Chapter 5. Focus and Perspectives

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Global Catastrophe Review – 2015

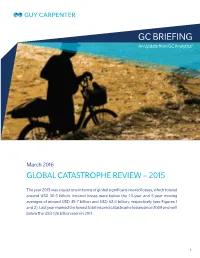

GC BRIEFING An Update from GC Analytics© March 2016 GLOBAL CATASTROPHE REVIEW – 2015 The year 2015 was a quiet one in terms of global significant insured losses, which totaled around USD 30.5 billion. Insured losses were below the 10-year and 5-year moving averages of around USD 49.7 billion and USD 62.6 billion, respectively (see Figures 1 and 2). Last year marked the lowest total insured catastrophe losses since 2009 and well below the USD 126 billion seen in 2011. 1 The most impactful event of 2015 was the Port of Tianjin, China explosions in August, rendering estimated insured losses between USD 1.6 and USD 3.3 billion, according to the Guy Carpenter report following the event, with a December estimate from Swiss Re of at least USD 2 billion. The series of winter storms and record cold of the eastern United States resulted in an estimated USD 2.1 billion of insured losses, whereas in Europe, storms Desmond, Eva and Frank in December 2015 are expected to render losses exceeding USD 1.6 billion. Other impactful events were the damaging wildfires in the western United States, severe flood events in the Southern Plains and Carolinas and Typhoon Goni affecting Japan, the Philippines and the Korea Peninsula, all with estimated insured losses exceeding USD 1 billion. The year 2015 marked one of the strongest El Niño periods on record, characterized by warm waters in the east Pacific tropics. This was associated with record-setting tropical cyclone activity in the North Pacific basin, but relative quiet in the North Atlantic. -

Appendix 8: Damages Caused by Natural Disasters

Building Disaster and Climate Resilient Cities in ASEAN Draft Finnal Report APPENDIX 8: DAMAGES CAUSED BY NATURAL DISASTERS A8.1 Flood & Typhoon Table A8.1.1 Record of Flood & Typhoon (Cambodia) Place Date Damage Cambodia Flood Aug 1999 The flash floods, triggered by torrential rains during the first week of August, caused significant damage in the provinces of Sihanoukville, Koh Kong and Kam Pot. As of 10 August, four people were killed, some 8,000 people were left homeless, and 200 meters of railroads were washed away. More than 12,000 hectares of rice paddies were flooded in Kam Pot province alone. Floods Nov 1999 Continued torrential rains during October and early November caused flash floods and affected five southern provinces: Takeo, Kandal, Kampong Speu, Phnom Penh Municipality and Pursat. The report indicates that the floods affected 21,334 families and around 9,900 ha of rice field. IFRC's situation report dated 9 November stated that 3,561 houses are damaged/destroyed. So far, there has been no report of casualties. Flood Aug 2000 The second floods has caused serious damages on provinces in the North, the East and the South, especially in Takeo Province. Three provinces along Mekong River (Stung Treng, Kratie and Kompong Cham) and Municipality of Phnom Penh have declared the state of emergency. 121,000 families have been affected, more than 170 people were killed, and some $10 million in rice crops has been destroyed. Immediate needs include food, shelter, and the repair or replacement of homes, household items, and sanitation facilities as water levels in the Delta continue to fall. -

