 76 5 (FOR FERRY RD) 3 20 27 CRAIGMILLAR ROYAL BOTANIC GARDEN BROUGHTON RD 21 WARRISTON CRES WESTER DRYLAW DR T WARRISTON RD FERRY RD EAS FILLYSIDE RD EASTER RD / THORNTREEHAWKHILL ST AVERESTALRIG / RD FINDLAY GDNS CASTLE PARK 45 SCOTLAND ST (FOR LEITH WALK)LOCHEND PARK WESTER DRYLAW DR EASTER DRYLAW DR (FOR NEW TOWN) WELLINGTON PL 1 6 54 46 7 SEAFIELD RD 53 KINGS RD TELFORD DR 28 WESTER DRYLAW ROW (FOR WESTERN (FOR TELFORD RD) GENERAL HOSPITAL) (FOR STOCKBRIDGE) / 44 BRIDGE ST / HOLYROOD RD / DYNAMIC EARTH EYRE PL / KING GEORGE V PARK 56 MAIDENCRAIG CRES / DUKEʼS WALK CRAIGLEITH RETAIL PARK ROSEFIELD PARK FIGGATE -

Downloaded Here

Cramond & Barnton Community Council Incorporating Cramond, Barnton, Cammo and Quality Street (West) Chair: Andrew Mather Secretary: Ian Williamson Planning Rep.: Peter Scott 21 Inveralmond Drive 17 Cramond Village 86 Cammo Grove Edinburgh EH4 6JX Edinburgh EH4 6NS Edinburgh EH4 8HD Phone: 336 2336 Phone: 476 3897 Phone: 339 7839 Rick Finc Associates 3 Walker Street Edinburgh EH3 7JY 22/04/2016 Dear Rick CRAIGIEHALL VILLAGE PAN Please accept our gratitude to you and your colleagues for attending last night’s meeting of the Community Council and outlining aspects of the Craigiehall Village proposals, as developed at this early pre-application consultation stage. The following submission is based on views expressed by members of communities we represent, as expressed at your exhibitions, presentation and Q&A session at the Community Council meeting, and subsequent discussion at the meeting. Positive comments have been made in respect of – a. the clear presentation of the proposals, as so far developed, as made by the team verbally and on presentation boards at the Community Council’s meeting, public exhibitions and meeting of local community councils b. the concept of a ‘village’ development, which could be partly self-supporting with community facilities, including shop, primary school, health facilities, and recreational open space c. the inclusion of a Park-and-Ride facility and transport hub to promote use of public transport by residents of the proposed development d. indications that the environmental qualities of the site will be retained wherever possible and that there are opportunities for strengthening the surrounding landscape features to enhance the limited landscape containment of parts of the site. -

River Almond Walkway Management Plan

RIVER ALMOND WALKWAY MANAGEMENT PLAN 2011 – 2020 City of Edinburgh Council Countryside Ranger Service Hermitage of Braid 69a Braid Road Edinburgh EH10 6JF 1 Contents Dcocument Reference Page 1.0 Overview 5 2.0 Purpose of River Almond Walkway Management Plan 5 3.0 City of Edinburgh Council Countryside Ranger Service 5 4.0 General Information 6 4.1 Location 6 4.2 Description of Site 6 4.3 Land Tenure 7 4.4 Designation 7 5.0 The Management Plan in Relation to Legislation, Policy and Relevent Strategies 7 5.1 Local Strategies and Policy 7 5.2 National Legislation, Strategies and Policy 10 6.0 Monitoring and Reviewing 11 6.1 Grounds Maintenance and Taskforce Duties 12 6.2 Parks and Greenspace Survey 13 6.3 Ezytreev 13 7.0 Evaluation 13 7.1 Statement of Significance 13 8.0 Recreation 15 8.1 Recreational Facilities 15 9.0 Partnerships 16 10.0 Marketing and Events 17 11.0 Interpreting the River Almond Walkway 17 12.0 Safety and Security 19 13.0 Sustainability 19 14.0 Significant Key Features 20 14.1 Physical Features 20 14.1.1 Hydrology 20 14.1.2 Geology 21 14.1.3 Soils 23 14.2 Natural Features 24 14.2.1 Habitat 24 14.2.2 Flora 24 14.2.2.1 Woodland Management 24 14.2.2.2 Wooded areas along the River Almond Walkway – current condition 25 14.2.2.3 Arboricultural Management 26 14.2.2.4 Specimen Tree Planting 27 14.2.2.5 Nature Conservation in relation to Woodland Management 27 14.2.2.6 Rhododendron/Laurel Removal 28 14.2.3 Fauna 28 14.3 Cultural Features 29 14.4 Social Significance 30 15.0 Cramond Ferry Boat 31 16.0 Salvesen Steps 32 2 Dcocument -

It's Our Centenary Issue!

