GEOLOGIC STUDY of SAND DEPOSITS in the STATE of MICHIGAN

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Articles of Precious Metals in Finland

1 Articles of precious metals in Finland guidebook Manufacture, import and sale jalometallituotteet – valmistus, maahantuonti ja myynti 2 Text: Tukes Photographs: Lauri Mannermaa, Pixhill (p.21) publication data Layout: Print Line Helsinki Oy, 2016 ISBN 978-952-5649-84-0 What are articles of precious metals? 4 Mutual Recognition and the Houtwipper Case 13 Requirements for articles on sale 5 International markings in a nutshell 14 Technical requirements 6 Lightweight articles without hallmarking 14 Finenesses and solders 6 Articles without hallmarking Fillings, glue and solder 6 exceeding weight limits for marking 14 Coatings 6 Assay offices 15 Articles with several precious metals Manufacture and import of articles or other materials 6 of precious metals 16 Nickel, cadmium and lead in jewellery 7 Sale of articles of precious metals 17 Marks on articles of precious metals 8 Internet trading 17 contents Marking 8 Weighing instruments used in trade 18 Weight limits of Marking 8 Applying for a responsibility mark 19 Mandatory Marks 8 Finnish Safety and Chemicals Agency (Tukes) 20 Voluntary marks 10 Surveillance of articles of precious metals Other marks and markings 10 in Finland 21 Replacing marks with a certificate 11 Further information 22 Products outside the scope of the legislation 11 Key to date marks in Finland 23 The Vienna Convention 12 finnish safety and chemicals agency (tukes) Introduction 3 Jewellery and other products made of precious metals Nowadays, EU legislation and principles are binding and have been a part of Finnish tradition since time immemo- have to be followed, but there are no harmonized require- rial. The assaying of articles of precious metals began in ments or legislation for articles of precious metals in the the Middle Ages, with the authorities starting to supervise European Union. -

INFORMATION BULLETIN #50 SALES TAX JULY 2017 (Replaces Information Bulletin #50 Dated July 2016) Effective Date: July 1, 2016 (Retroactive)

INFORMATION BULLETIN #50 SALES TAX JULY 2017 (Replaces Information Bulletin #50 dated July 2016) Effective Date: July 1, 2016 (Retroactive) SUBJECT: Sales of Coins, Bullion, or Legal Tender REFERENCE: IC 6-2.5-3-5; IC 6-2.5-4-1; 45 IAC 2.2-4-1; IC 6-2.5-5-47 DISCLAIMER: Information bulletins are intended to provide nontechnical assistance to the general public. Every attempt is made to provide information that is consistent with the appropriate statutes, rules, and court decisions. Any information that is inconsistent with the law, regulations, or court decisions is not binding on the department or the taxpayer. Therefore, the information provided herein should serve only as a foundation for further investigation and study of the current law and procedures related to the subject matter covered herein. SUMMARY OF CHANGES Other than nonsubstantive, technical changes, this bulletin is revised to clarify that sales tax exemption for certain coins, bullion, or legal tender applies to coins, bullion, or legal tender that would be allowable investments in individual retirement accounts or individually-directed accounts, even if such coins, bullion, or legal tender was not actually held in such accounts. INTRODUCTION In general, an excise tax known as the state gross retail (“sales”) tax is imposed on sales of tangible personal property made in Indiana. However, transactions involving the sale of or the lease or rental of storage for certain coins, bullion, or legal tender are exempt from sales tax. Transactions involving the sale of coins or bullion are exempt from sales tax if the coins or bullion are permitted investments by an individual retirement account (“IRA”) or by an individually-directed account (“IDA”) under 26 U.S.C. -

