Manhattan Hotel Market Overview 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

June 11, 2013 Shop Around the Clock by Jenny Cusack

June 11, 2013 Shop Around the Clock By Jenny Cusack New York City Ah, New York, the city that never sleeps. Where else can you visit the salon for an impromptu treatment in the middle of the night, and dine on worldly delights at 5am, and party straight through sunrise to lunch? With this 24-hour New York lifestyle in mind, the 1920s-era Mark Hotel has launched a new service: round-the-clock private shopping at Bergdorf Goodman. The five-star hotel in Manhattan's Upper East Side gives guests exclusive access to personal shopping at the luxury department store, round the corner on Fifth Avenue, at any time during their stay. The service will put an end to last-minute wardrobe malfunctions - such as forgotten dress shirts or heels through hems - which threaten to ruin big events or meetings. It's also a saving grace for those with precious little time for shopping (so much to do, so little time during the day), and for those who prefer to browse in blissful solitude. The new shopping service is available through The Mark's concierge who has direct access to perhaps one of the most covetable private shopping lines in the city: Bergdorf's director of personal shopping. And the store also has a team of Bergdorf personal shoppers with a client list of socialites and fashionistas, who can cater for styles from Uptown glamour to Downtown cool. The Mark Hotel, Madison Avenue at 77th Street, Manhattan, New York (00 1 212 744 4300; www.themarkhotel.com). Doubles from $650. -

To Download a PDF of an Interview with Izak Senbahar, Alexico Group

NEWNEW YORKYORK Building the Extraordinary An Interview with Izak Senbahar, Alexico Group LLC EDITORS’ NOTE Izak Senbahar but you were able to take it to an- affl uent travelers, be it for business or leisure, moved to the U.S. in 1977 to attend other level. How did you achieve is growing. A lot of emerging countries are do- The Catholic University of America that? ing very well and are creating more affluent in Washington, D.C. After graduat- There is a lot of work that goes travelers. The European visitors travel to the ing with a B.A. in mechanical en- into the planning. It doesn’t occur to U.S. routinely; however, the pool of interna- gineering, he moved to New York, me in one second. I analyze the site tional travelers from various other continents where he earned his master’s de- and the immediate vicinity. I walk is increasing greatly because of globalization. gree in finance from New York the neighborhood ad nauseam and I The Mark happens to be a landmark building University. Before he entered the dream about what I can create that in a fabulous location, and it has all of the right real estate market, Senbahar was a will add to life in the area. attributes to be at the top of the list of the af- Gold Trader for the French fi nan- When the start-to-finish on fl uent traveler. cial fi rm Sucre et Denrées. a project is so long, is it hard to be A visitor staying at The Mark, in a matter of Izak Senbahar patient in the early stages? a day or two, feels like living the life of a local COMPANY BRIEF Based in New York, One can control everything ex- Eastsider. -

Nyc & Company Unveils New York City's 2020 Holiday

*Information enclosed reflects a November 16 distribution; may be subject to change NYC & COMPANY UNVEILS NEW YORK CITY’S 2020 HOLIDAY PROGRAMMING NYC & Company is pleased to release 2020 holiday programming across the five boroughs. There’s never been a more important time to support local businesses during the holiday season, and there are multiple ways to do that through NYC & Company. Below are three ways to give the gift of New York City this year. New Yorkers and visitors can show support for NYC by masking up and taking an NYC-cation, staying overnight at one of the City’s welcoming hotels. NYC & Company’s most ambitious savings program ever—All In NYC: Neighborhood Getaways—offers nearly 300 deals across accommodations, attractions, dining, retail, tours and more, available at nycgo.com/neighborhoodgetaways. Those who register their Mastercard for the All In NYC: Neighborhood Getaways program—now including new offers through a unique holiday collection— can receive up to $100 total in statement credit when spending $100 or more at hotels and $20 or more at all other businesses. Those unable to visit are encouraged to Shop NYC this year, through purchases at nycgo.com/shopinnyc, including a roundup of e-commerce/gift cards, distinctive apparel and accessories, signature hotel items, museum gifts and memberships, food and gift baskets, souvenirs, books, music, games and more. Additionally, Virtual NYC experiences are available online for those from afar to enjoy NYC this festive season, including live stream presentations from Alvin Ailey American Dance Theater, Carnegie Hall, Cathedral of St. John the Divine, Lincoln Center and more, available at nycgo.com/virtualnyc, along with a special holiday collection. -

