Berenberg Equity Research

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TLG Finance S.À R.L. TLG IMMOBILIEN AG

Not for distribution in the United States of America TLG Finance S.à r.l. (a limited liability company (société à responsabilité limitée) under the laws of the Grand Duchy of Luxembourg) €600,000,000 Undated Subordinated Notes subject to Interest Rate Reset with a First Call Date in 2024 ISIN XS2055106210, Common Code 205510621 and German Securities Code (WKN) A2R77Q Issue Price: 98.835% guaranteed on a subordinated basis by TLG IMMOBILIEN AG (a stock corporation (Aktiengesellschaft) under the laws of the Federal Republic of Germany) TLG Finance S.à r.l., incorporated under the laws of the Grand Duchy of Luxembourg (“Luxembourg”) as a limited liability company (société à responsabilité limitée), (the “Issuer”) will issue, on September 23, 2019 (the “Issue Date”), €600,000,000 in the aggregate principal amount of undated subordinated notes (the “Notes”) subject to an interest rate reset at 5-year intervals commencing on December 23, 2024 (the “First Reset Date”, and a “Reset Date” being the First Reset Date and thereafter each fifth anniversary of the immediately preceding such Reset Date, as specified in the Terms and Conditions, and a “Reset Period” being a period from and including the First Reset Date to but excluding the next following Reset Date and thereafter from and including each Reset Date to but excluding the next following Reset Date). The Notes, which are governed by the laws of the Federal Republic of Germany (“Germany”), will be issued in a denomination of €100,000 each (the “Principal Amount”). The Notes are unconditionally and irrevocably guaranteed by TLG IMMOBILIEN AG, incorporated under the laws of Germany as a stock corporation (Aktiengesellschaft) (the “Guarantor” and, together with all its consolidated subsidiaries, “TLG” or the “Group”) pursuant to a subordinated guarantee (the “Subordinated Guarantee”). -

Commerzbank German Investment Seminar Christian Bruch, President and CEO Siemens Energy January 13, 2021

Commerzbank German Investment Seminar Christian Bruch, President and CEO Siemens Energy January 13, 2021 Siemens Energy is a registered trademark licensed by Siemens AG. © Siemens Energy, 2021 Disclaimer INFORMATION AND FORWARD-LOOKING STATEMENTS This document contains statements related to our future business and financial performance, and future events or developments involving Siemens Energy that may constitute forward-looking statements. These statements may be identified by words such as “expect,” “look forward to,” “anticipate” “intend,” “plan,” “believe,” “seek,” “estimate,” “will,” “project,” or words of similar meaning. We may also make forward-looking statements in other reports, prospectuses, in presentations, in material delivered to shareholders, and in press releases. In addition, our representatives may from time to time make oral forward-looking statements. Such statements are based on the current expectations and certain assumptions of Siemens Energy´s management, of which many are beyond Siemens Energy´s control. These are subject to a number of risks, uncertainties, and other factors, including, but not limited to, those described in disclosures, in particular in the chapter “Report on expected developments and associated material opportunities and risks” in the Annual Report. Should one or more of these risks or uncertainties materialize, should acts of force majeure, such as pandemics, occur, or should underlying expectations including future events occur at a later date or not at all, or should assumptions prove incorrect, Siemens Energy´s actual results, performance, or achievements may (negatively or positively) vary materially from those described explicitly or implicitly in the relevant forward-looking statement. Siemens Energy neither intends, nor assumes any obligation, to update or revise these forward-looking statements in light of developments which differ from those anticipated. -

