Saving UK Biotech

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Guidelines with Regard to the Composition, Calculation and Management of the Index

INDEX METHODOLOGY Solactive Pharma Breakthrough Value Index Version 2.1 dated September 03, 2020 Contents Important Information 1. Index specifications 1.1 Short Name and ISIN 1.2 Initial Value 1.3 Distribution 1.4 Prices and Calculation Frequency 1.5 Weighting 1.6 Index Committee 1.7 Publication 1.8 Historical Data 1.9 Licensing 2. Composition of the Index 2.1 Selection of the Index Components 2.2 Ordinary Adjustment 2.3 Extraordinary Adjustment 3. Calculation of the Index 3.1 Index Formula 3.2 Accuracy 3.3 Adjustments 3.4 Dividends and other Distributions 3.5 Corporate Actions 3.6 Correction Policy 3.7 Market Disruption 3.8 Consequences of an Extraordinary Event 4. Definitions 5. Appendix 5.1 Contact Details 5.2 Calculation of the Index – Change in Calculation Method 2 Important Information This document (“Index Methodology Document”) contains the underlying principles and regulations regarding the structure and the operating of the Solactive Pharma Breakthrough Value Index. Solactive AG shall make every effort to implement regulations. Solactive AG does not offer any explicit or tacit guarantee or assurance, neither pertaining to the results from the use of the Index nor the Index value at any certain point in time nor in any other respect. The Index is merely calculated and published by Solactive AG and it strives to the best of its ability to ensure the correctness of the calculation. There is no obligation for Solactive AG – irrespective of possible obligations to issuers – to advise third parties, including investors and/or financial intermediaries, of any errors in the Index. -

List of Section 13F Securities, First Quarter, 2014

List of Section 13F Securities First Quarter FY 2014 Copyright (c) 2014 American Bankers Association. CUSIP Numbers and descriptions are used with permission by Standard & Poors CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. All rights reserved. No redistribution without permission from Standard & Poors CUSIP Service Bureau. Standard & Poors CUSIP Service Bureau does not guarantee the accuracy or completeness of the CUSIP Numbers and standard descriptions included herein and neither the American Bankers Association nor Standard & Poor's CUSIP Service Bureau shall be responsible for any errors, omissions or damages arising out of the use of such information. U.S. Securities and Exchange Commission OFFICIAL LIST OF SECTION 13(f) SECURITIES USER INFORMATION SHEET General This list of “Section 13(f) securities” as defined by Rule 13f-1(c) [17 CFR 240.13f-1(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [15 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.13f-1] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of March 15, 2014, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending March 31, 2014. Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by [ Section 13(f)(1) and Rule 13f-1] thereunder. -

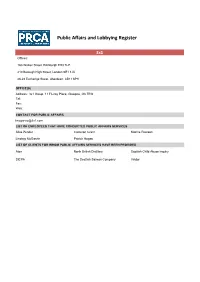

Public Affairs and Lobbying Register

Public Affairs and Lobbying Register 3x1 Offices: 16a Walker Street, Edinburgh EH3 7LP 210 Borough High Street, London SE1 1JX 26-28 Exchange Street, Aberdeen, AB11 6PH OFFICE(S) Address: 3x1 Group, 11 Fitzroy Place, Glasgow, G3 7RW Tel: Fax: Web: CONTACT FOR PUBLIC AFFAIRS [email protected] LIST OF EMPLOYEES THAT HAVE CONDUCTED PUBLIC AFFAIRS SERVICES Ailsa Pender Cameron Grant Katrine Pearson Lindsay McGarvie Patrick Hogan LIST OF CLIENTS FOR WHOM PUBLIC AFFAIRS SERVICES HAVE BEEN PROVIDED Atos North British Distillery Scottish Child Abuse Inquiry SICPA The Scottish Salmon Company Viridor Public Affairs and Lobbying Register Aiken PR OFFICE(S) Address: 418 Lisburn Road, Belfast, BT9 6GN Tel: 028 9066 3000 Fax: 028 9068 3030 Web: www.aikenpr.com CONTACT FOR PUBLIC AFFAIRS [email protected] LIST OF EMPLOYEES THAT HAVE CONDUCTED PUBLIC AFFAIRS SERVICES Claire Aiken Donal O'Neill John McManus Lyn Sheridan Shane Finnegan LIST OF CLIENTS FOR WHOM PUBLIC AFFAIRS SERVICES HAVE BEEN PROVIDED Diageo McDonald’s Public Affairs and Lobbying Register Airport Operators Associaon OFFICE(S) Address: Airport Operators Association, 3 Birdcage Walk, London, SW1H 9JJ Tel: 020 7799 3171 Fax: 020 7340 0999 Web: www.aoa.org.uk CONTACT FOR PUBLIC AFFAIRS [email protected] LIST OF EMPLOYEES THAT HAVE CONDUCTED PUBLIC AFFAIRS SERVICES Ed Anderson Henk van Klaveren Jeff Bevan Karen Dee Michael Burrell - external public affairs Peter O'Broin advisor Roger Koukkoullis LIST OF CLIENTS FOR WHOM PUBLIC AFFAIRS SERVICES HAVE BEEN PROVIDED N/A Public Affairs and -

