Letters to Shareholders – First 10 Years Collection 2.82 MB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prospectus for the Listing of $1.5 Billion 4.500% Senior Notes

Prospectus dated August 14, 2015 FIAT CHRYSLER AUTOMOBILES N.V. (a public limited liability company incorporated under the laws of the Netherlands No. 60372958) $1,500,000,000 4.500% SENIOR NOTES DUE 2020 $1,500,000,000 5.250% SENIOR NOTES DUE 2023 _________________________________________________________________ On April 14, 2015, Fiat Chrysler Automobiles N.V. (the “Issuer”), a public limited liability company (naamloze vennootschap) incorporated and operating under the laws of the Netherlands, issued its $1,500,000,000 4.500% Senior Notes due 2020 (the “Initial 2020 Notes”) and its $1,500,000,000 5.250% Senior Notes due 2023 (the “Initial 2023 Notes” and collectively, the “Initial Notes”). The Initial Notes have not been registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”), or any state securities laws. The Initial Notes may not be offered or sold to U.S. persons, except to persons reasonably believed to be qualified institutional buyers in reliance on the exemption from registration provided by Rule 144A under the Securities Act and to certain persons in offshore transactions in reliance on Regulation S under the Securities Act. You are hereby notified that sellers of the Notes may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. For a description of certain restrictions on transfers of the Notes see “Transfer Restrictions” in the Original Prospectus (as such term is defined below). On July 28, 2015 the Issuer issued $1,460,345,000 aggregate principal amount of its 4.500% Senior Notes due 2020 registered under the Securities Act (the “2020 Notes”) and $1,467,939,000 aggregate principal amount of its 5.250% Senior Notes due 2023 registered under the Securities Act (the “2023 Notes” and together with the 2020 Notes, the “New Notes”). -

30 06 2019 Annual Financial Report

30 06 2019 ANNUAL FINANCIAL REPORT ANNUAL FINANCIAL REPORT 30 06 2019 REGISTERED OFFICE Via Druento 175, 10151 Turin Contact Center 899.999.897 Fax +39 011 51 19 214 SHARE CAPITAL FULLY PAID € 8,182,133.28 REGISTERED IN THE COMPANIES REGISTER Under no. 00470470014 - REA no. 394963 CONTENTS REPORT ON OPERATIONS 6 Board of Directors, Board of Statutory Auditors and Independent Auditors 9 Company Profile 10 Corporate Governance Report and Remuneration Report 17 Main risks and uncertainties to which Juventus is exposed 18 Significant events in the 2018/2019 financial year 22 Review of results for the 2018/2019 financial year 25 Significant events after 30 June 2019 30 Business outlook 32 Human resources and organisation 33 Responsible and sustainable approach: sustainability report 35 Other information 36 Proposal to approve the financial statements and cover losses for the year 37 FINANCIAL STATEMENTS AT 30 JUNE 2019 38 Statement of financial position 40 Income statement 43 Statement of comprehensive income 43 Statement of changes in shareholders’ equity 44 Statement of cash flows 45 Notes to the financial statements 48 ATTESTATION PURSUANT TO ARTICLE 154-BIS OF LEGISLATIVE DECREE 58/98 103 BOARD OF STATUTORY AUDITORS’ REPORT 106 INDEPENDENT AUDITORS’ REPORT 118 ANNUAL FINANCIAL REPORT AT 30 06 19 5 REPORT ON OPERATIONS BOARD OF DIRECTORS, BOARD OF STATUTORY AUDITORS AND INDEPENDENT AUDITORS BOARD OF DIRECTORS CHAIRMAN Andrea Agnelli VICE CHAIRMAN Pavel Nedved NON INDEPENDENT DIRECTORS Maurizio Arrivabene Francesco Roncaglio Enrico Vellano INDEPENDENT DIRECTORS Paolo Garimberti Assia Grazioli Venier Caitlin Mary Hughes Daniela Marilungo REMUNERATION AND APPOINTMENTS COMMITTEE Paolo Garimberti (Chairman), Assia Grazioli Venier e Caitlin Mary Hughes CONTROL AND RISK COMMITTEE Daniela Marilungo (Chairman), Paolo Garimberti e Caitlin Mary Hughes BOARD OF STATUTORY AUDITORS CHAIRMAN Paolo Piccatti AUDITORS Silvia Lirici Nicoletta Paracchini DEPUTY AUDITORS Roberto Petrignani Lorenzo Jona Celesia INDEPENDENT AUDITORS EY S.p.A. -

