Tanzania Mortgage Market Update – 31 December 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

China Export and Import Bank (China EXIM Bank) Issuance Notice Of

UNOFFICIAL TRANSLATION (OFFICIAL CHINESE GUIDELINES BELOW) China Export and Import Bank (China EXIM Bank) Issuance Notice of the “Guidelines for Environmental and Social Impact Assessments of the China Export and Import Bank’s (China EXIM Bank) Loan Projects" Guidelines for Environmental and Social Impact Assessments of the China Export and Import Bank’s (China EXIM Bank) Loan Projects General Principles Article 1. In order to implement the national strategies for sustainable development, promote economic, social and environmental development, and effectively control credit risks, the Guidelines were developed according to the "People's Republic of China’s Environmental Impact Assessment (EIA) Act," "People's Republic of China’s Environmental Protection Law", "Environmental Management for Construction Project Ordinance" and other relevant state laws and regulations, and with reference to the relevant regulations and procedures for the environmental and social assessments of international financial organizations. Article 2. These Guidelines apply to the loan procedure of China EXIM Bank. Article 3. The China EXIM Bank’s loan projects are classified as domestic or offshore projects, according to the area in which the projects are implemented. Domestic projects mean that the projects are implemented inside China with China EXIM Bank’s loan support. Offshore projects refer to the projects that are implemented outside China with China EXIM Bank’s loan support. Article 4. When China EXIM Bank reviews its loan projects, not only economic benefits, but also social benefits and environmental demands are considered. Article 5. Environmental assessment refers to the systematic analysis and evaluation of the environmental impacts and its related impacts on human health and safety due to the implementation of the projects. -

Financing Infrastructure in Tanzania

TOWARDS INDUSTRIALIZED ECONOMY: THE ROLE OF DFIs IN TANZANIA IN THE IMPLEMENTATION OF THE SECOND FIVE YEAR DEVELOPMENT PLAN. (FYDPII) Charles G Singili Ag. Managing Director TIB Development Bank 6 June 2017 Early Development Arena & the Notion of Development National Development Corporation was established in 1962 i. To catalyze economic development in all sectors of the economy; ii. NDC became a holding corporation under the Public Corporation Act 1969; iii. Had a broad mandate as a development and promotion institution to stimulate industrialization in partnership with private sector. Tanzania Investment Bank was established in 1970- i. To make available long and medium term finance for economic development ii. To provide technical assistance and advice for the purpose of promoting industrial development iii. To administer such funds as may from time to time be placed at the disposal of the Bank iv. To undertake such other activities as may be necessary or advantageous for the purpose of furthering the foregoing objects. Early Development Arena & the Notion of Development Tanzania Agricultural Development Bank was established in 2012 i. apex national-level bank with the key role of being a catalyst for delivery of short, medium and long- term credit facilities for development of agriculture in Tanzania ii. enshrined in the Vision 2025 to achieve food self-sufficiency and food security, economic development and poverty reduction Early Development Arena & the Notion of Development During establishment of the above SOEs “Economic Development” was defined as: i. The development of manufacturing, assembly and processing industries including industries engaged in the processing of products of agriculture, forestry or fishing; ii. -

Issn 0856 – 8537 Directorate of Banking

ISSN 0856 – 8537 DIRECTORATE OF BANKING SUPERVISION ANNUAL REPORT 2017 21ST EDITION For any enquiries contact: Directorate of Banking Supervision Bank of Tanzania 2 Mirambo Street 11884 Dar Es Salaam TANZANIA Tel: +255 22 223 5482/3 Fax: +255 22 223 4194 Website: www.bot.go.tz TABLE OF CONTENTS ....................................................................................................... Page LIST OF CHARTS ........................................................................................................................... iv ABBREVIATIONS AND ACRONYMS ............................................................................................ v MESSAGE FROM THE GOVERNOR ........................................................................................... vi FOREWORD BY THE DIRECTOR OF BANKING SUPERVISION .............................................. vii CHAPTER ONE .............................................................................................................................. 1 OVERVIEW OF THE BANKING SECTOR .................................................................................... 1 1.1 Banking Institutions ................................................................................................................. 1 1.2 Branch Network ....................................................................................................................... 1 1.3 Agent Banking ........................................................................................................................ -

