3.1 Assessment and Collection of Property Tax in the Municipal

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Accused Persons Arrested in Kollam Rural District from 07.06.2020To13.06.2020

Accused Persons arrested in Kollam Rural district from 07.06.2020to13.06.2020 Name of Name of Name of the Place at Date & Arresting the Court Sl. Name of the Age & Cr. No & Police father of Address of Accused which Time of Officer, at which No. Accused Sex Sec of Law Station Accused Arrested Arrest Rank & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 1953/2020 U/s 269 IPC & 118(e) of GEETHA KP Act & VILASOM, 13-06-2020 ANCHAL G.PUSHPAK 20, RO JN Sec. 5 of BAILED BY 1 ABHIJITH SURESH KURUVIKKONAM, at 21:05 (Kollam UMAR ,SI OF Male ANCHAL Kerala POLICE ANCHAL Hrs Rural) POLICE Epidemic VILLAGE Diseases Ordinance 2020 1952/2020 U/s 188, 269 KOCHU VEEDU, IPC & Sec. 5 13-06-2020 ANCHAL G.PUSHPAK MADHAVA 33, NEAR ANCHAL RO JN of Kerala BAILED BY 2 ANOOP at 20:15 (Kollam UMAR ,SI OF N NAIR Male CHC, ANCHAL ANCHAL Epidemic POLICE Hrs Rural) POLICE VILLAGE Diseases Ordinance 2020 1952/2020 U/s 188, 269 IPC & Sec. 5 KAILASOM, 13-06-2020 ANCHAL G.PUSHPAK AJAYA 25, RO JN of Kerala BAILED BY 3 ANANDU ANCHAL at 20:15 (Kollam UMAR ,SI OF KUMAR Male ANCHAL Epidemic POLICE VILLAGE Hrs Rural) POLICE Diseases Ordinance 2020 1951/2020 U/s 188, 269 IPC & Sec. 5 THIRUVATHIRA 13-06-2020 ANCHAL G.PUSHPAK 25, RO JN of Kerala BAILED BY 4 AROMAL SASIDARAN VAKKAMMUK at 20:25 (Kollam UMAR ,SI OF Male ANCHAL Epidemic POLICE THAZHAMEL Hrs Rural) POLICE Diseases Ordinance 2020 1951/2020 U/s 188, 269 IPC & Sec. -

Accused Persons Arrested in Kollam Rural District from 26.07.2020To01.08.2020

Accused Persons arrested in Kollam Rural district from 26.07.2020to01.08.2020 Name of Name of the Name of the Place at Date & Arresting Court at Sl. Name of the Age & Cr. No & Sec Police father of Address of Accused which Time of Officer, which No. Accused Sex of Law Station Accused Arrested Arrest Rank & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 SNEHA BHAVAN, NEAR 26-07-2020 39/2020 U/s ACHANKO KARUPPAY 45, ACHANKOVIL ACHANKOV BAILED BY 1 SELVARAJ at 12:19 6(b) r/w 24 of VIL (Kollam Nazarudeen YA Male TEMPLE, IL POLICE Hrs COTPA Act Rural) ARYANKAVU VILLAGE 2385/2020 U/s 4(2)(a) r/w 5 of BASHEER MANZIL 31-07-2020 ANCHAL ARRESTED - ABDHUL 51, THADIKKAD Kerala 2 KABEER EZHIYAM at 20:05 (Kollam RAJU.T JFMC Ist SALAM Male U Epidemic KOLLAM Hrs Rural) PUNALUR Diseases Ordinance 2020 2384/2020 U/s 4(2)(d) r/w 5 of SIYAD MANZIL 31-07-2020 ANCHAL ARRESTED - 20, PANACHAVI Kerala 3 BINSHAD NIYAS PARUTHIYIL at 16:50 (Kollam RAJU.T JFMC Ist Male LA JN Epidemic KURIYODU Hrs Rural) PUNALUR Diseases Ordinance 2020 2383/2020 U/s 4(2)(d) r/w 5 of SAJEER MANZIL 31-07-2020 ANCHAL ARRESTED - 23, PANACHAVI Kerala 4 SAJEER SAHIL VAYALA PO at 12:55 (Kollam RAJU.T JFMC Ist Male LA JN Epidemic ANCHAL Hrs Rural) PUNALUR Diseases Ordinance 2020 2382/2020 U/s 4(2)(d) r/w 5 of RAHUL BHAVAN 31-07-2020 ANCHAL ARRESTED - RADHAKRI 24, PANACHAVI Kerala 5 RAHUL KOTTIYAM PO at 12:35 (Kollam RAJU.T JFMC Ist SHNAN Male LA JN Epidemic KOLLAM Hrs Rural) PUNALUR Diseases Ordinance 2020 2381/2020 U/s 4(2)(d) r/w 5 of MUHAMME PILLA VEEDU 31-07-2020 ANCHAL ARRESTED - 22, PANACHAVI Kerala 6 ANEESH D THOTTATHARA at 12:05 (Kollam RAJU.T JFMC Ist Male LA JN Epidemic HANEEFA ELAMADU Hrs Rural) PUNALUR Diseases Ordinance 2020 2380/2020 U/s 4(2)(d) r/w 5 of RAJESH BHAVAN 31-07-2020 ANCHAL ARRESTED - 30, MARKET JN. -