Enzo Ferrari Ende Der 1930Er Jahre Selbstständig Machen Wollte, Suchte Er Einen Kreditgeber

Interview mit Piero Ferrari ______________________ Als sich Enzo Ferrari Ende der 1930er Jahre selbstständig machen wollte, suchte er einen Kreditgeber. Er fand ihn im italienischen Reifenhersteller PIRELLI. Piero Pirelli, um genau zu sein. Aus Dankbarkeit für diesen 15 Milliarden Lire-Kredit, der das solide Fundament für die Entwicklung, Konstruktion und Fertigung des ersten 12-Zylinder-Ferrari-Motors unter Ingenieur Colombo und die Zukunft des Unternehmens FERRARI sein sollte, gab Enzo Ferrari wohl seinem zweitgeborenen Sohn den Namen Piero. Zweitgeborener Sohn deshalb, weil der Erstgeborene namens Alfredino - abgekürzt Dino - trotz engagierter Bemühungen seiner Mutter Laura und seines die Krankheit akribisch schriftlich dokumentierenden Vaters Enzo im Jahre 1956 an Multipler Sklerose verstarb. Beide Söhne zeigten sich dem Erbe ihres Vaters würdig. Beide waren und sind begnadete Techniker und Ingenieure, die durch ihre Konstruktion von Motoren dem Unternehmen Ferrari, Piero aber auch für das mit 42.000 verkauften Motorrädern der italienischen Marke DUCATI im Jahre 2010, dem bisher erfolgreichsten Jahr in der Firmengeschichte, für Anerkennung, mehr noch: für Furore gesorgt haben. Der Markenname DINO, für die in den 1960er Jahren gebauten Sportwagen mit dem von Dino Ferrari gezeichneten 6-Zylinder-Motoren in hoher Mindest-Stückzahl für die rennsportliche Registrierung als Formel 2-Motor, gilt als zuverlässiges und erfolgreiches Bindeglied für die seit 1969 praktizierte Erfolgsehe mit dem Unternehmen FIAT des Avocato Gianni Agnelli und seiner Ehefrau, der Marquesa Carraciolo, in Turin-Italien. Hinter vorgehaltener Hand geben Mitarbeiter von Ferrari sogar preis, Piero sei nicht nur für die Konstruktion und den Einsatz des überaus erfolgreichen Ferrari-Sportwagens 333 verantwortlich gewesen, sondern habe auch die technische Zuständigkeit in Sachen Weltmeister-Motoren von Michael Schumacher in der Formel 1 der Jahre 2000 bis 2004 zu verantworten gehabt. -

The Canadian Watchman for 1932

In This Issue This T‘%entieth Century Nlaratho The Tragedy of Geneva The Adding Machine Fails Some Simple Ailments and what to Do October Oshawa, Ontario 25C • The BIBLE I and the 1 DEPRESSION By Robert E. Speer When the days are dark, men need its light. A When the times are hard, men need its comfort. • When the outlook is discouraging, men needs its confidence. When despair is abroad, men need its word of hope. There are luxuries that may well be spared. There are even necessities that can be curtailed. But the Bible, indispensable at all times, is still more indispensable in times like these today. The Bible is not a book of political maxims or of economic theories. It is not a book of maxims or theories at all. It is a book of living principles. Its spirit is the spirit of brotherliness and goodwill. It is a summons to helpful- ness: "Bear ye one another's burdens." It is a summons also to self-respecting independence: "Let every man bear his own burden." It teaches charity, but also justice. It calls us to the giving and serving which the strong owe to the weak, and those who have to those who lack; but it also strikes straight and clear at the moral defects in individuals which are responsible for a large part of the poverty and suffering of the world; and also at the moral and economic defects in society, in business relations, and in the distribution of the common • resources of the world, which are responsible for the remaining part. -

