2006 Economic Background and 2007 Prospects

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prospectus E.Pdf

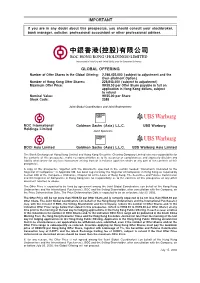

IMPORTANT If you are in any doubt about this prospectus, you should consult your stockbroker, bank manager, solicitor, professional accountant or other professional adviser. (Incorporated in Hong Kong with limited liability under the Companies Ordinance) GLOBAL OFFERING Number of Offer Shares in the Global Offering: 2,298,435,000 (subject to adjustment and the Over-allotment Option) Number of Hong Kong OÅer Shares: 229,843,500 (subject to adjustment) Maximum OÅer Price: HK$9.50 per OÅer Share payable in full on application in Hong Kong dollars, subject to refund Nominal Value: HK$5.00 per Share Stock Code: 2388 Joint Global Coordinators and Joint Bookrunners BOC International Goldman Sachs (Asia) L.L.C. UBS Warburg Holdings Limited Joint Sponsors BOCI Asia Limited Goldman Sachs (Asia) L.L.C. UBS Warburg Asia Limited The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. A copy of this prospectus, together with the documents speciÑed in the section headed ""Documents Delivered to the Registrar of Companies'' in Appendix VIII, has been registered by the Registrar of Companies in Hong Kong as required by Section 38D of the Companies Ordinance, Chapter 32 of the Laws of Hong Kong. The Securities and Futures Commission and the Registrar of Companies in Hong Kong take no responsibility as to the contents of this prospectus or any other document referred to above. -

Hong Kong SAR

Hong Kong SAR 104 Doing Business in Asia Pacific SEPTEMBER 2020 Chapter 1: Introduction 108 Chapter 2: Business environment 110 2.1 Hong Kong’s free economy 110 2.2 Gateway to mainland China 111 2.3 International outlook 112 2.4 Well-established legal and financial infrastructures 112 2.5 Favourable tax regime 113 Chapter 3: Business and corporate structures 114 3.1 Limited company 114 3.2 Unincorporated businesses 116 3.3 Forms of business collaboration 116 Chapter 4: Takeovers (friendly M&A) 117 4.1 Introduction 117 4.2 Hong Kong company law 118 4.3 Other common legal issues 118 4.4 Typical documentation 119 4.5 Due diligence 120 4.6 Sale and purchase agreement 120 Chapter 5: Foreign investment 122 5.1 Overview of Hong Kong’s business and investment environment 122 5.2 Restrictions on foreign investment 123 Chapter 6: Restructuring and insolvency 124 6.1 Legal framework 124 6.2 Liquidation 124 6.3 Restructuring 125 6.4 International insolvency 126 Doing Business in Asia Pacific SEPTEMBER 2020 105 Chapter 7: Employment, industrial relations, and work health and safety 127 7.1 Basic employment rights 127 7.2 Employment contract 128 7.3 Expatriates 129 7.4 Termination 129 7.5 Work health and safety 130 Chapter 8: Taxation 131 8.1 Outline 131 8.2 Profits tax 131 8.3 Salaries tax 133 8.4 Property tax 134 8.5 Stamp duty 134 8.6 Tax disputes 135 8.7 Anti-avoidance 135 Chapter 9: Intellectual property 135 9.1 Trademarks 136 9.2 Copyright 136 9.3 Registered designs 137 9.4 Patents 137 9.5 Confidential information 138 9.6 Private information 138 -

