Annual Investment Report 2015-2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FTSE Factsheet

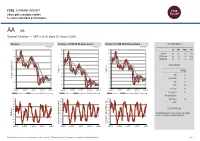

FTSE COMPANY REPORT Share price analysis relative to sector and index performance AA AA. General Retailers — GBP 0.25 at close 03 August 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 03-Aug-2020 03-Aug-2020 03-Aug-2020 0.7 140 140 1D WTD MTD YTD 130 130 Absolute 4.6 4.6 4.6 -57.0 0.6 Rel.Sector 2.4 2.4 2.4 -48.8 120 120 Rel.Market 2.5 2.5 2.5 -46.1 110 110 0.5 100 100 VALUATION 90 0.4 90 80 Trailing Relative Price Relative Relative Price Relative 80 70 0.3 PE 1.6 70 Absolute Price (local currency) (local Price Absolute 60 EV/EBITDA 8.0 60 50 0.2 PB -ve 50 40 PCF 0.7 0.1 40 30 Div Yield 2.6 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Price/Sales 0.1 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity - 100 90 90 Div Payout 4.6 90 80 80 ROE - 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 The principal activity of the Company is providing 40 RSI RSI (Absolute) service of consumer roadside assistance. -

Autumn Conference Proceedings 2015 British Society of Baking

2FWREHU $XWXPQ&RQIHUHQFH 3URFHHGLQJV %ULWLVK6RFLHW\RI%DNLQJ $IILOLDWHGWRWKH$PHULFDQ6RFLHW\RI%DNLQJ %ULWLVK6RFLHW\RI%DNLQJ $XWXPQ&RQIHUHQFH %LFHVWHU+RWHO*ROIDQG6SD2[IRUGVKLUH 7XHVGD\WKDQG:HGQHVGD\WK2FWREHU 3DSHU 6SHDNHU 3DJH 7KH%6%²3DVW3UHVHQWDQG)XWXUH -LP%URZQ 3DXO7XUQHU 3 0LNH%DJVKDZ 0D[LPLVLQJ%XVLQHVVDQG+XPDQ3RWHQWLDO 'DYLG6PDUW 8 :DVWH0DQDJHPHQWLQ)RRG0DQXIDFWXUH &DPSEHOO0XUUD\ 13 7KH&XUUHQW8.(FRQRPLF&OLPDWHIRU%XVLQHVV 'DQLHO/HH 19 7KH%,$5LVLQJ6WDU$ZDUG 1DWKDQ*LOHV 23 )UHHIURP'HYHORSPHQW %DNHU\3URGXFW,QQRYDWLRQ&KULV%URFNPDQ 27 7KH9LOODJH%DNHU\·V7UDLQLQJDQG,QQRYDWLRQ$FDGHP\5RELQ-RQHV 32 7KH6HFUHWDU\ %ULWLVK6RFLHW\RI%DNLQJ 9LQH&RWWDJH7RPSNLQV/DQH0DUVK*LEERQ %LFHVWHU2[RQ2;(; 7HO)D[(PDLOEVE#IUHHXNFRP 1 7+(%5,7,6+62&,(7<2)%$.,1* $IILOLDWHGWRWKH$PHULFDQ6RFLHW\RI%DNLQJ ([HFXWLYH&RPPLWWHH 0LNH%DJVKDZ &KDLUPDQ %ULDQ&ODUNH 3DXO7XUQHU 9LFH&KDLUPDQ 5LFKDUG+D]HOGLQH -LP%URZQ +RQ7UHDVXUHU 6\OYLD0DFGRQDOG &RQIHUHQFH&RRUGLQDWRU *RUGRQ3ROVRQ 6KDURQ%\UQH 6HFUHWDU\ -DQH7\OHU 6DUD$XWWRQ ,PPHGLDWH3DVW&KDLUPDQ 3DXO:HVWRQ 6DUD3ULHVWOH\ 6WXGHQW/LDLVRQ 0DLO&KLPS 0DUN<RXQJ 3DVW&KDLUPHQ -7KRPVRQ $%XFKDQDQ 5)HUJXVRQ +&ROERXUQH )(OOLV 3+H\JDWH )%DWHV *3ULQFH 6&DXYDLQ $+DOO 32UW 10HDGRZV -6WHYHQV '5REHUWV &/RPD[ 36KHQWRQ 51HZVWHDG 1-DFNVRQ *+XPSKUH\ 70RVV $03ROODUG :*XQVWRQH 'U3:RRG .+RXOLVWRQ '.LQJ 30DVVH\ 6$XWWRQ 5+DUH $:DWHUILHOG 7%HDOH $+RGJHV 5+XPSKUH\ -%URZQ -5LWFKLH 3:DUG 5+RUQVE\ -53DUNLQVRQ -$QWKRQ\ ,0HOOLQJ *9HUH .6KDZ '*DUUDWW 56LPPV )6D\HU *&ULWLFRV )(OOLV 30RUURZ 5)OLQW 5.LUN .6\GQH\ -*ULHYHV 3DVWQG9LFH&KDLUPHQ EHIRUHWKHQG9LFH&KDLUPDQGLGQRWSURFHHGWR VW9LFH&KDLUPDQDQG&KDLUPDQEHFDXVHKHGLGQRWZRUNIRUDEDNHU\FRPSDQ\ 36DYRU\ 57XUQHU *%UXFH .0RUJDQ -0DKOLFK .&ROOLQJH **LOEHUW 1'RXJODV 7&ROOLQV -3ULFH 6/DPEHUW -%URZQ 1%HVVDQW -+X[WDEOH ::DOODFH 56DQGHUVRQ :3ULQJOH *6FKLQGOHU -3HONPDQ '(OLDV &&XUWLV ,.LQJ .:LOOLDPVRQ -3ULQJOH &%UDFHZHOO -*UHHQILHOG 2 Paul Turner; and to then look to the future with Chairman Mike 2015 DIAMOND JUBILEE AUTUMN Bagshaw. -