Methods for Determining the Gold Content of Jewelry Metals

By Meredit11 E. Mercer Verifying the gold content of karat-gold jew- n jewelry! the integrity of the metal is as impoitant as the elry is a problem for the entire industry. This identity and integrity of the gemstones (&re 1).The mis- st~~dycompares four widely available testing representation of gold content (l'underlzaratingll)has been a methods: de~~sity(measured by hydrostatic source of concern at all levels of the industry for literally hun- weighing),chemical reactivily (toz~chstone dreds of years. For the protection of retailers and consumers testing), capocilive decay (Tri-Electronics alilze) a testing method that can verify the gold content of fin- G-XL-18Gold Tesler),and X-ray fl~~oracence ished jewelry at point of sale is needed. Ideallyl this method (Seiko Ins~rumentsSEA 2001 Iewehy Assay System). The latter thee methods all proved would be rapid! simple! reliable! inexpensive! nondestructivel ~isefulw'thn certain limitations; hydrostatic and widely accepted by the jewelry industry. The study report- weighing was least szljtable. None of these ed here was conducted to determine whether existing methods methods reliobly determined gold conteni co~~ldmeet these requirements. Four testing methods cur- within the 3-ppt toler~znceallowed by U.S. rently used in the trade-density! che~nicalreactivityl capac- pl~zn?b laws. itive decay! and X-ray fluorescence-were applied to the same set of well-characterized reference standards and the results compared. Gold-testing methods SLIC~Ias fire assay! touchstone test- ing) and l~ydrostaticweighing have been used since antiquity. Tests for plated material include c~~tting)heating! and ringing (Oddy! 1983; Revere! 1990).Much worlz has been done on the development of analyses to detect very sn~allquantities of gold for mining (Yoq1980). -

Hallmarking Guidance Notes

HALLMARKING GUIDANCE NOTES PRACTICAL GUIDANCE IN RELATION TO THE HALLMARKING ACT 1973 INFORMATION FROM THE ASSAY OFFICES OF GREAT BRITAIN OCTOBER 2016 London Edinburgh Birmingham Sheffield Guaranteeing The Quality Of Precious Metals Since 1327 HALLMARKING GUIDANCE NOTES HALLMARKING GUIDANCE NOTES THE PURPOSE OF THESE HALLMARKING PRECIOUS METALS GUIDANCE NOTES WHY ARE PRECIOUS METAL ARTICLES The purpose of these notes is to give practical guidance in relation to the HALLMARKED? Hallmarking Act 1973 and subsequent amendments. No reliance must be placed on the document for a legal interpretation. The UK Assay Offices are happy to Silver, palladium, gold and platinum are rarely used in their purest form but answer questions arising from these guidance notes and on any articles or other instead they are normally alloyed with lesser metals in order to achieve a issues not specifically mentioned. desired strength, durability, colour etc. It is not possible to detect by sight or by touch the gold, silver, platinum or palladium content of an item. It is therefore a legal requirement to hallmark CONTENTS OF THIS BOOKLET: all articles consisting of silver, palladium, gold or platinum (subject to certain exemptions) if they are to be described as such. Contents Page The main offence under the UK Hallmarking Act 1973 is based on description. It is Hallmarking precious metals 3 - 17 an offence for any person in the course of trade or business to: Guidance on describing precious metals 18 - 19 • Describe an un-hallmarked article as being wholly or partly made of silver, palladium, gold or platinum. Contact details for UK Assay Offices Back Page • Supply or offer to supply un-hallmarked articles to which such a description is applied. -

EUROPEAN PHARMACOPOEIA Free Access to Supportive Pharmacopoeial Texts in the Field of Vaccines for Human Use During the Coronavirus Disease (COVID-19) Pandemic