Techwatch No. 39

TechWatch is a publication designed to alert members to topics and issues that impact on CPAs and their working environment. We welcome your comments and feedback. Comments and suggestions on TechWatch should be addressed to Stephen Chan, Executive Director by email. ISSUE 39 • November/December 2005 HEADLINES Season’s Greetings from The Hong Kong Institute of Certified Public Accountants Wishing you a Merry Christmas and a Peaceful and Prosperous New Year 聖誕快樂 新年進步 Spotlight 1. Handbook Updates No. 22 & 23 CPD & Events 2. Technical Update Evening (TUE) 3. Professional Development Activities January And February 2006 4. New CPD Requirements Effective From 1 December 2005 International Submissions 5. IASB Submissions 6. IAASB Submission 7. International Ethics Standards Board Submission Financial Reporting 8. Amendments To Standards Arising From Companies (Amendment) Ordinance 2005 9. New Transitional Provisions In HKAS 16 And HKAS 40 10. Institute Issues Accounting Guideline 5 And Withdraws SSAP 27 11. Institute Invites Comments On Two IASB Discussion Papers 12. FRSC Meeting Summaries – 12 October and 9 November 2005 Audit & Assurance 13. Institute Invites Comments On IAASB ED Of Improving The Clarity Of IAASB Standards 14. Innovation And Technology Fund – Revised Example Report By Auditors 15. AASC Meeting Summary – 26 October 2005 HEADLINES Ethics 16. New Code Of Ethics For Professional Accountants Corporate Governance 17. Results Of The 2005 Best Corporate Governance Disclosure Awards Announced Banking 18. Example Disclosure Note On Regulatory Reserve 19. Commencement Of Banking (Amendment) Ordinance 2005 Insolvency & Corporate Restructuring 20. Institute Comments On Draft Subsidiary Legislation Under Bankruptcy (Amendment) Ordinance 2005 Taxation 21. Revenue (Abolition of Estate Duty) Ordinance 2005 Gazetted 22. -

Ejournal of Tax Research

eJournal of Tax Research Volume 11, Number 3 December 2013 Special Edition: 10th Anniversary Edition CONTENTS 245 Editorial announcement Binh Tran-Nam Introduction to the 10th anniversary issue of the eJournal of Tax 246 Research Binh Tran-Nam, C John Taylor 259 Buenas notches: lines and notches in tax system design Joel Slemrod 284 Designing tax policy: constraints and objectives in an open economy Richard M. Bird, J. Scott Wilkie 321 The European Union constitution and the development of tax policy Nigar Hashimzade and Gareth Myles Far east tax policy lessons: good and bad stories from Hong Kong 342 Richard Cullen Crossed lines: two cases of tax policy incoherence 375 Sheila Killian Conduit companies, beneficial ownership, and the test of substantive 386 business activity in claims for relief under double tax treaties Saurabh Jain, John Prebble, Kristina Bunting Too rich to rein in? The under-utilised wealth tax base 434 Natalia Chatalova and Chris Evans © School of Taxation and Business Law (Atax), Australian School of Business The University of New South Wales ISSN 1448-2398 eJournal of Tax Research (2013) vol. 11, no. 3, pp. 342 - 374 Far east tax policy lessons: good and bad stories from Hong Kong Richard Cullen1 Abstract Some claim that Hong Kong is a remarkable tax policy museum while others say it is a centre of tax policy innovation – who is right? In fact, both views are credible. In both cases, these outcomes are the product of a near continuous economic dialectic - and happenstance - set within a particularly relevant culture. Textbook policy planning has provided after-the-fact rationales far more than it has generated future policy blueprints. -

As an Executor of a Deceased Taxpayer

How should the executor report the income earned by a deceased taxpayer before death And rental income derived from the deceased’s properties Introduction According to section 54 of the Inland Revenue Ordinance (‘IRO’), the executor of a deceased taxpayer’s estate is obliged to handle the deceased’s tax affairs. Section 2 of the IRO defines ‘executor’ as any executor, administrator, or other person administering the estate of a deceased person, and includes a trustee acting under a trust created by the last will of the author of the trust. This leaflet will help executors and other persons gain a better understanding on: 1. the obligations of an executor under the IRO; 2. the specific areas that an executor has to attend to in handling the tax affairs of the deceased; 3. how to report to the Inland Revenue Department (IRD) : (a) income before death derived by the deceased taxpayer from - office, employment or pension - operating business (b) income from the letting of the deceased’s properties, both before and after death; and 4. the time limit for the Assessor to make assessments on the deceased taxpayer’s income. Obligations of an executor under the IRO As explained above, an executor of a deceased taxpayer is obliged to handle the tax affairs of the deceased taxpayer, including the submission of tax returns, supplying information and settlement of tax bills. If the deceased taxpayer had only salaries income or profits from a sole-proprietorship business, all that the executor is required to do is to report the relevant income earned before death in the deceased’s Tax Return - Individuals (BIR60). -