The Future of Business Using Enterprise Server

Market Review Market Review Paper by Bloor Author David Norfolk Publish date June 2021 The Future of Business …using Enterprise Server 3.0 Services A company has to stay“ in business while modernising its systems and any modernisation must have a clearly documented business case and properly managed risk. What this means is that migrating a working system to a new platform may not be a good use of resources, especially as alternative modernisation options (such as the provision of cloud APIs or Application Programming Interfaces) are available. ” Executive summary he Future of Business will Well, the nub of the business issue we be largely built on the past, spotlight here is that migration to Cloud T for existing companies. is often recommended simplistically as Modernisation of what you have already, a platform for future business, almost as presumably “fit for current purpose” (or you a fashion option, with implied promises wouldn’t be in business) avoids waste and of ultimate agility, elastic capabilities mitigates certain classes of risk (although, without limits and low cost; but the if not done properly, it can add new risks). actuality is often different – and never Modernisation, of course, implies fit for quite being able to complete a migration evolution and change – once modernised, off Enterprise Server 3.0, because the you will be making further changes to business realities won’t let you, is accommodate new business. probably the most expensive scenario Modernisation of what For big enterprises, the world still runs of all. Cloud provides a wide choice of you have already,“ on very large, very resilient, servers – often platforms, some with innovative and presumably “fit for current referred to as “mainframes”, although attractive characteristics, but three truths Bloor prefers the term Enterprise Server remain important: purpose” (or you wouldn’t be in business) avoids 3.0. -