Women-On-Board-Index

WOMENONBOARDINDEX III Aufsichtsräte (Stand 14.01.2012) powered by FidAR Zahl Anteil WoB-Index Posit Zahl AR- Unternehmen Notierung Frauen Frauen nur ion Mitgl. AR AR Aufsichtsräte 1 Douglas Holding AG MDAX 16 8 50% 50,00% 2 Kabel Deutschland Holding AG MDAX 12 5 42% 41,67% 3 Deutsche Bank AG DAX 20 8 40% 40,00% 4 Amadeus Fire AG SDAX 11 4 36% 36,36% 5 Bechtle AG TecDAX 12 4 33% 33,33% 5 Beiersdorf AG DAX 12 4 33% 33,33% 5 Bertrandt AG SDAX 6 2 33% 33,33% 5 Biotest AG SDAX 6 2 33% 33,33% 5 centrotherm photovoltaics AG TecDAX 3 1 33% 33,33% 5 comdirect bank AG SDAX 6 2 33% 33,33% 5 HAMBORNER REIT SDAX 9 3 33% 33,33% 5 TAG Immobilien AG SDAX 6 2 33% 33,33% 13 Deutsche Post AG DAX 20 6 30% 30,00% 13 GfK SE SDAX 10 3 30% 30,00% 15 Sky Deutschland AG MDAX 7 2 29% 28,57% 16 Commerzbank AG DAX 20 5 25% 25,00% 16 Fielmann AG MDAX 16 4 25% 25,00% 16 Fraport AG MDAX 20 5 25% 25,00% 16 Henkel AG & Co. KGaA DAX 16 4 25% 25,00% 16 Merck KGaA DAX 16 4 25% 25,00% 16 Q-CELLS SE TecDAX 8 2 25% 25,00% 16 Software AG TecDAX 12 3 25% 25,00% 16 Symrise AG MDAX 12 3 25% 25,00% 24 Axel Springer AG MDAX 9 2 22% 22,22% 24 STADA Arzneimittel AG MDAX 9 2 22% 22,22% 26 ADVA AG Optical Networking TecDAX 5 1 20% 20,00% 26 Deutsche Telekom AG DAX 20 4 20% 20,00% 26 Hawesko Holding AG SDAX 5 1 20% 20,00% 26 Münchener Rück AG DAX 20 4 20% 20,00% 26 RHÖN-KLINIKUM AG MDAX 20 4 20% 20,00% 26 Siemens AG DAX 20 4 20% 20,00% 26 ThyssenKrupp AG DAX 20 4 20% 20,00% 33 Praktiker Bau- und Heimwerkermärkte SDAX 16 3 19% 18,75% 33 TUI AG MDAX 16 3 19% 18,75% 35 adidas AG DAX 12 -

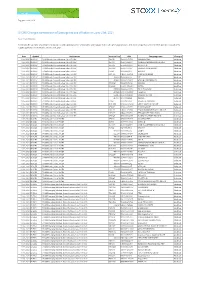

STOXX Changes Composition of Strategy Indices Effective on June 21St, 2021

Zug, June 11th, 2021 STOXX Changes composition of Strategy Indices effective on June 21st, 2021 Dear Sir and Madam, STOXX Ltd., the operator of Qontigo’s index business and a global provider of innovative and tradable index concepts, today announced the new composition of STOXX Strategy Indices as part of the regular quarterly review effective on June 21st, 2021 Date Symbol Index name Internal Key ISIN Company name Changes 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK SE502D SE0006593927 KLOVERN PREF. Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK SE0039 SE0011844091 SAMHALLSBYGGNADSBOL AGET Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK SE50HS SE0002626861 CLOETTA 'B' Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK SE50MX SE0007100607 SVENSKA HANDBKN.'B' Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK FI5024 FI4000058870 AKTIA 'A' Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK DK1064 DK0060036564 SPAR NORD BANK Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK 498539 FI0009800643 YIT Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK 453890 SE0000191827 ATRIUM LJUNGBERG 'B' Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK SE50BM SE0007185418 NOBINA Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK NO40AP NO0010716418 ENTRA Addition 11.06.2021 BDXDSX STOXX Nordic Diversification Select 30 SEK 597838 SE0000667925 TELIA COMPANY Deletion -

