Pricing Credit from Equity Options

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WHS FX Options Guide

Getting started with FX options WHS FX options guide Predict the trend in currency markets or hedge your positions with FX options. Refine your trading style and your market outlook. Learn how FX options work on the WHS trading environment. WH SELFINVEST Copyrigh 2007-2011: all rights attached to this guide are the sole property of WH SelfInvest S.A. Reproduction and/or transmission of this guide Est. 1998 by whatever means is not allowed without the explicit permission of WH SelfInvest. Disclaimer: this guide is purely informational in nature and can Luxemburg, France, Belgium, in no way be construed as a suggestion or proposal to invest in the financial instruments mentioned. Persons who do decide to invest in these Poland, Germany, Netherlands financial instruments acknowledge they do so solely based on their own decission and risks. Alle information contained in this guide comes from sources considered reliable. The accuracy of the information, however, is not guaranteed. Table of Content Global overview on FX Options Different strategies using FX Options Single Vanilla Vertical Strangle Straddle Risk Reversal Trading FX Options in WHSProStation Strategy settings Rules and Disclaimers FAQ Global overview on FX Options An FX option is a contract between a buyer and a seller for the What is an FX option? right to buy or sell an underlying currency pair at a specific price on a particular date. EUR/USD -10 Option Premium Option resulting in a short position 1.3500 - 1.3400 +100 PUT Strike Price – Current Market Price Overal trade Strike price +90 You believe EUR/USD will drop in the weeks to come. -

Do Options-Implied RND Functions on G3 Currencies Move Around the Times of Interventions on the JPY/USD Exchange Rate? by O

WORKING PAPER SERIES NO. 410 / NOVEMBER 2004 DO OPTIONS- IMPLIED RND FUNCTIONS ON G3 CURRENCIES MOVE AROUND THE TIMES OF INTERVENTIONS ON THE JPY/USD EXCHANGE RATE? by Olli Castrén WORKING PAPER SERIES NO. 410 / NOVEMBER 2004 DO OPTIONS- IMPLIED RND FUNCTIONS ON G3 CURRENCIES MOVE AROUND THE TIMES OF INTERVENTIONS ON THE JPY/USD EXCHANGE RATE? 1 by Olli Castrén 2 In 2004 all publications will carry This paper can be downloaded without charge from a motif taken http://www.ecb.int or from the Social Science Research Network from the €100 banknote. electronic library at http://ssrn.com/abstract_id=601030. 1 Comments by Kathryn Dominguez, Gabriele Galati, Stelios Makrydakis, Filippo di Mauro,Takatoshi Ito and participants of internal ECB seminars are gratefully acknowledged.All opinions expressed in this paper are those of the author only and not those of the European Central Bank or the European System of Central Banks. 2 DG Economics, European Central Bank, Kaiserstrasse 29, D-60311 Frankfurt am Main, Germany; e-mail: [email protected] © European Central Bank, 2004 Address Kaiserstrasse 29 60311 Frankfurt am Main, Germany Postal address Postfach 16 03 19 60066 Frankfurt am Main, Germany Telephone +49 69 1344 0 Internet http://www.ecb.int Fax +49 69 1344 6000 Telex 411 144 ecb d All rights reserved. Reproduction for educational and non- commercial purposes is permitted provided that the source is acknowledged. The views expressed in this paper do not necessarily reflect those of the European Central Bank. The statement of purpose for the ECB Working Paper Series is available from the ECB website, http://www.ecb.int. -

Consolidated Financial Statements for the Year Ended 31 December 2017 Azimut Holding S.P.A

Consolidated financial statements for the year ended 31 december 2017 Azimut Holding S.p.A. Consolidated financial statements for the year ended 31 december 2017 Azimut Holding S.p.A. 4 Gruppo Azimut Contents Company bodies 7 Azimut group's structure 8 Main indicators 10 Management report 13 Baseline scenario 15 Significant events of the year 19 Azimut Group's financial performance for 2017 25 Main balance sheet figures 28 Information about main Azimut Group companies 32 Key risks and uncertainties 36 Related-party transactions 40 Organisational structure and corporate governance 40 Human resources 40 Research and development 41 Significant events after the reporting date 41 Business outlook 42 Non-financial disclosure 43 Consolidated financial statements 75 Consolidated balance sheet 76 Consolidated income statement 78 Consolidated statement of comprehensive income 79 Consolidated statement of changes in shareholders' equity 80 Consolidated cash flow statement 84 Notes to the consolidated financial statements 87 Part A - Accounting policies 89 Part B - Notes to the consolidated balance sheet 118 Part C - Notes to the consolidated income statement 147 Part D - Other information 159 Certification of the consolidated financial statements 170 5 6 Gruppo Azimut Company bodies Board of Directors Pietro Giuliani Chairman Sergio Albarelli Chief Executive Officer Paolo Martini Co-Managing Director Andrea Aliberti Director Alessandro Zambotti (*) Director Marzio Zocca Director Gerardo Tribuzio (**) Director Susanna Cerini (**) Director Raffaella Pagani Director Antonio Andrea Monari Director Anna Maria Bortolotti Director Renata Ricotti (***) Director Board of Statutory Auditors Vittorio Rocchetti Chairman Costanza Bonelli Standing Auditor Daniele Carlo Trivi Standing Auditor Maria Catalano Alternate Auditor Luca Giovanni Bonanno Alternate Auditor Independent Auditors PricewaterhouseCoopers S.p.A. -