Popular Employer Names Number of Data Profiles Blackrock, Inc. 43

S.No Popular Employer Names Number of Data Profiles 1. Blackrock, Inc. 43 2. BMC Software, Inc. 55 3. BNP Paribas Inc. 113 4. BRISTLECONE India Ltd 57 5. British Telecom 131 6. Broadcom Corporation 59 7. Broadridge Financial Solutions, Inc. 44 8. Bureau Veritas 47 9. CA Technologies 65 10. CA, Inc. 39 11. Cairn India 45 12. Calsoft Pvt Ltd 44 13. Capgemini 1,309 14. Capgemini Consulting 578 15. Capita india 82 16. Capital Iq, Inc. 41 17. Caterpillar, Inc. 75 18. CBRE Group 60 19. CenturyLink 47 20. Cerner Corporation 65 21. CGI Group Inc. 300 22. Cipla Medpro Manufacturing 43 23. Cisco Systems (India) Private Limited 57 24. Cisco Systems Inc 396 25. Citibank 235 26. Citigroup, Inc. 53 27. CitiusTech 59 28. Citrix Systems Inc 40 29. CMC Group 102 30. Cognizant 1,374 31. Cognizant Technology Solutions Corp 1,715 32. Collabera Inc. 74 33. Computer Sciences Corporation (CSC) 653 34. Concentrix Corporation 159 35. Convergys Corporation 113 36. Credit Suisse 90 37. Crisil 117 38. CTS Corporation 109 39. Cummins India Ltd 70 40. Cvent, Inc. 46 41. Cybage 201 42. Daimler India Commercial Vehicles Pvt Ltd 61 43. Dell, Inc. 516 44. Deloitte 414 45. Deloitte & Touche LLP 107 46. Deloitte Consulting LLP 282 47. Deloitte Support Services India Private Ltd 94 48. Deloitte Touche Tohmatsu (DTT) 79 49. Deutsche Bank 235 50. Dimension Data 63 51. Directi 44 52. Dr Reddy's Laboratories Ltd 85 53. Dun & Bradstreet Corp 50 54. E.I. Du Pont De Nemours & Co (DuPont) 47 55. -

Sponsorship (Opportunities for Participation)

Sponsorship (Opportunities for partiCipation) Connect with Asia’s largest Agile and Lean Software Conference delegates. Naresh Jain, Chair and Sponsor liaison [email protected] Presented by http://2014.agileindia.org 1/30/14 ©2014, Agile Software Community of India. 1 WelCome to Agile India 2014 Following the grand success of Agile India 2013 and Agile India 2012 Conferences, the Agile Software Community of India (ASCI) is planning a muCh bigger event, with more than 100 Sessions over 4 days. Similar to last year, we plan to bring together thought leaders from all over the globe to India. The Indian software development Community is a hotbed for Agile and Lean movement. Number of organizations embraCing Agile is growing exponentially over the last 6 years. As there organizations are implementing Agile, they are faCed with many Questions and Challenges. This conference creates an exceptional opportunity for developers, testers, managers, exeCutives, and those who Care about the software industry to Come together to have the Conversations neCessary to push the movement forward. Join us! ASCI expeCts to host up to 1500 passionate attendees in Bengaluru, India, on February 26 – MarCh 1, 2014. SpeCial events are planned to showCase this grand, international ConferenCe on Agile Software Development. Your presenCe with us will help Create an international event. I invite you to partiCipate and tell your story at this international gathering. This is an opportunity to stand out on an international stage. Naresh Jain Founder & Conference Chair Agile Software Community of India http://agileindia.org http://2014.agileindia.org 1/30/14 ©2014, Agile Software Community of India. -