Lyxor German Mid-Cap MDAX UCITS ETF - Dist

LYXOR ETF MONTHLY REPORT 31st August 2021 Lyxor German Mid-Cap MDAX UCITS ETF - Dist 1. FUND INFORMATION Ticker: MD4X GY Description Ticker MD4X GY Lyxor Asset Management Group ("Lyxor") was founded in 1998 and comprises two subsidiaries (1) (2) of Société Générale group. Lyxor benefits from the Fund Type SICAV expertise of 600 professionals across the wealth management world, advising EUR 117.6 billion* in assets. Lyxor offers bespoke asset management services, UCITS compliant Yes capitalising on its know-how in ETFs and indexing, Alternative and Multi Management, and Absolute Performance and Solutions. As one of the most ISIN FR0011857234 experienced players on the market, Lyxor ETF is Europe's number three provider of ETFs (number two in terms of liquidity (3)), with AuM of more than EUR UKFRS Yes 49.8 billion*. With 220 ETFs listed on 13 financial marketplaces, Lyxor ETF provides investors with varied investment solutions enabling them to diversify their allocation across the entire spectrum of asset classes (equities, bonds, money market instruments and commodities via forward financial instruments). Replication method Indirect (Swap Based) Demonstrating its commitment to high-quality ETFs, in 2011, Lyxor ETF implemented an ETF quality charter with the aim of ensuring that each ETF it offers Full ownership of fund assets Yes complies with the strictest requirements in terms of replication quality, risk monitoring, liquidity and transparency. www.lyxoretf.com Share Class Currency EUR Investment objective Inception Date 15/05/2014 Nav per share at inception (EUR) 100 The Lyxor German Mid-Cap MDAX UCITS ETF - Dist is a UCITS compliant exchange traded fund that aims to track the benchmark index MDAX PERF INDEX. -

In This Issue

FI.News June 2019 In this issue: Island stopping: The importance of digital standards Supply chain finance: Making it more inclusive The Belt and Road Initiative: Bridging east and west Post-trade services: Delivering on new expectations Clearing the decks 10 Bridging east and west Making supply chain finance more inclusive 12 08 Contents Editorial welcome 03 Eye on the industry: Delivering on new 14 expectations in post-trade Big Interview: Island stopping 05 Regional spotlight: Are trade opportunities 16 in Africa shifting south? Innovation focus: Making supply chain 08 Regional focus: Seizing opportunities in 18 finance more inclusive central America Eye on the industry: Clearing the 10 News & awards 20 decks Expert view: Bridging east and west 12 Commerzbank in the press 22 2 Editorial welcome Never standing still Nikolaus Giesbert Divisional Board Member, Trade Finance & Cash Management While Commerzbank takes pride in its history, • Moving towards end-to-end, front-to-back, we are not a bank content to stand still. Having digital solutions; financed trade since 1870, we are accustomed to change. And today, technology, regulation • Being at the forefront of exploring how and changing client preferences stand to emerging technologies can transform fundamentally alter transaction banking, the landscape for trade finance and cash bringing new services, business models and management, and; competition. It’s a dynamic we are embracing. • Recognising permanent changes in the banking So rather than take a short-sighted view and sector and understanding the possibilities. focus simply on the automation of processes, we have invested resources and energy into Of course, extensive transformation must be digital transformation. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

MFS Meridian® Funds

Shareholder Semiannual Report 31 July 2021 MFS Meridian® Funds Luxembourg-Registered SICAV RCS: B0039346 SICAV-UK-SEM-7/21 MFS Meridian® Funds CONTENTS General information .................................................................... 3 Shareholder complaints or inquiries .......................................................... 3 Schedules of investments ................................................................. 4 Statements of assets and liabilities ........................................................... 130 Statements of operations and changes in net assets ............................................... 135 Statistical information ................................................................... 140 Notes to financial statements .............................................................. 179 Addendum .......................................................................... 217 Directors and administration ............................................................... 223 Primary local agents ................................................................ back cover MFS Meridian® Funds listing The following sub-funds comprise the MFS Meridian Funds family. Each sub-fund name is preceded with “MFS Meridian Funds –” which may not be stated throughout this report. Asia Ex-Japan Fund ® Blended Research European Equity Fund Continental European Equity Fund Contrarian Value Fund Diversified Income Fund Emerging Markets Debt Fund Emerging Markets Debt Local Currency Fund Emerging Markets Equity Fund Emerging Markets -