MDMS-Allotment of Contingent Charge to Schools - Quarter 1 - 2014-15 - AEO Wise

MDMS-Allotment of contingent charge to schools - Quarter 1 - 2014-15 - AEO Wise Code School School School Name Bank Account IFSCode Bank Branch Amount No. Code Type THIRUVANANTHAPURAM 423 ATTINGAL 1 42006 GOVT.BHS ATTINGAL G 67111616552 SBTR0000039 SBT ATTINGAL 111803 2 42007 GOVT.HSS ALAMCODE G 67111858456 SBTR0000667 SBT ALAMCODE 59229 3 42008 GOVT.GHS ATTINGAL G 67132614276 SBTR0000039 SBT ATTINGAL 229187 4 42011 GOVT.HS ELAMBA G 67112505555 SBTR0000039 SBT ATTINGAL 277475 5 42013 SCV BHS CHIRAYINKIL GA 67112428239 SBTR0000044 SBT CHIRAYINKEEZHU 121616 6 42014 SSV GHS CHIRAYINKIL GA 67112248610 SBTR0000044 SBT CHIRAYINKEEZHU 168092 7 42015 PNM HS KOONTHALLOR G 67112150011 SBTR0000044 SBT CHIRAYINKEEZHU 112033 8 42021 GOVT.HS AVANANAVANCHERY G 67112377485 SBTR0000039 SBT ATTINGAL 270581 9 42023 GOVT.HS KAVALAYOOR G 67112070463 SBTR0000347 SBT CHERUNNIYOOR 126703 10 42035 GOVT.HS NJEKKAD G 67110542395 SBTR0000221 SBT KALLAMBALAM 365137 11 42051 GOVT.HS VENJARAMOODU G 67111635031 SBTR0000254 SBT VENJARAMOODU 268785 12 42070 JANATHA HS THEMPAMOODU GA 67152191276 SBTR0000039 SBT ATTINGAL 255358 13 42072 GOVT.HS AZOOR G 67111735171 SBTR0000312 SBT PERUNGUZHI 185082 14 42301 LMSLPSATINGAL GA 67110367478 SBTR0000039 SBT ATTINGAL 39819 15 42302 LPS.KEEZHATINGAL G 67111917377 SBTR0000038 SBT KADAKKAVOOR 20863 16 42303 LPS ANDOOR G 67110960208 SBTR0000039 SBT ATTINGAL 30799 17 42304 LPS.ATTINGAL G 67111955856 SBTR0000039 SBT ATTINGAL 21851 18 42305 LPS. MELATTINGAL G 67110464483 SBTR0000667 SBT ALAMCODE 41489 19 42306 LPS MELKADAKKAVOOR G 67110742837 SBTR0000038 SBT KADAKKAVOOR 31548 20 42307 LPS.ELAMBA G 67111864469 SBTR0000039 SBT ATTINGAL 173914 21 42308 LPS ALAMCODE G 67112200869 SBTR0000667 SBT ALAMCODE 41356 22 42309 LPS MADATHUVATHUKKAL G 67110530809 SBTR0000052 SBT VAMANAPURAM 74110 23 42310 PTM LPS KUMPALATHUMPARA GA 67112281715 SBTR0000052 SBT VAMANAPURAM 42812 24 42311 .LPS. -