Cramond Grapevine 100_Grapevine 27/08/2018 12:12 Page 1 CRAMOND KIRK MAGAZINE SEPTEMBER 2018 ISSUE No. 100 IT’S OUR CENTENARY ISSUE! When the first edition of a then-unnamed Kirk newsletter edited The Grapevine for the past 50 issues; Grahame Boyne dropped through the letterboxes of the people of Cramond in (and previously Brenda Wilson) collate the adverts; Irene November 1993, giving details of the Christmas Fair and Dunn (and previously Willie Prest) plan and commission Services, I doubt anyone anticipated we’d still be perusing content; Parish Committee conveners have mobilised a vast that very same magazine some 25 years later. distribution network to ensure the magazine reaches The second issue, published in March 1994, contained Easter everyone in the Cramond and Barnton area. Louise Madeley, Eating recipes from Masterchef Sue Lawrence. our Church Secretary, quietly ensures all the components come together smoothly. By the third issue, following a competition, the magazine had a name. Eschewing suggestions like Cramond Eggs and And now, following this landmark edition, The Grapevine is Cramond Cantorial, the shortlist included Cramond Eagle, changing again. Our next issue will appear in full colour, with Pew Review and the Cramond Kirk Beacon, but the winner - more photos, fewer pages, and shorter articles. Longer announced by Russell Barr in his sermon of 5 June 1994 - was features will be published online: you can read them in full on The Grapevine. our website www.cramondkirk.org. “... through the grapevine of the magazine an important This reflects the way more of us get our news nowadays, and ministry takes place,” said Dr Barr. -

The Edinburgh Graveyards Project

The Edinburgh Graveyards Project A scoping study to identify strategic priorities for the future care and enjoyment of five historic burial grounds in the heart of the Edinburgh World Heritage Site The Edinburgh Graveyards Project A scoping study to identify strategic priorities for the future care and enjoyment of ve historic burial grounds in the heart of the Edinburgh World Heritage Site Greyfriar’s Kirkyard, Monument No.22 George Foulis of Ravelston and Jonet Bannatyne (c.1633) Report Author DR SUSAN BUCKHAM Other Contributors THOMAS ASHLEY DR JONATHAN FOYLE KIRSTEN MCKEE DOROTHY MARSH ADAM WILKINSON Project Manager DAVID GUNDRY February 2013 1 Acknowledgements his project, and World Monuments Fund’s contribution to it, was made possi- ble as a result of a grant from The Paul Mellon Estate. This was supplemented Tby additional funding and gifts in kind from Edinburgh World Heritage Trust. The scoping study was led by Dr Susan Buckham of Kirkyard Consulting, a spe- cialist with over 15 years experience in graveyard research and conservation. Kirsten Carter McKee, a doctoral candidate in the Department of Architecture at Edinburgh University researching the cultural, political, and social signicance of Calton Hill, undertook the desktop survey and contributed to the Greyfriars exit poll data col- lection. Thomas Ashley, a doctoral candidate at Yale University, was awarded the Edinburgh Graveyard Scholarship 2011 by World Monuments Fund. This discrete project ran between July and September 2011 and was supervised by Kirsten Carter McKee. Special thanks also go to the community members and Kirk Session Elders who gave their time and knowledge so generously and to project volunteers David Fid- dimore, Bob Reinhardt and Tan Yuk Hong Ian. -

20 Murrayfield Drive Edinburgh

20 MURRAYFIELD DRIVE EDINBURGH 20 Murrayfield Drive Edinburgh Wonderful family home offering spacious and flexible accommodation over three floors. This magnificent family home has retained many prolific period features throughout and benefits from magnificent south facing views over the south of the city and to the Pentland’s beyond. Accommodation Ground Floor: Vestibule, entrance hallway, hall, WC, sitting room/family room, dining room, kitchen, utility/pantry room with study above First floor: Drawing room, master bedroom, WC and bathroom. Second floor: Four double bedrooms, shower room and box room/cupboard Outside Space: South facing front garden, large garden to the rear. Situation Lying within Murrayfield, a well-established and popular residential area, Murrayfield Drive is one of Edinburgh’s most sought after streets. Approximately 1.5 miles to the west of Edinburgh’s centre the area benefits from easy access into the city yet is also conveniently located for the City Bypass, Edinburgh International airport and the motorway links to the North, South and West. Nearby Haymarket Station also offers further transport options. A desired area for many families, some of Edinburgh’s best schools, including The Mary Erskine School, Stewart’s Melville College and St. George’s School for Girls, are within walking distance of the property while several others, including Fettes College and The Edinburgh Academy, are a short drive away. There is a range of local shops in nearby Roseburn, with larger facilities at Craigleith Retail Park including a Sainsbury’s Supermarket and a Marks & Spencer while the art galleries, cafes, delicatessens, bars, restaurants and speciality shops of both Stockbridge and the West End are also conveniently located.