31 December 2018 Transition and Annual Report 2018

TRANSITION AND ANNUAL REPORT 2018 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended OR ⌧ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from October 1, 2018 to December 31, 2018 Commission File Number 001-35892 GW PHARMACEUTICALS PLC (Exact name of Registrant as specified in its charter) England and Wales Not Applicable (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) Sovereign House, Vision Park Chivers Way, Histon Cambridge, CB24 9BZ United Kingdom +44 1223 266800 (Address of principal executive offices) (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of exchange on which registered American Depositary Shares, each representing 12 Ordinary The Nasdaq Global Market Shares, par value £0.001 per share Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☑ NO ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ☐ NO ☑ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

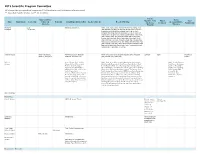

2019 Scientific Program Committee All Relationships Are Considered Compensated

2019 Scientific Program Committee All relationships are considered compensated. Relationships are self-held unless otherwise noted. I = Immediate Family Member, Inst = My Institution Patents, Stock and Other Travel, Royalties, Other Expert Other Name Employment Leadership Ownership Honoraria Consulting or Advisory Role Speakers' Bureau Research Funding Accommodations, Intellectual Testimony Relationship Interests Expenses Property Monica M. Leap Syntalogic, Syntimmune Abbvie (Inst), Agenus (Inst), Astellas Pharma (Inst), AstraZeneca Bertagnolli Therapeutics (Inst), Baxalta (Inst), Bayer Health (Inst), Breast Cancer Research Foundation (Inst), Bristol-Myers Squibb (Inst), Celgene (Inst), Complion (Inst), Eisai (Inst), Exelixis (Inst), Genentech (Inst), GHI Pharma (Inst), Gilead Sciences (Inst), GlaxoSmithKline (Inst), Incyte (Inst), Janssen (Inst), Jazz Pharmaceuticals (Inst), Leidos (Inst), Lexicon (Inst), Lilly (Inst), Matrex (Inst), Mayo Clinic (Inst), Merck (Inst), MGH (Inst), Millenium Pharamceuticals (Inst), Novartis (Inst), Patient Centered Outcomes Research Institute (PCORI) (Inst), Pfizer (Inst), Pharmacyclics (Inst), Robert Wood Johnson Foundation (Inst), Sagerock Advisors (Inst), Sanofi (Inst), Taiho Pharmaceutical (Inst), Takeda (Inst), Tesaro (Inst), Teva (Inst) Suzanne George Abbott Laboratories, AstraZeneca, Bayer, Blueprint ARIAD (Inst), Bayer (Inst), Blueprint Medicines (Inst), Deciphera UptoDate Bayer Research to Abbvie (I), Allergan (I) Medicines, Deciphera, Lilly (Inst), Novartis (Inst), Pfizer (Inst) Practice Melissa -

2019 Emerging Science Program Schedule

2019 Emerging Science Program Schedule Following is the schedule of Emerging Science abstracts to be presented at the 2019 AAN Annual Meeting. Abstracts qualify for Emerging Science presentations by having key aspects of research conducted after the October 22 abstract submission deadline and must be new and of sufficient scientific importance to warrant expedited presentation and publication. The Science Committee is committed to presenting the best neuroscientific research at the Annual Meeting so we are excited to announce that there will be 11 abstracts presented as part of the Emerging Science program. 11 dual presentation abstracts will be featured in data blitz format during the first 35 minutes of the Emerging Science Platform session on Tuesday, May 7 from 11:45 a.m. to 12:20 p.m., followed by poster presentations in the same room from 12:20 p.m. to 12:45 p.m. One abstract will be presented during the Clinical Trials Plenary session. The 2019 Emerging Science abstracts are embargoed until 12:01 a.m. Eastern Standard Time on Friday, May 3. EMERGING SCIENCE PLATFORM SESSION Tuesday, May 7, 2019, 11:45 a.m.-12:45 p.m. 001 Efficacy and safety of PXT3003 in patients with Charcot-Marie-Tooth type 1A (CMT1A): results of PLEO-CMT, an International Pivotal Phase 3 Trial Florian P. Thomas, MD, MA, PhD, FAAN 002 SerumLincLNMAT1Correlated with Phosphorylatedα-Synucleinas Serum Biomarkers of Parkinson’s Disease: A Cross- Sectional Study. Jing Zou, MD, PhD, MBBS 003 Development of an AAV-based microRNA Gene Therapy for Treating Spinocerebellar -