State of Kerala & Mahe District of UT of Puducherry In

Notice for appointment of Regular / Rural Retail Outlet Dealerships - State of Kerala & Mahe District of UT of Puducherry Indian Oil Corporation proposes to appoint Retail Outlet dealers in the State of Kerala & Mahe District of UT of Puducherry, as per following details: Minimum Dimension Finance to be Fixed fee/Minimum Bid Estimated monthly Type of Mode of Security deposit Sl. Name of location Revenue District Type of RO Category (in M.)/Area of the site arranged amont sales Potential # site* Selection (Rs in lakhs) No. ( in Sq.M.)* by the Applicant (Rs. In lakhs) 1 2 3 4 5 6 7 8 9a 9b 10 11 12 Regular/Rural MS + HSD in Kls SC, SC Cc1, CC/DC/CFS Frontage Depth Area Estimated Estimated fund Draw of Lots/Bidding SC CC2,SC PH, working capital required for ST, ST CC1, ST requirement for development of CC2, ST PH, operation of infrastructure OBC, OBC Cc1, RO at RO OBC CC2, OBC PH, OPEN, OPEN CC1, OPEN CC2, OPEN PH 1 Punnumoodu Alappuzha Regular 160 SC CFS 25 25 625 0 0 Draw of Lots 0 3 2 Mararikulam to Thaikkal Beach on SH 66 Alappuzha Regular 130 SC CFS 30 30 900 0 0 Draw of Lots 0 3 3 Kavalam - Kidangara Road Alappuzha Rural 100 SC CFS 20 20 400 0 0 Draw of Lots 0 2 4 Angamaly Jn - Adlux International (NH - LHS) Ernakulam Regular 150 SC CFS 35 45 1575 0 0 Draw of Lots 0 3 5 Kunnumpuram Jn, Kakkanad to Thrikkakara Ernakulam Regular 160 SC CFS 25 25 625 0 0 Draw of Lots 0 3 on Kunnumpuram NGO Quarters Road 6 Fort Kochi to Mattancherry Ernakulam Regular 160 SC CFS 25 25 625 0 0 Draw of Lots 0 3 7 Puthencruz to Kolenchery Ernakulam Regular -

Physical Geography of Edava - Nadayara and Paravur Backwaters, Kerala, India

International Journal of Science and Research (IJSR) ISSN: 2319-7064 ResearchGate Impact Factor (2018): 0.28 | SJIF (2019): 7.583 Physical Geography of Edava - Nadayara and Paravur Backwaters, Kerala, India Haritha .Y .A1, Dr. Jayalekshmi .V .K2 1Research Scholar, Department of Geography, University College, Thiruvananthapuram-695034, India 2Assistant Professor, Department of Geography, University College, Thiruvananthapuram-695034, India Abstract: Water is the important phenomenon that differentiates the Earth from other members in the Milky Way. Besides being the prominent life sustaining component in the ecosystem, water plays a versatile role in the functioning of the bio-geo-chemical cycles. A backwater means the network of interconnected lakes and they were formed by the actions of shore currents and sea waves constructing low depressions at the mouth of rivers. The backwaters of Kerala are located where the freshwater from rivers meet Lakshadweep Sea in the west. Man has been using the backwaters for ages for fishing, transportation, agriculture and other related activities. Edava- Nadayara and Paravur backwaters lies between Lakshadweep Sea and Western Ghats in the south-western part of Kerala, India and is well known for their scenic beauty. Ithikkara river is the main feeder of Paravur lake and Ayiroor River, which is the second smallest river in Kerala finally emptying into the Edava- Nadayara lake. The backwater system has a total area of 101.026 sq. kms including the lakes which covers 10.325 sq. kms. The main objective of this study is to analyse the physical settings and characteristics of Edava- Nadayara and Paravur backwaters by inventorying the geomorphology, geology, climate, soil, slope, flora and fauna with the help of primary and secondary data sources. -

