A Key Currency View of Global Imbalance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ft. Myers Rare Coins and Paper Money Auction (08/23/14) 8/23/2014 13% Buyer's Premium 3% Cash Discount AU3173 AB1389

Ft. Myers Rare Coins and Paper Money Auction (08/23/14) 8/23/2014 13% Buyer's Premium 3% Cash Discount AU3173 AB1389 www.gulfcoastcoin.com LOT # LOT # 400 1915S Pan-Pac Half Dollar PCGS MS67 CAC Old Holder 400r 1925 Stone Mountain Half Dollar NGC AU 58 1915 S Panama-Pacific Exposition 1925 Stone Mountain Memorial Half Dollar Commemorative Half Dollar PCGS MS 67 Old NGC AU 58 Holder with CAC Sticker - Toned with Min. - Max. Retail 55.00 - 65.00 Reserve 45.00 Beautiful Colors Min. - Max. Retail 19,000.00 - 21,000.00 Reserve 17,000.00 400t 1925 S California Half Dollar NGC MS 63 1925 S California Diamond Jubilee Half Dollar NGC MS 63 400c 1918 Lincoln Half Dollar NGC MS 64 Min. - Max. Retail 215.00 - 235.00 Reserve 1918 Lincoln Centennial Half Dollar NGC MS 190.00 64 Min. - Max. Retail 170.00 - 185.00 Reserve 150.00 401 1928 Hawaii Half Dollar NGC AU 58 1928 Hawaiian Sesquicentennial Half Dollar NGC AU 58 400e 1920 Pilgrim Half Dollar NGC AU 58 Min. - Max. Retail 1,700.00 - 2,000.00 Reserve 1920 Pilgrim Tercentenary Half Dollar NGC 1,500.00 AU 58 Min. - Max. Retail 68.00 - 75.00 Reserve 55.00 401a 1928 Hawaiian Half Dollar PCGS MS 65 CAC 1928 Hawaiian Sesquicentennial 400g 1921 Alabama Half Dollar NGC MS 62 Commemorative Half Dollar PCGS MS 65 with 1921 Alabama Centennial Commemorative Half CAC Sticker Dollar NGC MS 62 Min. - Max. Retail 4,800.00 - 5,200.00 Reserve Min. - Max. -

In Reaction to Rising Consumer Prices and New Basel III Banking

July 2021, Volume 27 Issue 7 Liberty Coin Service’s Monthly Review of Precious Metals and Numismatics June 29, 2021 In Reaction To Rising Consumer Prices And New Basel III Banking Regulations Taking Effect, US Government Suppresses Gold And Silver Prices! US Dollar Surges In Value Over 2021 Year To Date Results South Africa Rand -2.6% Past 34 Days Through June 28, 2021 Canada Dollar -3.3% Brazil Real -5.2% May 25, 2021-June 28, 2021 Precious Metals Palladium +9.9% U.S. Dollar Index 91.888 +2.22% Currency US $ Change vs Currency Platinum +4.2% US And World Stock Market Indices Sweden Krona +3.1% Silver -0.7% Russell 2000 +17.6% South Africa Rand +2.8% Gold -6.1% Standard & Poors 500 +14.2% New Zealand Dollar +2.7% Numismatics Frankfurt Xetra DAX +13.4% Euro +2.7% US MS-65 Morgan Dollar, Pre-1921 +32.3% NASDAQ +12.5% Denmark Krone +2.7% US MS-63 $20 St Gaudens +1.9% Dow Jones Industrial Average +12.0% US MS-63 $20 Liberty -1.6% Australia S&P/ASX 200 +10.9% Switzerland Franc +2.7% London FT 100 +9.5% Canada Dollar +2.5% US Dollar vs Foreign Currencies Dow Jones World (excluding US) +8.9% Australia Dollar +2.4% Argentina Peso +13.2% Sao Paulo Bovespa +7.1% Colombia Peso +8.2% Tokyo Nikkei 225 +5.8% India Rupee +2.0% Peru New Sol +7.3% Shanghai Composite ` +3.8% Great Britain Pound +1.9% Japan Yen +7.2% Thailand Baht +6.3% 10 Year US Treasury Note interest rate Thailand Baht +1.7% 1.49% +60.22% Switzerland Franc ` +4.0% Japan Yen +1.7% South Korea Won +3.9% Energy and Other Metals Peru New Sol +1.5% Sweden Krona +3.7% Molybdenum +94.8% Singapore -

In 2018, Gold and Silver Prices Poised to Rise Against Unstable US Dollar!