Issued by the Britain-Tanzania Society No 112 Sept - Dec 2015

Tanzanian Affairs Issued by the Britain-Tanzania Society No 112 Sept - Dec 2015 ELECTION EDITION: MAGUFULI vs LOWASSA Profiles of Key Candidates Petroleum Bills Ruaha’s “Missing” Elephants ta112 - final.indd 1 8/25/2015 12:04:37 PM David Brewin: SURPRISING CHANGES ON THE POLITICAL SCENE As the elections approached, during the last two weeks of July and the first two weeks of August 2015, Tanzanians witnessed some very dra- matic changes on the political scene. Some sections of the media were even calling the events “Tanzania’s Tsunami!” President Kikwete addessing the CCM congress in Dodoma What happened? A summary 1. In July as all the political parties were having difficulty in choosing their candidates for the presidency, the ruling Chama cha Mapinduzi (CCM) party decided to steal a march on the others by bringing forward their own selection process and forcing the other parties to do the same. 2. It seemed as though almost everyone who is anyone wanted to become president. A total of no less than 42 CCM leaders, an unprec- edented number, registered their desire to be the party’s presidential candidate. They included former prime ministers and ministers and many other prominent CCM officials. 3. Meanwhile, members of the CCM hierarchy were gathering in cover photos: CCM presidential candidate, John Magufuli (left), and CHADEMA / UKAWA candidate, Edward Lowassa (right). ta112 - final.indd 2 8/25/2015 12:04:37 PM Surprising Changes on the Political Scene 3 Dodoma to begin the lengthy and highly competitive selection process. 4. The person who appeared to have the best chance of winning for the CCM was former Prime Minister Edward Lowassa MP, who was popular in the party and had been campaigning hard. -

A Case of Akiba Commercial Bank John

Adoption of mobile banking services by micro, small and medium enterprises in Tanzania: A Case of Akiba Commercial Bank John Leon Masters of Business Administration University of Dar es Salaam, Business School, 2017 Despite benefits of mobile banking technological advancement, customers running SMEs have continued to use traditional banking services characterized by long queues, long distance traveling and time wasting that negatively affect time allocated for other economic activities. This study aimed to assess the adoption of mobile banking services by SMEs in Tanzania using Akiba Commercial Bank as a case study. Out of 13 branches of Akiba Commercial Bank located in Dar es Salaam, 6 of them were selected randomly, where a random sample of 18 bank staff and 180 bank customers running SMEs in the respective branches were also selected to represent the study population. Questionnaires were administered to the randomly selected customers and purposive selected staff. It was found that, out of the interviewed 180 customers running SMEs at Akiba Commercial Bank, the majority of them (57.8%) had a positive perception on the use of the services. Out of them, 74.4% were aware of the existence of various mobile banking services, 17.8% of them were registered with mobile banking services but only 3.9% of the SMEs were using such services. Perceived risks of the banking services was a major reason (84.4%) for the non-use of the mobile banking services, followed by network problems (69.4%), transaction costs (49.7%), perceived complexity in using the services (43.9%), poor skills and knowledge in using the services (27.7%) and poor customer care of the bank (20.8%).Despite the fact that the majority of SMEs had a positive perception on the use of mobile banking services, the level of adoption of the services was very low. -

