Transformational Year for Rare Scotch Whisky Sales

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Four Facts About Whisky Casks Distillers Don't Want You to Know

Malt Maniacs E-pistle #2010-08 By Oliver Klimek, Germany This article is brought to you by 'Malt Maniacs'; an international collective of more than two dozen fiercely independent malt whisky aficionados. Since 1997 we have been enjoying and discussing the pleasures of single malt whisky with like-minded whisky lovers from all over the world. In 2010 our community had members from 16 countries; The United Kingdom, Sweden, Germany, Holland, Belgium, France, Switzerland, Italy, Greece, The U.S.A., Canada, India, Japan, Taiwan, Australia & South Africa. More information on: www.maltmaniacs.org . Four Facts About Whisky Casks Distillers Don't Want You to Know "All casks are different." This a commonplace and it's one of the basic rules all aspiring maltheads and apprentice whisky anoraks will learn rather early on after they have started their journey into the whisky wonderland. When you take the step from standard distillery expressions to single cask whiskies mainly bottled by independents you will discover a seemingly endless variety of malts that sometimes can have very different characteristics, even if they are made in the same distillery. In this E-pistle I would like to highlight a few aspects of whisky casks that for some strange reason do not get very much attention, even though their consequences are rather significant. 1. Seaweed? What Seaweed? Tasting notes of Islay malts usually feature descriptors like “seaweed”, “sea spray”, “Atlantic jetty” or the likes. We all know that Islay is both caressed and mistreated by the powers of the Irish Sea, so in a way it is not a surprise that we can find maritime flavours in Islay whisky. -

9—11 September 2016

ISLAY JAZZ FESTIVAL 2016 9—11 SEPTEMBER 2016 Presented by Jazz Scotland and Islay Arts Association Welcome ISLAY JAZZ Nowhere else in the world offers such an extraordinary context for a Jazz Festival of FESTIVAL 2016 international class as Islay. What we hope to create is a giant house party where musicians, local audiences and visitors meet and enjoy each other’s company whilst creating and listening to music that always feels immediate and often intimate, in the unique settings of the island’s distilleries, village halls, hotels, and the RSPB Centre. The Lagavulin™ Islay Jazz Festival 2016 will form part of the celebrations for 200 years of Lagavulin. Everyone involved in the Festival thanks Lagavulin for the support, especially Fraser Fifi eld and Graeme Stephen Pocion De Fe this year, where to mark the bicentenary, we present the most ambitious and exciting programme in our 17 year history. In this vintage year the programme offers an impressive international cast, from a host of Islay Jazz Festival favourites to some of the most exciting young musicians changing the face of today’s Scottish Jazz scene, it’s all packed into a weekend that’s rich with musical excitement. We look forward to sharing a dram with old and new friends. Fiona Alexander, Jazz Scotland Stuart Todd, Islay Arts Association Ulf Wakenius Ryan Quigley www.islayjazzfestival.co.uk 0845 111 0302 FRIDAY 9TH SEPTEMBER 1. Martin Taylor and Ulf Wakenius SATURDAY 10TH SEPTEMBER Two of the greatest guitarists in the world. Each played for nearly a decade with jazz 6. Haf tor Medbøe, Espen Eriksen, 10. -