Full Property Address Primary Liable

Full Property Address Primary Liable party name 2019 Opening Balance Current Relief Current RV Write on/off net effect 119, Westborough, Scarborough, North Yorkshire, YO11 1LP The Edinburgh Woollen Mill Ltd 35249.5 71500 4 Dnc Scaffolding, 62, Gladstone Lane, Scarborough, North Yorkshire, YO12 7BS Dnc Scaffolding Ltd 2352 4900 Ebony House, Queen Margarets Road, Scarborough, North Yorkshire, YO11 2YH Mj Builders Scarborough Ltd 6240 Small Business Relief England 13000 Walker & Hutton Store, Main Street, Irton, Scarborough, North Yorkshire, YO12 4RH Walker & Hutton Scarborough Ltd 780 Small Business Relief England 1625 Halfords Ltd, Seamer Road, Scarborough, North Yorkshire, YO12 4DH Halfords Ltd 49300 100000 1st 2nd & 3rd Floors, 39 - 40, Queen Street, Scarborough, North Yorkshire, YO11 1HQ Yorkshire Coast Workshops Ltd 10560 DISCRETIONARY RELIEF NON PROFIT MAKING 22000 Grosmont Co-Op, Front Street, Grosmont, Whitby, North Yorkshire, YO22 5QE Grosmont Coop Society Ltd 2119.9 DISCRETIONARY RURAL RATE RELIEF 4300 Dw Engineering, Cholmley Way, Whitby, North Yorkshire, YO22 4NJ At Cowen & Son Ltd 9600 20000 17, Pier Road, Whitby, North Yorkshire, YO21 3PU John Bull Confectioners Ltd 9360 19500 62 - 63, Westborough, Scarborough, North Yorkshire, YO11 1TS Winn & Co (Yorkshire) Ltd 12000 25000 Des Winks Cars Ltd, Hopper Hill Road, Scarborough, North Yorkshire, YO11 3YF Des Winks [Cars] Ltd 85289 173000 1, Aberdeen Walk, Scarborough, North Yorkshire, YO11 1BA Thomas Of York Ltd 23400 48750 Waste Transfer Station, Seamer, Scarborough, North Yorkshire, -

Tokyo Food Technology Week 2021

Exhibit Brochure Tokyo Food Technology Week 2021 Sep. 2-3 2021 Sep. 2-3 2021 10:00~17:00 PACIFICO YOKOHAMA Exhibition Hall C [Website] https://tokyofoodtechnology.com/2021/en.pdf Organizer:EJK Japan, Ltd./ The Japan Food News Show profile The Gateway into Japan Market ! Tokyo Food Technology Week “Tokyo Food Technology Week” will be expandingly held by including “P & B JAPAN”, “Nutritious Food Ingredients EXPO”, and “food ingredients EXPO for Pre-packaged, Frozen, and Instant food”. TFTW creates the synergistic effect of 3 shows by proposing the cutting- edge technology that shows new trends in the whole food industry. LOGO nd NAME OF 2 Nutritious Food 1st food ingredients EXPO for Pre- 9th P&B JAPAN (P&B) SHOW Ingredients EXPO (NFI) packaged, Frozen, and Instant food (PFI) ORGANIZER(S) EJK Japan, Ltd. EJK Japan, Ltd./ The Japan Food News Food ingredients for bread Health functional food Food Ingredients (meat, & confectionery (flour, oil, ingredients (vitamin & sea food, vegetable, fruit, yeast, jam, honey, frozen mineral, oligo sugar, food cereal, seasoning, spice, dough, etc. ) / Food fiber, lactic acid bacteria, herb etc.) / Food additives ingredients for sandwich, sugar alcohol, protein, / Professional products for EXHBITOR burger (meat, vegetable, amino acid, enzyme, etc.) restaurant chain / Food PROFILE dairy product, sauce, etc. ) Vegetable / Herb / Honey processing technology / Coffee & tea & beverages product / Soy product / (freezing, thawing, / Kitchen equipment / POS Component analysis / sterilizer drying etc. )/ register -

