City Budget 2011-2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A TIMELINE for GOLDEN, COLORADO (Revised October 2003)

A TIMELINE FOR GOLDEN, COLORADO (Revised October 2003) "When a society or a civilization perishes, one condition can always be found. They forgot where they came from." Carl Sandburg This time-line was originally created by the Golden Historic Preservation Board for the 1995 Golden community meetings concerning growth. It is intended to illustrate some of the events and thoughts that helped shape Golden. Major historical events and common day-to-day happenings that influenced the lives of the people of Golden are included. Corrections, additions, and suggestions are welcome and may be relayed to either the Historic Preservation Board or the Planning Department at 384-8097. The information concerning events in Golden was gathered from a variety of sources. Among those used were: • The Colorado Transcript • The Golden Transcript • The Rocky Mountain News • The Denver Post State of Colorado Web pages, in particular the Colorado State Archives The League of Women Voters annual reports Golden, The 19th Century: A Colorado Chronicle. Lorraine Wagenbach and Jo Ann Thistlewood. Harbinger House, Littleton, 1987 The Shining Mountains. Georgina Brown. B & B Printers, Gunnison. 1976 The 1989 Survey of Historic Buildings in Downtown Golden. R. Laurie Simmons and Christine Whitacre, Front Range Research Associates, Inc. Report on file at the City of Golden Planning and Development Department. Survey of Golden Historic Buildings. by R. Laurie Simmons and Christine Whitacre, Front Range Research Associates, Inc. Report on file at the City of Golden Planning and Development Department. Golden Survey of Historic Buildings, 1991. R. Laurie Simmons and Thomas H. Simmons. Front Range Research Associates, Inc. -

Proxy Statement Pursuant to Section 14(A) of the Securities Exchange Act of 1934 (Amendment No

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant Filed by a Party other than the Registrant Check the appropriate box: Preliminary Proxy Statement Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) Definitive Proxy Statement Definitive Additional Materials Soliciting Material under §240.14a-12 MOLSON COORS BEVERAGE COMPANY (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): No fee required. Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: Fee paid previously with preliminary materials. Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: P.O. -

Adolph COORS Company and Its Unincorporated Affiliate, Coors

,•, UNITED STATES ENVIRONMENTAL PROTECTION AGENCY .SEFORE THE ADMINISTRATOR. In the Matter of ) ) Adolph ·~~ors company ) Docket No. RCRA-VIII-90-09 '• and i't.s unincorporated ) aftil~ate, ) coors Brewing company, ) ··........ ) R~spondent ) ·~. ORDER DENYING MOTIONS FOR AN ACCELERATED DECISION AND TO DISMISS The complaint in this proceeding under section 3008 of the Solid Waste Disposal Act, as amended (42 u.s. C. § 6928), commonly referred to as RCRA, issued on June 19, 1990, charged ·Respondent Coors with violations of the Act and applicable regulations. Specifically, Count I charged Coors with disposal of hazardous waste without a permit during the period october 1981 to .. August 1984, to-wit: spent solvents 1,1,1-Trichloroethane (TCA) ..... ··; . .. : and Tetrachloroethylene (PCE) . designated as FOOl and F002, --·-· ... respectively, in the list of hazardous wastes appearing in 40 CFR ,· .. -~;i:-:.::."§ 261.31. The disposal allegedly occurred through leaks from sewer ,' ·~. ' _·-;:~ ;iines beneat~ Coors• container plant. count II charged Coors with .t· '- .f '·· · · <' :· · failure ·t.o . truthfully disclose information re~ired by 40 CFR § § 270.10(d) and 270.30(1~) and Count III charged Coors with failing to truthfully disclose information required by an EPA ncall-in" letter. Count IV charged Coors with failing to certify its 2 response to an EPA section 3007(a) information request as required by 40 CFR § 270.ll(d). In its answer and request for a hearing, dated July 24, 1990, Coors, among other things, denied that it allowed solvents identified in the complaint to leak from sewer lines at its container plant and alleged that upon discovery of an unanticipated sewer line failure it took steps to prevent leakage from the sewer line and to mitigate the effects of such leakage. -