At Arusha Commercial Case No 3 of 2019 Crdb

IN THE HIGH COURT OF TANZANIA (COMMERCIAL DIVISION) AT ARUSHA COMMERCIAL CASE NO 3 OF 2019 CRDB BANK PLC.......................................................... PLAINTIFF Vs LAZARO SAMWEL NYALANDU................................... DEFENDANT RULING B.K. PHILLIP, 3 This ruling is in respect of the points of preliminary objection to wit; i. That, the suit is bad in law as it contravenes Order VII, Rule 1 (c) of the Civil Procedure Code, Chapter 33 R.E. 2019. ii. That the suit is bad in law as it contravenes Order VII, Rule 1 (c) of the Civil Procedure Code, Chapter 33 R.E. 2019 as amended by G.N No. 381 of 2019. iii. That, the suit is bad in law as it contravenes section 18 (a), (b)and (c) of the Civil Procedure Code, Chapter 33, R.E. 2019 The plaint reveals that this case emanates from a loan facility agreement signed between the parties herein, whereby the plaintiff granted to the defendant a loan to a tune of TZS 400,000,000/= The defendant offered his property located at Plot No. 9 & 10 Block "B", with CT No. 58063, LO No. 635518, Gomba Area, in Arumeru District, Arusha Region as security i for the loan. It is alleged in the plaint that the plaintiff defaulted the repayment of the loan. In this case the plaintiff prays for judgment and decree against the defendant as follows; i. An order for payment of the sum of Tshs. 304,795,267/= to the plaintiff by the defendant. ii. An order for payment of interest on the principal sum in prayers (i) above at the contractual rate of 14.5% from 16th August, 2019 to the date of Judgement. -

Peter Mapigano

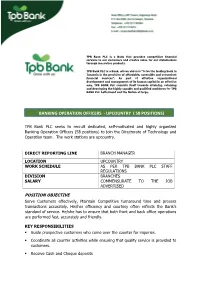

TPB Bank PLC is a Bank that provides competitive financial services to our customers and creates value for our stakeholders through innovative products. TPB Bank PLC is a Bank, whose vision is “to be the leading bank in Tanzania in the provision of affordable, accessible and convenient financial services”. As part of effective organizational development and management of its human capital in an effective way, TPB BANK PLC commits itself towards attaining, retaining and developing the highly capable and qualified workforce for TPB BANK PLC betterment and the Nation at large. BANKING OPERATION OFFICERS - UPCOUNTRY ( 58 POSITIONS) TPB Bank PLC seeks to recruit dedicated, self-motivated and highly organized Banking Operation Officers (58 positions) to join the Directorate of Technology and Operation team. The work stations are upcountry . DIRECT REPORTING LINE BRANCH MANAGER LOCATION UPCOUNTRY WORK SCHEDULE AS PER TPB BANK PLC STAFF REGULATIONS DIVISION BRANCHES SALARY COMMENSURATE TO THE JOB ADVERTISED POSITION OBJECTIVE Serve Customers effectively, Maintain Competitive turnaround time and process transactions accurately. His/her efficiency and courtesy often reflects the Bank’s standard of service. He/she has to ensure that both front and back office operations are performed fast, accurately and friendly. KEY RESPONSIBILITIES . Guide prospective customers who come over the counter for inquiries. Coordinate all counter activities while ensuring that quality service is provided to customers. Receive Cash and Cheque deposits . Posting Transactions . Verify teller proof of cash and teller proof of cheques against actual documents by ticking and signing the printouts. Scrutinize internal vouchers to ensure that they are properly drawn and authorized in line with the approval limits. -