January 2018, Volume 24 Issue 1 Liberty Coin Service’s Monthly Review of Precious Metals and Numismatics January 10, 2018 In 2018, Gold And Silver Prices Poised To Rise Against Unstable US Dollar! Gold’s 2017 Performance 2017 Annual Results Malaysia Ringgit -9.5% Israel Shekel -9.6% Versus Selected Currencies Precious Metals South Africa Rand -9.8% Palladium +58.4% Sweden Krona -10.2% Currency 2017 Gold Price Change Gold +13.6% Argentine Peso +33.0% South Korea Won -11.7% Silver +7.4% Denmark Krone -12.2% Brazil Real +15.6% Platinum +3.7% Euro -12.4% Philippines Peso +14.7% Numismatics U.S. Dollar Index 92.22 -9.84% Hong Kong Dollar +14.4% US MS-63 $20 St Gaudens +9.8% US Dollar +13.6% US MS-63 $20 Liberty +6.4% US And World Stock Market Indices LCS US Currency Index +5.1% NASDAQ +28.2% Indonesia Rupiah +13.1% LCS Collector Key Date Coin Index -0.5% Sao Paulo Bovespa +26.9% Colombia Peso +12.9% LCS Investor Rare Coins Index -1.1% Dow Jones Industrial Average +25.1% New Zealand Dollar +10.1% LCS Collector Generic Coins Index -1.6% Dow Jones World (excluding US) +24.6% Peru New Sol +9.7% US Silver Proof Sets, 1950-1968 -1.7% S&P 500 +19.4% Japan Yen +9.4% LCS Invest Blue Chip Coins Index -2.1% Nikkei 225 +19.1% US Proof Sets, 1968-1998 -4.3% Russell 2000 +13.1% Switzerland Franc +8.6% US MS-65 Morgan Dollar, Pre-1921 -8.5% Frankfurt Xetra DAX +12.5% Mexico Peso +7.8% US Proof Silver Eagles, 1986-1998 -25.2% London FT 100 +7.6% Australia S&P/ASX 200 +7.1% Russia Ruble +6.9% US Dollar vs Foreign Currencies Shanghai Composite +6.6% India Rupee -

Schedule Proposals (1)” of the John Marsh Files at the Gerald R

The original documents are located in Box 71, folder “Schedule Proposals (1)” of the John Marsh Files at the Gerald R. Ford Presidential Library. Copyright Notice The copyright law of the United States (Title 17, United States Code) governs the making of photocopies or other reproductions of copyrighted material. Gerald R. Ford donated to the United States of America his copyrights in all of his unpublished writings in National Archives collections. Works prepared by U.S. Government employees as part of their official duties are in the public domain. The copyrights to materials written by other individuals or organizations are presumed to remain with them. If you think any of the information displayed in the PDF is subject to a valid copyright claim, please contact the Gerald R. Ford Presidential Library. THE WHITE HOUSE WASHINGTON January 24, 1975 APPEARANCE AT EISENHOWER THEATER KENNEDY CENTER Sunday, January 26, 1975 6:00 P.M. to 8:00 P.M. From: Jack Marsh I. PURPOSE To attend the premiere showing of a film, "City Out Of Wilderness" and to participate in the official Bicentennial recognition of this project undertak~n by the United States Capitol Historical Society. II. BACKGROUND, PARTICIPANTS & PRESS PLAN A. Background: The United States Capitol Historical Society, of which you serve on the Honorary Board of Trustees, has two major Bicentennial projects: A film entitled "City Out Of Wilderness" and a sound and light production for the East Front of the Capitol Building. The Kennedy Center showing of the film is its premiere to members of the federal establishment and attendance is by invitation only. -

