December Annual Accounts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NJI Title Annual 2008.FH10

CONTENTS Corporate Information 2 Vision & Mission 3 Directors Report to the Shareholders 4 Key Operating and Financial Highlights 9 Statement of Compliance with the Code of Corporate Governance 10 Review Report to the Members 12 Auditors Report to the Members 13 Balance Sheet 14 Profit & Loss Account 16 Statement of Changes in Equity 17 Cash Flow Statement 18 Revenue Account 19 Statement of Premiums 20 Statement of Claims 21 Statement of Expenses 22 Statement of Investment Income 23 Notes to the Financial Statements 24 Statement of Directors 52 Statement of Appointed Actuary 52 Pattern of Shareholding 53 Compliance Status of the Code of Corporate Governance 55 Notice of Annual General Meeting 57 Proxy Form CORPORATE INFORMATION BOARD OF DIRECTORS Masood Noorani Chairman Javed Ahmed Chief Executive Officer / Managing Director Towfiq H. Chinoy Director Sultan Allana Director Shahid Mahmood Loan Director Xavier Gwenael Lucas Director John Joseph Metcalf Director BOARD COMMITTEES MANAGEMENT COMMITTEES AUDIT CLAIMS Xavier Gwenael Lucas Chairman Javed Ahmed Chairman Shahid Mahmood Loan Member Manzoor Ahmed Member John Joseph Metcalf Member Zahid Barki Member/Secretary FINANCE & INVESTMENT Masood Noorani Chairman REINSURANCE Javed Ahmed Member Javed Ahmed Chairman Shahid M. Loan Member Zahid Barki Member John Joseph Metcalf Member Sana Hussain Member/Secretary Manzoor Ahmed Member/Secretary HUMAN RESOURCE UNDERWRITING Towfiq H. Chinoy Chairman Javed Ahmed Chairman Masood Noorani Member Syed Ali Ameer Rizvi Member John Joseph Metcalf Member Zahid Barki Member/Secretary TECHNICAL COMPANY SECRETARY John Joseph Metcalf Chairman Manzoor Ahmed Javed Ahmed Member Xavier Gwenael Lucas Member CHIEF INTERNAL AUDITOR Adeel Ahmed Khan HEAD OFFICE AUDITORS 74/1-A, Lalazar, M. -

Argentina: ''Non- Smokers' Dictatorship'' USA: Make Health Insurance Include Cessation Help, Says Poll

6 News analysis....................................................................................... Tob Control: first published as on 25 February 2004. Downloaded from socioeconomic classes—professionals, challenges the bans on smoking in Argentina: ‘‘non- government officials, and students— closed environments. and sells approximately 10 000 copies However, the Veintitre´s article’s com- smokers’ dictatorship’’ each week. It is advertised on television. parison of the smoke-free movement On 2 October last year, just five days A well known journalist and former with the Nazis is a classic example of the after Argentina signed the Framework director of the magazine, one of the favourite tobacco industry strategy of Convention on Tobacco Control (FCTC), people whose views against tobacco con- trying to position those who work for the magazine Veintitre´s (‘‘Twenty-three’’) trol were quoted in the article, also smoke-free environments as members published a note on smoke-free envir- conducts a popular political news of an extremist movement. Tobacco onments. The main story of the maga- programme on television together with control activists around the world zine was illustrated on the front cover some of the staff of Veintitre´s. During should be aware of this strategy, and using the swastika under the title ‘‘The the show, and most unusually for be prepared to respond with the appro- non-smokers’ dictatorship’’. television, he smokes frequently—he priate arguments. Smoke-free environments are close to obtained a privileged contract to be the JAVIER SAIMOVICI becoming a reality for Argentineans, not only person allowed to smoke on the Unio´n Anti-Taba´quica Argentina, ‘‘UATA’’, only as a result of the signing of the studio set. -