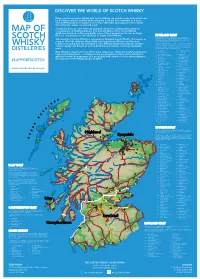

2019 Scotch Whisky

©2019 scotch whisky association DISCOVER THE WORLD OF SCOTCH WHISKY Many countries produce whisky, but Scotch Whisky can only be made in Scotland and by definition must be distilled and matured in Scotland for a minimum of 3 years. Scotch Whisky has been made for more than 500 years and uses just a few natural raw materials - water, cereals and yeast. Scotland is home to over 130 malt and grain distilleries, making it the greatest MAP OF concentration of whisky producers in the world. Many of the Scotch Whisky distilleries featured on this map bottle some of their production for sale as Single Malt (i.e. the product of one distillery) or Single Grain Whisky. HIGHLAND MALT The Highland region is geographically the largest Scotch Whisky SCOTCH producing region. The rugged landscape, changeable climate and, in The majority of Scotch Whisky is consumed as Blended Scotch Whisky. This means as some cases, coastal locations are reflected in the character of its many as 60 of the different Single Malt and Single Grain Whiskies are blended whiskies, which embrace wide variations. As a group, Highland whiskies are rounded, robust and dry in character together, ensuring that the individual Scotch Whiskies harmonise with one another with a hint of smokiness/peatiness. Those near the sea carry a salty WHISKY and the quality and flavour of each individual blend remains consistent down the tang; in the far north the whiskies are notably heathery and slightly spicy in character; while in the more sheltered east and middle of the DISTILLERIES years. region, the whiskies have a more fruity character. -

Glenglassaugh's Revival

Malt Maniacs E-pistle #2011- By ralfy, Isle of Man This article is brought to you by 'Malt Maniacs'; an international collective of more than two dozen fiercely independent malt whisky aficionados. Since 1997 we have been enjoying and discussing the pleasures of single malt whisky with like-minded whisky lovers from all over the world. In 2010 our community had members from 16 countries; The United Kingdom, Sweden, Germany, Holland, Belgium, France, Switzerland, Italy, Greece, The U.S.A., Canada, India, Japan, Taiwan, Australia & South Africa. More information on: www.maltmaniacs.org. Glenglassaugh's revival. A chat with Distillery Boss, Stuart Nickerson At a moment in time when expensive marketing dominates the public message of Scotch Whisky it is both refreshing and insightful to have the opportunity to chat with an Industry professional like Stuart Nickerson, Director of Glenglassaugh Distillery near Port Soy in Scotland who covers many roles in his job of running a small, craft-orientated and Independent Distillery which continues to do things the old-school way, something which experienced whisky drinkers are increasingly more aware of in terms of intrinsic quality and worth. I am happy to introduce a wee question and answers session with Stuart which helps to enhance our perspective on what's behind the amber-nectar which we all enjoy so much - could you introduce yourself to the whisky-fans ! • The story really starts when I left University back in 1979 (BSc in Chemical Engineering from Heriot-Watt University in Edinburgh – seems like a lifetime ago (and is) and started working with a company in Fife who, amongst other things manufactured by- products plants for the whisky industry. -

The Whiskey Machine: Nanofactory-Based Replication of Fine Spirits and Other Alcohol-Based Beverages

The Whiskey Machine: Nanofactory-Based Replication of Fine Spirits and Other Alcohol-Based Beverages © 2016 Robert A. Freitas Jr. All Rights Reserved. Abstract. Specialized nanofactories will be able to manufacture specific products or classes of products very efficiently and inexpensively. This paper is the first serious scaling study of a nanofactory designed for the manufacture of a specific food product, in this case high-value-per- liter alcoholic beverages. The analysis indicates that a 6-kg desktop appliance called the Fine Spirits Synthesizer, aka. the “Whiskey Machine,” consuming 300 W of power for all atomically precise mechanosynthesis operations, along with a commercially available 59-kg 900 W cryogenic refrigerator, could produce one 750 ml bottle per hour of any fine spirit beverage for which the molecular recipe is precisely known at a manufacturing cost of about $0.36 per bottle, assuming no reduction in the current $0.07/kWh cost for industrial electricity. The appliance’s carbon footprint is a minuscule 0.3 gm CO2 emitted per bottle, more than 1000 times smaller than the 460 gm CO2 per bottle carbon footprint of conventional distillery operations today. The same desktop appliance can intake a tiny physical sample of any fine spirit beverage and produce a complete molecular recipe for that product in ~17 minutes of run time, consuming <25 W of power, at negligible additional cost. Cite as: Robert A. Freitas Jr., “The Whiskey Machine: Nanofactory-Based Replication of Fine Spirits and Other Alcohol-Based Beverages,” IMM Report No. 47, May 2016; http://www.imm.org/Reports/rep047.pdf. 2 Table of Contents 1. -