2018-Annual-Report.Pdf

Contents Welcome from the Chair ................................................................................................................................................................. 3 Treasurer’s Report ........................................................................................................................................................................... 5 Membership Report ......................................................................................................................................................................... 6 Partnership Report ........................................................................................................................................................................... 7 Commercial Report .......................................................................................................................................................................... 8 Careers & Academic Liaision Committee (CALC) ...................................................................................................................... 9 External Affairs ............................................................................................................................................................................... 11 Communication & Publications Report ....................................................................................................................................... 12 PSI/EFSPI Regulatory Report ..................................................................................................................................................... -

GW Pharmaceuticals Annual Report 2021

GW Pharmaceuticals Annual Report 2021 Form 10-K (NASDAQ:GWPH) Published: April 30th, 2021 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K/A (Amendment No. 1) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission File Number 001-35892 GW PHARMACEUTICALS PLC (Exact name of Registrant as specified in its charter) England and Wales Not Applicable (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) Sovereign House, Vision Park Chivers Way, Histon Cambridge, CB24 9BZ United Kingdom +44 1223 266800 (Address of principal executive offices) (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of exchange on which registered American Depositary Shares, each GWPH The Nasdaq Global Market representing 12 Ordinary Shares, par value £0.001 per share Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☒ NO ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ☐ NO ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

UR-Coeus Sponsor List

UR-Coeus Sponsor Table (alphabetical by sponsor name) Sponsor Sponsor Code Sponsor Type 2138 21st Century Medicine CORP Sponsor Type Key 1 3M CORP CORP = Corporate 3803 4S3 Bioscience Inc CORP FED = Federal 5207 A. F. Associates Family Medicine ONFA FND = Foundation 2602 A. P. Pharma CORP IND = Individuals 2 A.L. Mailman Foundation FND NYS = New York State 2023 AA Implant Dentistry Research Foundation ONFA OLG = Other Local Gov't 3 AAA Fnd for Traffic Safety ONFA ONFA = Other Non-Fed Agency 2329 aaiPharma Inc CORP VHA = Voluntary Health Agency 3257 Aamjiwnaang First Nations Community ONFA 5345 Aarhus University Hospital ONFA 3713 Aaron Copland Fund for Music, Inc. ONFA 4 AARP Andrus Fdn FND 3853 AB Sciences CORP 3378 AB Vector, Inc CORP 899 Abbott Diagnostics CORP 3864 Abbott Fund FND 14 Abbott Laboratories CORP 5126 AbbVie, Inc. CORP 5854 Abeona Therapeutics CORP 5063 Abington Medical Specialists ONFA 5331 Abington Memorial Hospital ONFA 2835 ABIOMED, Inc. CORP 3687 Ablation Frontiers CORP 5118 Ablynx NV CORP 2053 ABMRF/Fnd for Alcohol Research ONFA 2171 Abortion Rights Mobilization ONFA 3361 Abraxix BioScience, LLC CORP 4953 Abt Associates, Inc. CORP 5037 Academic Gastrointestinal Cancer Consortium ONFA 15 Academic Med Ctr Cons ONFA 3733 Academic Pediatric Association ONFA 3160 Academy of Orofacial Pain ONFA 2122 Academy of Prosthodontics Foundation ONFA 3663 Acadia Pharmaceuticals, Inc. CORP 3273 Accelerate Brain Cancer Cure ONFA 5584 Acceleron Pharma Inc. CORP 5601 Accelovance, Inc. CORP 5940 Accreditation Council Grad Med Educ ONFA 5832 Accriva Diagnostics CORP 3888 AccuGenomics, Inc. CORP 5656 Acerta Pharma CORP 6101 Acessa Health, Inc. -

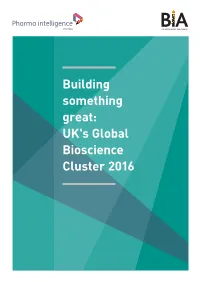

UK's Global Bioscience Cluster 2016 the UK Bioindustry Association: Delivering the Best Possible Environment for Biotechnology Growth and Innovation