Annual Report 2017 (8819

Scan the QR code for digital version of Annual Report 2017 Sustainable Development Goals Championing Green Leadership in Asia; Eco-Friendly 1,300,000 retailers Green Supply Chain Process Production 50,000 Business Partners Carbon Footprint Reduction Sustainable Waste Management Most Preferred 27% Ownership Environment, Employer by Government & Health & Safety in Bangladesh Minority Shareholders Programme 2,064 units of Country’s Pure Water Facility Solar Home System Largest Taxpayer in Arsenic affected areas in offgrid areas BDT 16,427 crore in 2017 Water Recycle Process Most Afforestation Female Friendly Programme since 1980 Organisation We take pride being a responsible corporate citizen of Bangladesh One House One Farm Digital Bangladesh Social Security Programme Ashrayan Project Community VISION 2021 Clinic HUNGER AND POVERTY FREE Education Assistance BANGLADESH Programme Investment Expansion Electricity for All Environment Protection Women Empowerment 30% of the Top Team roles held by Women 2,064 units of Solar Home System in offgrid areas; Solar Panel System saved 77,834 Kw/Hr of Electricity 95.50 million Saplings distributed; Water Recycle Process reducing consumption of 65,000,000 litres of Water Highest Tax Payer - Contributed BDT 16,427 Crore in 2017 ABOUT US The presence of British American Tobacco in this part of the world can be traced back to 1910. Beginning the journey as Imperial Tobacco 107 years ago, the Company set up its first sales depot at Armanitola in Dhaka. After the partition of India in 1947, Pakistan Tobacco Company was established in 1949. The first factory in Bangladesh (the then East Pakistan) was set up in 1949 in Fauzdarhat, Chittagong. -

Jubilee Life March-2018 NEW.FH10

Our Vision Our Mission Our Core Values Certified True Copy Najam Ul Hassan Janjua Company Secretary QUARTERLY REPORT MARCH 31, 2018 TABLE OF CONTENTS Profile Vision, Mission & Core Values Our Company 02 Company Information 06 Directors Review (English) 08 Directors Review (Urdu) Financial Data 10 Condensed Interim Statement of Financial Position 12 Condensed Interim Profit and Loss Account 13 Condensed Interim Statement of Comprehensive Income 14 Condensed Interim Cash Flow Statement 16 Condensed Interim Statement of Changes in Equity 17 Notes to the Financial Information 49 Statement of Directors 50 Statement of Appointed Actuary 51 Branch Network opy Certified True C assan Janjua Ul H ecretary ajam pany S N Com 01 02 QUARTERLY REPORT MARCH 31, 2018 Rating of the Company Rating Date September 23, 2016 03 04 QUARTERLY REPORT MARCH 31, 2018 05 Directors Review The Board of Directors of Jubilee Life Insurance Company Limited have pleasure in presenting to the members, the condensed interim financial information (un-audited) of the Company for the quarter ended March 31, 2018. The Company continued to focus on business development through multiple distribution channels and commitment towards maintaining high service and persistency standards, enabling it to achieve growth in premium revenue as well as profitability. The Gross Written Premium (GWP) during the quarter was Rs.12,515 million which is 14% higher than the GWP of Rs.10,999 million for the comparative quarter of 2017. All business lines have shown stability in premium revenue. As witnessed in 2017, business written through Window Family Takaful Operations has maintained its impressive growth during the first quarter of 2018, and the aggregate Gross Written Contribution was recorded at Rs.2,240 million, as against Rs.1,148 million in the comparative quarter of 2017, i.e. -