Delta and Vega Hedging in the SABR and LMM-SABR Models

CUTTING EDGE. INTEREST RATE DERIVATIVES Delta and vega hedging in the SABR and LMM-SABR models T Riccardo Rebonato, Andrey Pogudin and Richard d t T T T dwt (2) White examine the hedging performance of the SABR t and LMM-SABR models using real market data. As a Q T E dzT dwT T dt (3) by-product, they gain indirect evidence about how well t t specified the two models are. The results are extremely The LMM-SABR model extension by Rebonato (2007) posits the following joint dynamics for the forward rates and their instanta- encouraging in both respects neous volatilities: q M i i i i dft idt ft t eijdz j , i 1, N (4) j1 model (Hagan et al, 2002) has become a market i i t gt,Ti kt (5) The SABR standard for quoting the prices of plain vanilla options. Its main claim to being better than other models capable i M dk k i t =μ i + = + × of recovering exactly the smile surface (see, for example, the local t dt ht ∑ eijdz j , i N 1, 2 N (6) k i volatility model of Dupire, 1994, and Derman & Kani, 1996) is t j=1 its ability to provide better hedging (Hagan et al, 2002, Rebon- with: ato, 2004, and Piterbarg, 2005). M = N + N (7) The status of market standard for plain vanilla options enjoyed V F by the SABR model is similar to the status enjoyed by the Black NV and NF are the number of factors driving the forward rate and formula in the pre-smile days. -

Equity Derivatives Neil C Schofield Equity Derivatives

Equity Derivatives Neil C Schofield Equity Derivatives Corporate and Institutional Applications Neil C Schofield Verwood, Dorset, United Kingdom ISBN 978-0-230-39106-2 ISBN 978-0-230-39107-9 (eBook) DOI 10.1057/978-0-230-39107-9 Library of Congress Control Number: 2016958283 © The Editor(s) (if applicable) and The Author(s) 2017 The author(s) has/have asserted their right(s) to be identified as the author(s) of this work in accordance with the Copyright, Designs and Patents Act 1988. This work is subject to copyright. All rights are solely and exclusively licensed by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilms or in any other physical way, and transmission or informa- tion storage and retrieval, electronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made. -

Consolidated Policy on Valuation Adjustments Global Capital Markets

Global Consolidated Policy on Valuation Adjustments Consolidated Policy on Valuation Adjustments Global Capital Markets September 2008 Version Number 2.35 Dilan Abeyratne, Emilie Pons, William Lee, Scott Goswami, Jerry Shi Author(s) Release Date September lOth 2008 Page 1 of98 CONFIDENTIAL TREATMENT REQUESTED BY BARCLAYS LBEX-BARFID 0011765 Global Consolidated Policy on Valuation Adjustments Version Control ............................................................................................................................. 9 4.10.4 Updated Bid-Offer Delta: ABS Credit SpreadDelta................................................................ lO Commodities for YH. Bid offer delta and vega .................................................................................. 10 Updated Muni section ........................................................................................................................... 10 Updated Section 13 ............................................................................................................................... 10 Deleted Section 20 ................................................................................................................................ 10 Added EMG Bid offer and updated London rates for all traded migrated out oflens ....................... 10 Europe Rates update ............................................................................................................................. 10 Europe Rates update continue ............................................................................................................. -