Flashupdate 8May TC Noul.Pdf (PDF | 592.82

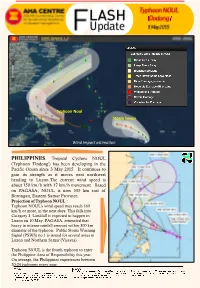

10 Dec 278 kph 9 Dec 8 Dec Typhoon Noul Storm Seven Wind impact estimation PHILIPPINES. Tropical Cyclone NOUL (Typhoon 'Dodong') has been developing in the THAILAND INDONESIA LAO PDR Pacific Ocean since 3 May 2015. It continues to Flood (Ongoing since 16-09-13) Flood Storm (Ongoing since 18-09-13) http://adinet.ahacentre.org/report/view/426 http://adinet.ahacentre.org/report/view/437 http://adinet.ahacentre.org/report/view/428 gain its strength as it moves west northwest Heavy rains caused flooding in Central and Due to the heavy rainfall, flood occurred in Sigi, Tropical Depression from South Cina Sea heading to Luzon.The current wind speed is Northern part of Thailand claiming for 31 death. Central Sulawesi Province. This incident causing flood in Champasack, Saravanne, about 150 km/h with 17 km/h movement. Based More than 3 million families have been affected affected 400 people and damaged 50 houses. Savannakhet, Sekong and Attapeu, impacting with more than 1,000 houses were damaged. 200,000 people and causing 4 deaths and on PAGASA, NOUL is now 595 km east of Twister damaging 1,400 houses. Bicol http://adinet.ahacentre.org/report/view/438 Borongan, Eastern Samar Province. CAMBODIA Eastern Visayas Flood (Ongoing since 24-09-13) VIET NAM Projection of Typhoon NOUL : Twister occurred in Binjai, North Sumatra Storm http://adinet.ahacentre.org/report/view/434 Province. The wind damaged 328 houses and 2 Typhoon NOUL's wind speed may reach 160 Central Visayas http://adinet.ahacentre.org/report/view/436 office buildings. km/h or more, in the next days. -

Estimation of the Sea Surface Wind in the Vicinity of Typhoon Using Himawari-8 Low-Level Amvs

Estimation of the sea surface wind in the vicinity of typhoon using Himawari-8 low-level AMVs Kenichi NONAKA, Kazuki SHIMOJI (MSC/JMA) and Koji KATO (Forecast Division/JMA) 13th International Winds Workshop June 27 – July 1, 2016 @Monterey, California, USA MSC/JMA Contents l Usefulness of Himawari-8 AMV for typhoon analysis l Comparison low-level AMV with ASCAT and RapidScat and estimation of sea surface wind from AMV l Accuracy of the estimated sea surface wind l Future plans l Summary IWW13@Monterey, California, USA 2 MSC/JMA Typhoon analysis Analysts and forecasters estiMate the tropical cyclone intensity using wind data over the ocean. But in situ observations such as ships and buoys are sparse. ASCAT and RapidScat sea wind data are very helpful and are Mainly used for the analysis, but the aMounts of data are not so enough. If we can evaluate surface winds over the ocean froM AMVs that assigned to low level, they are also very helpful for analysts and forecasters. ? IWW13@Monterey, California, USA 3 MSC/JMA IMproveMent in AMVs Retrieval Himawari-8 AMVs derived from MTSAT-2 AMVs derived from MTSAT- Himawari-8 imagery with new algorithm 2 imagery and heritage algorithm Resolution Resolution 2km/10min. 4km/30min. Resolution 4km/60min. Colder color : upper level wind warmer color : low level wind Himawari-8 and MTSAT-2 IR AMV (QI>60, 2015 01 14 1700UTC) IWW13@Monterey, California, USA 4 MSC/JMA AHI spectral bands Himawari-8/9 Imager (AHI) Spatial Central Band Primary Use Resolution Wavelength 1 0.47 µm vegetation, aerosol 1 km 2 Visible -

Island Echoes

ISLAND ECHOES Summary of Ministry Needs Dear Friends, is a publication of Growing up in the island world where the word Pacific Mission Aviation Personnel Needs: “Typhoon” raises a lot of fear, concern and (PMA). Missionary pastors emotion... I know what it’s like to spend the night Administrative and ministry assistants on land or sea, with the screaming gusts of wind Issue Youth workers for island churches and torrential rains causing chaos and leaving 2-2015 (July) Boat captain for medical ship M/V Sea Haven destruction in its wake. Typhoons... a rare Boat mechanic for medical ship M/V Sea Haven phenomenon? No! In one year the Philippines, the On our Cover Missionary pilots/mechanics for Micronesia/Philippines archipelago of more than 7,100 islands is hit by an Tyhpoon Maysak Relief Computer personnel for radio, media and print ministry average of 20 typhoons or tropical storms each Efforts, photos courtesy of Short term: Canon copier technician needed for year, which kill hundreds and sometimes Brad Holland maintenance and repair at Good News Press PMA President Nob Kalau thousands of people. Editors Bringing relief items to victims in the outer islands of Micronesia via the MV Sea Melinda Espinosa Infrastructure Needs: Haven, I have witnessed the mutilating destruction to atolls and islands. For some Sylvia Kalau islanders, the only means of safety and survival is tying their children to a coconut tree Sabine Musselwhite Renovation/Improvement for PMF Patnanungan as the waves sweep over their homeland. For others, it’s packing as many islanders as Parsonage including outside kitchen and dining area – After you can into the only cement-roof-building on the island, after your hut has blown Layout several typhoons and wear and tear of the building due to away. -