Improving Life

Improving Life through inclusive finance 1 2 3 Preface Letshego Holdings Limited (“Letshego”) was incorporated in 1998, is headquartered in Gaborone and has been publicly listed on the Botswana Stock Exchange since 2002. Today it is one of Botswana’s largest indigenous groups, with a market capitalisation of approximately USD500mn, placing Contents it in the top 50 listed sub-Sahara African companies (ex-South Africa), with an agenda focused on inclusive finance. Through its eleven country presence across Southern, East and West Africa (Botswana, Ghana, Kenya, Lesotho, Mozambique, Namibia, Nigeria, Rwanda, Swaziland, Tanzania and Uganda), Preface 5 its subsidiaries provide simple, appropriate and accessible consumer and micro-finance banking solutions to the financially under-served in a sustainable manner. Letshego Group Structure 6 At Letshego, we are intent on operating a profitable business on a sustainable basis and we are committed to contributing to Our Business – Our Letshego 8 Africa’s growth and prosperity, as well as to improving the lives of our customers. Letshego’s vision is to become Africa’s leading inclusive finance group. Our inclusive finance solutions 9 In 2016, we have launched our customer engagement initiative, the Improving Life Campaign. For the duration of this campaign, we asked our customers to share their stories by telling us how Our history and milestones 10 they have used their loans productively. Prizes were awarded to the customers that had used their loans wisely, that is, generated income for their family while being able to service the loan and Our social impact 12 most of all, impacted society and left the community a better place than they had found it. -

The Kenya Power & Lighting Company Plc Half-Year Financial Statements 31

THE KENYA POWER & LIGHTING COMPANY PLC HALF-YEAR FINANCIAL STATEMENTS 31 DECEMBER 2020 THE KENYA POWER & LIGHTING COMPANY PLC FINANCIAL STATEMENTS FOR SIX MONTHS PERIOD ENDED 31 DECEMBER 2020 CONTENTS PAGES Report of the Directors 2 Statement of Comprehensive Income 3 Statement of Financial Position 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 Notes to the Financial Statements 7 - 22 1 THE KENYA POWER & LIGHTING COMPANY PLC REPORT OF THE DIRECTORS The Directors submit the unaudited interim financial statements for the six months’ period ended 31 December 2020 ACTIVITIES The core business of the Company continues to be the transmission, distribution and retail of electricity purchased in bulk from The Kenya Electricity Generating Company Limited (KenGen), Independent Power Producers (IPPs), Uganda Electricity Transmission Company (UETCL) and Tanzania Electric Supply Company Limited (TANESCO). RESULTS Shs’000 Profit before Taxation 332,658 Taxation charge (194,297) Profit for the Period 138,361 DIVIDENDS The Directors recommend no payment of interim dividend for the period. 2 THE KENYA POWER & LIGHTING COMPANY PLC STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE SIX MONTHS PERIOD ENDED 31 DECEMBER 2020 Note 31.12.2020 31.12.2019 Revenue Shs’ 000 Shs’ 000 Electricity Sales 2 (a) 61,497,156 61,241,134 Foreign Exchange adjustment 2 (a) 2,662,375 571,532 Fuel cost adjustment 2 (a) 4,855,056 7,793,993 69,014,587 69,606,659 Power Purchase Costs Non Fuel Power Purchase Costs 3 (a) (38,122,496) (37,190,151) Foreign -

India: an Ideal Partner in Tanzanian Agriculture?

Journal of Language, Technology & Entrepreneurship in Africa Vol. 4 No. 1 2013 India: An Ideal Partner in Tanzanian agriculture? Darlene K. Mutalemwa [email protected] Mzumbe University, Tanzania. Abstract The agricultural sector is the driving force of the Tanzanian economy. Therefore the need to develop and modernize it is of paramount importance for food production, poverty reduction and growth in other sectors. This paper aims at increasing knowledge and understanding of the contribution of India including its private companies, in Tanzanian agricultural investments, development and transformation. The paper concludes with some final remarks broadly stating that while Tanzania has enormous potential for attracting private investment in agriculture, there are serious constraints to India’s effective engagement in Tanzanian agriculture that include the need for improving the business environment, engaging the Indian Diaspora and increasing public expenditures on drivers of productivity. Key Words: Agriculture, India, Tanzania, Partner Introduction The Necessity for a Green Revolution In the opinion of the late President of Tanzania, J.K. Nyerere, Tanzania needs a Green revolution which has been the cornerstone of India’s agricultural achievement, transforming the country from one of food deficiency to self- sufficiency ( Tanzania National Business Council, 2009: ii): “Because of the importance of agriculture in our development, one would expect that agriculture and the needs of the agricultural producers would be the beginning, and the central reference point of all our economic planning. Instead, we have treated agriculture as if it was something peripheral, or just another activity in the country, to be treated at par with all the others, and used by the others without having any special claim upon them… We are neglecting agriculture. -