Building something great: UK's Global Bioscience Cluster 2016 The UK BioIndustry Association: Delivering the best possible environment for biotechnology growth and innovation. We advocate to government at both the UK and European levels to improve policies, funding and taxation. We also work to improve the business environment by engaging with regulators, the City, venture capitalists, charities and patient groups. Join now: 320 members, 135 companies represented on Advisory Committees Save: Our members saved over £5.8M in 2016 through our Business Solutions programme Connect: Network and build relationships with 2,500+ industry leaders at our UK-wide events Influence: Be at the heart of policy development. Shape our sector and represent positive change for UK biotech Join UK’s trade association for biotechnology now: www.bioindustry.org/membership Contents Foreword from UK BioIndustry Association Chief Executive, Steve Bates, OBE 4 Foreword from Informa Pharma Executive Editor, John Hodgson 5 Overall trends for UK biotech in 2016 7 Venture capital funding 9 The UK venture capital picture has matured 9 Top UK venture capital rounds 2016 11 Venture capital raised – rest of Europe and USA 14 Public markets 16 UK IPOs 2016 16 Changes in global public markets for UK biotech 19 AIM persists as a source of follow-on finance, even when markets are more closed 21 Partnering and deal making 24 Selected acquisition by UK companies in 2016 24 Pipeline 28 The future 30 Updated 22 September 2017 Foreword from UK BioIndustry Association Chief Executive, Steve Bates, OBE The UK has some of the world’s most exciting science, a supportive business environment, and strong companies led by experienced management teams. -

[ Emc-Lusinnufll'lergcrta'rgets

US 20070255633Al (19) United States (12) Patent Application Publication (10) Pub. N0.: US 2007/0255633 A1 Kridel (43) Pub. Date: NOV. 1, 2007 (54) SYSTEMS AND METHODS FOR INVESTING (52) US. Cl. ....................................................... .. 705/35 (76) Inventor: FIVJigiam J. Kridel, New York, NY (57) ABSTRACT The present invention discloses systems and methods for Correspondence Address? creating and managing ?nancial instruments and indexes PAUL’ HASTINGS’ JANOFSKY & WALKER comprised of securities for companies in subsectors of the LLP economy. These ?nancial instruments alloW investment in R0' BOX 919092 subsectors of the economy Will still being able to minimize SAN DIEGO CA 92191-9092 ’ risk by diversi?cation. The indexes serve as benchmarks for (21) App1_ NO; 11/465,768 companies in the subsectors of the economy. A procedure may be used to identify the securities to include in the (22) Filed: Allg- 18, 2006 ?nancial instruments. This procedure may include (a) iden _ _ tifying securities for companies in a sector of the economy; Related U's‘ Apphcatlon Data (b) limiting the identi?ed securities to those for companies (60) Provisional application No. 60/778,492, ?led on Mar. in a SubSeCIOr Of the SBCIOI‘ Of the economy; (0) applying 1, 2006. focus rules to further limit the identi?ed securities to those _ _ _ _ for companies Who are focused in the subsector of the Pubhcatlon Classl?catlon economy; and (d) limiting the securities included in the (51) Int, Cl, ?nancial instrument or index to those that satisfy other G06Q 40/00 (2006.01) objective criteria. ETF RULE. SET->| APPLICATION’ ' "1 _. -

EU Financial Accounts Reports

EU Financial accounts reports David Citron GW Pharmaceuticals plc – Results The company’s share price has had a for the year to 30th September, rocky ride since its June 2001 listing at 182p. 2001 By September 2001 the price had fallen to only just over one-third of that value at 67p. Well known as the only company in the UK Since then, however, it has registered a licensed to develop cannabis for medicinal reasonably steady improvement. This has purposes, GW Pharmaceuticals floated on been helped by the Home Secretary’s the Alternative Investment Market in June October 2001 announcement that he was 2001, raising £23.5m net. Including a pre- intending to approve a change in the law to listing private share placement, the enable the prescription of cannabis-based company raised a total of just over £30m medicines, which produced a 13 per cent during the year to September 2001, giving it share price improvement, and further a year-end cash balance of over £25m. government moves in this direction in Discoveries in the last decade or so have February 2002 which produced an triggered renewed interest in the therapeutic additional 12 per cent price increase. potential for a wide range of medical As at the time of writing the company’s conditions of cannabinoids, molecules found shares had recovered to 138p, boosted by only in the cannabis plant. GW the positive noises from government, its Pharmaceuticals embarked on its first Phase healthy cash balance, its unique market III multiple sclerosis trial in May 2001, which position and steady progress in clinical was expected to be completed by the end of trials.