Company Presentation

H1 2019 FINANCIAL RESULTS PRESENTATION AUG 2019 Cologne TABLE OF CONTENTS 1 Financial Highlights 2 Financial and Portfolio performance 3 ESG 4 Guidance 5 Appendix 2 1 FINANCIAL HIGHLIGHTS H1 2019 Net profit Rental and Consistent top-line & Net rental income Adjusted EBITDA € 250 million operating income bottom-line growth € 189 million € 146 million EPS (Basic) € 278 million € 1.28 FFO I per share FFO I per share 65% of FFO I Robust operational FFO I after perpetual notes Dividend yield over performance € 0.64 attribution € 106 million 1) (FFO I yield: 6.3 %1) € 0.54 2019 guidance: 4.0 % 1) based on a share price of €20.4 EPRA NAV EPRA NAV incl. perpetuals Secure financial structure Total Assets LTV enabling consistent € 3.9 billion, € 4.9 billion, € 9.3 billion 34 % shareholder value creation per share € 23.1 per share € 29.2 *Dividend adjusted 3 2 OPERATIONAL RESULTS Selected Income Statement Data H1 2019 H1 2018 NET RENTAL INCOME (IN € MILLION) ADJUSTED EBITDA (IN € MILLION) in € ‘000 unless otherwise indicated Rental and operating income 278,195 268,275 146 Net rental income 189,320 181,682 182 189 137 Property revaluations and capital gains 210,877 249,985 Property operating expenses (128,581) (127,076) Administrative & other expenses (6,015) (6,062) EBITDA 356,386 387,544 Adjusted EBITDA 146,253 136,749 H1 2018 H1 2019 H1 2018 H1 2019 Finance expenses (22,807) (23,322) Other financial results (19,731) (24,061) Current tax expenses (15,429) (13,600) Deferred tax expenses (47,264) (54,088) ADJUSTED EBITDA (IN € MILLIONS) Profit for -

Eurex Circular 043/14

eurex circular 043/14 Date: 6 March 2014 Recipients: All Trading Participants of Eurex Deutschland and Eurex Zürich and Vendors Authorized by: Thomas Book Action required A. Single Stock Futures: Introduction of SSFs on Belgian, French, German, Italian, Spanish and Swiss underlyings; B. Equity options: Introduction of equity options on CompuGroup Medical AG, Flughafen Wien AG Inhaber-Aktien o.N. and Nemetschek AG Inhaber-Aktien o.N. Contact: Derivatives Trading Operations, T +49-69-211-1 12 10, Michael Durica, T +49-69-211-1 59 23 Content may be most important for: Attachments: Ü All departments 1. Updated Annexes A and B of the Contract Specifications for Futures Contracts and Options Contracts at Eurex Deutschland and Eurex Zürich 2. Market Maker Obligations (excerpt) Summary: The Management Board of Eurex Deutschland and the Executive Board of Eurex Zürich AG took the following decisions with effect from 10 March 2014: 1. Introduction of Single Stock Futures on Beneteau S.A. Actions Port. EO -,10, Société Foncière Lyonnaise SA Actions Port. EO 2, Carl Zeiss Meditec AG, Dt. Annington Immobilien SE Namens-Aktien o.N., CompuGroup Medical AG, CANCOM SE, Almirall S.A. Acciones Port. EO -,12, GameLoft SE Actions Port. EO 0,05, Helvetia Holding AG, KBC Ancora Actions au Port. o.N, LEG Immobilien AG, LPKF Laser & Electronics AG, C.M.B. (Cie Maritime Belge) SA Actions Nouvelles au Port.o.N., Nemetschek AG Inhaber-Aktien o.N., Norma Group SE, Telefonica Deutschland Holding, Swiss Prime Site AG, Sartorius AG, Temenos Group AG and Yoox S.p.A. Azioni nom. -