The United Republic of Tanzania the Economic Survey

THE UNITED REPUBLIC OF TANZANIA THE ECONOMIC SURVEY 2017 Produced by: Ministry of Finance and Planning DODOMA-TANZANIA July, 2018 Table of Contents ABBREVIATIONS AND ACRONYMS ......................................... xiii- xvii CHAPTER 1 ................................................................................................. 1 THE DOMESTIC ECONOMY .................................................................... 1 GDP Growth ............................................................................................. 1 Price Trends .............................................................................................. 7 Capital Formation ................................................................................... 35 CHAPTER 2 ............................................................................................... 37 MONEY AND FINANCIAL INSTITUTIONS ......................................... 37 Money Supply ......................................................................................... 37 The Trend of Credit to Central Government and Private Sector ............ 37 Banking Services .................................................................................... 38 Capital Markets and Securities Development ......................................... 37 Social Security Regulatory Authority (SSRA) ....................................... 39 National Social Security Fund (NSSF) ................................................... 40 GEPF Retirement Benefits Fund ........................................................... -

Annual Report 2019 East African Development Bank

Your partner in development ANNUAL REPORT 2019 EAST AFRICAN DEVELOPMENT BANK 2 2019 ANNUAL REPORT EAST AFRICAN DEVELOPMENT BANK EAST AFRICAN DEVELOPMENT BANK EAST AFRICAN DEVELOPMENT BANK ANNUAL REPORT 2019 3 2019 ANNUAL REPORT EAST AFRICAN DEVELOPMENT BANK CORPORATE PROFILE OF EADB Uganda (Headquarters) Plot 4 Nile Avenue EADB Building P. O. Box 7128 Kampala, Uganda Kenya Country office, Kenya 7th Floor, The Oval Office, Ring Road, Rwanda REGISTERED Parklands Westland Ground Floor, OFFICE AND P.O. Box 47685, Glory House Kacyiru PRINCIPAL PLACE Nairobi P.O. Box 6225, OF BUSINESS Kigali Rwanda Tanzania 349 Lugalo/ Urambo Street Upanga P.O. Box 9401 Dar es Salaam, Tanzania BANKERS Uganda (Headquarters) Standard Chartered –London Standard Chartered – New York Standard Chartered - Frankfurt Citibank – London Citibank – New York AUDITOR Standard Chartered – Kampala PricewaterhouseCoopers Stanbic – Kampala Certified Public Accountants, Citibank – Kampala 10th Floor Communications House, 1 Colville Street, Kenya P.O. Box 882 Standard Chartered Kampala, Uganda Rwanda Bank of Kigali Tanzania Standard Chartered 4 2019 ANNUAL REPORT EAST AFRICAN DEVELOPMENT BANK EAST AFRICAN DEVELOPMENT BANK ESTABLISHMENT The East African Development Bank (EADB) was established in 1967 SHAREHOLDING The shareholders of the EADB are Kenya, Uganda, Tanzania and Rwanda. Other shareholders include the African Development Bank (AfDB), the Netherlands Development Finance Company (FMO), German Investment and Development Company (DEG), SBIC-Africa Holdings, NCBA Bank Kenya, Nordea Bank of Sweden, Standard Chartered Bank, London, Barclays Bank Plc., London and Consortium of former Yugoslav Institutions. MISSION VISION OUR CORE To promote sustain- To be the partner of VALUES able socio-economic choice in promoting development in East sustainable socio-eco- Africa by providing nomic development.