Speyside the Land of Whisky

The Land of Whisky A visitor guide to one of Scotland’s five whisky regions. Speyside Whisky The practice of distilling whisky No two are the same; each has has been lovingly perfected its own proud heritage, unique throughout Scotland for centuries setting and its own way of doing and began as a way of turning things that has evolved and been rain-soaked barley into a drinkable refined over time. Paying a visit to spirit, using the fresh water from a distillery lets you discover more Scotland’s crystal-clear springs, about the environment and the streams and burns. people who shape the taste of the Scotch whisky you enjoy. So, when To this day, distilleries across the you’re sitting back and relaxing country continue the tradition of with a dram of our most famous using pure spring water from the export at the end of your distillery same sources that have been tour, you’ll be appreciating the used for centuries. essence of Scotland as it swirls in your glass. From the source of the water and the shape of the still to the Home to the greatest wood of the cask used to mature concentration of distilleries in the the spirit, there are many factors world, Scotland is divided into five that make Scotch whisky so distinct whisky regions. These are wonderfully different and varied Highland, Lowland, Speyside, Islay from distillery to distillery. and Campbeltown. Find out more information about whisky, how it’s made, what foods to pair it with and more: www.visitscotland.com/whisky For more information on travelling in Scotland: www.visitscotland.com/travel Search and book accommodation: www.visitscotland.com/accommodation 05 15 03 06 Speyside 07 04 08 16 01 Speyside is home to some of Speyside you’re never far from a 10 Scotland’s most beautiful scenery distillery or two. -

Cost of the Malts

Kingston Single Malt Society www.kingstonsinglemaltsociety.com A social club for the appreciation of Single Malt Whisky since 1998 JULY 27th, 2020 VOLUME 14; NUMBER 1c ---------------------------- COST OF THE MALTS GLENMORANGIE 18 YEAR OLD HIGHLAND SINGLE MALT SCOTCH WHISKY LCBO 398784 | 750 mL bottle Price $199.20 Spirits, Whisky/Whiskey 43.0% Alcohol/Vol. GLENMORANGIE SIGNET LCBO 327452 | 750 mL bottle Price: $336.20 Spirits, Scotch Whisky 46.0% Alcohol/Vol. NEW BEN NEVIS 10 YEARS OLD LCBO 432281 | 700 mL bottle Price: $85.00 Spirits, Whisky/Whiskey, Scotch Single Malts 46.0% Alcohol/Vol. OLD BEN NEVIS 10 YEARS OLD LCBO 432281 | 700 mL bottle Price: $85.00 Spirits, Whisky/Whiskey, Scotch Single Malts 46.5% Alcohol/Vol. DISTILLER’S ART BLAIR ATHOL 14 YEAR OLD Distilled: 2003; Bottled: 2018; Bottle # 076 of 397; LCBO 614783 | 700 mL bottle Spirits, Price: $173.85 Whisky/Whiskey 48.0% Alcohol/Vol. BUNNAHABHAIN 2003 AMONTILLADO CASK FINISH Distilled: 20/02/2003; Bottled: 26/02/2016; ---------------------------- LIMITED TO 1710 BOTTLES; VINTAGES 807462 | 700 mL bottle Price: $225.95 Spirits, Scotch Whisky 57.45% MENU Alcohol/Vol. 1st and 2nd and Welcome Nosing: ---------------------------- GLENMORANGIE 18 GLENMORANGIE SIGNET Upcoming Dinner Dates (introduced by: Dave Finucan) Upcoming Dinner Dates 1st Course: Grilled Corn & Bacon Gazpacho August 10th 2020 - Distell Tasting - with Crème Fraîche and Roasted Red Pepper Bunnahabhain / Tobermory / Ledaig - Mike Brisebois th th Friday August 28 2020 - 13 Annual Premium Night rd 3 Nosing: NEW BEN -