2019 Annual Financial Report

Comprehensive Annual Financial Report For the Year Ended December 31, 2019 Golden, Colorado CITY OF GOLDEN, COLORADO COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR YEAR ENDED DECEMBER 31, 2019 Jason T. Slowinski City Manager Prepared by the Finance Department Jeffrey A. Hansen Finance Director City of Golden, Colorado Comprehensive Annual Financial Report For the Fiscal Year Ended December 31, 2019 TABLE OF CONTENTS Page INTRODUCTORY SECTION Letter of Transmittal ................................................................................................................. i List of Elected and Appointed Officials ................................................................................ vii Organizational Chart ............................................................................................................. viii GFOA Certificate of Achievement ......................................................................................... ix FINANCIAL SECTION Independent Auditors’ Report .................................................................................................. 1 Management’s Discussion and Analysis ................................................................................. 3 Basic Financial Statements: Government-wide Financial Statements: Statement of Net Position ............................................................................................. 15 Statement of Activities .................................................................................................. 16 Fund Financial -

View Annual Report

Adolph Coors Company Annual Report Coors Company 1999 Adolph Adolph Coors Company Golden, Colorado 80401, (303) 279-6565 1999 Annual Report Ready for Better another round. than ever. ADOLPH COORS COMPANY ave you ever been to the Colorado Rocky Mountains? Investor Information range of topics of interest to our customers, investors, neighbors and other stakeholders. Simply call the Coors Consumer Information Center at (800) 642-6116. It’s different here. People are more relaxed. Friendly. Annual Shareholders’ Meeting The Company will hold its Annual Meeting of Shareholders Transfer Agent starting at 2:00 p.m. on Thursday, May 11, 2000, in the Sixth- BankBoston N.A., 150 Royall Street, Canton, Massachusetts The air is cool and crisp, clear and clean. Back in floor Auditorium, located in the Brewery Office Complex, 02021, (781) 575-3400. H Coors Brewing Company, Golden, Colorado. 1873, Adolph Coors knew this would be a special place to Stock Information Shareholder Relations Adolph Coors Company Class B common stock is traded on Questions about stock ownership and dividends should be the New York Stock Exchange and is listed under the ticker brew beer. Today, he’d be proud to see that the beers that directed to Ann Boe in Shareholder Relations, (303) 277-3466. symbol “RKY.” Daily stock prices are listed in major newspapers, Shareholders may obtain a copy of the Company’s 1999 Annual generally alphabetically under “Coors B.” Report on Form 10-K filed with the Securities and Exchange Dividends on common stock have historically been paid in carry his name embody the unique spirit of the Rockies. -

View Annual Report

Adolph Coors Company Adolph Coors Company Adolph Coors Company 2002 Annual Report Golden, Colorado 80401 (303) 279-6565 www.coors.com To be the 2002 Annual Report BEST ADOLPH COORS COMPANY 1 Investor Information To be the BEST Annual Informational Meeting for Shareholders Transfer Agent The Company will hold its Annual Informational Meeting for EquiServe Trust Company, N.A., Shareholder Services, in the beer business. Shareholders starting at 2:00 p.m. on Thursday, August 14, 150 Royall Street, Canton, Massachusetts 02021, 2003, in the Sixth-floor Auditorium, located in the Brewery (781) 575-3400. Office Complex, Coors Brewing Company, Golden, Colorado. It’s like a long climb up a tall and Stock Information Shareholder Relations Adolph Coors Company Class B common stock is traded difficult mountain. It’s exhilarating, Questions about stock ownership and dividends on the New York Stock Exchange and is listed under the should be directed to Kay Guthrie in Shareholder Relations, ticker symbol “RKY.” Daily stock prices are listed in major but it’s hard work that requires (303) 277-7759. Shareholders may obtain a copy of the newspapers, generally alphabetically under “Coors B.” Company’s 2002 Annual Report on Form 10-K filed with Dividends on common stock have historically been paid absolute focus. the Securities and Exchange Commission by visiting our in the months of March, June, September and December to Web site, www.coors.com; writing to the Coors Consumer shareholders of record on the last day of the preceding month. The climb accelerated as we trans- Information Center, Mail No. NH475, Adolph Coors Company, Shareholders of record as of February 28, 2003: 2,963. -