CORNELL CLUB, NYC By

GREAT HANGER STEAK AND GREAT HANGERS TOO THE CORNELL CLUB, NYC by Lew Toulmin SUMMARY We stayed at the Cornell Club of New York for four nights in early August 2010. The Club is about 200 yards west of Grand Central Station in a very good location. The public rooms are relatively modest but the bedrooms are excellent and more reasonably priced than most NYC reciprocal clubs. Rates for a twin room were $220 per night in the low summer season (a negotiated rate), including breakfast, rising to $302 in the fall. CLUB HISTORY AND FACILITIES The Club was founded in 1889 and rented rooms at the Royalton Hotel for a time. Subsequently the Club moved five times around Manhattan, arriving at the current location in 1985. A three year renovation of the existing building was required. The Club is in a 14 storey building at 6 East 44th Street, about a short block west of Grand Central Station, between Madison Avenue and Fifth Avenue. (Unfortunately, this station does not offer train service to and from Washington, DC. The Station is a landmark in itself, with a fruit, veg and meat market, restaurants, shops, great architecture, regular tours and access to the subway.) The Club library is very modest, consisting of a couple of walls of books. There are five function rooms, with square footage totaling 3500 square feet. These rooms are all right but not gorgeous, and in fact the bedrooms are definitely nicer than the public rooms, the reverse of the usual club situation. Other Club facilities include a moderate sized gym, about 50 x 50 feet with free weights, stationery bicycles, exercise balls and treadmills. -

Hotels Send Mixed Signals for 2017

Hotels Send Mixed Signals for 2017 hotel-online.com/press_releases/release/hotels-send-mixed-signals-for-2017 by Daniel Lesser NEW YORK CITY—To the surprise of many, the US lodging industry closed out 2016 with operating metrics still at record setting levels; however, its growth trajectory was notably lower when compared to years past. In general, occupancy levels have peaked and any short term RevPAR growth will be driven by increases to ADR. New supply of hotel rooms will continue to occur primarily in the Upper Midscale and Upscale chain scales. Of the nation’s top 25 markets, New York, Seattle, and Denver are experiencing double digit increases of new rooms under construction while eight other markets are currently slated for increases of five to eight percent of existing room supply. The LW Hospitality Advisors (LWHA) 2016 Major US Hotel Sales Survey includes 173 single asset sale transactions over $10 million, none of which are part of a portfolio. These transactions totaled roughly $12.7 billion, and included approximately 42,400 hotel rooms with an average sale price per room of $300,000. By comparison, the LWHA 2015 Major US Hotel Sales Survey identified 200 transactions totaling roughly $14.0 billion including 53,000 hotel rooms with an average sale price per room of nearly $265,000. Comparing 2016 with 2015, the number of trades decreased by 14 percent while total dollar volume declined roughly 9 percent and sales price per room increased by 13 percent. Interesting observations from the LWHA 2016 Major US Hotel Sales Survey include: -

Manhattan Year BA-NY H&R Original Purchaser Sold Address(Es)