SELLER MANAGED Reseller Online Auction - Woodbine Road

09/28/21 03:52:48 Kingston (Ontario, Canada) SELLER MANAGED Reseller Online Auction - Woodbine Road Auction Opens: Wed, Nov 13 1:15pm ET Auction Closes: Tue, Nov 19 8:15pm ET Lot Title Lot Title 0001 Bryan Adams Into The Fire LP 0031 Everquest Coin 0002 1954 Canada Five Dollar Bill Note Beattie 0032 The Monks Bad Habits Rasminski 0033 1954 Canada Five Dollar Note Bill 0003 Elton John Greatest Hits Record LP 0034 Sterling Silver Antique Art Deco Pin 0004 1974-75 OPC Henri Richard Hockey Card 0035 1967 Canada One Dollar Centennial Note Bill 0005 April Wine Harder Faster Record LP Beattie Rasminski 0006 Pewter Gothic Pendant 0036 Royal Canadian Mint Coin Watch Mint 0007 Blondie Auto American Record LP 0037 The Pretenders Record LP 0008 1972 Charlton Popeye 115 Comic Book 0038 1776-1976 USA JFK Half Dollar Coin 0009 Foreigner First Record LP 0039 Religious Set Vintage 0010 Sterling Silver Worry Ring Sz 11 0040 1976 USA Two Dollar Note Bill 0011 1975-76 OPC Jacques Lemaire Hockey Card 0041 Vintage I Love New York Pin 0012 Rolling Stones Tattoo You Record LP 0042 2010 OPC Martin St Louis Certified 0013 1975 Matchbox Lesney Die Cast Firetruck Autographed Hockey Card 0014 Antique Sugar Olive Tongs 0043 1972-73 OPC Dave Keon Hockey Card 0015 Michael Jackson Thriller LP 0044 Molly Hatchet Beatin The Odds Record LP 0016 Australia Five Euro Dollar Silver Coin Mint 0045 Harry Potter Snitch Pocket Watch 0017 Native Ulu Knife Pendant Necklace 0046 Vintage Hot Wheels Funny Money Die Cast Brinks Truck 0018 1975 Matchbox Lesney Die Cast Car 0047 Vintage -

COIN AUCTION by Baxa Auctions, LLC Sunday, April 7, 2019 Kenwood Hall, 900 Greeley, Salina, KS Auction Starts at 12:30, Doors Open at 10:30

COIN AUCTION by Baxa Auctions, LLC Sunday, April 7, 2019 Kenwood Hall, 900 Greeley, Salina, KS Auction starts at 12:30, Doors open at 10:30 Note: Payment due immediately after the sale. Please review terms on last page before bidding. Lot # Description Grade Tokens & Misc 1 Silver Certificate Redemption Bullion in Plastic Unc 2 (13) Encased Cents (10-Lincolns, 3-Indian Head) Circ 3 (7) Rectangular Wooden Nickels (1939-1970) Unc 4 (5) Wm. J. Schwartz Hanover, KS Trade Tokens (5c-1$) Circ 5 (4) Coin Design Coasters Unc 6 (4) California $50 Gold Slug Replicas Unc 7 (5) California Souvenir Gold Replicas in Display Case Unc 8 (2) 1961 KS Statehood 3-inch Medals (Silver & Bronze) Unc 9 (2) 1971 Concordia KS 1-inch Medals (Silver & Bronze) Unc 10 1960 P&D Large/Small Date Cent Set in Plastic (4 coins) Unc 11 1960 Proof Large/Small Date Cent Set in Plastic (2 coins) Proof 12 1995-P Unc Bank Set & 1976 Bicentennial Coinage Mixed 13 1979 & 1980 ANA Convention Souvenir Sets (5 $ Coins) Unc Groups 14 (3) Indian Head Cents (1905, 1906, 1907) AU 15 (4) Jefferson Unc 5c (1938-D&S, 1939-D&S) MS63-65 16 (3) 1945-PDS Unc War Nickels Unc 17 (2) 1950-D Unc Jefferson Nickels MS65 18 (23) Proof Jefferson Nickels (1960-1964) (in mint cello) Proof 19 (9) Proof Silver Roosevelt Dimes (1956-1964 1 each) Proof 20 (15) Proof Clad Roosevelt Dimes (1968-1990) Proof 21 (12) Proof Washington Quarters (1959-1990) Proof 22 (6) Proof Kennedy Half Dollars (1964, 68S, 69S, 70S, 88S, 90S) Proof 23 (6) Susan B. -