Estate Duty Review Consultation Document

ESTATE DUTY REVIEW CONSULTATION DOCUMENT FOREWORD In the 2004-05 Budget Speech, the Financial Secretary proposed that a review on estate duty should be conducted to examine whether we should adjust the current duty regime to attract more foreign capital. This consultation document highlights salient features of our estate duty system and invites your opinion on the review, with a view to enabling the Government to formulate proposals on estate duty for the 2005-06 Budget. Treasury Branch Financial Services and the Treasury Bureau Government Secretariat July 2004 2 Estate duty Estate duty is a form of capital tax which, in essence, is levied on the estate of a deceased person. It was first introduced in 1915 to generate revenue and to ‘enable the whole community to benefit upon the death of persons who had grown very rich partly through the appreciation in value of assets and the progress of Hong Kong to which the whole community contributed’. 2. Under the Estate Duty Ordinance, Cap.111 (EDO), estate duty shall be charged in respect of all property passing on the death of a person. Both movable and immovable properties are subject to estate duty. In line with the principle of territoriality, only property situated in Hong Kong at the time of death is subject to the tax. A number of exemptions are provided, as follows- (a) property passed on for charitable purposes in Hong Kong; (b) matrimonial home inherited by the surviving spouse of the deceased; (c) life insurance benefits; and (d) estate which has a value below a certain threshold (which is currently set at $7.5 million). -

CHAPTER 1 Inland Revenue Department Assessment and Collection of Estate Duty

CHAPTER 1 Inland Revenue Department Assessment and collection of estate duty The audit team consisted of: Audit Commission Hong Kong Philip LAU Sun-wo, Kenneth HO Jock-chu, and 18 October 2003 Adam CHAN Ming-yui under the direction of Peter CHAN Bar-keung ASSESSMENT AND COLLECTION OF ESTATE DUTY Contents Paragraphs SUMMARY PART 1: INTRODUCTION 1.1 Background 1.2 – 1.4 Audit review 1.5 PART 2: GRANTING OF CERTIFICATES OF 2.1 EXEMPTION FROM ESTATE DUTY EDO’s procedures for issuing estate duty clearance papers 2.2 – 2.6 Audit observations 2.7 – 2.9 Audit recommendations 2.10 Response from the Administration 2.11 – 2.12 PART 3: ASSESSMENT OF ESTATE DUTY 3.1 EDO’s procedures for assessing estate duty 3.2 – 3.5 Audit observations 3.6 – 3.17 Audit recommendations 3.18 Response from the Administration 3.19 – 3.20 PART 4: COLLECTION OF ESTATE DUTY 4.1 Requirements for the payment of estate duty 4.2 – 4.3 EDO’s procedures for recovering estate duty 4.4 — i — Paragraphs Audit observations 4.5 – 4.15 Audit recommendations 4.16 Response from the Administration 4.17 – 4.19 PART 5: RECOVERY OF EARNINGS AND PROFITS TAX 5.1 FROM THE ESTATES OF DECEASED TAXPAYERS IRD’s procedures for recovering earnings and 5.2 profits tax from the estates of deceased taxpayers Procedures used by the EDO to supply 5.3 estate information to the CES Audit observations 5.4 – 5.19 Audit recommendations 5.20 Response from the Administration 5.21 – 5.23 PART 6: ESTATE DUTY AVOIDANCE SCHEMES 6.1 Anti-avoidance provisions of the Estate Duty Ordinance 6.2 Anti-avoidance rules of the common law 6.3 Audit observations 6.4 – 6.11 Audit recommendations 6.12 Response from the Administration 6.13 – 6.14 Appendices A : 13 cases in which estate duty affidavit was received over 10 to 25 years ago but estate duty and interest were still outstanding as at 31 March 2003 B : 20 cases with earnings and profits tax written off during the period 2000-01 to 2002-03 or outstanding as at 31 March 2003 C : Acronyms and abbreviations — ii — ASSESSMENT AND COLLECTION OF ESTATE DUTY Summary 1. -