EUROPEAN PHARMACOPOEIA Free access to supportive pharmacopoeial texts in the field of vaccines for human use during the coronavirus disease (COVID-19) pandemic Updated package - October 2020 Published in accordance with the Convention on the Elaboration of a European Pharmacopoeia (European Treaty Series No. 50) European Directorate Direction européenne for the Quality de la qualité of Medicines du médicament & HealthCare & soins de santé Council of Europe Strasbourg Free access to supportive pharmacopoeial texts in the field of vaccines for human use during the coronavirus disease (COVID-19) pandemic Updated package The EDQM is committed to supporting users during the coronavirus disease (COVID-19) pandemic – as well as contributing to the wider global effort to combat the virus – by openly sharing knowledge and providing access to relevant guidance/standards. To support organisations involved in the development, manufacture or testing of COVID-19 vaccines worldwide, many of which are universities and small and medium-sized enterprises, the EDQM is offeringte mporary free access to texts of the European Pharmacopoeia (Ph. Eur.) in the field of vaccines. This package includes quality standards for vaccines which developers can take into account to help build appropriate analytical control strategies for their COVID-19 candidate vaccines and ensure the quality and safety of the final product. Application of such quality requirements may ultimately help to facilitate regulatory acceptance of a subsequent marketing authorisation application. For ease of reading, a summary table listing the pharmacopoeial texts, with information regarding the vaccine types or vaccine platforms concerned (e.g. live attenuated viral vaccine, recombinant viral-vectored vaccines) is provided. -

THE WORLD of COINS an Introduction to Numismatics

THE WORLD OF COINS An Introduction to Numismatics Jeff Garrett Table of Contents The World of Coins .................................................... Page 1 The Many Ways to Collect Coins .............................. Page 4 Series Collecting ........................................................ Page 6 Type Collecting .......................................................... Page 8 U.S. Proof Sets and Mint Sets .................................... Page 10 Commemorative Coins .............................................. Page 16 Colonial Coins ........................................................... Page 20 Pioneer Gold Coins .................................................... Page 22 Pattern Coins .............................................................. Page 24 Modern Coins (Including Proofs) .............................. Page 26 Silver Eagles .............................................................. Page 28 Ancient Coins ............................................................. Page 30 World Coins ............................................................... Page 32 Currency ..................................................................... Page 34 Pedigree and Provenance ........................................... Page 40 The Rewards and Risks of Collecting Coins ............. Page 44 The Importance of Authenticity and Grade ............... Page 46 National Numismatic Collection ................................ Page 50 Conclusion ................................................................. Page -

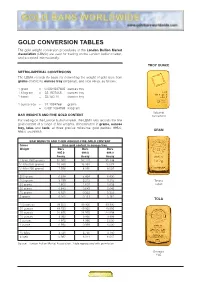

Gold Conversion Tables

GOLD CONVERSION TABLES The gold weight conversion procedures of the London Bullion Market Association (LBMA) are used for trading on the London bullion market, and accepted internationally. TROY OUNCE METRIC-IMPERIAL CONVERSIONS The LBMA records its basis for converting the weight of gold bars from grams (metric) to ounces troy (imperial), and vice versa, as follows: 1 gram = 0.0321507465 ounces troy 1 kilogram = 32.1507465 ounces troy 1 tonne = 32,150.70 ounces troy 1 ounce troy = 31.1034768 grams = 0.0311034768 kilogram Valcambi BAR WEIGHTS AND FINE GOLD CONTENT Switzerland For trading on the London bullion market, the LBMA also records the fine gold content of a range of bar weights, denominated in grams, ounces troy, tolas and taels, at three precise millesimal gold purities: 995.0, GRAM 999.0 and 999.9. BAR WEIGHTS AND THEIR AGREED FINE GOLD CONTENT Gross Fine gold content in ounces troy Weight Bars Bars Bars 995.0 999.0 999.9 Assay Assay Assay 1 kilo (1000 grams) 31.990 32.119 32.148 1/2 kilo (500 grams) 15.995 16.059 16.074 1/4 kilo (250 grams) 7.998 8.030 8.037 200 grams 6.398 6.424 6.430 100 grams 3.199 3.212 3.215 Tanaka 50 grams 1.600 1.607 1.608 Japan 20 grams 0.640 0.643 0.643 10 grams 0.321 0.322 0.322 5 grams 0.161 0.161 0.161 TOLA 100 ounces 99.500 99.900 99.990 50 ounces 49.750 49.950 49.995 25 ounces 24.875 24.975 24.998 10 ounces 9.950 9.990 9.999 5 ounces 4.975 4.995 5.000 1 ounce 0.995 0.999 1.000 10 tolas 3.731 3.746 3.750 5 taels 5.987 6.011 6.017 Source: London Bullion Market Association. -

