In the Court of Chancery of the State of Delaware

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report and Accounts 2019

IMPERIAL BRANDS PLC BRANDS IMPERIAL ANNUAL REPORT AND ACCOUNTS 2019 ACCOUNTS AND REPORT ANNUAL ANNUAL REPORT AND ACCOUNTS 2019 OUR PURPOSE WE CAN I OWN Our purpose is to create something Everything See it, seize it, is possible, make it happen better for the world’s smokers with together we win our portfolio of high quality next generation and tobacco products. In doing so we are transforming WE SURPRISE I AM our business and strengthening New thinking, My contribution new actions, counts, think free, our sustainability and value creation. exceed what’s speak free, act possible with integrity OUR VALUES Our values express who we are and WE ENJOY I ENGAGE capture the behaviours we expect Thrive on Listen, challenge, share, make from everyone who works for us. make it fun connections The following table constitutes our Non-Financial Information Statement in compliance with Sections 414CA and 414CB of the Companies Act 2006. The information listed is incorporated by cross-reference. Additional Non-Financial Information is also available on our website www.imperialbrands.com. Policies and standards which Information necessary to understand our business Page Reporting requirement govern our approach1 and its impact, policy due diligence and outcomes reference Environmental matters • Occupational health, safety and Environmental targets 21 environmental policy and framework • Sustainable tobacco programme International management systems 21 Climate and energy 21 Reducing waste 19 Sustainable tobacco supply 20 Supporting wood sustainability -

Current Status of the Reduced Propensity Ignition Cigarette Program in Hawaii

Hawaii State Fire Council Current Status of the Reduced Propensity Ignition Cigarette Program in Hawaii Submitted to The Twenty-Eighth State Legislature Regular Session June 2015 2014 Reduced Ignition Propensity Cigarette Report to the Hawaii State Legislature Table of Contents Executive Summary .…………………………………………………………………….... 4 Purpose ..………………………………………………………………………....................4 Mission of the State Fire Council………………………………………………………......4 Smoking-Material Fire Facts……………………………………………………….............5 Reduced Ignition Propensity Cigarettes (RIPC) Defined……………………………......6 RIPC Regulatory History…………………………………………………………………….7 RIPC Review for Hawaii…………………………………………………………………….9 RIPC Accomplishments in Hawaii (January 1 to June 30, 2014)……………………..10 RIPC Future Considerations……………………………………………………………....14 Conclusion………………………………………………………………………….............15 Bibliography…………………………………………………………………………………17 Appendices Appendix A: All Cigarette Fires (State of Hawaii) with Property and Contents Loss Related to Cigarettes 2003 to 2013………………………………………………………18 Appendix B: Building Fires Caused by Cigarettes (State of Hawaii) with Property and Contents Loss 2003 to 2013………………………………………………………………19 Appendix C: Cigarette Related Building Fires 2003 to 2013…………………………..20 Appendix D: Injuries/Fatalities Due To Cigarette Fire 2003 to 2013 ………………....21 Appendix E: HRS 132C……………………………………………………………...........22 Appendix F: Estimated RIPC Budget 2014-2016………………………………...........32 Appendix G: List of RIPC Brands Being Sold in Hawaii………………………………..33 2 2014 -

150526Reynoldsjbstatement.Pdf

Dissenting Statement of Commissioner Julie Brill In the Matter of Reynolds American, Inc. and Lorillard Inc. File No. 141-0168 May 26, 2015 A majority of the Commission has voted to accept a consent to resolve competitive concerns stemming from Reynolds American, Inc.’s $27.4 billion acquisition of Lorillard Tobacco Company, a transaction combining the second and third largest cigarette manufacturers in the United States. Under the terms of the consent, Reynolds will divest some of its weaker non-growth brands – Winston, Kool, and Salem – as well as Lorillard’s brand Maverick to Imperial Tobacco Group plc, a British firm that currently operates as Commonwealth here in the United States.1 The Commission will allow Reynolds to retain its sought-after growth brands, Camel and Pall Mall, as well as Lorillard’s flagship brand Newport. I respectfully dissent because I am not convinced that the remedy accepted by the Commission fully resolves the competitive concerns arising from this transaction. By accepting the parties’ proposed divestitures and allowing the merger to proceed, the Commission is betting on Imperial’s ability and incentive to compete vigorously with a set of weak and declining brands. For the reasons explained below, Imperial’s ability to do so is at best uncertain. I thus have reason to believe that Reynolds’ acquisition of Lorillard, even after the divestitures to Imperial, is likely to substantially lessen competition in the U.S. cigarette market. As a result of the Commission’s failure to take meaningful action against this merger, the remaining two major cigarette manufacturers – Altria/Philip Morris and Reynolds – will likely be able to impose higher cigarette prices on consumers. -