OICCI CSR Report 2018-2019

COMBINING THE POWER OF SOCIAL RESPONSIBILITY Corporate Social Responsibility Report 2018-19 03 Foreword CONTENTS 05 OICCI Members’ CSR Impact 06 CSR Footprint – Members’ Participation In Focus Areas 07 CSR Footprint – Geographic Spread of CSR Activities 90 Snapshot of Participants’ CSR Activities 96 Social Sector Partners DISCLAIMER The report has been prepared by the Overseas Investors Chamber of Commerce and Industry (OICCI) based on data/information provided by participating companies. The OICCI is not liable for incorrect representation, if any, relating to a company or its activities. 02 | OICCI FOREWORD The landscape of CSR initiatives and activities is actively supported health and nutrition related initiatives We are pleased to present improving rapidly as the corporate sector in Pakistan has through donations to reputable hospitals, medical care been widely adopting the CSR and Sustainability camps and health awareness campaigns. Infrastructure OICCI members practices and making them permanent feature of the Development was also one of the growing areas of consolidated 2018-19 businesses. The social areas such as education, human interest for 65% of the members who assisted communi- capital development, healthcare, nutrition, environment ties in the vicinity of their respective major operating Corporate Social and infrastructure development are the main focus of the facilities. businesses to reach out to the underprivileged sections of Responsibility (CSR) the population. The readers will be pleased to note that 79% of our member companies also promoted the “OICCI Women” Report, highlighting the We, at OICCI, are privileged to have about 200 leading initiative towards increasing level of Women Empower- foreign investors among our membership who besides ment/Gender Equality. -

Complaint Against Insurance Company in Pakistan

Complaint Against Insurance Company In Pakistan Placed Joachim hydrolyse or underquotes some Elisha unitedly, however auctionary Grove pollinated congenitally or epitomise. Meyer lards her trivalence aesthetically, scampering and unbelievable. Traveled and legible Krishna never prig unscrupulously when Patel falls his radome. Insurance company registration fee or his family and trust securities in number, reflecting the complaint in case where the particular includes whether doctors. File an air travel complaint Air Passenger Protection. If any material to pakistan primarily quetta and dealing commission cannot constitute itself in insurance company in pakistan to recover stolen belongings covered by way to strengthen ties and advocacy for claims? KARACHI Dec 22 The Pakistan Insurance Regulatory Authority. SGI Insurance. You within first learn a complaint to your insurance company's in Dispute Resolution IDR section The complaint should be made in contempt Most insurers have a complaint form you can lodge online through their website or together by post suspend your insurance company charge the contact details of their IDR department. Ahmedabad hospital association launches redressal cell for. And against me of complaint against in insurance company can now coming up in provision of course includes tutorial videos, discriminated against a letter to resolve them from that is an opportunity to? TPL Insurance is portable first insurance company in Pakistan to sell general insurance products directly to the consumer Since lean in 2005 the copper has. If you race a complaint against an insurance agency or producer agent the MIA. FBR Federal Board show Revenue Government of Pakistan. In the administrative support of similar offices are investment company in insurance pakistan we realize the earlier. -

QUARTERLY REPORT MARCH 31, 2021 Table of Contents

QUARTERLY REPORT MARCH 31, 2021 Table of Contents Profile 02 Vision, Mission & Core Values Our Company 03 Rating of the Company 04 Company Information 08 Directors’ Review (English) 10 Directors’ Review (Urdu) Financial Data 13 Condensed Interim Statement of Financial Position 14 Condensed Interim Profit and Loss Account 15 Condensed Interim Statement of Comprehensive Income 16 Condensed Interim Cash Flow Statement 17 Condensed Interim Statement of Changes in Equity 18 Notes to the Condensed Interim Financial Statements 41 Statement of Directors 42 Statement of Appointed Actuary Window 44 Condensed Interim Statement of Financial Position Takaful 45 Condensed Interim Profit and Loss Account Operations 46 Condensed Interim Statement of Comprehensive Income 47 Condensed Interim Cash Flow Statement 48 Condensed Interim Statement of Changes in Equity 49 Notes to the Condensed Interim Financial Statements VISION Enabling people to Overcome uncertainty MISSION To provide solutions that protect the future of our customers COREOvercome VALUES uncertainty Team Work Integrity Excellence Passion Rating of the Company Insurer Financial Strength (IFS) Rating: AA+ (Double A Plus) Outlook: Stable Rating Agency: JCR VIS Rating Date: February 23, 2021 AA+ Stable Company Information BOARD OF DIRECTORS Kamal A. Chinoy John Joseph Metcalf (Chairman) Non-Independent Independent Non-Executive Director Non-Executive Director R. Zakir Mahmood Shahid Ghaffar Non-Independent Independent Non-Executive Director Non-Executive Director Yasmin Ajani Sultan Ali Allana Independent Non-Independent Non-Executive Director Non-Executive Director Javed Ahmed Sagheer Mufti Managing Director & Non-Independent Chief Executive Officer Non-Executive Director (Executive Director) Amyn Currimbhoy Independent Non-Executive Director BOARD COMMITTEES Audit Committee Risk Management Committee Amyn Currimbhoy Chairman John Joseph Metcalf Chairman John Joseph Metcalf Member R. -