Introduction to Options Strategies

INTRODUCTION TO OPTIONS STRATEGIES TABLE OF CONTENTS 1. Option Investing Considerations 2. Risk / Reward Considerations 3. Directional Strategies 4. Bullish Strategies 5. Neutral Strategies 6. Bearish Strategies 7. Yield Enhancement Strategy 8. Protection Strategy 9. Risk Reversal Strategy 10. Summary OPTION INVESTING CONSIDERATIONS Success with Options Trading Depends on 5 Main Factors: Direction (Bullish / Neutral / Bearish) Magnitude (Strong View / Moderate View) Time Horizon (Maturity / Time Decay of Options) Volatility Prior to Expiration (Upward Trend / Downward Trend) Personal Risk Tolerance (Risk Adverse / Risk Seeking) RISK / REWARD CONSIDERATIONS At-The Money Out-Of-The- Money In-The Money TM Options TM Options TM Options Initial Cost Highest In-Between Lowest Highest Percentage Payout Highest Dollar Return In-Between Return Greatest Dollar Greatest Percentage Volatility Change Smallest Percentage and Impact on Option Impact on Option (Prior to Expiration) Dollar Impact on Option Price Price Price Time Decay Lowest Highest In-Between DIRECTIONAL STRATEGIES Moderately Bearish Neutral Moderately Bullish Bullish Bearish Put Spread Stock Stock Buy (Less ATM Put (Buy ATM Call Spread (Buy ATM Call Risky) OTM Put Put / Sell ATM Call / Sell OTM Call OTM Put) OTM Call) ATM Put ATM Call Stock Straddle OTM Call Stock (Sell ATM OTM Put Call Spread Sell (More ATM Call Put / ATM Put Spread (Sell ATM Put (Sell ATM Risky) ITM Call Call) ATM Put / Buy ITM Put Call / Buy Strangle OTM Put) OTM Call) (Sell OTM Put / OTM Call) -

The Billionaire Limited Risk Reversal Trade

The Billionaire Limited Risk Reversal Trade The Optionomics Group LLC Did you ever wonder how Carl Icahn and Warren Buffett are able to take over major corporations without anyone noticing until they release the forms to the SEC? Buying the stock would be obvious to the other big traders and like the “Duke Brothers” they would want in on the action. How they do it is by using options. Their staffs have a superior knowledge of the way the option market works, and they take advantage of it. Trading options is a probability model but a lot of it is common sense. The longer the time until an event can happen the greater the uncertainty. Let’s say you find a house you want to buy which is listed at $200,000. You would like to buy it today but don’t have the ready cash. You can afford a lease of $1,000 a month and you know you will have the cash for a down payment in the near future. You ask the seller if they would give you an “option” on the house. The seller agrees. You know the house is worth $200,000 today but what will it be worth in the future? You can guess, but nobody knows for sure. Let’s say that real estate values where you are living have gone up an average of 1% a year for the past 20 years, but it has been a bumpy ride because of the real estate meltdown in 2008. If you are going to look at the near term, an option premium of 1% a year should seem adequate. -

Calibrating the SABR Model to Noisy FX Data

Calibrating the SABR Model to Noisy FX Data Kellogg College University of Oxford A thesis submitted in partial fulfillment of the MSc in Mathematical Finance Hilary 2018 Abstract We consider the problem of fitting the SABR model to an FX volatility smile. It is demonstrated that the model parameter β cannot be deter- mined from a log-log plot of σATM against F . It is also shown that, in an FX setting, the SABR model has a single state variable. A new method is proposed for fitting the SABR model to observed quotes. In contrast to the fitting techniques proposed in the literature, the new method allows all the SABR parameters to be retrieved and does not require prior beliefs about the market. The effect of noise on the new fitting technique is also investigated. Acknowledgements I would like to thank both of my supervisors Dr Daniel Jones and Guil- laume Bigonzi for their guidance and support throughout this project. They provided the direction for this work and offered invaluable insight and advice along the way. I also gratefully acknowledge the financial support from Bank Julius Baer and Co. Ltd. Finally I thank Dr Beate Solleder for her love and tireless support and for tolerating me during the time it has taken me to complete this project. 1 Introduction The work presented here is concerned with fitting the SABR stochastic volatility model to foreign exchange (FX) data. Specifically, we are interested in the implied volatility of an option, σ, as a function of the strike of the option, K. This relation- ship between σ and K is known as the volatility smile. -