Directory for Cigarettes and Roll-Your-Own Tobacco

DEPARTMENT OF THE ATTORNEY GENERAL STATE OF HAWAI‘I DIRECTORY FOR CIGARETTES AND ROLL-YOUR-OWN TOBACCO of (Available at: http://ag.hawaii.gov/cjd/tobacco-enforcement-unit/) Certified Tobacco Product Manufacturers Their Brands and Brand Families DEPARTMENT OF THE ATTORNEY GENERAL TOBACCO ENFORCEMENT UNIT 425 QUEEN STREET HONOLULU, HAWAI‘I 96813 (808) 586-1203 INDEX I. Directory: Cigarettes and Roll-Your-Own Tobacco Page 1. INTRODUCTION 3 2. DEFINITIONS 3 3. NOTICES 5 II. Update Summary For June 1, 2018 Posting * III. Alphabetical Brand List IV. Compliant Participating Manufacturers List V. Compliant Non-Participating Manufacturers List Posted: June 1, 2018 (updated most recent 9/5/2018) 2 1. INTRODUCTION Pursuant to Haw. Rev. Stat. §245-22.5(a), beginning December 1, 2003, it shall be unlawful for an entity (1) to affix a stamp to a package or other container of cigarettes belonging to a tobacco product manufacturer or brand family not included in this directory, or (2) to import, sell, offer, keep, store, acquire, transport, distribute, receive, or possess for sale or distribution cigarettes1 belonging to a tobacco product manufacturer or brand family not included in this directory. Pursuant to §245-22.5(b), any entity that knowingly violates subsection (a) shall be guilty of a class C felony. Pursuant to Haw. Rev. Stat. §§245-40 and 245-41, any cigarettes unlawfully possessed, kept, stored, acquired, transported, or sold in violation of Haw. Rev. Stat. §245-22.5 may be ordered forfeited pursuant to Haw. Rev. Stat., Chapter 712A. In addition, the attorney general may apply for a temporary or permanent injunction restraining any person from violating or continuing to violate Haw. -

PGY1 Community-Based Pharmacy Residency Program Chicago, Illinois

About Albertsons Companies Application Requirements • Albertsons Companies is one of the largest food and drug • Residency program application retailers in the United States, with both a strong local • Personal statement PGY1 Community-Based presence and national scale. We operate stores across 35 • CV or resume states and the District of Columbia under 20 well-known Pharmacy Residency Program banners including Albertsons, Safeway, Vons, Jewel- • Three electronic references Chicago, Illinois Osco, Shaw’s, Haggen, Acme, Tom Thumb, Randalls, • Official transcripts United Supermarkets, Pavilions, Star Market and Carrs. • Electronic application submission via Our vision is to create patients for life as their most trusted https://portal.phorcas.org/ health and wellness provider, and our mission is to provide a personalized wellness experience with every patient interaction. National Matching Service Code • Living up to our mission and vision, we have continuously 142515 advanced pharmacist-provided patient care and expanded the scope of pharmacy practice. Albertsons Companies has received numerous industry recognitions and awards, Contact Information including the 2018 Innovator of the Year from Drug Store Chandni Clough, PharmD News, Top Large Chain Provider of Medication Therapy Management Services by OutcomesMTM for the past 3 Residency Program Director years, and the 2018 Corporate Immunization Champion [email protected] from APhA. (630) 948-6735 • Albertsons Companies is pleased to offer residency positions by Baltimore, Boise, Chicago, Denver, Houston, Philadelphia, Phoenix, Portland, and San Francisco. To build upon the Doctor of Pharmacy (PharmD) education and outcomes to develop www.albertsonscompanies.com/careers/pharmacy-residency-program.html community‐based pharmacist practitioners with diverse patient care, leadership, and education skills who are eligible to pursue advanced training opportunities including postgraduate year two (PGY2) residencies and professional certifications. -