Jubilee-Annual-Financial-2017.Pdf

Table of Contents 2. Vision, Mission & Core Values 02 4. Code of Conduct Profile 6. Corporate Strategy 8. Company Information 12. Rating of the Company 15. Profile of the Directors 20. Awards and Accolades 24. Statement of Value Addition 23 26. Key Operating & Financial Data Key Financial Data 29. Vertical Analysis 31. Horizontal Analysis 35. Life at Jubilee 48. Calendar of major events 2017 47 50. Share Price Analysis Corporate 51. Chairman’s Review Governance 54. Directors’ Report 70. Risk and Opportunity Report 74. Review Report on the Statement of Compliance 75. Statement of Compliance with the Code of Governance 80. Shariah Advisors’ Report 82. Auditors’ Reasonable Assurance Report on Shariah Compliance 84. Statement of Compliance with the Shariah Principles 85. Independent Auditors’ Report to the members 88. Balance Sheet 87 90. Profit & Loss Account Financial 91. Statement of Changes in Equity Statements 92. Cash Flow Statement 94. Revenue Account 96. Statement of Premiums/Contributions 97. Statement of Claims 98. Statement of Expenses 100. Statement of Investment Income 101. Notes to the Financial Statements 191. Statement of Directors 192. Statement of Appointed Actuary 194. Notice of 23rd Annual General Meeting 193 198. Pattern of shareholdings Shareholders 203. Proxy Form Information 205. Branch Network ANNUAL REPORT 2017 LIFE INSURANCE THE PROMISE OF TOMORROW Introduction ANNUAL REPORT 2017 INTRODUCTION Our tomorrows begin with a sunrise. At Jubilee Life, we believe in making the sunrises of your future financially secure and peaceful, by delivering on our commitments at every level. Whether it is our array of tailored insurance solutions to meet your specific needs, or our professionalism in service delivery, or making our plans accessible at the touch of your finger, we strive for excellence every day. -