1 Directorate of Higher Secondary Education

DIRECTORATE OF HIGHER SECONDARY EDUCATION NATIONAL SERVICE SCHEME Special Camping Programme From 20 to 26 th December 2009 District wise list of Schools THIRUVANANTHAPURAM Name of Name of Camp Venue with Distance/Route Sl No Name of School Programme Officer Principal Nearest Town from the School with Phone No. with Phone No. 1 St.Johns HSS, T.Sadanandan Nursery Hall,Thresiapuram Undancode-Nellimoodu- Undancode, 9495407253 B.T. Ajith Kumar Thresiapuram Trivandrum 9895624747 2 Govt.HSS VG Karmala Bai Venjaranmoodu, Najeeb.B 9495312153 Govt. LPS Venjaramood Trivandrum 9446794019 3 Govt.V&HSS For Jessy.R Govt.TTI, Girls Manacaud, Sreekumar.B 9846173273 Manacaud Trivandrum 9447553935 4 LMS HSS, Isiah Thanka Bose CSI T.T.I,Chemboor LMS HSS-CSI T. T. I-OSM Chemboor, Nisha K S 9446011777 Junction Trivandrum 9447696540 Chemboor Bus Stand 5 Govt. HSS, Suku S Jayasree H Govt.UPS 1.5 KM East From AJ Thonnakkal, 9447018293 9847270028 Kalloor,ManjamalaP.O. College Jn, Thonnakkal, Kadavoor Thonnakkal near Aasan Smarakam. Trivandrum 6 P.R.William HSS, Joy Mon F D Stanlo John Govt LPS Tottampara. Dam Route, 2KM from Kattakkada, 9995354623 9495493045 Kattakkada. School Trivandrum 1 7 Govt. Model HSS Nishi KA R Sujatha Govt. Girls HSS Manacaud. Pattom- East Fort- For Girls, 9447218076 9497268544 Manacaud Pattom, Trivandrum 8 Janardhanapuram V Sreekala LPS Ottasekharamangalam 1KM from JP HSS. HSS, V N Sreeja Kumari 9447696498 Ottasekaramangalam, 9961884475 Trivandrum 9 Govt. Model Boys Govt. Town UPS Attingal. 0.5 KM From KSRTC/ Santhosh Kumar K HSS, Attingal, T Selvaraj Private Bus station, Attingal 9447254641 Trivandrum 974538430 10 Govt. HSS, Justin Raj N L Kumai Geetha Pzhanjipara harijan Colony. -

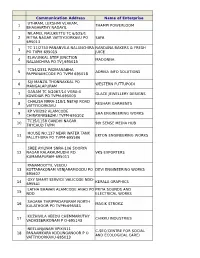

Communication Address Name of Enterprise 1 THAMPI

Communication Address Name of Enterprise UTHRAM, LEKSHMI VLAKAM, 1 THAMPI POWERLOOM BHAGAVATHY NADAYIL NILAMEL NALUKETTU TC 6/525/1 2 MITRA NAGAR VATTIYOORKAVU PO SAFA 695013 TC 11/2750 PANANVILA NALANCHIRA NANDANA BAKERS & FRESH 3 PO TVPM 695015 JUICE ELAVUNKAL STEP JUNCTION 4 MADONNA NALANCHIRA PO TV[,695015 TC54/2331 PADMANABHA 5 ADRIKA INFO SOLUTIONS PAPPANAMCODE PO TVPM 695018 SIJI MANZIL THONNAKKAL PO 6 WESTERN PUTTUPODI MANGALAPURAM GANAM TC 5/2067/14 VGRA-4 7 GLACE JEWELLERY DESIGNS KOWDIAR PO TVPM-695003 CHALISA NRRA-118/1 NETAJI ROAD 8 RESHAM GARMENTS VATTIYOORKAVU KP VIII/292 ALAMCODE 9 SHA ENGINEERING WORKS CHIRAYINKEEZHU TVPM-695102 TC15/1158 GANDHI NAGAR 10 9th SENSE MEDIA HUB THYCAUD TVPM HOUSE NO.137 NEAR WATER TANK 11 EKTON ENGINEERING WORKS PALLITHURA PO TVPM-695586 SREE AYILYAM SNRA-106 SOORYA 12 NAGAR KALAKAUMUDHI RD. VKS EXPORTERS KUMARAPURAM-695011 PANAMOOTTIL VEEDU 13 KOTTARAKONAM VENJARAMOODU PO DEVI ENGINEERING WORKS 695607 OXY SMART SERVICE VALICODE NDD- 14 KERALA GRAPHICS 695541 LATHA BHAVAN ALAMCODE ANAD PO PRIYA SOUNDS AND 15 NDD ELECTRICAL WORKS SAGARA THRIPPADAPURAM NORTH 16 MAGIK STROKZ KULATHOOR PO TVPM-695583 KUZHIVILA VEEDU CHEMMARUTHY 17 CHIKKU INDUSTRIES VADASSERIKONAM P O-695143 NEELANJANAM VPIX/511 C-SEC(CENTRE FOR SOCIAL 18 PANAAMKARA KODUNGANOOR P O AND ECOLOGICAL CARE) VATTIYOORKAVU-695013 ZENITH COTTAGE CHATHANPARA GURUPRASADAM READYMADE 19 THOTTAKKADU PO PIN695605 GARMENTS KARTHIKA VP 9/669 20 KODUNGANOORPO KULASEKHARAM GEETHAM 695013 SHAMLA MANZIL ARUKIL, 21 KUNNUMPURAM KUTTICHAL PO- N A R FLOUR MILLS 695574 RENVIL APARTMENTS TC1/1517 22 NAVARANGAM LANE MEDICAL VIJU ENTERPRISE COLLEGE PO NIKUNJAM, KRA-94,KEDARAM CORGENTZ INFOTECH PRIVATE 23 NAGAR,PATTOM PO, TRIVANDRUM LIMITED KALLUVELIL HOUSE KANDAMTHITTA 24 AMALA AYURVEDIC PHARMA PANTHA PO TVM PUTHEN PURACKAL KP IV/450-C 25 NEAR AL-UTHMAN SCHOOL AARC METAL AND WOOD MENAMKULAM TVPM KINAVU HOUSE TC 18/913 (4) 26 KALYANI DRESS WORLD ARAMADA PO TVPM THAZHE VILAYIL VEEDU OPP. -