Manhattan Year BA-NY H&R Original Purchaser Sold Address(es) Location Remains UN Plaza Hotel (Park Hyatt) 1981 1 UN Plaza Manhattan N Reader's Digest 1981 28 West 23rd Street Manhattan Y NYC Dept of General Services 1981 NYC West Manhattan * Summit Hotel 1981 51 & LEX Manhattan N Schieffelin and Company 1981 2 Park Avenue Manhattan Y Ernst and Company 1981 1 Battery Park Plaza Manhattan Y Reeves Brothers, Inc. 1981 104 W 40th Street Manhattan Y Alpine Hotel 1981 NYC West Manhattan * Care 1982 660 1st Ave. Manhattan Y Brooks Brothers 1982 1120 Ave of Amer. Manhattan Y Care 1982 660 1st Ave. Manhattan Y Sanwa Bank 1982 220 Park Avenue Manhattan Y City Miday Club 1982 140 Broadway Manhattan Y Royal Business Machines 1982 Manhattan Manhattan * Billboard Publications 1982 1515 Broadway Manhattan Y U.N. Development Program 1982 1 United Nations Plaza Manhattan N Population Council 1982 1 Dag Hammarskjold Plaza Manhattan Y Park Lane Hotel 1983 36 Central Park South Manhattan Y U.S. Trust Company 1983 770 Broadway Manhattan Y Ford Foundation 1983 320 43rd Street Manhattan Y The Shoreham 1983 33 W 52nd Street Manhattan Y MacMillen & Co 1983 Manhattan Manhattan * Solomon R Gugenheim 1983 1071 5th Avenue Manhattan * Museum American Bell (ATTIS) 1983 1 Penn Plaza, 2nd Floor Manhattan Y NYC Office of Prosecution 1983 80 Center Street, 6th Floor Manhattan Y Mc Hugh, Leonard & O'Connor 1983 Manhattan Manhattan * Keene Corporation 1983 757 3rd Avenue Manhattan Y Melhado, Flynn & Assocs. 1983 530 5th Avenue Manhattan Y Argentine Consulate 1983 12 W 56th Street Manhattan Y Carol Management 1983 122 E42nd St Manhattan Y Chemical Bank 1983 277 Park Avenue, 2nd Floor Manhattan Y Merrill Lynch 1983 55 Water Street, Floors 36 & 37 Manhattan Y WNET Channel 13 1983 356 W 58th Street Manhattan Y Hotel President (Best Western) 1983 234 W 48th Street Manhattan Y First Boston Corp 1983 5 World Trade Center Manhattan Y Ruffa & Hanover, P.C. -

EDC Will Restructure to Lobby Legally Fat Lady?

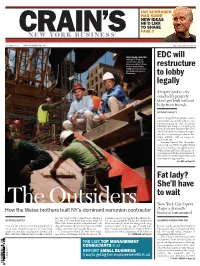

20120716-NEWS--0001-NAT-CCI-CN_-- 7/13/2012 7:12 PM Page 1 IAN SCHRAGER HAS SOME NEW IDEAS HE’D LIKE TO SHARE PAGE 3 CRAIN’S® NEW YORK BUSINESS VOL. XXVIII, NO. 29 WWW.CRAINSNEWYORK.COM JULY 16-22, 2012 PRICE: $3.00 WEISS WORK—AND THEY EDC will CAN GET IT: Flintlock Construction’s Andrew Weiss (crouching, left) and restructure brother Stephen Weiss (right) have nine 20-story- plus building projects in Manhattan. to lobby legally Despite probe, city concludes projects don’t get built without help from friends BY DANIEL MASSEY After its illegal lobbying led to a settle- ment earlier this month with the state attorney general, the city’s Economic Development Corp. is not giving up trying to influence legislative decisions surrounding land use.Quite the oppo- site: It is restructuring so that its lob- bying activities will no longer be against the law. Attorney General Eric Schneider- man found that EDC illegally lobbied the City Council to win approval of its Willets Point and Coney Island redevel- opment projects.It also played a behind- the-scenes role in the illegal lobbying of two nonprofit organizations. See EDC on Page 22 Fat lady? She’ll have to wait buck ennis The Outsiders New York City Opera How the Weiss brothers built NY’s dominant nonunion contractor stages a dramatic financial turnaround into the earth on West 42nd Street, digging a er might seem to be no big deal.But all three ho- BY DANIEL MASSEY hole for a 37-story hotel. Just to the south, on tels are being built by Flintlock Construction BY MIRIAM KREININ SOUCCAR West 30th Street, workers unloaded steel rods Services—and all three are being built using Last month, a boom truck lifted hundreds of that will reinforce the concrete structure of what nonunion labor. -

“It's Not What You Know, It's Who You Know.”