Liberty Coin Service Collecting Kennedy Half Dollars

Liberty Coin Service Collecting Kennedy Half Dollars by Thomas Coulson November 22, 1963 is one of the handful of days in United States History that will always be remembered clearly by those who lived it. The assas- sination of President John F. Kennedy in Dallas was devastating to the United States populace. Before his funeral was over, there was already discussion of a lasting tribute for such a beloved president. In only thir- ty eight days, the Kennedy Half Dollar was designed and approved into law. Production began in January, 1964 and coins reached commerce in late March, 1964. It was a remarkably fast time for a coin to go from concept to circulation. 1964 Kennedy Half Dollar Because of President Kennedy’s tragic death and great popularity, the coins were aggressively hoarded by the public. Some wanted a memento of the slain president. Others saw opportunity in future demand for the coin. Many went to Europe, par- ticularly Germany, where Kennedy’s visit a year earlier made him very popular. Further exacerbating the supply of new halves was the rising price of silver, which drew virtually all 90% silver coins out of circula- tion quickly. Few Kennedy Halves made it into circulation for long. When one was seen in circulation, it was considered an oddity to be saved; so even more were withdrawn in this manner. As few kennedy half dollars were seen, the denomination faded from public consiousness and mintages gradually declined from year to year. By 2001, there was ostensibly no demand for Half Dollars in commerce. -

Kingston (Ontario, Canada) Pickers World SELLER MANAGED Coins Online Auction - Princess St

09/25/21 10:14:21 Kingston (Ontario, Canada) Pickers World SELLER MANAGED Coins Online Auction - Princess St Auction Opens: Tue, May 17 5:00pm ET Auction Closes: Tue, May 24 8:00pm ET Lot Title Lot Title 0001 1954 Canada Five Dollar Bill 0033 1967 Canadian Silver Dollar 0002 1954 Canadian Twenty Dollar Bill 0034 1864-1964 Canada PEI Silver Dollar 0003 1954 Canadian Two Dollar Bill 0035 1982 Jamaica Dollar Coin 0004 1911 Canadian Five Cent Coin 0036 1867-1967 Canada Confederation Coin 0005 1979 Canadian Twenty Dollar Bill Medallion 0006 1964 JFK Silver Half Dollar Coin 0037 1979 Grande Cache Coal Mine Coin 0007 1956 Canadian Half Dollar Silver Coin 0038 1964 USA Silver Kennedy Half Dollar Coin 0008 1952 Canadian Half Dollar Silver Coin 0039 1975 Canadian Dollar Coins 0009 1945 Canadian Half Dollar Silver Coin 0040 1971 USA Liberty Dollar Coin 0010 1944 Canadian Half Dollar Silver Coin 0041 1937 Cornwall Canada Coronation Coin Medallion 0011 1965 Canadian Silver Half Dollar Coin 0042 1929 Canadian Penny Cent Coin 0012 1963 Canadian Silver Half Dollar Coin 0043 1930 Canadian Silver Dime 0013 1966 Canadian Silver Half Dollar Coin 0044 Canadian Half Dollar Coin Lot Of 5 0014 1959 Canadian Silver Half Dollar Coin 0045 1974 USA Kennedy Half Dollar Coin 0015 1967 Canadian Silver Half Dollar Coin 0046 1972 USA Kennedy Half Dollar Coin 0016 1964 Canadian Silver Half Dollar Coin 0047 1870-1970 Canada Manitoba Dollar Coin 0017 1951 Canadian Silver Half Dollar Coin 0048 1918 Canadian One Cent Large Penny Coin 0018 1960 Canadian Silver Half Dollar -