FORM - 1 I Basic Information S

2 APPENDIX I (See paragraph – 6) FORM - 1 I Basic Information S. No. Item Details 1. Name of the Project Building Stone Mine ( Quarry, Minor Mineral Mining ) project of M/s Al Fathima Crusher India Pvt. Ltd. 2. S. No. in the schedule 1(a) 3. Proposed capacity / area / length/ Proposed Capacity 1,50,000 MTA tonnage to be handled /command Area 4.7968 hectares area/ lease area /number of wells Mineable reserves 14,83,201 MT ( 10 years) to be drilled Top Soil 62,000 Cu. m. ( 5 years) Over Burden 31,000 Cu. m. ( 5 years) Life of Mine About 10 years 4. New/ Expansion / Modernization New Quarry Project with partially old abandoned quarry site 5. Existing capacity/ Area etc. Nil 6. Category of project i.e. 'A' or 'B' Category ‘B’ 7. Does it attract the general NO condition? If yes, please specify. General Conditions are not applicable to the project. 8. Does it attract the specific NO condition? If yes, please specify. Specific Conditions are not applicable to the project. 9. Location The building stone quarry project is situated at Re-Survey Nos. 34/3-2, 34/10, 34/9, 35/1-2, 31/1-2, 31/1-3, 31/1-4, 45/2, 45/7, 45/8-2, 46/1-2, 34/8, 34/12, 44/2-3, 46/3, 45/5, 45/6, 34/3, 44/4 (Private own land) & Re-Survey Nos. 44/5, 34/2 (Govt. land) of Mancode Village, Kottarakkara Taluk, Kollam District, Kerala for mine lease area of 4.7968 hectares ( 3.3134 ha. -

