Trucking Industry Update – January 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Talking Tesla Elon Musk

Bridge to Someday Top 10 of 2017 Waiting for a new U.S. crossing PG. 10 Products that topped our list PG. 36 The Business Magazine of Canada’s Trucking Industry EVERYONE’S TALKING TESLA W 5C4. Will it be the game changer? January 2018 www.todaystrucking.com plus Yard Dogs Tools to keep your trailers rolling Sleep Well Canadian Mail Sales Product Agreement #40063170. Return postage guaranteed. Newcom Media Inc., 451 Attwell Dr., Toronto, ON M9 Researchers fascinated by fatigue Contents January 2018 | VOLUME 32, NO.1 5 Letters 7 John G. Smith 10 16 9 Rolf Lockwood 31 Mike McCarron NEWS & NOTES Dispatches 13 MacKinnon Sold Ontario fleet sold to Contrans 22 Heard on the Street 32 36 23 Logbook 24 Truck Sales 25 Pulse Survey 26 Stat Pack 27 Trending 30 Truck of the Month In Gear 44 Yard Dogs Features Keep trailers moving in the yard with 10 Bridge to Someday specialized equipment Work on the Gordie Howe International 48 Southern Stars Bridge continues, but at a slow pace By Elizabeth Bate Cabovers gaining ground in Mexico 16 Talking Tesla 51 Product Watch Elon Musk (partially) unveils his electric truck. 52 Guess the location, Will it be the game changer he promises? By John G. Smith win a hat 32 Sleep Well Good health begins with proper sleep. Researchers want to know if drivers are getting what they need. By Elizabeth Bate 36 The Top 10 Here’s the tech that topped our editor’s list in 2017 By John G. Smith Cover Image: Courtesy of Tesla For more visit www.todaystrucking.com JANUARY 2018 3 BORN TO BE Designed with decades of experience BETTER. -

1 in the United States District Court for the Northern

Case: 1:11-cv-01983 Document #: 1 Filed: 03/22/11 Page 1 of 22 PageID #:1 IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF ILLINOIS CHICAGO DIVISION PJC LOGISTICS, LLC, : : Plaintiff : : v. : Civil Case No. 11-cv-1983 : A&R LOGISTICS, INC.; ACE HARDWARE : JURY TRIAL DEMANDED CORPORATION; ALLIED VAN LINES, INC.; : ATLAS VAN LINES, INC.; BEST WAY : EXPRESS, INC.; BULKMATIC TRANSPORT : COMPANY; CARDINAL TRANSPORT, INC.; : CARTER EXPRESS, INC.; CELADON GROUP, : INC.; CENTRAL TRANSPORT NORTH : AMERICA, INC.; CON-WAY FREIGHT, INC.; : CON-WAY, INC.; DAWES TRANSPORT, INC.; : deBOER TRANSPORTATION, INC.; DO IT : BEST CORP.; DOHRN TRANSFER COMPANY; : EARL L. HENDERSON TRUCKING COMPANY; : EQUITY TRANSPORTATION COMPANY, INC.; : G & F TRUCKING LEASING, INC.; GULLY : TRANSPORTATION, INC.; H.O. WOLDING, : INC.; JBS LOGISTICS, INC.; JOHNSON : TRUCKING OF NEENAH, INC.; MARTEN : TRANSPORTS, LLC; THE MASON AND DIXON : LINES, INCORPORATED; NORTH AMERICAN : VAN LINES, INC.; ORMSBY TRUCKING, INC.; : POINT DEDICATED SERVICES, LLC; R&M : TRUCKING CO.; ROADRUNNER : TRANSPORTATION SERVICES, INC.; ROEHL : TRANSPORT, INC.; RUSH TRUCKING : CORPORATION; SCHNEIDER NATIONAL : CARRIERS, INC.; STANDARD FORWARDING, : LLC; SUPER SERVICE, LLC; THOMASON : EXPRESS, LLC; TRANSPORTATION : SERVICES, INC. (TSI); UNIVERSAL : TRUCKLOAD SERVICES, INC.; USF : HOLLAND, INC.; and VENTURE LOGISTICS : SERVICES, INC. : : Defendants. : : 1 Case: 1:11-cv-01983 Document #: 1 Filed: 03/22/11 Page 2 of 22 PageID #:2 COMPLAINT Plaintiff PJC Logistics LLC (“PJC Logistics” or “Plaintiff), by way of Complaint against defendants A&R Logistics, Inc.; Ace Hardware Corporation; Allied Van Lines, Inc.; Atlas Van Lines, Inc.; Best Way Express, Inc.; Bulkmatic Transport Company; Cardinal Transport, Inc.; Carter Express, Inc.; Celadon Group, Inc.; Central Transport North America, Inc.; Con-Way Freight, Inc.; Con-Way, Inc.; Dawes Transport, Inc.; deBoer Transportation, Inc.; Do It Best Corp.; Dohrn Transfer Company; Earl L. -