Practicalities of Pricing Exotic Derivatives

Practicalities of Pricing Exotic Derivatives John Crosby Grizzly Bear Capital My website is: http://www.john-crosby.co.uk If you spot any typos or errors, please email me. My email address is on my website. Lecture given 1st July 2014 for Module 4 of the M.Sc. course in Mathematical Finance at the Mathematical Institute at Oxford University. File date 11th June 2014 at 10.30 Presentation on Practicalities of Pricing Exotic Derivatives June 2014 Oxford University Motivation p 2=77 • Your course of studies has now shown you how to price several types of exotics analytically. You have studied generic pricing techniques such as Monte Carlo simulation and PDE lattice methods which can, potentially, price many different types of exotic options under many different types of stochastic processes. • So pricing exotic options is easy, right? • We are given the payoff of the exotic option by our trader. We choose our favourite stochastic process. Naturally, to show how clever we are, it has stochastic vol, stochastic skew, jumps, local volatility, stochastic interest-rates,... • We calibrate our model to the market prices of vanilla (standard European) options. Naturally, the fit to vanillas is wonderful which just reinforces how great our model must be. • We price the exotic option in question. The trader now has an arbitrage-free price - so nothing could possibly be wrong with it (!). The trader puts a bid-offer spread around our price (usually the spread is 10 per cent or more of the price). The sales person may add on a further sales margin (which may be another 10 per cent or more). -

(12) United States Patent (10) Patent No.: US 8,775,295 B2 Gershon (45) Date of Patent: *Jul

US008775295B2 (12) United States Patent (10) Patent No.: US 8,775,295 B2 Gershon (45) Date of Patent: *Jul. 8, 2014 (54) METHOD AND SYSTEM FORTRADING (56) References Cited OPTIONS U.S. PATENT DOCUMENTS (75) Inventor: David Gershon, Tel Aviv (IL) 3,933,305 A 1/1976 Murphy 5,557.517 A 9/1996 Daughterty, III (73) Assignee: Super Derivatives, Inc., New York, NY 5,806,050 A 9, 1998 Shinn et al. (US) 5,873,071 A 2/1999 Ferstenberg et al. 5,884.286 A * 3/1999 Daughtery, III ............ TOS/36 R. 5,926,801 A 7/1999 MatSubara et al. (*) Notice: Subject to any disclaimer, the term of this 5,946,667 A 8/1999 Tull, Jr. et al. patent is extended or adjusted under 35 6,016,483 A 1/2000 Rickard et al. U.S.C. 154(b) by 0 days. 6,061,662 A 5, 2000 Makivic This patent is Subject to a terminal dis (Continued) claimer. FOREIGN PATENT DOCUMENTS (21) Appl. No.: 13/168,980 JP H3-50687 A 3, 1991 JP 10-509257 9, 1998 (22) Filed: Jun. 26, 2011 (Continued) (65) Prior Publication Data OTHER PUBLICATIONS US 2011 FO270734 A1 Nov. 3, 2011 Internet Citation, “Track data announces its AIO Systems division released its option analysis”, Nov. 9, 1999, XP002958 101, retrieved on Jun. 15, 2002. Related U.S. Application Data (Continued) (63) Continuation of application No. 1 1/797.692, filed on Primary Examiner — Hani M Kazimi May 7, 2007, now Pat. No. 8,001,037, which is a continuation of application No. -

Implied Volatility Surface

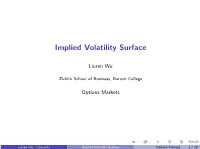

Implied Volatility Surface Liuren Wu Zicklin School of Business, Baruch College Options Markets Liuren Wu ( Baruch) Implied Volatility Surface Options Markets 1 / 25 Implied volatility Recall the BMS formula: Ft;T 1 2 r(T t) ln K ± 2 σ (T − t) c(S; t; K; T ) = e− − [Ft T N(d1) − KN(d2)] ; d1 2 = p ; ; σ T − t The BMS model has only one free parameter, the asset return volatility σ. Call and put option values increase monotonically with increasing σ under BMS. Given the contract specifications (K; T ) and the current market observations (St ; Ft ; r), the mapping between the option price and σ is a unique one-to-one mapping. The σ input into the BMS formula that generates the market observed option price (or sometimes a model-generated price) is referred to as the implied volatility (IV). Practitioners often quote/monitor implied volatility for each option contract instead of the option invoice price. Liuren Wu ( Baruch) Implied Volatility Surface Options Markets 2 / 25 The relation between option price and σ under BMS 45 50 K=80 K=80 40 K=100 45 K=100 K=120 K=120 35 40 t t 35 30 30 25 25 20 20 15 Put option value, p Call option value, c 15 10 10 5 5 0 0 0 0.2 0.4 0.6 0.8 1 0 0.2 0.4 0.6 0.8 1 Volatility, σ Volatility, σ An option value has two components: I Intrinsic value: the value of the option if the underlying price does not move (or if the future price = the current forward).