A Brief Guide to Taxes Administered by the Inland Revenue Department 2020 - 2021

INFORMATION PAMPHLET A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT 2020 - 2021 INLAND REVENUE DEPARTMENT THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE’S REPUBLIC OF CHINA A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT This pamphlet is issued for the general information of persons unfamiliar with the tax legislation in Hong Kong. Being a brief guide, it can only cover the subject very broadly. For further details, reference may be made to our website (www.ird.gov.hk) or the relevant legislation. Table of Contents Pages TAXATION IN HONG KONG 1 – 36 Profits Tax 1 – 8 The Scope of the Charge 1 – 2 The Basis of Assessment 2 Non-Residents and Agents dealing 2 – 3 with Non-Residents Exemptions and Deductions 3 – 5 Tax Incentives 5 – 6 Losses 6 Depreciation Allowances 7 Books and Records 8 Salaries Tax 9 – 17 The Scope of the Charge 9 The Basis of Assessment 9 – 10 Income of Married Couple 10 Deductions Allowed 10 – 13 Tax Rates 14 Tax Reduction 14 Examples 15 – 17 Pages Property Tax 18 The Scope of the Charge 18 The Basis of Assessment 18 Properties for Owner’s Business Use 18 Allowances 18 – 22 Personal Assessment 23 – 25 Obligations of Taxpayers (Salaries, Profits and Property Tax) 26 under the Inland Revenue Ordinance Obligations of Employers under the Inland Revenue Ordinance 27 – 28 Completion of Tax Return 28 Approved Charitable Donations 28 Double Taxation Relief and 28 – 29 Exchange of Information Arrangements Collection of Taxes 29 – 30 MISCELLANEOUS LEVIES 31 – 35 Stamp Duty 31 – 32 Estate Duty 33 Betting Duty 33 Business Registration 33 – 34 Hotel Accommodation Tax 35 EVASION OF TAX - A CRIMINAL OFFENCE 35 Consequence of Filing Incorrect Return 35 ADVANCE RULINGS 35 FURTHER INFORMATION 36 INFORMATION PAMPHLET TAXATION IN HONG KONG The Inland Revenue Ordinance (Chapter 112) (IRO) provides for the levying of three separate direct taxes for a year of assessment which ends on 31 March. -

OFFICIAL REPORT of PROCEEDINGS Wednesday, 25

HONG KONG LEGISLATIVE COUNCIL―25 November 1981 197 OFFICIAL REPORT OF PROCEEDINGS Wednesday, 25 November 1981 The Council met at half past two o’clock PRESENT HIS EXCELLENCY THE GOVERNOR (PRESIDENT) SIR CRAWFORD MURRAY MACLEHOSE, G.B.E., K.C.M.G., K.C.V.O. THE HONOURABLE THE CHIEF SECRETARY SIR CHARLES PHILIP HADDON-CAVE, K.B.E., C.M.G., J.P. THE HONOURABLE THE FINANCIAL SECRETARY MR. JOHN HENRY BREMRIDGE, O.B.E. THE HONOURABLE THE ATTORNEY GENERAL MR. JOHN CALVERT GRIFFITHS, Q.C. THE HONOURABLE THE SECRETARY FOR HOME AFFAIRS MR. DENIS CAMPBELL BRAY, C.M.G., C.V.O., J.P. THE HONOURABLE DAVID AKERS-JONES, C.M.G., J.P. SECRETARY FOR THE NEW TERRITORIES THE HONOURABLE LEWIS MERVYN DAVIES, C.M.G., O.B.E., J.P. SECRETARY FOR SECURITY THE HONOURABLE DAVID WYLIE MCDONALD, C.M.G., J.P. SECRETARY FOR LANDS AND WORKS THE HONOURABLE DAVID GREGORY JEAFFRESON, C.B.E., J.P. SECRETARY FOR ECONOMIC SERVICES THE HONOURABLE ALAN JAMES SCOTT, J.P. SECRETARY FOR INFORMATION DR. THE HONOURABLE THONG KAH-LEONG, C.B.E., J.P. DIRECTOR OF MEDICAL AND HEALTH SERVICES THE HONOURABLE ERIC PETER HO, C.B.E., J.P. SECRETARY FOR SOCIAL SERVICES THE HONOURABLE JOHN MARTIN ROWLANDS, C.B.E., J.P. SECRETARY FOR THE CIVIL SERVICE THE HONOURABLE JAMES NEIL HENDERSON, J.P. COMMISSIONER FOR LABOUR THE HONOURABLE GERALD PAUL NAZARETH, O.B.E., Q.C. LAW DRAFTSMAN THE HONOURABLE WILLIAM DORWARD, O.B.E., J.P. DIRECTOR OF TRADE, INDUSTRY AND CUSTOMS THE HONOURABLE JOHN MORRISON RIDDELL-SWAN, O.B.E., J.P. -

