A Regional Brand on a Global Mission

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Postcom Webinar:Is Saving for Their Funeral Killing the Postal Service?

Association for Postal Commerce "Representing those who use or support the use of mail for Business Communication and Commerce" "You will be able to enjoy only those postal rights you believe are worth defending." 1800 Diagonal Rd., Ste 320 * Alexandria, VA 22314-2862 * Ph.: +1 703 524 0096 * Fax: +1 703 997 2414 Postal News from January 2013 January 31, 2013 CNBC: The assertion that paper use automatically equals environmental damage is a tired argument and is no longer defensible. Marked improvement in paper and print manufacturing has redefined the impacts this industry has on the environment. Today's savvy consumers are not easily duped by unsubstantiated claims focused on vilifying an entire industry; particularly when those pointing the finger are positioned to reap monetary gain as a result. Politico: Rep. Stephen Lynch (D-Mass.) launched his Senate campaign Thursday with a shot at the Democratic establishment. oining Lynch were his parents, wife, daughter and five sisters. His mom spent 30 years as a member of the American Postal Workers Union. The Saint James Press: U.S. Senator Claire McCaskill, who last year led a successful fight that prevented the closure of hundreds of post offices in rural Missouri, continues her advocacy to protect postal services for Missourians. In a letter, McCaskill requested additional information from the Postmaster General about the Postal Service's claims that it would realize substantial savings by moving to a five-day delivery model-claims McCaskill questions. Bay of Plenty Times: Twenty-odd years ago I used to love the daily trip to the mailbox to see if there were any letters for me. -

DMM Advisory Keeping You Informed About Classification and Mailing Standards of the United States Postal Service

July 2, 2021 DMM Advisory Keeping you informed about classification and mailing standards of the United States Postal Service UPDATE 184: International Mail Service Updates Related to COVID-19 On July 2, 2021, the Postal Service received notifications from various postal operators regarding changes in international mail services due to the novel coronavirus (COVID-19). The following countries have provided updates to certain mail services: Mauritius UPDATE: Mauritius Post has advised that the Government of Mauritius has announced the easing of COVID-related restrictions as of July 1, 2021, subject to strict adherence to sanitary protocols and measures. On July 15, 2021, Mauritius will gradually open its international borders. However, COVID-19 continues to have a direct impact on international inbound and outbound mails to and from Mauritius. Therefore, the previously announced provisions and force majeure continue to apply for all inbound and outbound international letter-post, parcel-post and EMS items. New Zealand UPDATE: New Zealand Post has advised that the level-2 alert in the Wellington region has ended as of June 29, 2021. Panama UPDATE: Correos de Panama has advised that post offices, mail processing centers (domestic and international) and the air transhipment office at Tocúmen International Airport are operating under normal working hours and the biosafety measures established by the Ministry of Health of Panama (MINSA). Correos de Panamá confirms that it is able to continue to receive inbound mail destined for Panama. However, Correos de Panama is unable to guarantee service standards for inbound and outbound mail. As a result, force majeure with respect to quality of service for all categories of mail items will apply until further notice. -

DMM Advisory

August 13, 2020 DMM Advisory Keeping you informed about classification and mailing standards of the United States Postal Service International Service Impacts – Country Suspensions as of August 14, 2020 Effective August 14, 2020, the Postal Service will temporarily suspend international mail acceptance to destinations where transportation is unavailable due to widespread cancellations and restrictions into the area. Customers are asked to refrain from mailing items addressed to the following country, until further notice: • Syria This service disruption affects Priority Mail Express International® (PMEI), Priority Mail International® (PMI), First-Class Mail International® (FCMI), First-Class Package International Service® (FCPIS®), International Priority Airmail® (IPA®), International Surface Air Lift® (ISAL®), and M-Bag® items. Unless otherwise noted, service suspensions to a particular country do not affect delivery of military and diplomatic mail. For already deposited items, other than Global Express Guarantee® (GXG®), Postal Service International Service Center (ISC) employees will endorse the items as “Mail Service Suspended — Return to Sender” and then place them in the mail stream for return. Due to COVID-19, international shipping has been suspended to many countries. According to DMM 604.9.2.3, customers are entitled to a full refund of their postage costs when service to the country of destination is suspended. The detailed procedures to obtain refunds for Retail Postage, eVS, PC Postage, and BMEU entered mail can be found through -

Designated Postal Operators Authorized to Accept Equipment Containing Lithium Batteries (ECLB)