Current Directory

Current Directory Manufacturer Manufacturer Brand Brand Brand Style Descriptors Brand Style Descriptors Cheyenne International, LLC (NPM) Grand River Enterprises Six Nations, Ltd. (NPM) Aura Seneca Menthol Glen Kings Box Blue 100s Box Radiant Gold Kings Box Blue 100s Soft Pack Robust Red Kings Box Blue 72s Slide Box Sky Blue Kings Box Blue King Size Box Blue King Size Soft Pack Cheyenne Chill King Size Box Gold 100 Box Extra Smooth Menthol 100s Box Gold King Box Extra Smooth Menthol 100s Soft Pack Menthol 100 Box Full Flavor 100s Box Menthol King Box Full Flavor 100s Soft Pack Menthol Silver 100 Box Full Flavor 120s Box Menthol Silver King Box Full Flavor 72s Slide Box Non-filter King Box Full Flavor King Size Box Red 100 Box Full Flavor King Size Soft Pack Red King Box Medium 100s Box Silver 100 Box Medium King Size Box Silver King Box Menthol 100s Box Decade Menthol 100s Soft Pack Gold 100 Box Menthol 120s Box Gold King Box Menthol 72s Slide Box Menthol 100 Box Menthol King Size Box Menthol King Box Menthol King Size Soft Pack Menthol Silver 100 Box Nonfilter King Size Box Menthol Silver King Box Silver 100s Box Red 100 Box Silver 100s Soft Pack Red King Box Silver King Size Box Silver 100 Box Silver King Size Soft Pack Silver King Box Smooth 120s Box Smooth Menthol 100s Box Smooth Menthol 100s Soft Pack Grand River Enterprises Six Nations, Ltd. (NPM) Smooth Menthol 120s Box Couture Smooth Menthol King Size Box Smooth Menthol King Size Soft Pack Slims 100s Amethyst Box Ultra 120s Box Slims 100s Aquamarine Box Slims 100s Diamond Box -

Permit Num Retail Name Address City RS-0055-21 Albertsons 0131 1410

Cancell Sales Last Name Sales First ZIP County In Out Tent Stand Wholesaler 1 Wholesaler 2 Wholesaler 3 Wholesaler 4 Wholesaler 5 Sales Location ed Permit Retail Name Address City Num Name Fire Dept RS-0055-21 Albertsons 0131 Shriner Sarah 1410 W Park Plaza Ontario 97914 Malheur TRUE FALSE FALSE FALSE American ONTARIO F&R Promotional Events NW RS-0331-21 Albertsons 0505 Onchi Chad 5415 SW Beaverton-Hillsdale Hwy Portland 97221 Multnomah TRUE FALSE FALSE FALSE American PORTLAND F&R Promotional Events NW RS-0340-21 Albertsons 0513 Walline Jenni 4740 Royal Ave Eugene 97402 Lane TRUE FALSE FALSE FALSE American EUGENE Promotional Events SPRINGFIELD NW FIRE RS-0058-21 Albertsons 0515 Patterson Michelle 3013 NW Stewart Parkway Roseburg 97471 Douglas TRUE FALSE FALSE FALSE American ROSEBURG FD Promotional Events NW RS-0562-21 Albertsons 0536 Maglnigal Danielle 25691 SE Stark St Troutdale 97060 Multnomah TRUE FALSE FALSE FALSE American GRESHAM FIRE Promotional Events & EMERG SRVCS NW RS-0563-21 Albertsons 0564 Dehann Jannine 451 NE 181st St Portland 97230 Multnomah TRUE FALSE FALSE FALSE American GRESHAM FIRE Promotional Events & EMERG SRVCS NW RS-0056-21 Albertsons 0571 Rainsier Mark 19007 S Beavercreek Rd Oregon City 97045 Clackamas TRUE FALSE FALSE FALSE American CLACKAMAS CO Promotional Events FIRE DIST #1 NW RS-0339-21 Albertsons 0572 Souliyalaovong Ruby 311 Coburg Rd Eugene 97401 Lane TRUE FALSE FALSE FALSE American EUGENE Promotional Events SPRINGFIELD NW FIRE RS-0338-21 Albertsons 0574 Vails Tracey 5755 Main St Springfield 97478 Lane TRUE -