NACD Public Company Full Board Members

NACD Public Company Full Board Members: Rank | Company Rank | Company Rank | Company Rank | Company A.O. Smith Corp. Analog Devices Bridge Housing Corporation Clearwire Corp. AAA Club Partners Ansys, Inc. Briggs & Stratton Corp. Cliffs Natural Resources Inc. AARP Foundation Apogee Enterprises, Inc. Brightpoint, Inc. Cloud Peak Energy Inc. Aastrom Biosciences, Inc. Apollo Group, Inc. Bristow Group Inc. CME Group Acadia Realty Trust Applied Industrial Technologies, Broadwind Energy CoBiz, Inc. ACI Worldwide, Inc. Inc. Brookdale Senior Living Inc. Coherent, Inc. Acme Packet, Inc. Approach Resources, Inc. Bryn Mawr Bank Corporation Coinstar, Inc. Active Power, Inc. ArcelorMittal Buckeye Partners L.P. Colgate-Palmolive Co. ADA-ES, Inc. Arch Coal, Inc. Buffalo Wild Wings, Inc. Collective Brands, Inc. Adobe Systems, Inc. Archer Daniels Midland Co. Bunge Limited Commercial Metals Co. Advance Auto Parts ARIAD Pharmaceuticals, Inc. CA Holding Community Health Systems Advanced Energy Industries, Inc. Arkansas Blue Cross Blue Shield CACI International, Inc. Compass Minerals Aerosonic Corp. Arlington Asset Investment Corp. Cal Dive International, Inc. Comverse Technology, Inc. Aetna, Inc. Arthur J. Gallagher & Co. Calamos Asset Management, Inc. Conmed Corp. AFC Enterprises, Inc. Asbury Automobile Cameco Corp. Connecticut Water Service, Inc. AG Mortgage Investment Trust Inc. Aspen Technology, Inc. Cameron ConocoPhillips Agilent Technologies Associated Banc-Corp.5 Campbell Soup Co. CONSOL Energy Inc. Air Methods Corp. Assurant, Inc. Capella Education Co. Consolidated Edison Co. Alacer Gold Corp. Assured Guaranty Ltd. Capital One Financial Corp. Consolidated Graphics, Inc. Alaska Air Group, Inc. ATMI Capstead Mortgage Corp. Consolidated Water Co., Ltd. Alaska Communication Systems Atwood Oceanics, Inc. Cardtronics, Inc. Continental Resources, Inc. Group, Inc. Auxilium Pharmaceuticals Inc. -

UK Annual Report 2015 (Including the Transparency Report)

Investing to become the Clear Choice UK Annual Report 2015 (including the Transparency Report) December 2015 KPMG.com/uk Highlights Strategic report Profit before tax and Revenue members’ profit shares £1,958m £383m (2014: £1,909m) (2014: £414m) +2.6% -7% 2013 2014 2015 2013 2014 2015 Average partner Total tax payable remuneration to HMRC £623k £786m (2014: £715K) (2014: £711m) -13% +11% 2013 2014 2015 2013 2014 2015 Contribution Our people UK employees KPMG LLP Annual Report 2015 Annual Report KPMG LLP 11,652 Audit Advisory Partners Tax 617 Community support Organisations supported Audit Tax Advisory Contribution Contribution Contribution £197m £151m £308m (2014: £181m) (2014: £129m) (2014: £324m) 1,049 +9% +17% –5% (2014: 878) © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Strategic report Contents Strategic report 4 Chairman’s statement 10 Strategy 12 Our business model 16 Financial overview 18 Audit 22 Solutions 28 International Markets and Government 32 National Markets 36 People and resources 40 Corporate Responsibility 46 Our taxes paid and collected 47 Independent limited assurance report Governance 52 Our structure and governance 54 LLP governance 58 Activities of the Audit & Risk Committee in the year 59 Activities of the Nomination & Remuneration Committee in the year KPMG in the UK is one of 60 Activities of the Ethics Committee in the year 61 Quality and risk management the largest member firms 2015 Annual Report KPMG LLP 61 Risk, potential impact and mitigations of KPMG’s global network 63 Audit quality indicators 66 Statement by the Board of KPMG LLP providing Audit, Tax and on effectiveness of internal controls and independence Advisory services. -