Transportation & Logistics

TRANSPORTATION & LOGISTICS INDUSTRY UPDATE │ JUNE 2017 www.harriswilliams.de Harris Williams & Co. Ltd is a private limited company authorised and regulated by the Financial Conduct Authority, incorporated under English law with its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales under company number 7078852. Directors: Mr. Ned Valentine, Mr. Paul Poggi, Mr. Thierry Monjauze and Mr. Aadil Khan. Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the Local Court (Amtsgericht) of Frankfurt am Main, Germany, under registration number HRB 96687, having its business address at Bockenheimer Landstrasse 33-35, 60325 Frankfurt am Main, Germany. Permanent Representative (Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H. Perkins. 0 TRANSPORTATION & LOGISTICS INDUSTRY UPDATE │ JUNE 2017 WHAT WE’RE READING CONTENTS LOGISTICS | FORTUNE 500 HIGHLIGHTS E-COMMERCE LOGISTICS IMPACT . M&A TRANSACTIONS This year’s Fortune 500 list of largest US publicly owned companies, released June . PUBLIC MARKETS OVERVIEW 7, underscores a growing rift in the transportation sector: Those companies . STOCK PRICE PERFORMANCE involved in e-commerce, last-mile delivery, and supply-chain solutions continue to . OUR GROUP grow faster than traditional freight-moving competitors. That is a sign of the growing impact of what is been called the “Amazon Effect” on distribution and order fulfillment, and greater specialization in last-mile and dedicated transportation. It also reaffirms those more dependent on traditional freight CONTACTS markets suffered as those markets stagnated in 2016. That shift is likely to touch more of the Fortune 500 transport operators in 2017. -

Transportation & Logistics Industry Update

TRANSPORTATION & LOGISTICS INDUSTRY UPDATE │ FEBRUARY 2016 www.harriswilliams.com Investment banking services are provided by Harris Williams LLC, a registered broker-dealer and member of FINRA and SIPC, and Harris Williams & Co. Ltd, which is authorised and regulated by the Financial Conduct Authority. Harris Williams & Co. is a trade name under which Harris Williams LLC and Harris Williams & Co. Ltd conduct business. 0 TRANSPORTATION & LOGISTICS INDUSTRY UPDATE │ FEBRUARY 2016 WHAT WE’RE READING CONTENTS LOGISTICS | ADDRESSING FUTURE DEMAND LEVELS NOW . M&A TRANSACTIONS Increased variation in what buyers require at a given time means it is no longer . PUBLIC MARKETS OVERVIEW sufficient to rely on traditional baseline ordering patterns. Meeting demand on a . STOCK PRICE PERFORMANCE more consistent basis therefore requires complex stock management systems, building and maintaining key relationships throughout the supply chain and a . OUR GROUP review of the triggers that influence buying behavior. Recent years have seen a concerted focus on suppliers adopting more products lines – both in terms of volume and variation – in order to react quickly to the demands of buyers, which can often come at a moment’s notice. CONTACTS Supply Chain Digital UNITED STATES TRUCKING | LOGISTICS CHIEF EXPECTS TRUCKERS TO ADAPT TO NEW RULES Frank Mountcastle Logistics provider C.H. Robinson Worldwide Inc. says the trucking industry should Managing Director [email protected] absorb new federal safety regulations with relative ease despite sharp divisions +1 (804) 915-0124 among trucking companies over the rules. The requirement for electronic logging devices and restrictions on driving hours for truck drivers will raise costs for some Jason Bass smaller trucking companies, John Wiehoff, the company’s chief executive, said in Managing Director an earnings conference call with analysts on Wednesday. -