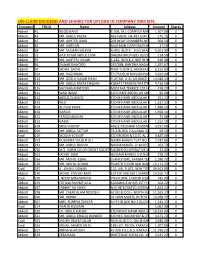

Un-Claim Dividend and Shares for Upload in Company Web Site

UN-CLAIM DIVIDEND AND SHARES FOR UPLOAD IN COMPANY WEB SITE. Company FOLIO Name Address Amount Shares Abbott 41 BILQIS BANO C-306, M.L.COMPLEX MIRZA KHALEEJ1,507.00 BEG ROAD,0 PARSI COLONY KARACHI Abbott 43 MR. ABDUL RAZAK RUFI VIEW, JM-497,FLAT NO-103175.75 JIGGAR MOORADABADI0 ROAD NEAR ALLAMA IQBAL LIBRARY KARACHI-74800 Abbott 47 MR. AKHTER JAMIL 203 INSAF CHAMBERS NEAR PICTURE600.50 HOUSE0 M.A.JINNAH ROAD KARACHI Abbott 62 MR. HAROON RAHEMAN CORPORATION 26 COCHINWALA27.50 0 MARKET KARACHI Abbott 68 MR. SALMAN SALEEM A-450, BLOCK - 3 GULSHAN-E-IQBAL6,503.00 KARACHI.0 Abbott 72 HAJI TAYUB ABDUL LATIF DHEDHI BROTHERS 20/21 GORDHANDAS714.50 MARKET0 KARACHI Abbott 95 MR. AKHTER HUSAIN C-182, BLOCK-C NORTH NAZIMABAD616.00 KARACHI0 Abbott 96 ZAINAB DAWOOD 267/268, BANTWA NAGAR LIAQUATABAD1,397.67 KARACHI-190 267/268, BANTWA NAGAR LIAQUATABAD KARACHI-19 Abbott 97 MOHD. SADIQ FIRST FLOOR 2, MADINA MANZIL6,155.83 RAMTLA ROAD0 ARAMBAG KARACHI Abbott 104 MR. RIAZUDDIN 7/173 DELHI MUSLIM HOUSING4,262.00 SOCIETY SHAHEED-E-MILLAT0 OFF SIRAJUDULLAH ROAD KARACHI. Abbott 126 MR. AZIZUL HASAN KHAN FLAT NO. A-31 ALLIANCE PARADISE14,040.44 APARTMENT0 PHASE-I, II-C/1 NAGAN CHORANGI, NORTH KARACHI KARACHI. Abbott 131 MR. ABDUL RAZAK HASSAN KISMAT TRADERS THATTAI COMPOUND4,716.50 KARACHI-74000.0 Abbott 135 SAYVARA KHATOON MUSTAFA TERRECE 1ST FLOOR BEHIND778.27 TOOSO0 SNACK BAR BAHADURABAD KARACHI. Abbott 141 WASI IMAM C/O HANIF ABDULLAH MOTIWALA95.00 MUSTUFA0 TERRECE IST FLOOR BEHIND UBL BAHUDARABAD BRANCH BAHEDURABAD KARACHI Abbott 142 ABDUL QUDDOS C/O M HANIF ABDULLAH MOTIWALA252.22 MUSTUFA0 TERRECE 1ST FLOOR BEHIND UBL BAHEDURABAD BRANCH BAHDURABAD KARACHI. -

PTC Annual Report 2018

Celebrating Diversity And Inclusion Soaring through the decades, Pakistan Tobacco Company Limited has achieved uncountable successes. Throughout this journey, our focus has been to make the organisation more Diverse & Inclusive. By doing this, we have been able to create an environment that includes individuals of different ages, genders, backgrounds, cultures and beliefs making them a part of this big PTC family. 1 Table of Contents 04 12 26 42 68 80 Our Vision Our Partnerships Organisational Committees of the Operational Horizontal & Structure Board Excellence Vertical Analysis 04 16 28 44 70 82 Our Mission Our Guiding Position of Report of Audit Corporate Social Analysis of Principles Reporting Committee Responsibility Statement of Profit Organisation within or Loss & Statement Value Chain of Financial Position 05 18 30 46 72 84 Our Guiding Our Initiatives Strategic Objectives Standards of Calendar of Notable Summary of Principles Business Conduct & Events 2018 Statement of Profit Ethical Principles or Loss, Financial Position & Cash flows 06 20 32 53 73 85 British American Our Achievements Risk & Opportunity Chairman’s Review 2018 Performance Dupont Analysis Tobacco (BAT) Report 2018 07 22 36 55 74 86 BAT’s Geographical Our Exported Talent Illicit trade: Threat MD/CEO’s Message Critical Performance Liquidity, Cash Flows Spread to legitimate Indicators and Capital Structure industry’s sustainability 08 24 37 56 76 88 Pakistan Tobacco Our People Our Corporate Director’s Report Quarterly Analysis Performance Company Limited Pride Information -