Proptech 3.0: the Future of Real Estate

University of Oxford Research PropTech 3.0: the future of real estate PROPTECH 3.0: THE FUTURE OF REAL ESTATE WWW.SBS.OXFORD.EDU PROPTECH 3.0: THE FUTURE OF REAL ESTATE PropTech 3.0: the future of real estate Right now, thousands of extremely clever people backed by billions of dollars of often expert investment are working very hard to change the way real estate is traded, used and operated. It would be surprising, to say the least, if this burst of activity – let’s call it PropTech 2.0 - does not lead to some significant change. No doubt many PropTech firms will fail and a lot of money will be lost, but there will be some very successful survivors who will in time have a radical impact on what has been a slow-moving, conservative industry. How, and where, will this happen? Underlying this huge capitalist and social endeavour is a clash of generations. Many of the startups are driven by, and aimed at, millennials, but they often look to babyboomers for money - and sometimes for advice. PropTech 2.0 is also engineering a much-needed boost to property market diversity. Unlike many traditional real estate businesses, PropTech is attracting a diversified pool of talent that has a strong female component, representation from different regions of the world and entrepreneurs from a highly diverse career and education background. Given the difference in background between the establishment and the drivers of the PropTech wave, it is not surprising that there is some disagreement about the level of disruption that PropTech 2.0 will create. -

FORM 10-K Costar Group, Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE ☐ SECURITIES EXCHANGE ACT OF 1934 For the transition period from ______ to ______ Commission file number 0-24531 CoStar Group, Inc. (Exact name of registrant as specified in its charter) Delaware 52-2091509 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 1331 L Street, NW Washington, DC 20005 (Address of principal executive offices) (zip code) (202) 346-6500 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of each exchange on which registered Common Stock ($0.01 par value) CSGP Nasdaq Global Select Market Securities registered pursuant to section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. -

Find Your Nearest Site

Find your nearest site Scotland Northern Ireland North East Isle of Man Yorkshire and the Humber North West East Midlands Wales West Midlands East of England Greater London South West South East East Midlands Site name Phone number Address Town/City Post code PRESTIGE - PROMECH GARAGE SERVICES 01664 503467 UNIT 3B ARNOLD NG5 7FJ PRESTIGE - AUTOMOTO CAR CARE CENTRE 01664 503467 33-41 HIGH ROAD BEESTON NG9 4AF STONEACRE PETERBOROUGH BOONGATE 01405 744192 FORTY ACRE ROAD BOONGATE PE1 5PS PRESTIGE - BOSTON TYRE & AUTO CENTRE 01664 503467 46 FYDELL STREET BOSTON PE21 8LF VERTU HONDA BOSTON 1 MARSH LANE BOSTON PE21 7QS NTA COALVILLE LEICS (503) 01530 834321 26 ASHBY ROAD COALVILLE LE67 3LA PRESTIGE - ANDERSON COMMERCIALS LTD 01664 503467 UNIT 7-8 SOUTH STREET COALVILLE LE67 1EU NTA CORBY NORTHANTS (495) 01536 203508 LLOYDS ROAD CORBY NN17 1AW PRESTIGE - CORBY CAR CARE CENTRE 01664 503467 3 CURIE COURTYARD CORBY NN17 5DU PRESTIGE - M & A CARS LTD 01664 503467 11 WHITTLE ROAD CORBY NN17 5DX HALFORDS GRANTHAM (677) 01476 591435 LONDON ROAD GRANTHAM NG31 6HS NTA GRANTHAM (655) 01476 575887 68 LONDON ROAD GRANTHAM NG31 6HR PRESTIGE - GRANTHAM SERVICE & MOT CENTRE 01664 503467 UNIT 1 ALMA PARK ROAD GRANTHAM NG31 9SE STONEACRE GRANTHAM 01405 744192 TOLLEMACHE ROAD SOUTH GRANTHAM NG31 7UH HALFORDS NOTTINGHAM HUCKNALL (210) 0115 963 8825 UNIT 4 CHRISTOPHER COURT HUCKNALL NG15 6EP PRESTIGE - ROMANS TYRES & EXHAUST LTD 01664 503467 11 STONEHILL HUNTINGDON PE29 6ED HALFORDS KETTERING (005) 01536 410421 TRAFALGAR ROAD KETTERING NN16 8DB PRESTIGE - SIGNATURE