3Rd Quarter 2015

Climate Impacts and Hawaii and U.S. Pacific Islands Region Outlook 3rd Quarter 2015 nd Significant Events and Impacts for 2 Quarter 2015 El Niño Advisory Drought conditions continue Above normal rainfall fell across the Hawaiian Islands.. over most of the Federated States of Micronesia, Guam and the Commonwealth of Typhoon Dolphin passed the Northern Marianas. between Guam and Rota in May. Near-normal rainfall was observed in American Samoa and the Marshall Islands. Tropical Storm Nangka brought Prolonged dryness damaging winds and sea inundation Hot and dry weather was continues in Palau to the Marshall Islands in July. recorded across Hawaii. and western Micronesia. Through July, there have been a record 11 typhoons so far this season in the western Shading indicates each Island’s Exclusive Economic Zone (EEZ). North Pacific. nd Regional Climate Overview for 2 Quarter 2015 Sea-Surface Temperature Anomalies, valid Jul 25, July 2015 precipitation anomaly. Source: U.S. Drought Monitor for Hawaii, Aug 4, 2015. 2015 . Source: http://coralreefwatch.noaa.gov http://iridl.ldeo.columbia.edu/ Source: http://www.drought.gov The region is under an El Niño Advisory, and weather patterns were unambiguously in a climate state of El Niño during the quarter (e.g., abundant early- rd season typhoons, decadal -low sea levels, and wet weather across most of Micronesia). As of August 3 , the Niño 3.4 region anomaly was +1.7°C, supporting a strong El Niño state. Sea-surface temperatures were above normal across the central and eastern equatorial Pacific, with the warmest anomalies exceeding 1.5°C from Hawaii southwest to the Marshall Islands and further west toward Guam. -

Appendix 3 Selection of Candidate Cities for Demonstration Project

Building Disaster and Climate Resilient Cities in ASEAN Final Report APPENDIX 3 SELECTION OF CANDIDATE CITIES FOR DEMONSTRATION PROJECT Table A3-1 Long List Cities (No.1-No.62: “abc” city name order) Source: JICA Project Team NIPPON KOEI CO.,LTD. PAC ET C ORP. EIGHT-JAPAN ENGINEERING CONSULTANTS INC. A3-1 Building Disaster and Climate Resilient Cities in ASEAN Final Report Table A3-2 Long List Cities (No.63-No.124: “abc” city name order) Source: JICA Project Team NIPPON KOEI CO.,LTD. PAC ET C ORP. EIGHT-JAPAN ENGINEERING CONSULTANTS INC. A3-2 Building Disaster and Climate Resilient Cities in ASEAN Final Report Table A3-3 Long List Cities (No.125-No.186: “abc” city name order) Source: JICA Project Team NIPPON KOEI CO.,LTD. PAC ET C ORP. EIGHT-JAPAN ENGINEERING CONSULTANTS INC. A3-3 Building Disaster and Climate Resilient Cities in ASEAN Final Report Table A3-4 Long List Cities (No.187-No.248: “abc” city name order) Source: JICA Project Team NIPPON KOEI CO.,LTD. PAC ET C ORP. EIGHT-JAPAN ENGINEERING CONSULTANTS INC. A3-4 Building Disaster and Climate Resilient Cities in ASEAN Final Report Table A3-5 Long List Cities (No.249-No.310: “abc” city name order) Source: JICA Project Team NIPPON KOEI CO.,LTD. PAC ET C ORP. EIGHT-JAPAN ENGINEERING CONSULTANTS INC. A3-5 Building Disaster and Climate Resilient Cities in ASEAN Final Report Table A3-6 Long List Cities (No.311-No.372: “abc” city name order) Source: JICA Project Team NIPPON KOEI CO.,LTD. PAC ET C ORP. -