Q3 2015 Transportation & Logistics

TRANSPORTATION & LOGISTICS Q3 2015 CONTACTS STATE OF THE TRANSPORATION M&A MARKET Experts continue to view the Transportation & Logistics industry as a measure of the health of the Len Batsevitsky overall economy and thus far, 2015 has been a strong year for providers of commercial Director transport. The industry has been aided by significantly lower oil prices, increased personal (617) 619-3365 [email protected] consumption, expanded manufacturing and the continued rise of e-commerce as a viable retail channel. As a result, many transportation companies are experiencing improved financial Daniel Schultz performance which, coupled with a robust middle market M&A environment, has led to a Director of Business Development significant increase in deal activity. Furthermore, the industry’s high fragmentation will serve to (617) 619-3368 increase M&A activity as companies look to consolidate, increasing their efficiency through scale. [email protected] Overall, 2015 is shaping up to be a strong M&A year for the Transportation & Logistics industry Matthew Person because thus far through Q4, there have been 104 transactions. If that pace continues Associate (617) 619-3322 throughout the rest of calendar year, we could see nearly 140 M&A transactions during 2015, [email protected] which would near the record breaking high of 144 transactions in 2012. Transportation and Logistics Transactions 160 144 140 113 120 108 108 104 100 80 80 60 40 20 0 BOSTON 2010 2011 2012 2013 2014 YTD CHICAGO 9/30/2015 Sources: Capital IQ and Capstone Partners LLC research LONDON LOS ANGELES In addition, valuations have remained stable over the past several years with recent transaction PHILADELPHIA multiples for asset-light logistics businesses generally north of 8x LTM EBITDA, while traditional SAN DIEGO asset-heavy freight carriers (primarily in the trucking sub-industry) have traded at a range of 5x to 7x. -

CLOSING the DEAL Consolidation Trends in Transportation & Logistics

9/28/2017 CLOSING THE DEAL Consolidation Trends in Transportation & Logistics September 28, 2017 Chris Dalton Greg Lafin Jeff Ronsse Partner, National Practice Leader Managing Director Transaction Services BKD Corporate Finance Managing Partner [email protected] [email protected] [email protected] Matt Klauser Gerry DeBiasi Director Partner, Kidd & Co. Transaction Services [email protected] [email protected] 1 9/28/2017 TO RECEIVE CPE CREDIT • Participate in entire webinar • Answer polls when they are provided • If you are viewing this webinar in a group . Complete group attendance form with • Title & date of live webinar • Your company name • Your printed name, signature & email address . All group attendance sheets must be submitted to [email protected] within 24 hours of live webinar . Answer polls when they are provided • If all eligibility requirements are met, each participant will be emailed their CPE certificates within 15 business days of live webinar INTRODUCTION • Thank you for joining! • Consolidation in transportation & logistics – interest & importance . Transportation industry is highly competitive & fragmented – consolidation is attractive . Correlation with consumer spending . Increase in value added or niche services – key differentiators . Technology-based services 2 9/28/2017 INTRODUCTION • Numerous perspectives for today’s discussion . Corporate Finance . Transaction Services . Audit/Tax . Private Equity TRANSPORTATION & LOGISTICS INDUSTRY UPDATE – HY 2017 OUTLOOK BKD Corporate Finance, LLC (BKDCF) has seen an increase -

Location of North American 3PL Headquarters

Location of North American 3PL Headquarters California - 18 HQs New Jersey - 14 HQs Agility Logistics - Irvine* Alliance Shippers - Englewood Cliffs Aspen Logistics - Temecula Damco USA - Madison* CaseStack - Santa Monica Flash Global Logistics - Montville D.W. Morgan Company - Pleasanton Geodis Wilson - Iselin* Number of HQs Dependable Distribution Centers - Kuehne + Nagel - Jersey City* Los Angeles National Retail Systems - North Ingram Micro Logistics - Santa Ana Bergen 1 Johanson Transportation Service NFI Industries - Cherry Hill - Fresno Panalpina - Morristown* Megatrux Companies - Rancho Port Jersey Logistics - Monroe 2-4 Cucamonga Township Menlo Worldwide Logistics - San Priority Solutions International - Mateo Swedesboro 5-9 Nexus Distribution - Oakland The Gilbert Company - Keasbey OOCL Logistics (USA) - Fountain Tucker Company Worldwide - Valley* Cherry Hill 10+ Pantos Logistics - Rancho Wallenius Wilhelmsen - Woodcliff Dominguez* Lake* Performance Team - Santa Fe Yusen Logistics - Secaucus* Springs Serec of California - Industry Source Logistics - Montebello Illinois - 13 HQs The RK Logistics Group - Fremont UTi Worldwide - Long Beach A&R Logistics - Morris Weber Logistics - Santa Fe Springs AFN - Niles AIT Worldwide - Itasca ArrowStream - Chicago Caterpillar Logistics Services - Morton DSC Logistics - Des Plaines Echo Global Logistics - Chicago Fidelitone Logistics - Wauconda Hub Group - Downers Grove LeSaint Logistics - Romeoville RR Donnelley - Chicago Sankyu USA - Wood Dale* * Denotes regional headquarters. SEKO Logistics -