The Balvenie Single Malt Scotch Whisky

The Balvenie Single Malt Scotch Whisky The Balvenie is a unique range of single malts created by David Stewart, The Balvenie Malt Master and longest-serving Malt Master in the industry. Each has a very individual taste, but each is rich, luxuriously smooth and underpinned by the distinctively honeyed character of The Balvenie. Produced in Speyside in the Scottish Highlands, the exceptional quality of The Balvenie Single Malt is due to the fact that The Balvenie Distillery retains and nurtures a high level of craftsmanship that other malt whisky producers no longer employ: nowhere else will you find a distillery that still grows its own barley, still malts in its own traditional floor maltings, still employs coopers to tend all the casks and a coppersmith to maintain the stills. Today the Balvenie Distillery produces a multi award-winning range of The Balvenie Single Malts, which includes The Balvenie DoubleWood 12 Year Old, The Balvenie Signature 12 Year Old, The Balvenie Single Barrel 15 Year Old, The Balvenie PortWood 21 Year Old and The Balvenie Thirty. A limited edition and a rare vintage cask over 30 years old are also bottled each year. Our Award Winning Single Malt The Balvenie Malt Master, David Stewart, and his team of craftsmen are thrilled that their time honoured skills have been so highly rewarded. With over one hundred whisky awards in the last ten years, the world’s most acclaimed experts have recognised The Balvenie’s unique quality and range of tastes and the commitment to traditional malt whisky making, which sets us apart from other single malts. -

WHISKEY AMERICAN WHISKEY Angel's Envy Port Barrel Finished

WHISK(E)YS BOURBON WHISKEY AMERICAN WHISKEY Angel's Envy Port Barrel Finished ............................................................ $12.00 High West Campfire Whiskey ................................................................... $10.00 Basil Hayden's ............................................................................................ $12.00 Jack Daniel's ............................................................................................... $8.00 Belle Meade Sour Mash Whiskey ............................................................. $10.00 Gentleman Jack ........................................................................................ $11.00 Belle Meade Madeira Cask Bourbon ........................................................ $15.00 George Dickel No.12 ................................................................................... $9.00 Blackened Whiskey .................................................................................... $10.00 Mitcher's American Whiskey .................................................................... $12.00 Buffalo Trace ............................................................................................... $8.00 Mitcher's Sour Mash Whiskey .................................................................. $12.00 Bulleit Bourbon ............................................................................................ $8.00 CANADIAN WHISKY Bulleit Bourbon 10 year old ...................................................................... $13.00 -

History of Scotch Whiskey

Scotch Whiskey The Gaelic "usquebaugh", meaning "Water of Life", phonetically became "usky" and then "whisky" in English. However it is known, Scotch whisky, Scotch or Whisky (as opposed to whiskey), it has captivated a global market. Scotland has internationally protected the term "Scotch". For a whisky to be labeled Scotch it has to be produced in Scotland. If it is to be called Scotch, it cannot be produced in England, Wales, Ireland, America or anywhere else. Excellent whiskies are made by similar methods in other countries, notably Japan, but they cannot be called Scotches. They are most often referred to as "whiskey". While they might be splendid whiskies, they do not captivate the tastes of Scotland. "Eight bolls of malt to Friar John Cor wherewith to make aqua vitae" The entry above appeared in the Exchequer Rolls as long ago as 1494 and appears to be the earliest documented record of distilling in Scotland. This was sufficient to produce almost 1500 bottles, and it becomes clear that distilling was already a well-established practice. Legend would have it that St Patrick introduced distilling to Ireland in the fifth century AD and that the secrets traveled with the Dalriadic Scots when they arrived in Kintyre around AD500. St Patrick acquired the knowledge in Spain and France, countries that might have known the art of distilling at that time. The distilling process was originally applied to perfume, then to wine, and finally adapted to fermented mashes of cereals in countries where grapes were not plentiful. The spirit was universally termed aqua vitae ('water of life') and was commonly made in monasteries, and chiefly used for medicinal purposes, being prescribed for the preservation of health, the prolongation of life, and for the relief of colic, palsy and even smallpox. -