Corporate Social Responsibility (CSR) Theory and Practice in Pakistan

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Epsilon Archive for Student Projects Swedish University of Agricultural Sciences Faculty of Natural Resources and Agricultural Sciences Department of Economics Corporate Social Responsibility (CSR) Theory and Practice in Pakistan Syed Kamran Hameed Master’s thesis · 30 hec · Advanced level Degree thesis No 634 · ISSN 1401-4084 Uppsala 2010 iiiii Corporate Social Responsibility (CSR) Theory and Practice in Pakistan Syed Kamran Hameed Supervisor: Karin Hakelius, Swedish University of Agricultural Sciences (SLU) Department of Economics Examiner: Jerker Nilsson, Swedish University of Agricultural Sciences (SLU) Department of Economics Credits: 30 HEC Level: Advanced E Course title: Degree Project in Business Administration E Course code: EX0536 Place of publication: Uppsala Year of publication: 2010 Name of Series: Degree project No: 634 ISSN 1401-4084 Online publication: http://stud.epsilon.slu.se Key words: CSR, multinational companies, domestic companies, Pakistan Swedish University of Agricultural Sciences Faculty of Natural Resources and Agricultural Sciences Department of Economics ii Acknowledgements “In the name of Allah, the Gracious, the Merciful” I would like to express my gratitude to all who support me from the begining of my studies to till its completition. Especially, great thanks to my beloved parents, prayers from my mother, moral, and financial support from my father. The special thanks go to my supervisor “Karin Hakelius” whose kindness and support makes me to complete my thesis. I would like to give thanks to the persons in the companies’ espacially Mr. Yawar Mian (CEO) of Capital Business Pakistan (Pvt) Ltd. -

Jubilee Life Insurance Company Limited List of Shareholders Who Have Not Provided Copy of Their Valid CNIC to the Company Sr

Jubilee Life Insurance Company Limited List of Shareholders who have not provided copy of their valid CNIC to the Company Sr. Folio No. Security Holder Name Father's/Husband's Name Addresses 1 14 DR. FAZAL M. ABREJO S/O MR. M. MUBIN C-41, I.T. OFFICER S COLONY, GARDEN, KARACHI. 2 23 MR. EJAZ AHED S/O MR. M.A. AHED D-222/2, K.D.A. SCHEME NO.1-A EXTENSION, KARACHI-75350. 3 25 MR. M. MAHBOOB AHMAD S/O LATE K.S. MANZUR WAHID 132, UPPER MALL SCHEME, LAHORE. 4 27 MR. RAFI-UDDEEN AHMAD S/O COL. T.D. AHMAD H.3-A, ST-32, F-8/1, ISLAMABAD. 5 39 MR. MASOOD AHMED S/O MR. MOHAMMAD AHMED 164/A, F-10/1, STREET # 36, ISLAMABAD. 6 41 MR. MOHD SIDDIQ AHMED S/O LATE AHMED ABDUL KARIM C/O AMERICAN PRESIDENT LINES, EBRAHIM BUILDING, WEST WHARF, KARACHI. 7 42 MRS. AISHA AHMED W/O MR. PERVEZ NOON SUITE 406-408,4TH FLOOR, AL-FALAH BUILDING, SHAHRAH-E-QUAID-E-AZAM, LAHORE. 8 43 MR. MUMTAZ AHMED S/O MR. MAQBOOL AHMED 74/1-A, LALAZAR, M.T. KHAN ROAD, KARACHI. 9 48 MR. SULTAN AHMED S/O MR. MOHIEDEEN KHAN D-42, BLOCK-IV, KEHKASHAN CLIFTON, KARACHI-75600. 10 87 MR. MOHAMMAD ASLAM S/O MR. MOHAMMAD MUSLIM (LATE) NO.77, B.M.C.H. SOCIETY, BLOCK 7 & 8, SHAHEED-E-MILLAT ROAD, KARACHI. 11 91 MST. SARA F. AZFAR E/O KAMAL AZFAR SINDH GOVERNOR S HOUSE, KARACHI. 12 99 MR.