Ivecobus Range Handbook.Pdf

CREALIS URBANWAY CROSSWAY EVADYS 02 A FULL RANGE OF VEHICLES FOR ALL THE NEEDS OF A MOVING WORLD A whole new world of innovation, performance and safety. Where technological excellence always travels with a true care for people and the environment. In two words, IVECO BUS. CONTENTS OUR HISTORY 4 OUR VALUES 8 SUSTAINABILITY 10 TECHNOLOGY 11 MAGELYS DAILY TOTAL COST OF OWNERSHIP 12 HIGH VALUE 13 PLANTS 14 CREALIS 16 URBANWAY 20 CROSSWAY 28 EVADYS 44 MAGELYS 50 DAILY 56 IVECO BUS CHASSIS 68 IVECO BUS ALWAYS BY YOUR SIDE 70 03 OUR HISTORY ISOBLOC. Presented in 1938 at Salon de Paris, it was the fi rst modern European coach, featuring a self-supporting structure and rear engine. Pictured below the 1947 model. 04 PEOPLE AND VEHICLES THAT TRANSPORTED THE WORLD INTO A NEW ERA GIOVANNI AGNELLI JOSEPH BESSET CONRAD DIETRICH MAGIRUS JOSEF SODOMKA 1866 - 1945 1890 - 1959 1824 - 1895 1865 - 1939 Founder, Fiat Founder, Société Anonyme Founder, Magirus Kommanditist Founder, Sodomka des établissements Besset then Magirus Deutz then Karosa Isobloc, Chausson, Berliet, Saviem, Fiat Veicoli Industriali and Magirus Deutz trademarks and logos are the property of their respective owners. 05 OVER A CENTURY OF EXPERIENCE AND EXPERTISE IVECO BUS is deeply rooted into the history of public transport vehicles, dating back to when the traction motor replaced horse-drawn power. We are proud to carry on the tradition of leadership and the pioneering spirit of famous companies and brands that have shaped the way buses and coaches have to be designed and built: Fiat, OM, Orlandi in Italy, Berliet, Renault, Chausson, Saviem in France, Karosa in the Czech Republic, Magirus-Deutz in Germany and Pegaso in Spain, to name just a few. -

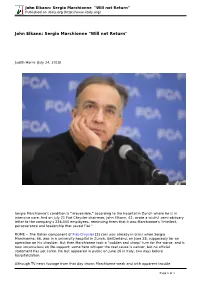

John Elkann: Sergio Marchionne "Will Not Return" Published on Iitaly.Org (

John Elkann: Sergio Marchionne "Will not Return" Published on iItaly.org (http://www.iitaly.org) John Elkann: Sergio Marchionne "Will not Return" Judith Harris (July 24, 2018) Sergio Marchionne's condition is "irreversible," according to the hospital in Zurich where he is in intensive care. And on July 21 Fiat Chrysler chairman, John Elkann, 42, wrote a wistful semi-obituary letter to the company's 236,000 employees, reminding them that it was Marchionne's "intellect, perseverance and leadership that saved Fiat." ROME -- The Italian component of Fiat-Chrysler [2] cars was already in crisis when Sergio Marchionne, 66, was in a university hospital in Zurich, Switzerland, on June 28, supposedly for an operation on his shoulder. But then Marchionne took a "sudden and sharp" turn for the worse, and is now unconscious on life-support; some here whisper the real cause is cancer, but no official statement has yet come. He last appeared in public on June 26 in Italy, two days before hospitalization. Although TV news footage from that day shows Marchionne weak and with apparent trouble Page 1 of 3 John Elkann: Sergio Marchionne "Will not Return" Published on iItaly.org (http://www.iitaly.org) breathing, some Italian press accounts say that the situation "precipitated almost without warning" while others spoke of an "unspecified aggressively infectious disease" only recently diagnosed. Whatever the cause, no improvement will come, for his condition is "irreversible," according to the hospital; and on July 21 Fiat Chrysler chairman, John Elkann, 42, wrote a wistful semi-obituary letter to the company's 236,000 employees, reminding them that it was Marchionne's "intellect, perseverance and leadership that saved Fiat." Marchionne, born in Italy but raised in Canada, took over the then failing 119-year-old Fiat company [3] in 2004. -

Celebrating Contemporary Art and Music from Africa in the Historic City of Évora, Portugal

Celebrating contemporary art and music from Africa in the historic city of Évora, Portugal 25 May - 25 August 2018 Preview: 25 May Évora - Portugal Omar Victor Diop, Aminata, 2013 ● More than 30 contemporary artists, musicians and performers from Africa will gather in the city of Évora in Portugal to celebrate the culture and heritage of the continent ● The contemporary art exhibition African Passions, curated by André Magnin and Philippe Boutté, will be accompanied by a music programme and concerts directed by Alain Weber and Alcides Nascimento ● Democratic Republic of Congo, Ivory Coast, Madagascar, Mali, Mozambique, Senegal, South Africa and Burkina Faso are some of the countries that will be represented in the festival ● Music and dance workshops will be part of the educational programme by the Mozambican music and dance company, the Xindiro Companhia, and by the orchestra of Ballaké Sissoko, master of the kora and Mandingue tradition From the 25 May until 25 August 2018, the Palace of the Dukes of Cadaval will present Evora Africa festival, a multicoloured and extravagant celebration of African heritage through a diverse programme of exhibitions, concerts, performances, conferences, griots and DJs, in the historic city of Évora in Portugal. With the opening on the 25 May coinciding with Africa Day, African traditions will be preserved and imparted while interlinked with the blossoming contemporary African art scene. Bringing art and music from Africa to Portugal, Evora Africa will retrace the roots and historical connections between the continents while celebrating new urban expressions and the influences on Portuguese culture. Over its 3-month duration, Evora Africa aims to strengthen the cultural bonds and exchange between Africa and Europe. -