ADVERTISING SUPPLEMENT TO CRAIN’S NEW YORK BUSINESS Restaurants, Conference Centers Venues and Catering New York Area Hotels Florists Results Address: 583 Park Ave, New York, NY 10065 “It’s not what Past success is often a good indicator of future success, but Phone: (212) 583-7200 keep in mind, success comes in many forms such as rave Email: [email protected] reviews, savings on budget, flawless execution, or a myriad Website: www.583parkave.com you know, it’s of other key performance indicators. Pick the ones that are most important to you and asses their success ratio. AMA New York Executive Conference Center Affordable meeting packages. Meeting rooms can who you know.” Remember, for long-term resources it’s always a good accommodate over 200 attendees. Executive chairs. High- idea to refresh and reassess every two years! speed Internet access. Complimentary Wi-Fi in lounges. Complimentary continuous beverage service. Optional catering. owhere is the phrase truer than in corporate No service charges and no guest room commitment required. event planning. The success of your event is Free projector and PC use. Noften the direct result of a carefully orchestrated CONFERENCE CENTERS Address: 1601 Broadway at 48th Street, dance among a handful of select providers. However, New York, NY 10019 assembling a team of reliable event vendors does not 92nd Street Y Contact: Valerie Mazzilli-Brown happen overnight. Your dream team should be curated Give your special event the extraordinary and versatile venue Phone: (212) 903-8277 over many years. A good rule of thumb to use when it deserves at 92nd Street Y. -

2005 Manhattan Hotel Market Overview Page 1 of 22

HVS International : 2005 Manhattan Hotel Market Overview Page 1 of 22 Manhattan Hotel Market Overview HVS International, in cooperation with New York University’s Preston Robert Tisch Center for Hospitality, Tourism, and Sports Management, is pleased to present the eighth annual Manhattan Hotel Market Overview. In 2004, the Manhattan lodging market experienced an impressive recovery, with a RevPAR increase of 22% compared to 2003. From March through December of 2004, the market recorded double-digit growth in RevPAR each month, ranging from a high of 41% in April to a low of roundly 17% in October. At 83.2%, overall occupancy reached close to the historical peak achieved in 2000 (at 83.7%) while marketwide average rate was less than 10% below the 2000 level. Occupancy and average rate in 2005 should surpass 2000 levels. Due to limited new supply and increased compression resulting from near-maximum-capacity occupancy levels, overall RevPAR will experience double-digit growth for the next few years. Based on an overall improved economic climate, strong barriers to entry, limited new supply, and increased compression, we forecast the Manhattan lodging market to achieve a robust ±17% RevPAR growth in 2005. HVS International HVS International is a global consulting and services organization focused on the hotel, restaurant, timeshare, gaming, and leisure industries. Its clients rely on the firm’s specialized industry knowledge and expertise for advice and services geared to enhance economic returns and asset value. Through a network of 23 offices staffed by more than 200 seasoned industry professionals, HVS offers a wide scope of services that track the development/ownership process. -

Retail Mid-Q2 2019

Manhattan Retail Market MID-2ND QUARTER 2019 REPORT Pictured: 915 Broadway Shops & Restaurants at Hudson Yards Shops & Restaurants at Hudson Yards Makes its Far West Side Debut Opening day arrived on Friday, March 15th for the highly anticipated 7-story, 1 million-square-foot retail center within the multi-building Hudson Yards complex. Anchored by Neiman Marcus, which has made its New York City debut in the 3-story, 250,000-square-foot space the Dallas, TX-based high-end department store leased back in 2014, the vertical mall adds a wide variety of retailers and food offerings to the burgeoning Far West Side neighborhood. Developed by Related Companies and Oxford Properties Group, the retail component that straddles the 10 and 30 Hudson Yards offi ce towers sits along 10th Avenue between West 30th and 33rd Streets. About 90% leased at opening, there are 100 stores and 25 restaurants from fast-casual to fi ne dining spread throughout, with several of the restaurants operated by well-known chefs including the 35,000-square-foot Mercado Little Spain, a Spanish-themed foot court operated by chef José Andrés located in the base of 10 Hudson Yards; as well as the casual all-day restaurant Cedric’s at the Shed by Danny Meyer’s Union Square Hospitality Group that opened in April within the arts and culture venue. In addition the entire 2nd fl oor dubbed Floor of Discovery is an experimental concept that offers a mix of “fi rst locations for digitally native brands and experiential shopping offerings from modern brands;” while the permanent Snark Park exhibition space operated by design studio Snarkitecture will feature a rotating schedule of design environments and unique retail experiences. -