Hallmarking Guidance Notes

HALLMARKING GUIDANCE NOTES PRACTICAL GUIDANCE IN RELATION TO THE HALLMARKING ACT 1973 INFORMATION FROM THE ASSAY OFFICES OF GREAT BRITAIN OCTOBER 2016 London Edinburgh Birmingham Sheffield Guaranteeing The Quality Of Precious Metals Since 1327 HALLMARKING GUIDANCE NOTES HALLMARKING GUIDANCE NOTES THE PURPOSE OF THESE HALLMARKING PRECIOUS METALS GUIDANCE NOTES WHY ARE PRECIOUS METAL ARTICLES The purpose of these notes is to give practical guidance in relation to the HALLMARKED? Hallmarking Act 1973 and subsequent amendments. No reliance must be placed on the document for a legal interpretation. The UK Assay Offices are happy to Silver, palladium, gold and platinum are rarely used in their purest form but answer questions arising from these guidance notes and on any articles or other instead they are normally alloyed with lesser metals in order to achieve a issues not specifically mentioned. desired strength, durability, colour etc. It is not possible to detect by sight or by touch the gold, silver, platinum or palladium content of an item. It is therefore a legal requirement to hallmark CONTENTS OF THIS BOOKLET: all articles consisting of silver, palladium, gold or platinum (subject to certain exemptions) if they are to be described as such. Contents Page The main offence under the UK Hallmarking Act 1973 is based on description. It is Hallmarking precious metals 3 - 17 an offence for any person in the course of trade or business to: Guidance on describing precious metals 18 - 19 • Describe an un-hallmarked article as being wholly or partly made of silver, palladium, gold or platinum. Contact details for UK Assay Offices Back Page • Supply or offer to supply un-hallmarked articles to which such a description is applied. -

The Precious Metals Book

© CIBJO 2020 All rights reserved. PRECIOUS METALS COMMISSION 2020-1 2020 – 1 2020-04-01 CIBJO/PRECIOUS METALS COMMISSION THE PRECIOUS METALS BOOK Precious Metals – Terminology & Classification CIBJO standard Page 1 of 29 © CIBJO 2020 All rights reserved. PRECIOUS METALS COMMISSION 2020-1 Table of Contents 1. Foreword .................................................................................................................................................................. 3 2. Background: ............................................................................................................................................................. 4 3. Scope ........................................................................................................................................................................ 6 4. Terms and definitions ............................................................................................................................................... 6 4.1. Adhesive .......................................................................................................................................................... 6 4.2. Base metals ..................................................................................................................................................... 6 4.3. Colour of Precious Metals ............................................................................................................................... 6 4.4. Fineness ......................................................................................................................................................... -