Universita' Degli Studi Di Padova Caso Juventus F.C

UNIVERSITA’ DEGLI STUDI DI PADOVA DIPARTIMENTO DI SCIENZE ECONOMICHE E AZIENDALI “MARCO FANNO” CORSO DI LAUREA MAGISTRALE IN ECONOMIA INTERNAZIONALE LM-56 Classe delle lauree magistrali in SCIENZE DELL’ECONOMIA Tesi di laurea CASO JUVENTUS F.C.: DALLA CRISI DEL 2006 AL PROCESSO DI INTERNAZIONALIZZAZIONE DEL BRAND JUVENTUS F.C.: FROM THE CRISIS OF 2006 TO THE INTERNATIONALIZATION OF ITS BRAND Relatore: Prof. BELUSSI FIORENZA Laureando: QUEIROLO FRANCESCO Anno Accademico 2018-2019 Il candidato dichiara che il presente lavoro è originale e non è già stato sottoposto, in tutto o in parte, per il conseguimento di un titolo accademico in altre Università italiane o straniere. Il candidato dichiara altresì che tutti i materiali utilizzati durante la preparazione dell‟elaborato sono stati indicati nel testo e nella sezione “Riferimenti bibliografici” e che le eventuali citazioni testuali sono individuabili attraverso l‟esplicito richiamo alla pubblicazione originale. Firma dello studente _________________ INDICE Introduzione ................................................................................................................... pag. 5 1. Il marketing ed il branding nello sport 1.1. Introduzione al marketing ................................................................................ pag. 7 1.2. Il marketing strategico e il marketing mix ....................................................... pag. 10 1.3. Inbound marketing ........................................................................................... pag. 18 1.4. Marketing -

30 06 2019 Annual Financial Report

30 06 2019 ANNUAL FINANCIAL REPORT ANNUAL FINANCIAL REPORT 30 06 2019 WorldReginfo - 5e6c0907-48a0-45c0-a606-45719a985900 WorldReginfo - 5e6c0907-48a0-45c0-a606-45719a985900 REGISTERED OFFICE Via Druento 175, 10151 Turin Contact Center 899.999.897 Fax +39 011 51 19 214 SHARE CAPITAL FULLY PAID € 8,182,133.28 REGISTERED IN THE COMPANIES REGISTER Under no. 00470470014 - REA no. 394963 WorldReginfo - 5e6c0907-48a0-45c0-a606-45719a985900 WorldReginfo - 5e6c0907-48a0-45c0-a606-45719a985900 CONTENTS REPORT ON OPERATIONS 6 Board of Directors, Board of Statutory Auditors and Independent Auditors 9 Company Profile 10 Corporate Governance Report and Remuneration Report 17 Main risks and uncertainties to which Juventus is exposed 18 Significant events in the 2018/2019 financial year 22 Review of results for the 2018/2019 financial year 25 Significant events after 30 June 2019 30 Business outlook 32 Human resources and organisation 33 Responsible and sustainable approach: sustainability report 35 Other information 36 Proposal to approve the financial statements and cover losses for the year 37 FINANCIAL STATEMENTS AT 30 JUNE 2019 38 Statement of financial position 40 Income statement 43 Statement of comprehensive income 43 Statement of changes in shareholders’ equity 44 Statement of cash flows 45 Notes to the financial statements 48 ATTESTATION PURSUANT TO ARTICLE 154-BIS OF LEGISLATIVE DECREE 58/98 103 BOARD OF STATUTORY AUDITORS’ REPORT 106 INDEPENDENT AUDITORS’ REPORT 118 ANNUAL FINANCIAL REPORT AT 30 06 19 5 WorldReginfo - 5e6c0907-48a0-45c0-a606-45719a985900 -