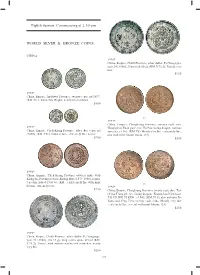

Eighth Session, Commencing at 2.30 Pm WORLD SILVER & BRONZE

Eighth Session, Commencing at 2.30 pm WORLD SILVER & BRONZE COINS CHINA 1996* China, Empire, Chihli Province, silver dollar, Pei Yang type, year 34 (1908), 39mm (26.60 g), (KM.Y.73.3). Toned, very fi ne. $150 1992* China, Empire, An-Hwei Province, twenty cents, nd.1897, (KM.43.1, Kann 50). Bright, nearly uncirculated. $500 part 1997* China, Empire, Chingkiang Province, twenty cash, obv. 1993* 'Kuang-hsu Yuan pao', rev. Hu Poo facing dragon, various China, Empire, Cheh-Kiang Province, silver fi ve cents, nd varieties, c.1903, (KM.Y5). Mostly very fi ne - extremely fi ne, (1898), (KM.Y51). Golden tone, extremely fi ne, scarce. one with mint bloom traces. (15) $200 $200 1994* China, Empire, Cheh-Kiang Province obverse mule with Kiang See Province reverse, Kuang Hsu, (1875-1908), copper ten cash, issued 1903-6), (KM.-). Extremely fi ne with mint part bloom, extremely rare. 1998* $250 China, Empire, Chingkiang Province, twenty cash, obv. 'Tai- ch'ing T'ung pi', rev. facing dragon, 'Kuang-hsu Nien-tsao' TAI CHING TI KUO, c.1905, (KM.Y11), also includes Pei Yang and Feng Tien, twenty cash coins. Mostly very fi ne - extremely fi ne, several with mint bloom. (25) $250 1995* China, Empire, Chihli Province, silver dollar, Pei Yang type, year 34 (1908), (26.44 g), long centre spine of tail (KM. Y.73.2). Toned, with surface marks and scratches, nearly very fi ne. $200 241 1999* 2004* China, Empire, Chingkiang, central mint, Tientsin, under China, Empire, Kirin Province, silver dollar, 1906, 38.5mm, Hsuen Tung (1908-1911), issued in 3rd year (1911), silver (26.37 g), (KM.Y183, Kann 537). -

The Kennedy Half Dollar Collector Checklist Compliments of Littleton Coin Company, Inc

The Kennedy Half Dollar Collector Checklist Compliments of Littleton Coin Company, Inc. How to Use This Checklist: The most popular way to collect Kennedy half dollars is to assemble all the different dates and mint marks of the series. This complimentary checklist lets you keep track of your growing collection. As you acquire various dates and mint marks, simply cross them off the list. When you complete your collection, return this checklist to us and you’ll receive a personalized Certificate of Achievement. With the certificate, we acknowledge your dedication to the numismatic hobby, and we extend our appreciation for having the opportunity to serve you. Kennedy Half Dollars Mint mark location Mint mark location Issued 1964-Date 1968 to date 1964-1967 1974-S Proof 1977-S Proof 1981-D 1985-S Proof 1990-P Bicentennial 1978 1981-S Proof 1986-P 1990-D Coinage 1978-D 1982-P 1986-D 1990-S Proof 1976 CN 1978-S Proof 1982-D 1986-S Proof 1991-P 1976-D CN 1979 1982-S Proof 1987-P 1991-D 1976-S CN Proof 1979-D 1983-P 1987-D 1991-S Proof 1976-S Silver Clad 1979-S Proof, 1983-D 1987-S Proof 1992-P Filled S Silver 1976-S Silver Clad 1983-S Proof 1988-P 1992-D 1979-S Proof, 1964 Copper-Nickel Proof 1984-P 1988-D 1992-S Proof Clear S 1964-D Clad 1984-D 1988-S Proof 1992-S Silver Proof 1964 Proof 1971 1984-S Proof 1989-P 1993-P Silver Clad 1971-D 1985-P 1989-D 1993-D 1965 1971-S Proof 1985-D 1989-S Proof 1993-S Proof 1966 1972 1993-S Silver Proof 1967 1972-D 1994-P 1968-D 1972-S Proof 1994-D 1968-S Proof 1973 1994-S Proof 1969-D 1973-D 1994-S Silver -