A D O L P H C O O R S C O M P a N Y 1 9 9 8 a N N U a L R E P O

ADOLPH COORS COMPANY 1998 ANNUAL REPORT CORPORATE PROFILE ABOUT THE COVER Adolph Coors Company, founded in 1873, is ranked among The connection between Coors the 675 largest publicly traded corporations in the United States. Its principal subsidiary is Coors Brewing Company, the nation’s and the Rocky Mountains is genuine, third-largest brewer. setting Coors apart from all other major Throughout its history, Coors has provided consumers with brewers. It's a powerful association high-quality malt beverages produced using an all-natural brewing that is valued by consumers because process and the finest ingredients available. The company’s it conveys Coors' commitment to produce portfolio of products, primarily premium and above-premium beers, includes Coors Light – the fourth-largest-selling beer in the highest quality malt beverages that the nation, Original Coors, George Killian’s Irish Red, Zima, Blue are as crisp, cold and refreshing as Moon specialty beers and Keystone popular-priced beers. Coors the Rockies. products are available throughout the United States and in about 30 international markets. The corporate headquarters and primary brewery are in Golden, Colorado, with other major brewing and packaging facilities in Elkton, Virginia; Memphis, Tennessee; and Zaragoza, Spain. In addition, Coors owns major aluminum can and end manufacturing facilities in Golden and is a partner in the joint venture that operates these plants. Coors is also a partner in a joint venture that owns and operates a glass bottle manufacturing plant in Colorado. -

Front Rangenews

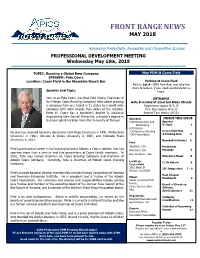

FRONT RANGE NEWS MAY 2018 Advancing Productivity, Innovation and Competitive Success PROFESSIONAL DEVELOPMENT MEETING Wednesday May 16th, 2018 TOPIC: Running a Global Beer Company Test MayYour PDM Skill @ andCoors Win Field Prizes SPEAKER: Pete Coors Location: Coors Field in the Mountain Ranch Bar Parking at Coors Field Park in Lot A (1694 Park Ave) and take the stairs to Gate A, if you need assistance let us Speaker and Topic: know. Join us as Pete Coors (yes that Pete Coors; Chairman of ENTRANCE the Molson Coors Brewing Company) talks about growing Gate B located at 22nd and Blake Streets a company from one brand in 11 states to a world wide Registration opens @ 5:15 company with more brands than colors of the rainbow. First Tour begins @ 5:30 Peter H. Coors has a bachelor’s degree in industrial Second Tour begins @5:50 engineering from Cornell University, a master’s degree in INSIDE THIS ISSUE business administration from the University of Denver. Schedule 5:30 Registration and Speaker Networking & Topic 1 6:30 Dinner He also has received honorary doctorates from Regis University in 1991, Wilberforce 7:30 Business Meeting Coors Field Map & Parking Info 2 TheUniversity in 1992, Johnson & Wales University in 1997, and Colorado State 7:45 Presentation University in 2011. Baseball in Denver 3 Fees Students: $10 Presidents Pete’s professional career in the brewing business follows a Coors tradition that has Members: $30 Message 4 spanned more than a century and five generations of Coors family members. In Non-members: $35 2002, Pete was named chairman of, Coors Brewing Company and chairman of Education News 5 Adolph Coors Company. -

Molson Coors Brewing Co

MOLSON COORS BREWING CO FORM 8-K (Unscheduled Material Events) Filed 6/2/2000 For Period Ending 5/11/2000 Address P.O. BOX 4030, MAIL #NH375 GOLDEN, Colorado 80401 Telephone 303-277-3271 CIK 0000024545 Industry Beverages (Alcoholic) Sector Consumer/Non-Cyclical Fiscal Year 12/28 U.S. SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported): May 11, 2000 ADOLPH COORS COMPANY (Exact name of registrant as specified in its charter) COLORADO 0-8251 84-0178360 (State or other jurisdiction of (Commission File No.) (I.R.S. Employer incorporation or organization) Identification No.) Golden, Colorado 80401 (Address of principal executive offices) (Zip Code) 303-279-6565 (Registrant's telephone number, including area code) Not applicable (Former name or address, if changed since last report) PART II. OTHER INFORMATION Item 5. Other Events On May 11, 2000, Adolph Coors Company (ACC) issued a news release announcing changes to certain Board of Directors and top management positions at ACC and the Company's principal subsidiary, Coors Brewing Company (CBC). ACC's May 11, 2000 news release is attached hereto as Exhibit 1. Item 7. Financial Statements and Exhibits (c) Exhibits 1. News Release of Adolph Coors Company dated May 11, 2000. Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized. ADOLPH COORS COMPANY By /s/ M. -