Members of the Local Authorities Kollam District

Price. Rs. 150/- per copy UNIVERSITY OF KERALA Election to the Senate by the member of the Local Authorities- (Under Section 17-Elected Members (7) of the Kerala University Act 1974) Electoral Roll of the Members of the Local Authorities- Kollam District Roll Name of Members Name of local Authorities Address No. MEMBER, ADICHANALLOOR SARASAMANI SOUHRIDAM, THAZHUTHALA, 691571 1 GRAMA PANCHAYAT MEMBER, ADICHANALLOOR NANDANAM, VADAKKE MYLAKKAD, BIJI RAJENDRAN 2 GRAMA PANCHAYAT KANNANALLOOR, 691576 MEMBER, ADICHANALLOOR SANTHOSH BHAVAN, NORTH MYLAKKAD, ROYSON 3 GRAMA PANCHAYAT KANNANALLOOR 691576 MEMBER, ADICHANALLOOR SURYA BHAVAN, PLAKKAD , M.SUBHASH 4 GRAMA PANCHAYAT ADICHANALLOOR P.O,691573 MEMBER, ADICHANALLOOR PALAVILA VEEDU, ADICHANALLOOR , AMRITHA. S 5 GRAMA PANCHAYAT ADICHANALLOOR P. O,691573 MEMBER, ADICHANALLOOR NEDIYAZHIKAM, KUNDUMON , K. NAZARUDEEN 6 GRAMA PANCHAYAT ADICHANALLOOR P. O MEMBER, ADICHANALLOOR SUBU BHAVAN , VELICHIKKALA P. O, OMANA BABU 7 GRAMA PANCHAYAT VELICHIKKALA MEMBER, ADICHANALLOOR MULAMOOTTIL , VELICHIKKALA, THOMAS JECOB 8 GRAMA PANCHAYAT VELICHIKKALA MEMBER, ADICHANALLOOR JOSHVA BHAVAN , KUMMALLOOR, J.L SHEEJA 9 GRAMA PANCHAYAT KUMMALLOOR P. O,691573 MEMBER, ADICHANALLOOR S. S. BHAVAN , KUMMALLOOR, SULOCHANA.S 10 GRAMA PANCHAYAT KUMMALLOOR P. O, 691573 MEMBER, ADICHANALLOOR MADHU MANDHIRAM, KAITHAKUZHY, MADHUSOODHANAN 11 GRAMA PANCHAYAT ADICHANALLOOR P. O, 691573 MEMBER, ADICHANALLOOR MUNNAM VADAKKATHIL VEEDU, N. AJAYAKUMAR 12 GRAMA PANCHAYAT MYLAKKAD, MYLAKKAD P. O, 691571 MEMBER, ADICHANALLOOR NETTOOR KUNNATHU VEEDU, MYLAKKAD , RAMLA BASHEER 13 GRAMA PANCHAYAT MYLAKKAD P. O , 691571 MEMBER, ADICHANALLOOR PLAVILA VEEDU, KOTTIYAM , KOTTIYAM P. O REKHA. S. CHANDRAN 14 GRAMA PANCHAYAT 691571 MEMBER, ADICHANALLOOR SHAJU NIVAS, KOTTIYAM , KOTTIYAM P. O, NADEERA KOCHASSAN 15 GRAMA PANCHAYAT 691571 MEMBER, ADICHANALLOOR HEMALAYAM , VADAKKE MYLAKKAD, HEMA SATHEESH 16 GRAMA PANCHAYAT KANNANALLOOR P. -

Kollam District, Kerala

कᴂ द्रीय भूमि जल बो셍ड जल संसाधन, नदी विकास और गंगा संरक्षण विभाग, जल शक्ति मंत्रालय भारि सरकार Central Ground Water Board Department of Water Resources, River Development and Ganga Rejuvenation, Ministry of Jal Shakti Government of India AQUIFER MAPPING AND MANAGEMENT OF GROUND WATER RESOURCES KOLLAM DISTRICT, KERALA केरल क्षेत्र, ति셁िनंिपुरम Kerala Region, Thiruvananthapuram FOREWORD The National Project on Aquifer Mapping (NAQUIM) is an initiative of the Ministry of Water Resources, Government of India, for mapping and managing the entire aquifer systems in the country. The aquifer systems in Kerala are being mapped as part of this Programme and this report pertains to aquifer mapping of the hard rock terrains of Kollam district. The target scale of investigation is 1:50,000 and envisages detailed study of the aquifer systems up to 200 m depth, to ascertain their resource, water quality, sustainability, and finally evolve an aquifer management plan. The report titled “Aquifer Mapping and Management plan of hard rock areas of Kollam district, Kerala” gives a complete and detailed scientific account of the various aspects of the hard rock aquifers in the area including its vertical and horizontal dimensions, flow directions, quantum and quality of the resources, of both - the shallow and deeper zones of the hard rock aquifers. Voluminous data were generated consequent to hydrogeological, ground water regime monitoring, exploratory drilling, geophysical studies etc. in the district, and incorporated in the report. The information is further supplemented by various data collected from State departments. -

Accused Persons Arrested in Thiruvananthapuram City District from 21.08.2016 to 27.08.2016