Date and Mint Mark

Littleton’s Illustrated Guide to Mint Marks on Regular-Issue U.S. Coins Philadelphia: Mint mark “P” – coinage Carson City: Mint mark “CC” – coinage New Orleans: Mint mark “O” – coinage years 1793 to date. Since this was the first years 1870-1893. Named after the famous years 1838-1861, 1879 to 1909. U.S. Mint and has always been the main frontiersman Kit Carson, this intriguing Nicknamed the “Crescent City” for its facility, most coins from historic Philadelphia have no capital city of Nevada was chosen as a mint location location stretching around a bend in the Mississippi mint mark. Exceptions are the Wartime nickels of because of its nearness to such rich silver mines as the River, fascinating New Orleans was the site of a branch 1942-45 (shown), Anthony dollars of 1979-81, and Comstock Lode of Virginia City, Nevada. mint which handled bullion ore from southern mines. all other Philadelphia coins after 1979 except the cent. Note: “C” mint mark gold coins were struck from After closure, the building lay vacant until converted to 1838-61 at Charlotte, North Carolina. a museum and art center. Denver: Mint mark “D” – coinage San Francisco: Mint mark “S” – About Mint Mark Punches: Until the 1990s, dies for branch mints were hand-punched with the mint mark, and the years 1906 to date. Establishment of a coinage years 1854 to 1955, 1968 to size and location of the mint mark varied depending on where Denver Mint was the natural result of major date. The mint facility in this romantic and how deeply the punch was impressed. -

Young Numismatists AUCTION CATALOG SEPTEMBER 14, 2019 | 10AM MST ONLINE AUCTION at MONEY.ORG

young numismatists AUCTION CATALOG SEPTEMBER 14, 2019 | 10AM MST ONLINE AUCTION AT MONEY.ORG 1 YOUNG NUMISMATIST ONLINE AUCTION SATURDAY SEPTEMBER 14, 2019 10:00 AM, MOUNTAIN DAYLIGHT TIME AUCTION LOT VIEWING AVAILABLE ONLINE AT MONEY.ORG Cataloguer: Sam Gelberd THE AMERICAN NUMISMATIC ASSOCIATION WANTS YOU to experience all the fun and knowledge that coin collecting can bring. In addition to the annual ANA Young Numismatist (YN) Online Auction, THE FOLLOWING PROGRAMS ARE OFFERED TO YOUNG COLLECTORS: ANA SUMMER SEMINAR brings collectors of all ages and experience together each summer to learn about numismatics and share their knowledge. Seminars are in Colorado Springs on the Colorado College campus, adjacent to ANA Headquarters. A course catalog will be available in early 2020. Students take classes of their choice, attend field trips to explore the local area and participate in special activities while living with fellow YN’s, interns, and mentors. Full and partial scholarships (tuition, room & board, airfare) are available to qualified ANA-member Young Numismatists. Applications are available at money.org, or by contacting the ANA Education Department at 719-482-9865. ANA YN TREASURE TRIVIA GAME is another exciting event held at the ANA National Money Show® and the World’s Fair of Money®. Participants follow a treasure map of the convention and bourse floors to find answers to numismatic trivia questions and collect treasures along the ywa . YOUNG COLLECTORS CORNER is a program held at ANA shows for children ages 5-17 that explains the origins and history of money in all of its forms, as well as the foundations of numismatics.