MERGER ANTITRUST LAW Albertsons/Safeway Case Study

MERGER ANTITRUST LAW Albertsons/Safeway Case Study Fall 2020 Georgetown University Law Center Professor Dale Collins ALBERTSONS/SAFEWAY CASE STUDY Table of Contents The deal Safeway Inc. and AB Albertsons LLC, Press Release, Safeway and Albertsons Announce Definitive Merger Agreement (Mar. 6, 2014) .............. 4 The FTC settlement Fed. Trade Comm’n, FTC Requires Albertsons and Safeway to Sell 168 Stores as a Condition of Merger (Jan. 27, 2015) .................................... 11 Complaint, In re Cerberus Institutional Partners V, L.P., No. C-4504 (F.T.C. filed Jan. 27, 2015) (challenging Albertsons/Safeway) .................... 13 Agreement Containing Consent Order (Jan. 27, 2015) ................................. 24 Decision and Order (Jan. 27, 2015) (redacted public version) ...................... 32 Order To Maintain Assets (Jan. 27, 2015) (redacted public version) ............ 49 Analysis of Agreement Containing Consent Orders To Aid Public Comment (Nov. 15, 2012) ........................................................... 56 The Washington state settlement Complaint, Washington v. Cerberus Institutional Partners V, L.P., No. 2:15-cv-00147 (W.D. Wash. filed Jan. 30, 2015) ................................... 69 Agreed Motion for Endorsement of Consent Decree (Jan. 30, 2015) ........... 81 [Proposed] Consent Decree (Jan. 30, 2015) ............................................ 84 Exhibit A. FTC Order to Maintain Assets (omitted) ............................. 100 Exhibit B. FTC Order and Decision (omitted) ..................................... -

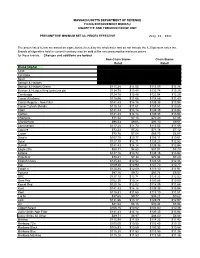

Cigarette Minimum Retail Price List

MASSACHUSETTS DEPARTMENT OF REVENUE FILING ENFORCEMENT BUREAU CIGARETTE AND TOBACCO EXCISE UNIT PRESUMPTIVE MINIMUM RETAIL PRICES EFFECTIVE July 26, 2021 The prices listed below are based on cigarettes delivered by the wholesaler and do not include the 6.25 percent sales tax. Brands of cigarettes held in current inventory may be sold at the new presumptive minimum prices for those brands. Changes and additions are bolded. Non-Chain Stores Chain Stores Retail Retail Brand (Alpha) Carton Pack Carton Pack 1839 $86.64 $8.66 $85.38 $8.54 1st Class $71.49 $7.15 $70.44 $7.04 Basic $122.21 $12.22 $120.41 $12.04 Benson & Hedges $136.55 $13.66 $134.54 $13.45 Benson & Hedges Green $115.28 $11.53 $113.59 $11.36 Benson & Hedges King (princess pk) $134.75 $13.48 $132.78 $13.28 Cambridge $124.78 $12.48 $122.94 $12.29 Camel All others $116.56 $11.66 $114.85 $11.49 Camel Regular - Non Filter $141.43 $14.14 $139.35 $13.94 Camel Turkish Blends $110.14 $11.01 $108.51 $10.85 Capri $141.43 $14.14 $139.35 $13.94 Carlton $141.43 $14.14 $139.35 $13.94 Checkers $71.54 $7.15 $70.49 $7.05 Chesterfield $96.53 $9.65 $95.10 $9.51 Commander $117.28 $11.73 $115.55 $11.56 Couture $72.23 $7.22 $71.16 $7.12 Crown $70.76 $7.08 $69.73 $6.97 Dave's $107.70 $10.77 $106.11 $10.61 Doral $127.10 $12.71 $125.23 $12.52 Dunhill $141.43 $14.14 $139.35 $13.94 Eagle 20's $88.31 $8.83 $87.01 $8.70 Eclipse $137.16 $13.72 $135.15 $13.52 Edgefield $73.41 $7.34 $72.34 $7.23 English Ovals $125.44 $12.54 $123.59 $12.36 Eve $109.30 $10.93 $107.70 $10.77 Export A $120.88 $12.09 $119.10 $11.91 -

Directory of Cigarettes Approved for Sale and Importation June 19, 2015

Directory of Cigarettes Approved for Sale and Importation June 19, 2015 The following cigarette manufacturers and their associated brands have been determined to be in compliance with Alaska Statutes 45.53.020 (see MSA Compliant Tobacco Manufacturers) and 18.74.010 (see Directory of Fire Safe Certified Brand Styles). Please be advised that cigarettes (to include roll-your-own) manufactured by companies not listed below may not be sold in Alaska. Cigarettes found in Alaska that are not on this list are contraband and subject to seizure and destruction. Violations of AS 45.53.020 may also be punished by revocation of a license issued under AS 43.50.010, 43.50.035, or 43.50.320 and imposition of civil and criminal penalties. Manufacturer type provides that the company is both a participating manufacturer (PM) and signatory to the Tobacco Master Settlement Agreement and all amendments to that agreement or a non-participating manufacturer (NPM) in full compliance with Alaska Statute 45.43. Lorillard Tobacco Company (Lorillard) merged with R.J. Reynolds Tobacco Company (RJR) as of June 12, 2015. As a result of the merger, the ownership of certain of Lorillard’s and RJR’s brands has changed. Kent, Newport, Old Gold and True, formerly Lorillard brands, are now held by RJR; Maverick was transferred from Lorillard to ITG Brands, LLC (ITG); and Kool, Winston and Salem were transferred from RJR to ITG. Although the transfers were effective as of June 12, 2015, the companies are selling off their product that was already in the distribution chain as of June 12, 2015. -