Citigroup Global Markets Deutschland AG

Citigroup Global Markets Deutschland AG Frankfurt am Main Ausschließlich zur Verbreitung in der Bundesrepublik Deutschland Endgültige Angebotsbedingungen - Nr. N010130 vom 05.09.2012 - zum Basisprospekt Nr. 5 vom 09.05.2012 in seiner jeweils aktuellen Fassung (der „Basisprospekt“) für Open End Turbo Stopp-Loss Optionsscheine mit Knock-Out und Gap-Risiko (Mini Future Optionsscheine) bezogen auf folgende Basiswerte: adidas, Aixtron, Allianz, Amazon.com, Apple Computer, Aurubis, BAIDU.COM, Bank of America, BASF, Bayer, Beiersdorf, Bilfinger Berger, BMW, Broadcom, Chesapeake, Cisco Systems, Commerzbank, Continental, Deutsche Wohnen, Deutz, Dialog Semiconductor, Equinix, Exxon Mobil, First Solar, freenet, Fresenius, Fresenius Medical Care, Fuchs Petrolub Vz., Gagfah, Gerry Weber, Google, Green Mountain Coffee Roasters, Halliburton, Hamburger Hafen und Logistik, Hannover Rück, HeidelbergCement, Infineon, Intel, Itron, IVG Immobilien, J. P. Morgan Chase & Co., Juniper Networks, Kloeckner & Co, Lanxess, Leoni, Linde, Lufthansa, Luminex, Marvell Technology, McDonalds, Merck KGaA, Monsanto, MTU, Münchener Rück, Netflix, NVIDIA, Porsche Vorzüge, ProSiebenSat.1 Media Vz., RWE, SAP, Schlumberger, Siemens, Software AG, SolarWorld, STADA, Starbucks, Südzucker, TAG Immobilien, Texas Instruments, United Internet, Vale, Volkswagen Vz., Vossloh, Wacker Chemie, Wincor Nixdorf, Wirecard ISIN: DE000CT7U8C8 - DE000CT7U8Z9 DE000CT7U900 - DE000CT7U991 DE000CT7U9A0 - DE000CT7U9Z7 DE000CT7UA08 - DE000CT7UA99 DE000CT7UAA7 - DE000CT7UAZ4 DE000CT7UB07 - DE000CT7UB98 -

LEG Immobilien AG (Incorporated in Germany As a Stock Corporation)

Not for distribution in the United States of America LEG Immobilien AG (incorporated in Germany as a stock corporation) €500,000,000 1.250% Fixed Rate Standalone Notes due 2024 ISIN XS1554456613, Common Code 155445661 and German Securities Code (WKN) A2E4W8 Issue Price: 99.409% LEG Immobilien AG, with its registered office at Hans-Böckler-Straße 38, 40476 Düsseldorf, Germany, and registered in the commercial register of the Local Court of Düsseldorf, Germany, under HRB 69386 (the “Issuer” or the “Company”, and together with its fully consolidated subsidiaries, the “Group”, “LEG” or “LEG Group”) will issue on January 23, 2017 Notes in the aggregate principal amount of €500,000,000 due 2024 (the “Notes”). The Notes will bear interest at a rate of 1.250% per year. The Issuer will pay interest on the Notes annually in arrears on January 23, commencing on January 23, 2018. The Notes, which are governed by the laws of the Federal Republic of Germany (“Germany”), will be issued in a denomination of €100,000 each. The Notes will constitute direct, unconditional, unsecured and unsubordinated obligations of the Issuer, ranking pari passu among themselves and pari passu with all other unsecured and unsubordinated obligations of the Issuer, unless such obligations are accorded priority under mandatory provisions of statutory law. Unless previously redeemed or purchased and cancelled in accordance with the terms and conditions of the Notes (“Terms and Conditions”), the Notes will be redeemed at par on January 23, 2024 (the “Maturity Date”). The Notes may be redeemed before the Maturity Date, in whole but not in part, at their principal amount, together with, if applicable, accrued interest, notably in the event of any change in taxation or in an event of default, see “Terms and Conditions of the Notes—§6 Redemption—(2) Early Redemption for Reasons of Taxation” and “Terms and Conditions of the Notes—§10 Events of Default”.