Downloaded 10/04/21 11:42 AM UTC 2800 MONTHLY WEATHER REVIEW VOLUME 146 Components (Reasor and Montgomery 2001)

SEPTEMBER 2018 S H I M A D A A N D H O R I N O U C H I 2799 Reintensification and Eyewall Formation in Strong Shear: A Case Study of Typhoon Noul (2015) UDAI SHIMADA Meteorological Research Institute, Tsukuba, Ibaraki, Japan TAKESHI HORINOUCHI Faculty of Environmental Earth Science, Hokkaido University, Sapporo, Hokkaido, Japan (Manuscript received 27 January 2018, in final form 9 July 2018) ABSTRACT Strong vertical wind shear produces asymmetries in the eyewall structure of a tropical cyclone (TC) and is generally a hostile environment for TC intensification. Typhoon Noul (2015), however, reintensified and 2 formed a closed eyewall despite 200–850-hPa vertical shear in excess of 11 m s 1. Noul’s reintensification and eyewall formation in strong shear were examined by using Doppler radar and surface observations. The evolution of the azimuthal-mean structure showed that the tangential wind at 2-km altitude increased from 30 2 to 45 m s 1 in only 5 h. During the first half of the reintensification, the azimuthal-mean inflow penetrated into the ;40-km radius, well inside the radius of maximum wind (RMW), at least below 4-km altitude, and re- flectivity inside the RMW increased. As for the asymmetric evolution, vigorous convection, dominated by an azimuthal wavenumber-1 asymmetry, occurred in the downshear-left quadrant when shear started to increase and then moved upshear. A mesovortex formed inside the convective asymmetry on the upshear side. The direction of vortex tilt between the 1- and 5-km altitudes rotated cyclonically from the downshear-left to the upshear-right quadrant as the vortex was vertically aligned. -

Typhoon Maysak

DREF Final Report Federated States of Micronesia: Typhoon Maysak DREF Operation no MDRFM001 Glide no TC-2015-000028-FSM Date of Issue: 26 February 2016 Date of disaster: 29 March 2015 Operation start date: 3 April 2015 Operation end date: 30 November 2015 Number of people assisted: 21,426 Operation budget: CHF 147,027 N° of National Societies involved in the operation: The Micronesia Red Cross Society has a total of seven staff members, four in its national office based in the capital, Pohnpei, and a Chapter Coordinator in each of its active chapters on Chuuk, Yap and Kosrae states. MRCS staff and 40 volunteers have been conducting assessments and distributing emergency relief supplies from their pre-positioned stock in each chapter and from the national office. Red Cross Red Crescent Movement partners actively involved in the operation: The National Society is working closely with the International Federation of Red Cross and Red Crescent Societies (IFRC) which is providing operational support and coordination with Partner National Societies (American Red Cross, Australian Red Cross and New Zealand Red Cross). Others agencies actively involved in the operation: National and local government departments, IOM, UN agencies, USAID/OFDA. A. Situation analysis Description of the disaster Typhoon Maysak formed from a tropical depression off Pohnpei State in the Federated States of Micronesia (FSM) which tracked west and intensified, making landfall in Chuuk lagoon on 29 March 2015 with damaging winds and torrential rainfall which also affected many of the outer islands. Maysak continued west making landfall again at Ulithi atoll in the north-west of Yap State on 1 April 2015. -