Manufacturer Brand Style Length (Mm's) Circ

Iowa Approved Fire Standard Compliant Cigarettes -04/01/2021 (SORTED BY BRAND STYLE) Date Length Circ Certified/ Manufacturer Brand Style (mm's) (mm's) Flavor Filter Package Test Date Recertified Premier Manufacturing, Inc. 1839 Blue 100 Box 97.90 24.60 Regular Filter Box 03/30/18 01/11/21 Premier Manufacturing, Inc. 1839 Blue King Box 82.40 24.60 Regular Filter Box 04/03/18 01/11/21 Premier Manufacturing, Inc. 1839 Menthol Blue 100 Box 97.90 24.70 Menthol Filter Box 03/30/18 01/11/21 Premier Manufacturing, Inc. 1839 Menthol Blue King Box 82.90 24.60 Menthol Filter Box 04/04/18 01/11/21 Premier Manufacturing, Inc. 1839 Menthol Green 100 Box 97.30 24.60 Menthol Filter Box 04/02/18 01/11/21 Premier Manufacturing, Inc. 1839 Menthol Green King Box 83.00 24.50 Menthol Filter Box 04/04/18 01/11/21 Premier Manufacturing, Inc. 1839 Red 100 Box 97.80 24.60 Regular Filter Box 03/30/18 01/11/21 Premier Manufacturing, Inc. 1839 Red King Box 82.80 24.70 Regular Filter Box 04/03/18 01/11/21 Premier Manufacturing, Inc. 1839 Silver 100 Box 97.40 24.70 Regular Filter Box 04/03/18 01/11/21 Premier Manufacturing, Inc. 1839 Silver King Box 82.80 24.70 Regular Filter Box 04/04/18 01/11/21 Premier Manufacturing, Inc. 1st Class Blue 100's Box 97.10 24.60 Regular Filter Box 04/05/18 01/11/21 Premier Manufacturing, Inc. 1st Class Blue Kings Box 82.80 24.70 Regular Filter Box 04/05/18 01/11/21 Premier Manufacturing, Inc. -

PI Setup & Steps for Success

PI Setup & Steps for Success Below is a high-level checklist to assist you with Product Introduction (PI) setup and new item submission. Detailed information is provided in the free Albertsons PI Supplier Training Modules under ‘Education’ on the Albertsons Companies Landing Site at: www.1worldsync.com/albertsons □ Must have a 6-digit Vendor Number and 3-digit Sub Account/Outlet setup in the Albertsons Companies system o Unsure? Contact your Albertsons Companies Sales Merchandising Team o The Sales Merchandising Team must approve supplier setup. More details located at: http://suppliers.safeway.com/pages/BecomeASupplier.htm □ Locate or create your Global Location Number (GLN) (unique identifier) o Suppliers: . Unsure? Contact 1WorldSync at 866-280-4013 or [email protected] . Need to setup a GLN? Contact GS1 at 937-435-3870 or [email protected] . Exclusion applies for Alcohol and Own Brands/Private Label o Brokers: . Ask your supplier to provide the GLN □ PI access o Next step depends on your company’s current engagement . GDSN: 1WorldSync customer (GDSN = Global Data Synchronization Network) . GDSN: Other data pool . Non-GDSN: Existing Account . Non-GDSN: New Account . Broker: Brand owner must give the broker access to PI under their GLN □ If your company already has access to PI o Ask your company administrator to grant you access to PI □ If you don’t have access to PI o GDSN/1WorldSync Customer: contact 1WorldSync at 866-280-4013 or [email protected] o Alcohol entities: Contact 1WorldSync Business Development at 866-280-4013 or [email protected] o Own Brands/Private Label: Contact your Albertsons Companies Own Brands team o Own Brands/Supply-Expense: Contact 1WorldSync Business Development at 866-280-4013 or [email protected] o GDSN/Other Data Pool or Non-GDSN (Fee Based System) .