Transportation & Logistics M&A Update September 2015

www.peakstone.com Transportation & Logistics M&A Update September 2015 Transportation & Logistics Industry Update | September 2015 Transportation & Logistics M&A Update . U.S. transportation & logistics M&A continues to see strong activity. Year-to-date 2015 transaction volume of 93 deals is on pace to surpass 2014 deal volume of 99 transactions. For the year-to-date 2015 period, strategic buyers accounted for 87% of the transportation & logistics M&A transactions with financial buyers making up the difference. During 2014, strategic buyers accounted for approximately 81% of the transactions. Asset-light transport and logistics companies are trading at premium valuations compared to the S&P 500. Many larger, publicly traded transportation and logistics companies have been very active in pursuing acquisitions. Notable publicly announced 2015 transactions: o XPO Logistics entered into a definitive agreement to acquire Con-way for approximately $3.5 billion. o United Parcel Service acquired Coyote Logistics for approximately $1.8 billion. o Apax Partners acquired Quality Distribution for approximately $780 million. o Echo Global Logistics acquired Command Transportation for approximately $410 million. 1 Transportation & Logistics Industry Update | September 2015 Transportation & Logistics – M&A Market Overview U.S. Transportation & Logistics Transactions by Buyer Type U.S. Transportation & Logistics Transaction Multiples 160 12 10.1x 140 10 8.6x 32 8.3x 120 NM NM 7.6x 8 7.0x 100 6.7x 25 23 18 19 12 80 6 16 16 60 106 4 40 79 81 83 80 81 64 -

Transportation & Logistics

www.mercercapital.com VALUE FOCUS Transportation & Logistics Second Quarter 2018 Second Quarter 2019 | Article: The Last Mile In This Issue The Last Mile 1 Industry Macro Trends 3 Trucking 6 Rail & Intermodal 9 M&A Activity 11 Public Company Performance 15 Mercer Capital’s Value Focus: Transportation & Logistics Second Quarter 2019 FEATURE ARTICLE Most marathon runners will tell you that the last leg of the race is the hardest. In the same vein, the final leg of freight deliv- ery is often the most complicated. This final leg – the delivery of a package from the warehouse or fulfillment center to the The Last Mile customer’s address – is known as the “last mile,” though the actual distance can vary. But why is the last mile important and how are companies attempting to “solve” the last mile problem? One reason is the increased popularity of online shopping. Another reason is its relative expense compared to other aspects of the logistics chain. According to a Honeywell estimate, last mile logistics account for 53% of total logistics cost. Finally, as more of the world’s population moves to urban areas in the coming decades, last mile difficulties will only grow. Rural last mile delivery poses its own challenges, such as low customer density. Although greater population density in cities is advantageous for concentration of deliveries, the traffic congestion and lack of parking cancel out many potential benefits. UNestimates put 55% of the world population living in an urban population right now, but projections show that this number will increase to 68% by 2050. -

Freight Assessment Blueprint Practical Guide for Evaluating Freight Transportation in Support of National Green Freight Programs

WHITE PAPER MARCH 2017 FREIGHT ASSESSMENT BLUEPRINT PRACTICAL GUIDE FOR EVALUATING FREIGHT TRANSPORTATION IN SUPPORT OF NATIONAL GREEN FREIGHT PROGRAMS Ben Sharpe www.theicct.org [email protected] BEIJING | BERLIN | BRUSSELS | SAN FRANCISCO | WASHINGTON ACKNOWLEDGMENTS This work is supported by the Climate and Clean Air Coalition and the U.S. Environmental Protection Agency. The critical reviews of Cristiano Façanha, Oscar Delgado, and Rachel Muncrief of the ICCT were very valuable. In addition, we are very grateful for the feedback provided by Buddy Polovick (U.S. EPA), Melissa Sutherland (Natural Resources Canada), and Alvin Mejia (Clean Air Asia). International Council on Clean Transportation 1225 I Street NW Suite 900 Washington, DC 20005 USA [email protected] | www.theicct.org | @TheICCT © 2017 International Council on Clean Transportation FREIGHT ASSESSMENT BLUEPRINT TABLE OF CONTENTS 1. Introduction .............................................................................................................................1 2. How to conduct a freight assessment ................................................................................4 3. What to include in a freight assessment ...........................................................................9 3.1 Roles and trends of trucking, shipping, and rail .................................................................. 9 3.2 Freight trucks and trailers sales market.................................................................................12 3.3 -