Accused Persons arrested in Thiruvananthapuram City district from 21.08.2016 to 27.08.2016 Name of the Name of Name of the Place at Date & Court at Sl. Name of the Age & Cr. No & Sec Police Arresting father of Address of Accused which Time of which No. Accused Sex of Law Station Officer, Rank Accused Arrested Arrest accused & Designation produced 1 2 3 4 5 6 7 8 9 10 11 Keezhikkonam Puthenveedu,Near 21.08.16 Cr.no.1235/16 SI Anoop R 1 Rajan Appu 47 Male Vattiyoorkavu Vattiyoorkavu Station Bail Kachani School 10.05 HRs U/s.279 IPC Chandran Kachani Annapurna MohanaChandr Veedu,SNRA 65 21.08.16 Cr,no.1236/16 SI Anoop R 2 Athmachandh an Nair 27 27 Male Soorya Vattiyoorkavu Vattiyoorkavu Station Bail 11.35 HRS U/s.279 IPC Chandran Male Nagar,Vazhottukona m NRRA D 31 (2) Chala Satheesh 21.08.16 Cr.no1237/16 SI Anoop R 3 Sanjay Kumar 19 Male Chakkaraparavilakam, Thoppumukku Vattiyoorkavu Station Bail Kumar 13.05HRS U/s.279 IPC Chandran Karimankulam KDRA 60 Rohini Cr,.No.1238/16 Thittamangala 21.08.16 SI Anoop R 4 Hareesh Gopi 30 Male Nivas,Pulluvilakam, U/s.15 © of Vattiyoorkavu Station Bail m 15.50 HRs Chandran Thittamangalam Abkari Act Ashmi Bhavan,KRA Cr.No.1239/16 Shaikh Thittamangala 21.08.16 SI Anoop R 5 Anwar 46 Male 23, Kerala U/s.279 IPC & Vattiyoorkavu Station Bail Pareedh m 15.55 HRS Chandran Nagar,Irukunnam 185 Of MV act MMRA D 158 Cr.No.1240/16 Gangadharan Sankara Moonnammood 21.08.16 SI Anoop R 6 Deepu 32 male 279 IPC & 185 Vattiyoorkavu Station Bail nair Nilayam,Moonnamood u 17.50 HRs Chandran Of MV act u Mayanivas,KRA 320 Cr.No.1241/16 -

Accused Persons Arrested in Kollam Rural District from 30.05.2021To05.06.2021

Accused Persons arrested in Kollam Rural district from 30.05.2021to05.06.2021 Name of Name of the Name of the Place at Date & Arresting Court at Sl. Name of the Age & Cr. No & Sec Police father of Address of Accused which Time of Officer, which No. Accused Sex of Law Station Accused Arrested Arrest Rank & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 05-06-2021 609/2021 U/s POOYAPAL GOPALAKR 47, VILASI BHAVAN POOYAPPAL GOPICHAND BAILED BY 1 SYAMALAN at 19:00 4(2)(d)4(Iv)oF LY (kollam ISHNAN Male OYOOR LY RAN POLICE Hrs KEDO rural) 05-06-2021 608/2021 U/s POOYAPAL KASIMKUNJ 48, KUNNIL VEEDU MULAYARA GOPICHAND BAILED BY 2 SHEREEF at 18:00 4(2)(d)4(IV)& LY (kollam U Male MEEYANA CHAL RAN POLICE Hrs kedo rural) KODIYIL VEEDU 05-06-2021 607/2021 U/s POOYAPAL 26, MULAYARACHAL GOPICHAND BAILED BY 3 SINOFAR ANZAR OYOOR at 18:00 4(2)(d),4(iv)of LY (kollam Male CHERIYAVELINAL RAN POLICE Hrs kedo rural) OOR Usha bhavanam 05-06-2021 520/2021 U/s EZHUKON Andhakrisha 25, Rakesh BAILED BY 4 Sreekumar choorapoyika Ezhukone at 18:40 4(2)(d)r/w4(i E (kollam n Male Kumar mr POLICE kuimathikkad Hrs v) of kedo rural) 857/2021 U/s KIZAKKE 05-06-2021 279 IPC, 118 KUNDARA 31, KALLUVILA BAILED BY 5 PRAVEEN PRAKASH Elampalloor at 17:25 (E) OF KP (kollam v g vinod Male VEEDU,THRIKKOV POLICE Hrs ACT (( rural) IL VATTAM, KEDO) MOHANA 856/2021 U/s VILASAM,ELAVO 05-06-2021 KUNDARA SUNIL SAHADEVA 45, 279 ipc.118(e) VINOD VG, BAILED BY 6 ORKKAVE Elampalloor at 16:55 (kollam KUMAR N Male ofkp act,5 of SI OF POLICE POLICE KIZAKKE Hrs rural) KEDO KALLADA ANILALAYAM