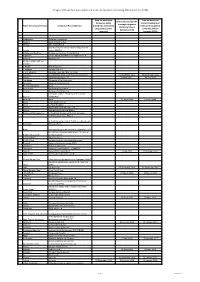

Designated Postal Operators authorized to accept equipment containing lithium batteries (ECLB) Date on which your Date on which you Date authorized by CAA dangerous goods started shipping mail to accept equipment Name Of Country/Territory Designated Postal Operator procedures and training items with equipment containing lithium programmes were containing lithium batteries (ECLB) approved batteries (ECLB) Afghanistan Postal administration Albania Posta Shqiptare sh.a. Algeria EPIC Algérie Poste Empresa Nacional de Correios e Telégrafos de Angola Angola (ENCTA) Antigua and Barbuda Antigua and Barbuda Postal Service Argentina Correo Oficial de la República Argentina S.A. Armenia Haypost CJSC Aruba, Curaçao and Sint Maarten – Aruba Post Aruba N.V. – Curaçao Nieuwe Post N.V. – Sint Maarten Postal Services Sint Maarten (PSS) Australia Australia Post (Australian Postal Corporation) 01 November 2012 11 November 2015 Austria Österreichische Post AG 04 July 2013 04 July 2013 Azerbaijan Entreprise d'Etat Azerpocht Bahamas Bahamas Postal Services Bahrain (Kingdom) None Bangladesh Bangladesh Post Office Barbados Barbados Postal Service Entreprise unitaire républicaine des postes Belarus "Belpochta" Belgium bPost 01 April 2014 01 April 2014 Belize Belize Postal Service Benin La Poste du Bénin Bhutan Bhutan Postal Corporation LTD Bolivia Empresa de Correos de Bolivia Bosnia and Herzegovina 1- The Public Entreprise BH Post, Sarajevo 2- The Croatian Post, Mostar 3- The Enterprise for Post Traffic a.d., Banja Luka Botswana BotswanaPost Brazil Empresa Brasileira de Correios e Telégrafos – ECT Brunei Postal Services Department, Ministry of Brunei Darussalam Communications Bulgaria (Rep.) Bulgarian Posts Burkina Faso Société nationale des postes (Sonapost) Burundi Régie nationale des postes (RNP) Cambodia Direction des postes Cameroon Cameron Postal Services – CAMPOST Canada Canada Post Corporation 11 July 2014 20 October 2014 Cape Verde Correios de Cabo Verde, S.A.R.L. -

DMM Advisory DMM Advisory DMM Advisory

April 28, 2020 DMM Advisory Keeping you informed about classification and mailing standards of the United States Postal Service UPDATE 30: International Mail Service Disruption Due to COVID-19 On April 28, 2020, the Postal Service received notification from CN Poșta Română SA, the designated operator for Romania, advising that the President of Romania has extended the state of emergency until May 14, 2020. Therefore, the previously declared force majeure remains in effect. Delays are to be expected for all types of inbound and outbound letter-post, parcel-post and EMS items until the end of the state of emergency. This service disruption affects Priority Mail Express International® (PMEI), Priority Mail International® (PMI), First-Class Mail International® (FCMI), First-Class Package International Service® (FCPIS®), International Priority Airmail® (IPA®), International Surface Air Lift® (ISAL®), and M-Bag® items. The DMM Advisory will continue to update mailers regarding new service disruptions as they are received. For a full list of international service disruptions, please visit https://about.usps.com/newsroom/service-alerts/international/welcome.htm The Domestic Mail Manual (DMM®) and DMM Advisories are available on Postal Explorer® (pe.usps.com) April 27, 2020 DMM Advisory Keeping you informed about classification and mailing standards of the United States Postal Service UPDATE 29: International Mail Service Disruptions Due to COVID-19 On April 27, 2020, the Postal Service received notifications from various postal operators regarding changes in international mail services due to the novel coronavirus (COVID-19). The following countries have suspended certain mail services: Nepal UPDATE: Nepal Post has advised that the suspension of all postal operations has been extended until May 15, 2020. -

DMM Advisory DMM Advisory DMM Advisory

April 23, 2020 DMM Advisory Keeping you informed about classification and mailing standards of the United States Postal Service International Service Impact: Alternate Transport – Air to Sea Diversion in Effect Effective April 20, 2020, the Postal Service™ will utilize sea transportation to address the issue of limited air transportation resulting from widespread flight cancellations and restrictions due to COVID-19. This option will remain in effect until sufficient air transportation capacity becomes available. The first sea transport departed from the JFK International Service Center on April 20, 2020, and is estimated to arrive at the Rotterdam (Netherlands) port on May 7, 2020. Sea route arrival dates are not exact and may vary depending on weather related events and queuing at port of arrival. The vessel is carrying 6,036 receptacles in 5 containers weighing 32,768 kilograms. It is serving mail destined to: • Austria • Denmark • Hungary • Poland • Sweden • Czech • Finland • Netherlands • Spain • Switzerland Republic When calculating estimated delivery times, additional days required for unloading, customs clearance and road transit should be considered. The table below outlines a typical sea transit delivery cycle that begins upon arrival to the destined port: Rotterdam Port Rotterdam Port Rotterdam Port Den Hague OE Den Hague OE Unloading Custom Clearance /Clear Transit to Den Hague OE Acceptance & Sorting Road Transit to Delivery Customs Address 1-2 Days 2 Days 1 Day 2-3 Days 1-4 Days OE – Office of Exchange This transportation alternative will be used for the following mail classes; Priority Mail Express International® (PMEI), Priority Mail International® (PMI), First-Class Mail International® (FCMI), First-Class Package International Service® (FCPIS®), International Priority Airmail® (IPA®), International Surface Air Lift® (ISAL®), and M-Bag® items. -