The Bloom Is on the Roses

20100426-NEWS--0001-NAT-CCI-CN_-- 4/23/2010 7:53 PM Page 1 INSIDE IT’S HAMMERED TOP STORIES TIME Journal v. Times: Story NY’s last great Page 3 Editorial newspaper war ® Page 10 PAGE 2 With prices down and confidence up, VOL. XXVI, NO. 17 WWW.CRAINSNEWYORK.COM APRIL 26-MAY 2, 2010 PRICE: $3.00 condo buyers pull out their wallets PAGE 2 The bloom is on the Roses Not bad for an 82-year-old, Adam Rose painted a picture of a Fabled real estate family getting tapped third-generation-led firm that is company that has come a surpris- for toughest property-management jobs known primarily as a residential de- ingly long way from its roots as a veloper. builder and owner of upscale apart- 1,230-unit project.That move came In a brutal real estate market, ment houses. BY AMANDA FUNG just weeks after Rose was brought in some of New York’s fabled real es- Today, Rose Associates derives as a consultant—and likely future tate families are surviving and some the bulk of its revenues from a broad just a month after Harlem’s River- manager—for another distressed are floundering, but few are blos- menu of offerings. It provides con- A tale of 2 eateries: ton Houses apartment complex was residential property, the vast soming like the Roses.In one of the sulting for other developers—in- taken over, owners officially tapped Stuyvesant Town/Peter Cooper Vil- few interviews they’ve granted,first cluding overseeing distressed prop- similar starts, very Rose Associates to manage the lage complex in lower Manhattan. -

The New Best of New York

THE NEW BEST OF NEW YORK Hotels Restaurants Corporate Neighbors Clubs 01. Algonquin Hotel 01. AJ Maxwell’s 20. Koi 01. Baker & McKenzie 21. Proskauer Rose 01. Century Club 02. Andaz 02. Ammos 21. Kuruma Zushi 02. Bank of America 22. Pryor Cashman 02. Columbia Club 03. Bryant Park Hotel 03. Asia de Cuba 22. La Fonda del Sol 03. Bates Worldwide 23. Reuters 03. Cornell Club 04. Courtyard by Marriott 04. At Vermilion 23. Le Marais 04. BDO Seidman 24. Royal Bank of 04. Dartmouth Club 05. Courtyard Fifth Avenue 05. Aureole 24. Metrazur 05. Calvin Klein Industries Scotland 05. Harvard Club 06. Dylan Hotel 06. Ben & Jack’s 25. Michael Jordan’s The 06. CIBC 25. Skadden, Arps, Slate, 06. New York Yacht Club 07. Grand Hyatt NY Steak House Steak House 07. CIT Group Meagher & Flom, LLP 07. Penn Club 08. Library Hotel 07. Benjamin Steak House 26. Morton’s The 08. Condé Nast 26. Time Inc. 08. Princeton Club 09. Marriott Marquis 08. Bobby Van’s Steakhouse 09. Cravath, Swaine & 27. UBS 09. Racquet & Tennis Club 10. Morgans Hotel Steakhouse 27. Oyster Bar Moore 28. US Bank 10. Union League 11. Royalton Hotel 09. Bond 28. Patroon 10. DE Shaw 29. Viacom 11. Yale Club 12. The Chatwal 10. Brasserie 29. Pera 11. Deloitte & Touche Retail 13. The Mansfield 11. Bryant Park Grill 30. Pershing Square 12. Ernst & Young 01. Alice + Olivia 14. The Setai 12. Café Centro 31. ReSette 13. Hachette Filipacchi 02. Banana Republic 15. The Strand Hotel 13. Capital Grille 32. Sparks Steak House 14.