Schedule 10 A5351 Part 1 Ord

Companies Ordinance Schedule 10 A5351 Part 1 Ord. No. 28 of 2012 Schedule 10 [ss. 912 & 920] Consequential and Related Amendments to Other Ordinances and Subsidiary Legislation Part 1 Amendment to Interpretation and General Clauses Ordinance (Cap. 1) 1. Section 88 amended (Provisions supplementary to section 84) Section 88(3)(a)— Repeal “(Cap. 32)” Substitute “(28 of 2012)”. Part 2 Amendment to Specification of Public Officers (Cap. 1 sub. leg. C) 2. Schedule amended The Schedule, the first and second entries relating to the Financial Secretary— Repeal the entries. Companies Ordinance Schedule 10 A5353 Part 3 Ord. No. 28 of 2012 Part 3 Amendment to High Court Ordinance (Cap. 4) 3. Section 21D amended (Sale of property in execution of judgment) Section 21D(1)— Repeal “section 29 of the Companies Ordinance (Cap. 32)” Substitute “section 11 of the Companies Ordinance (28 of 2012)”. Part 4 Amendments to The Rules of the High Court (Cap. 4 sub. leg. A) 4. Order 1 amended (Citation, application, interpretation and forms) (1) Order 1, rule 2(2), Table, item 2, under heading “Enactments”— Repeal “Companies Ordinance” Substitute “Companies (Winding Up and Miscellaneous Provisions) Ordinance”. (2) Order 1, rule 2(2), Table, after item 2— Add Companies Ordinance Schedule 10 A5355 Part 4 Ord. No. 28 of 2012 “2A. Proceedings relating to Companies Ordinance remedies for unfair (28 of 2012), section prejudice to members’ 727.”. interests. 5. Order 102 amended (The Companies Ordinance) (1) Order 102, heading— Repeal “THE COMPANIES ORDINANCE” Substitute “THE COMPANIES ORDINANCE AND THE COMPANIES (WINDING UP AND MISCELLANEOUS PROVISIONS) ORDINANCE”. (2) Order 102— Repeal rule 1. -

128 Calendar of Events of Significance for the Hong Kong

Calendar of Events of Significance for the Hong Kong Economy in 2006 1 Jan The third phase of Closer Economic Partnership Arrangement (CEPA) between the Mainland and Hong Kong came into effect. All products of Hong Kong origin could enter the Mainland tariff free, upon the CEPA rules of origin being agreed and met. 262 additional products were added to the list of goods with CEPA rules of origin, making a total of 1 370. Moreover, Hong Kong service suppliers enjoyed preferential access to the Mainland market in 27 service areas. The Mainland continued to reduce its import tariffs on more than 100 items in line with the World Trade Organization (WTO) commitments. The average import tariff rate was 9.9% in 2006. After this round of tariff reduction, the Mainland basically fulfilled its tariff reduction commitments under the WTO. The Mainland ceased levying export duty on textile exports. 3 Jan The People’s Bank of China (PBOC) announced further measures to improve the managed float exchange rate regime and promote development of the foreign exchange market in the Mainland. Among other measures, over-the-counter transactions were introduced in the inter-bank spot foreign exchange market on 4 January. 4 Jan The Heritage Foundation and the Wall Street Journal released the 2006 Index of Economic Freedom. Hong Kong was rated the freest economy in the world for the 12th straight year, followed by Singapore and Ireland. 6 Jan The Office of the Telecommunications Authority (OFTA) introduced a new Services-Based Operator (SBO) Licence for the provision of Internet Protocol (IP) Telephony services. -

DIPN 23(Revised)

Inland Revenue Department The Government of the Hong Kong Special Administrative Region of the People's Republic of China DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 23 (REVISED) RECOGNIZED RETIREMENT SCHEMES These notes are issued for the information of taxpayers and their tax representatives. They contain the Department’s interpretation and practices in relation to the laws as it stood at the date of publication. Taxpayers are reminded that their right of objection against the assessment and their right of appeal to the Commissioner, the Board of Review or the Court are not affected by the application of these notes. These notes replace those issued in September 2006. WONG Kuen-fai Commissioner of Inland Revenue May 2019 Our web site : www.ird.gov.hk DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES No. 23 (REVISED) CONTENT Paragraph Introduction Regulatory frameworks on retirement schemes 1 Different retirement schemes Approved retirement schemes 4 Recognized occupational retirement schemes 5 Mandatory provident fund schemes 7 Recognized retirement schemes 8 Important definitions and concepts Distinction between “retirement” and “termination of service” 12 Contributions to MPF schemes 13 - Mandatory contributions 14 - Voluntary contributions 17 - Tax deductible MPF voluntary contributions 18 Assessability of sums received by employees Amounts attracting salaries tax liability 23 Summary of the position 25 Proportionate benefit 28 - Accrued benefit 29 - Completed months of service 33 - Illustrative examples 35 Withdrawal of MPF