Informazione Regolamentata N. 0149-29-2015

Informazione Data/Ora Ricezione Regolamentata n. 04 Maggio 2015 MTA 0149-29-2015 20:08:05 Societa' : EXOR Identificativo : 57616 Informazione Regolamentata Nome utilizzatore : EXORN01 - Mariani Tipologia : IRCG 01 Data/Ora Ricezione : 04 Maggio 2015 20:08:05 Data/Ora Inizio : 04 Maggio 2015 20:23:05 Diffusione presunta Oggetto : Filing of EXORs lists of candidates for corporate bodies Testo del comunicato Vedi allegato. Turin, May 4, 2015 PRESS RELEASE Filing of EXOR’s lists of candidates for corporate bodies With reference to next Annual General Meeting, which will be held on May 29th, 2015 EXOR hereby reports that the shareholder Giovanni Agnelli e C. S.a.p.az. has filed the following list of candidates for the renewal of the EXOR’s Board of Directors: Annemiek Fentener van Vlissingen (Independent Director) Andrea Agnelli Vittorio Avogadro di Collobiano Ginevra Elkann John Elkann Mina Gerowin (Independent Director) Jae Yong Lee (Independent Director) António Horta-Osório (Independent Director) Sergio Marchionne Alessandro Nasi Lupo Rattazzi Robert Speyer (Independent Director) Michelangelo Volpi (Independent Director) Ruthi Wertheimer (Independent Director) Giuseppina Capaldo (Independent Director) A group of international and domestic investment management companies and institutional investors, which owns 1.02% of EXOR shares, filed the following list: Giovanni Chiura ( Independent Director) The Company welcomes these candidacies, which, if approved by Shareholders, will allow for the election of a Board of Directors -

2018 Annual Report

2018 ANNUAL REPORT 2018 ANNUAL REPORT AND FORM 20-F 2 2018 | ANNUAL REPORT 2018 | ANNUAL REPORT 3 Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes No Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and emerging growth company” in Rule 12b-2 of the Exchange Act. Large accelerated filer Accelerated filer Non-accelerated filer Emerging growth company If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: U.S. -

Rachel Howard

RACHEL HOWARD BIOGRAPHY Born 1969 in Easington, County Durham, UK Lives and works in UK EDUCATION 1989 - 1992 BA Fine Art & History or Art, Goldsmiths College, London, UK AWARDS 2008 British Council Award, London, UK 2004 Jerwood Drawing Prize, London, UK (shortlisted) FORTHCOMING SOLO EXHIBITIONS 2021 Simon Lee Gallery, London, UK SELECTED SOLO EXHIBITIONS 2019 Rachel Howard L'appel du vide, Blain Southern, New York, NY 2018 Paintings of Violence (Why I am Not a mere Christian), MASS MoCA, North Adams, MA Repetition is Truth - Via Dolorosa, Newport Street Gallery, London, UK Der Kuss, Blain Southern, London, UK 2016 Rachel Howard, MACRO Testaccio, Rome, Italy 2015 At Sea, Jerwood Gallery, Hastings, UK 2014 Northern Echo, BlainSouthern, London, UK 2011 Folie à Deux, BlainSouthern, London, UK Repetition is Truth – Via Dolorosa, Museo d’ArteContemporanea Donna Regina, Naples, Italy Still Life / Still Here. Rachel Howard. New Paintings, Sala Pelaires, Palma de Mallorca, Spain 2010 Human Shrapnel – oil drawings on paper, Other Criteria, London, UK 2009 Der Wald, Haunch of Venison, Zurich, Switzerland 2008 Rachel Howard: invited by Philippa van Loon, Museum van Loon, Amsterdam, The Netherlands (exh. cat.) How to Disappear Completely - New Work by Rachel Howard, Haunch of Venison, London, UK (exh. cat.) 2007 Fiction/Fear/Fact, Bohen Foundation, New York, NY (exh. cat.) Rachel Howard - New Paintings,Gagosian Gallery, Los Angeles, CA (exh. cat.) 2003 Guilty, Bohen Foundation, New York, NY Can’t Breathe Without You, Anne Faggionato, London, UK (exh. cat.) 2001 Painting 2001, Anne Faggionato, London, UK (exh. cat.) 1999 Rachel Howard: New Paintings, A22 Gallery, London, UK SELECTED GROUP EXHIBITIONS 2020 I WANT TO FEEL ALIVE AGAIN, Lyles and King, New York, NY MOVING ENERGIES – 10 years, me Collectors Room, Berlin, Germany Received Wisdom, Sunderland Museum and Winter Gardens, Arts Council Collection, UK A Dreadful Day, Paul Stolper Gallery, London, UK 2019 Galerie Simpson: Selection Box, Pallant House, Chichester, UK Birth, T.