Adolph Coors

ADOLPH COORS When: 1847–1929 Where: Born in Germany, settled in Golden, Colorado. Why Important: Adolph Coors founded the very successful Coors Brewing Company. His success through hard work and ingenuity is a good example of the American Dream. Adolph Coors and family members. “Coors: History.” http://www.coors.com/#/history ADOLPH COORS Adolph Herrman Kohrs, who later changed his surname to Coors, was born in Germany in 1847. To help his family earn money, Coors worked as a printer’s assistant when he was young. Coors became an apprentice at a brewery in Germany when he was fifteen. As an apprentice, he learned how to make beer from the master brewer and how to run a successful brewery. When he was twenty-one years old, Coors immigrated to the United States. He stowed away on a ship headed to Baltimore, Maryland. When he arrived, he had no money and could not speak any English. He decided to head West in search of new opportunities. In 1872 Coors came to Denver, Colorado. He worked as a gardener and a manager of a bottle plant six days a week. Coors worked hard and saved his money hoping to open his own brewery. His hard work had paid off by 1873. Coors went into business with Jacob Schueler. They bought an old tannery building and opened the Golden Brewery. Coors took over as owner of the company in 1880 and renamed it Coors Golden Brewery. He had dreamed of brewing the “perfect beer” and had widespread success with the beer he brewed in Golden. -

FORM 10-K Molson Coors Brewing Company

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 _______________________________________________________________ FORM 10-K (Mark One) ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 OR o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ______ to ______ . Commission File Number: 1-14829 Molson Coors Brewing Company (Exact name of registrant as specified in its charter) DELAWARE 84-0178360 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 1801 California Street, Suite 4600, Denver, Colorado 80202 1555 Notre Dame Street East, Montréal, Québec, Canada H2L 2R5 (Address of principal executive offices) (Zip Code) 303-927-2337 (Colorado) 514-521-1786 (Québec) (Registrant's telephone number, including area code) _______________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Name of each exchange Title of each class on which registered Class A Common Stock, $0.01 par value New York Stock Exchange Class B Common Stock, $0.01 par value New York Stock Exchange Senior Floating Rate Notes due 2019 New York Stock Exchange 1.25% Senior Notes due 2024 New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ý NO o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. -

Chapter 1: Understanding Sport Sponsorship

Chapter 1: Understanding Sport Sponsorship Introduction Sponsorship, in its essence, is based on a mutual exchange between a sport entity and a corporation (Copeland, Frisby, & McCarville, 1996; McCarville & Copeland, 1994). This reliance on exchange theory suggests that both entities can simultaneously provide and receive benefits. Thus, a symbiotic relationship can be attained. In the case of adidas‘ sponsorship of the New Zealand All Blacks rugby team, Motion, Leitch, and Brodie (2003, p. 1083) noted ―in sponsorship both the sponsor and the sponsored activity become involved in a symbiotic relationship with a transference of inherent values from the activity to the sponsor.‖ In the United States and many other nations, sport organizations have aggressively marketed themselves to sponsors in an effort to obtain the funds necessary to operate programs. Seaver‘s research with 50 of the top US sponsors indicated that 10% of sponsoring companies get more than 1300 proposals per year (Seaver, 2004). North American 2008 sponsorship spending was projected to reach $16.78 billion, up 12.6% over 2007. Contributing to this total were several companies that spent over $100 million each on sponsorship programs (IEG, 2007). Among the top spending corporations: $330-335 million - Anheuser-Busch $305-310 million - Pepsi $230-235 million - General Motors $225-230 million - Coca-Cola $225-230 million - Nike $175-180 million - Miller $150-155 million - Daimler-Chrysler $140-145 million - Ford $115-120 million - McDonalds $110-115 million - MasterCard The major areas of the economy where sponsorship spending is apportioned have been noted below (IEG, 2007): Sports - 69% Entertainment and Tours - 10% Cause Marketing - 9% Arts - 5% Festivals/Fairs - 4% Associations and Member Organizations - 3% Financial expenditures on sponsorship activities were not limited to North America.