Boisdale of Canary Wharf Whisky Bible

BOISDALE Boisdale of Canary Wharf Whisky Bible 1 All spirits are sold in measures of 25ml or multiples thereof. All prices listed are for a large measure of 50ml. Should you require a 25ml measure, please ask. All whiskies are subject to availability. 1. Springbank 10yr 19. Old Pulteney 12yr 37. Ardbeg Corryvreckan 55. Longmorn 16yr 2. Highland Park 12yr 20. Aberfeldy 12yr 38. Smokehead 56. Glenrothes Select Reserve 3. Bowmore 12yr 21. Blair Athol 12yr 39. Lagavulin 16yr 57. Glenfiddich 15yr Solera 4. Oban 14yr 22. Royal Lochnagar 12yr 40. Laphroaig Quarter Cask 58. Glenfarclas 10yr 5. Cragganmore 12yr 23. Talisker 10yr 41. Laphroaig 10yr 59. Ben Nevis 12yr 6. Fettercairn (Old) 10yr 24. Laphroaig 15yr 42. Octomore 7.1 60. Highland Park 18yr 7. Benromach 10yr 25. Benriach Curiositas 10yr 43. Tomintoul 16yr 61. Glenfarclas 40yr 105 8. Ardmore Traditional 26. Caol Ila 12yr 44. Glengoyne 10yr 62. Macallan 10yr Sherry Oak 9. Connemara Peated 27. Port Charlotte 2008 45. Cardhu 12yr 63. Glendronach 12yr 10. St. George’s Chapter 9 28. Loch Lomond 12yr 46. An Cnoc 16yr 64. Balvenie 12yr DoubleWood 11. Isle of Jura 10yr 29. Speyburn 10yr 47. Glenkinchie 12yr 65. Aberlour 10yr 12. Glen Garioch 21yr 30. Balblair 1997 48. Macallan 12yr Fine Oak 66. Glengoyne 12yr 13. Tobermory 10yr 31. Bruichladdie Classic 49. Glenfiddich 12yr 67. Penderyn Madeira 14. Dalwhinnie 15yr Laddie 50. Bushmills 10yr 68. Glen Moray 12yr 15. Glenmorangie Original 32. Tullibardine 223 51. Tomatin 12yr 69. Glen Grant 10yr 16. Bunnahabhain 12yr 33. Tomatin 18yr 52. Glenlivet 12yr 70. -

Islay Whisky

The Land of Whisky A visitor guide to one of Scotland’s five whisky regions. Islay Whisky The practice of distilling whisky No two are the same; each has has been lovingly perfected its own proud heritage, unique throughout Scotland for centuries setting and its own way of doing and began as a way of turning things that has evolved and been rain-soaked barley into a drinkable refined over time. Paying a visit to spirit, using the fresh water a distillery lets you discover more from Scotland’s crystal-clear about the environment and the springs, streams and burns. people who shape the taste of the Scotch whisky you enjoy. So, when To this day, distilleries across the you’re sitting back and relaxing country continue the tradition with a dram of our most famous of using pure spring water from export at the end of your distillery the same sources that have been tour, you’ll be appreciating the used for centuries. essence of Scotland as it swirls in your glass. From the source of the water and the shape of the still to the wood Home to the greatest concentration of the cask used to mature the of distilleries in the world, spirit, there are many factors Scotland is divided into five that make Scotch whisky so distinct whisky regions. These wonderfully different and varied are Islay, Speyside, Highland, from distillery to distillery. Lowland and Campbeltown. Find out more information about whisky, how it’s made, what foods to pair it with and more: www.visitscotland.com/whisky For more information on travelling in Scotland: www.visitscotland.com/travel Search and book accommodation: www.visitscotland.com/accommodation Islay BUNNAHABHAIN Islay is one of many small islands barley grown by local crofters.