Transportation & Logistics

TRANSPORTATION & LOGISTICS INDUSTRY UPDATE | DECEMBER 2017 www.harriswilliams.de Harris Williams & Co. Ltd is a private limited company authorised and regulated by the Financial Conduct Authority, incorporated under English law with its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales under company number 07078852. Directors: Mr. Ned Valentine, Mr. Paul Poggi, Mr. Thierry Monjauze and Mr. Aadil Khan. Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the Local Court (Amtsgericht) of Frankfurt am Main, Germany, under registration number HRB 96687, having its business address at Bockenheimer Landstrasse 33-35, 60325 Frankfurt am Main, Germany. Permanent Representative (Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H. Perkins. 0 TRANSPORTATION & LOGISTICS INDUSTRY UPDATE │ DECEMBER 2017 WHAT WE’RE READING CONTENTS LOGISTICS | SUPPLY CHAINS ARE GOING TO GET SMARTER IN 2018 . M&A TRANSACTIONS By the end of 2020, one-third of all manufacturing supply chains will be using . PUBLIC MARKETS OVERVIEW analytics-driven cognitive capabilities, thus increasing cost efficiency by 10% and . STOCK PRICE PERFORMANCE service performance by 5%. "Manufacturers of every size and shape are changing . OUR GROUP rapidly because of new digital technologies, new competitors, new ecosystems, and new ways of doing business,” says Kimberly Knickle, research vice president, IT Priorities and Strategies with analyst firm IDC Manufacturing Insights. “Manufacturers that can speed their adoption of digital capabilities in order to CONTACTS create business value will be the leaders of their industry.“ Technologies that will have the greatest impact include cloud, mobile, Big Data and analytics, and the Internet of Things (IoT). -

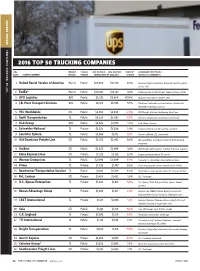

2016 Top 50 Trucking Companies 2016 Top 50 Trucking Companies

SPECIAL REPORT SPECIAL 2016 TOP 50 TRUCKING COMPANIES 2016 TOP 50 TRUCKING COMPANIES 2016 PRIMARY PUBLIC/ 2015 REVENUE 2016 REVENUE PERCENT SUBSIDIARY PORTFOLIO / RANK PARENT COMPANY SERVICE PRIVATE (IN MILLIONS OF DOLLARS) CHANGE SERVICES & COMMENTS 1 United Parcel Service of America Parcel Public $29,829 $31,770 6.5% Ground, freight, brokerage. Acquired Coyote Logistics in July 2015 TOP 50 TRUCKING COMPANIES TRUCKING 50 TOP 2 FedEx* Parcel Public $20,307 $22,127 9.0% FedEx Ground, FedEx Freight, FedEx Custom Critical 3 XPO Logistics IMC Public $3,273 $6,860 109.6% Acquired Con-way in October 2015 4 J.B. Hunt Transport Services IMC Public $6,188 $6,555 5.9% Truckload, dedicated contract service, intermodal, integrated capacity solutions 5 YRC Worldwide LTL Public $4,832 $4,698 -2.8% YRC Freight, Holland, Reddaway, New Penn 6 Swift Transportation TL Public $4,229 $4,032 -4.7% Dry-van, refrigerated, dedicated, nntermodal 7 Hub Group IMC Public $3,526 $3,573 1.3% Hub, Mode, Unyson 8 Schneider National TL Private $3,423 $3,506 2.4% Largest privately owned trucking company 9 Landstar System TL Public $3,364 $3,172 -5.7% Dry-van, flatbed, LTL, intermodal 10 Old Dominion Freight Line LTL Public $2,972 $2,992 0.6% Most profitable asset-based publicly held trucking company 11 ArcBest LTL Public $2,422 $2,496 3.0% ABF Freight, ABF Logistics, Panther Premium Logistics 12 Estes Express Lines LTL Private $2,135 $2,155 0.9% Largest privately owned LTL carrier 13 Werner Enterprises TL Public $2,094 $2,009 -4.0% One-way TL, dedicated, value-added services 14 Prime TL Private $1,736 $1,747 0.6% Prime Refrigerated, Prime Flatbed, Prime Tanker 15 Roadrunner Transportation Services TL Public $1,610 $1,709 6.2% Truckload revenue growth offset LTL revenue decline 16 R+L Carriers LTL Private $1,429 $1,452 1.6% LTL, Truckload 17 U.S.