Jewellery EU MARKET SURVEY 2004

EU MARKET SURVEY 2004 Jewellery EU MARKET SURVEY 2004 JEWELLERY Compiled for CBI by: Fair Trade Solutions in collaboration with Searce August 2004 DISCLAIMER CBI MARKET INFORMATION TOOLS Although the content of its market information tools has been compiled with the greatest care, the Centre for the Promotion of Imports from developing countries (CBI) is not able to guarantee that the information provided is accurate and/or exhaustive, and cannot be held liable for claims pertaining to use of the information. In the case of the market publications, neither CBI nor the authors of the publications accept responsibility for the use which might be made of the information. Furthermore, the information shall not be construed as legal advice. Original documents should, therefore, always be consulted where appropriate. The information does not release the reader from the responsibility of complying with any relevant legislation, regulations, jurisdiction or changes/updates of same. In the case of the Internet tools, CBI aims at minimising disruption caused by technical errors. However, CBI cannot guarantee that its service will not be interrupted or otherwise affected by technical problems. CBI accepts no responsibility with regard to problems incurred as a result of using this site or any linked external sites. The information provided is aimed at assisting the CBI target group, i.e. exporters and business support organisations (BSOs) in developing countries. It may, therefore, not be used for re-sale, the provision of consultancy services, redistribution or the building of databases, on a commercial basis. For utilization of the CBI market information tools by the CBI target group on a non-commercial basis, the condition applies that CBI is referred to as the source of the information. -

NEW 22 CARAT GOLD SOLDERS This Article Is Taken from Chapter 5 of Lengths

NEW 22 CARAT GOLD SOLDERS This article is taken from Chapter 5 of lengths. The brazing operation is by a powder method, which involves tumbling the chain in a Principles of Brazing. The chapter non-gold, silver-base braze powder. It is then re- is titled “Filler Metals for Carat Gold tumbled in talc to remove braze powder adhering and Hallmark Silver Jewelry.” to exposed surfaces, leaving it only in the gaps of the links. The chain is then brazed by passing the prepared chain through a belt furnace in an inert David M. Jacobson atmosphere. Wembley, England Giles Humpston Brazes for gold jewelry Most readers will be familiar with the term carat. Tessera Inc. It is a unit for measuring the purity of gold and, San Jose, California quite separately, as the mass of precious stones. On the scale of gold purity, 24 carat (karat in the razes for jewelry, silverware, and objets United States and Germany) represents pure gold. d’art merit separate consideration from Thus, an 18 carat gold alloy contains 18/24 (i.e., industrial brazing alloys because, in ad- 75%) weight fraction of the precious metal. dition to providing joints that are mechan- Quality items of jewelry are made with yellow Bically durable (in terms of their strength, ductility, gold of 18 or higher caratage. The word carat ac- and wear resistance), they must satisfy two addi- tually derives from the Arabic word quirrat, tional and fundamentally different criteria spe- meaning seed, and the weight of a semiprecious cific to this usage: They must match the caratage carob seed was taken as one carat. -

Fineness of Gold from Alaska Placers

UNITED STATES DEPARTMENT OF THE INTERIOR Harold L. Ickes, Secretary GEOLOGICAL SURVEY W. C. Mendenhall, Director Bulletin 910-C FINENESS OF GOLD FROM ALASKA PLACERS BY PHILIP S. SMITH Mineral resources of Alaska, 1937 (Pages 147-272) UNITED STATES GOVERNMENT PRINTING OFFICE WASHINGTON : 1941 For gale by the Superintendent of Documents, Washington, D. C. ....... Price 30 ceati CONTENTS Page Abstract ________________-______ ___ __ .. 147 Introduction __.. _ _ _ _ . 147 Definitions ________________________________-_____ 148 Sources of information___________._ ________ _ _____ 151 Arrangement of information._____ ___ _ _ 153 General summary___ _____ _ _ _ '.________ 154; Differences in fineness______________________-_____- 162 Metals other than gold in bullion from Alaska placers________ 164 Descriptions of regions in relation to fineness of placer gold 165' Southeastern Alaska region__________________________ 166- Juneau district ____________________ 16f Porcupine district_________________________^__ 168 Yakataga district_____._______________________ 168 Copper River region_______________________-_______ 169 Cliistochinn district____________________..________ 169 Slate Creek area__________________________ 170 Middle Fork area___________________________ 170 Rainy Creek area___.,___________-__-_____ 170 Niuina district_________________________________ 171 Nelchimi district ______________________________ 172 Cook Inlet-Snsitna region _____.._____________________ 172 Kenai district _ _________ _______ ________ 173 Sunrise and Hope areas______________________