U N Iv E R S a L P O S T a L U N Io N

Entities responsible for fulfilling the obligations arising from adherence to the Acts of the Union. Position at 15 August 2021 Member country Government entity Operator designated to fulfil the Operator designated to fulfil the Independent regulator other than the obligations arising from adherence to obligations arising from the Postal government entity the UPU Convention Payment Services Agreement UPU U P U O Afghanistan Afghanistan Postal Regulatory Afghan Post State Enterprise Afghan Post State Enterprise None N N I S I Authority (APRA) O V T E N A R Albania Ministry of Infrastructure and Energy Posta Shqiptare sh.a. Electronic and Postal Communication L S Authority (AKEP) A L Algeria Ministère de la Poste, des EPIC Algérie Poste EPIC Algérie Poste Autorité de régulation des postes et Télécommunications, des des télécommunications (ARPT) Technologies et du Numérique Angola Ministerio das Telecomunicações e Empresa Nacional de Correios de Empresa Nacional de Correios de Instituto Angolano das Comunicações Tecnologias de Informaçāo Angola Angola (INACOM) Antigua and Barbuda Ministry of Finance and Corporate Antigua and Barbuda Postal Service None Governance Argentina Ministerio de Modernización Correo Oficial de la República Ministerio de Modernización Argentina S.A. Subsecretaría de Regulación Armenia Ministry of High-Tech Industry Société par actions fermée “Haypost” Société par actions fermée “Haypost” Public Services Regulation Commission Aruba, Curaçao and Sint Maarten – Aruba Ministry of Finance, Communication, Post Aruba N.V. -

Designated Postal Operators Authorized to Accept Equipment Containing Lithium Batteries (ECLB)

Designated Postal Operators authorized to accept equipment containing lithium batteries (ECLB) Date acceptance of mail Date authorized by CAA items comprised of to accept equipment equipment containing containing lithium lithium batteries (ECLB) batteries (ECLB) Name Of Country/Territory Designated Postal Operator began Afghanistan Postal administration Albania Posta Shqiptare sh.a. Algeria EPIC Algérie Poste Empresa Nacional de Correios e Telégrafos de Angola Angola (ENCTA) Antigua and Barbuda Antigua and Barbuda Postal Service Argentina Correo Oficial de la República Argentina S.A. Armenia Haypost CJSC Aruba, Curaçao and Sint Maarten – Aruba Post Aruba N.V. – Curaçao Nieuwe Post N.V. – Sint Maarten Postal Services Sint Maarten (PSS) Australia Australia Post (Australian Postal Corporation) 01 November 2012 11 November 2015 Austria Österreichische Post AG 04 July 2013 04 July 2013 Azerbaijan Entreprise d'Etat Azerpocht Bahamas Bahamas Postal Services Bahrain (Kingdom) None Bangladesh Bangladesh Post Office Barbados Barbados Postal Service Entreprise unitaire républicaine des postes Belarus "Belpochta" Belgium bPost 1 April 2014 1 April 2014 Belize Belize Postal Service Benin La Poste du Bénin Bhutan Bhutan Postal Corporation LTD Bolivia Empresa de Correos de Bolivia Bosnia and Herzegovina 1- The Public Entreprise BH Post, Sarajevo 2- The Croatian Post, Mostar 3- The Enterprise for Post Traffic a.d., Banja Luka Botswana BotswanaPost Brazil Empresa Brasileira de Correios e Telégrafos – ECT Brunei Postal Services Department, Ministry of Brunei Darussalam Communications Bulgaria (Rep.) Bulgarian Posts Burkina Faso Société nationale des postes (Sonapost) Burundi Régie nationale des postes (RNP) Cambodia Direction des postes Cameroon Cameron Postal Services – CAMPOST Canada Canada Post Corporation 11 July 2014 20 October 2014 Cape Verde Correios de Cabo Verde, S.A.R.L.