Tropical Cyclone Characterization Via Nocturnal Low-Light Visible Illumination

TROPICAL CYCLONE CHARACTERIZATION VIA NOCTURNAL LOW-LIGHT VISIBLE ILLUMINATION JEFFREY D. HAWKINS, JEREMY E. SOlbRIG, STEVEN D. MIllER, MELINDA SURRATT, THOMAS F. LEE, RICHARD L. BANKERT, AND KIM RICHARDSON Nighttime visible digital data from the Visible Infrared Imaging Radiometer Suite (VIIRS) have the potential to complement the current infrared imagery standard-bearer in monitoring global tropical cyclone characteristics. he Suomi National Polar-Orbiting Partnership (IR) passive radiometer, whose special ability to sense (SNPP) satellite was launched on 28 October 2011 extremely low levels of light in the 500–900-nm T and placed into a sun-synchronous afternoon bandpass provides a unique opportunity to exploit polar orbit (1330 local time ascending node with a nighttime visible signals for nighttime environmental corresponding nocturnal 0130 local time descending characterization (Lee et al. 2006; Miller et al. 2013). The node). SNPP carries a day–night band (DNB) sensor as improved capabilities hold potentially high relevance to part of the Visible Infrared Imaging Radiometer Suite the nocturnal monitoring and characterization of tropi- (VIIRS). The DNB is a visible (VIS)–near-infrared cal cyclones (TC) within the world’s oceanic basins. Accurately detecting TC structure (rainband organization, eyewall characterization, surface cir- a a culation center location, and intensity) in near–real AFFILIATIONS: HAWKINS, SURRATT, LEE, BANKERT, AND RICHARDSON—Naval Research Laboratory, Marine Meteorology time typically is problematic owing to 1) a scarcity Division, Monterey, California; SOlbRIG AND MIllER—Cooperative of in situ observations, 2) the spatial and temporal Institute for Research of the Atmosphere, Fort Collins, Colorado scales involved, and 3) the storm’s potential for rapid a Retired intensity (RI; >30 kt in 24 h; 1 kt = 0.51 m s–1) changes. -

Noul Makes Landfall in Philippines, Thousands Flee 11 May 2015

Noul makes landfall in Philippines, thousands flee 11 May 2015 Public storm warning signal #3 is raised in Batanes Public storm warning signal #2 is raised in Babuyan and Calayan Group of Islands Public storm warning signal #1 is raised in Northern Cagayan These images from the MODIS instrument on Terra show Noul's landfall in the Philippines followed by its movement toward Taiwan over the course of three days -- May 8-11, 2015. Credit: NASA Goddard MODIS Rapid Response Team On Sunday, May 10, 2015, Super Typhoon Noul (designated Dodong in the Philippines) made landfall in Santa Ana, a coastal town in Cagayan on the northeastern tip of the Philippine Islands. Close to 2,500 residents evacuated as the storm The RapidScat instrument on the International Space crossed over, and as of today no major damage or Station captured this image of Noul as it made landfall. injuries have been reported. Trees were downed Winds speed of up to 67 mph (30 m/s) were present at by the high winds and power outages occurred the time it hit the Philippine Islands. Credit: NASA JPL, during the storm. Noul is expected to weaken now Doug Tyler that it has made land, and to move faster as it rides strong surrounding winds. It is forecast to completely leave the Philippines by Tuesday morning and head toward southern Japan and Taiwan. Noul is curving northeast and will pass Provided by NASA's Goddard Space Flight Center over Okinawa, weakening as it transitions into an extra-tropical cyclone to the south of Japan. -

The Situation Information Bulletin Philippines: Typhoon Noul

Information bulletin Philippines: Typhoon Noul Information Bulletin n° 1 GLIDE n° 1 TC-2015-000051-PHL 10 May 2015 This bulletin is being issued for information only, and reflects the current situation and details available at this time. The Philippine Red Cross (PRC) has placed its disaster response teams on standby for rapid deployment and preparedness stocks ready for dispatch to areas where they may be needed but is not seeking funding or other assistance from donors at this time. The situation Typhoon Noul (locally known as Dodong) skirted the north-eastern tip of Luzon Island, Philippines, after making landfall over Pananapan Point, Santa Ana Municipality, in the province of Cagayan late afternoon Sunday 10 May 2015. The affected municipality has a population of some 30,500 people and is an economic and tourism destination of the province. According to the Philippine Atmospheric Geophysical and Astronomical Services Administration (PAGASA), the state weather bureau, at the time of landfall, the typhoon was packing maximum sustained winds of 185 kilometres per hour (kph) near its centre and gusts of up to 220 kph – equivalent of a Category 4 cyclone – and moving at a speed of about 20 kph. 1 Though Typhoon Noul is projected to weaken as it takes a north-northeast curve, and heads towards Taiwan and Japan, it will bring heavy to intense rainfall within its 100 kilometre diameter. Details on the exact impact of the typhoon, in the area where it made landfall, will emerge starting Monday morning, 11 May 2015. Nevertheless, some level of damage to houses, infrastructure and livelihoods can be expected.