Report of the Comptroller and Auditor General of India on Public Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

State Industries Promotion Corporation of Tamil

Create account Log in Article Talk Read Edit View hSisetoarych State Industries Promotion Corporation of Tamil Nadu From Wikipedia, the free encyclopedia Main page The St at e Indust ries Promot ion Contents State Industries Promotion Corporat ion of Tamil Nadu Featured content Corporation of Tamil Nadu Limit ed (SIPCOT)(Tamil: Limited Current events Random article Donate to Wikipedia Interaction ( )), Help Limited is an institution owned by the About Wikipedia government of Tamil Nadu Community portal Recent changes Contents [hide] Headquart ers Rukmani Lakshmipathy Contact Wikipedia 1 History Road,Egmore,Chennai - 600 008 . Toolbox 2 Functions 3 SIPCOT Estates Key peo ple Thiru.Dr.Niranjan Mardi, Print/export 4 See also IAS,Principal Secretary/Chairman & 5 References Languages MD for SIPCOT 6 External links Owner(s) Government of Tamil 7 Other links Edit links Nadu Websit e in History [edit] http://www.sipcot.com The State Industries Promotion Corporation of Tamil Nadu Limited (SIPCOT) was formed in the year 1971, to promote industrial growth in the State and to advance term loans to medium and large industries [1] Functions [edit] The Functions of State Industries Promotion Corporation of Tamil Nadu Limited (SIPCOT) are:[2] Development of industrial complexes/parks/growth centers with basic infrastructure facilities Establishing sector-specific Special Economic Zones (SEZs); Implementation of Special infrastructure Projects; SIPCOT Estates [edit] SIPCOT has established industrial complexes in 16 areas, according to the SIPCOT webpage. -

Students' Opinion Towards Closure of Liquor Shops in Tamilnadu

RESEARCH PAPER Physical Education Volume : 5 | Issue : 12 | Special Issue Dec 2015 | ISSN - 2249-555X Impact Factor : 3.6241 Index Copernicus Ic Value: 74.50 Empowering People: Effective Social Work Approaches & Strategies STUDENTS' OPINION TOWARDS CLOSURE OF LIQUOR SHOPS IN TAMILNADU KEYWORDS Youth alcoholism, liquor free state Sakthi vignesh.C Social Work Trainee, PG Department of Social Work, Sri Krishna Arts and Science College, Bharathiar University ABSTRACT Alcoholism is one of the major social problems of any society from the beginning of civilization through various forms of beverages. Tamilnadu, a south Indian state with great tradition and culture is highly prone to alcoholism in the midst of its people in today's picture. This social problem is chiey concentrates on student community of the state, which jeopardizes the future of the young citizens of the nation. Though many protests and social actions by the public is staged to close the retail liquor outlets completely owned by the Tamilnadu State Marketing Corporation Ltd (TASMAC), the Government of Tamilnadu still thinks about the closure of outlets because of its generation of maximum revenue to the government. This quantitative study concentrates on the opinion of students' community towards closure of liquor shop in Tamilnadu. Introduction Ÿ FOUR TN SCHOOL STUDENTS ATTEND CLASSES AFTER Alcoholism is a broad term for problems with alcohol, and is gen- DRINKING LIQUOR and DISMISSED, news article by Times erally used to mean compulsive and uncontrolled consumption of India on 23rd July 2015. Four Class 12 students studying of alcoholic beverages, usually to the detriment of the drinker’s at a gover nment higher secondary school in health, personal relationship, and social standing. -

Industry Chapter Vi

INDUSTRY CHAPTER VI Rapid industrial development coupled with modernization of agriculture is a necessary condition for launching the State economy into a self sustaining economic growth. The multiple roles of industry are: a huge employment provider, a mechanism for breaking the vicious circle of poverty, a sizable foreign exchange earner, a source of productivity and diffusion of proven technologies and efficiency gains, a trigger for bringing about the structural changes and as an engine of ratcheting economic growth. Considering the immense benefits that flow to the State from the process of industrialization, the Government has been fostering and nurturing the industrial sector with commitment and resourcefulness. 6.1 Industrial Environment: The degree of industrialization is mediated by a slew of factors such as adequate supply of skilled manpower, availability of sound social and economic infrastructure, a well established banking network with a copious supply of financial products, formulation of a proactive and dynamic industrial policy markets for the goods produced, availability of warehousing facilities, competitiveness for commodities in the domestic and overseas markets, mass production of high quality products, uninterrupted supply of raw materials and advancement in cutting edge technologies. Over a span of 10 years, the industrial GSDP in the State increased from Rs.45,066 crore in 2004-05 to Rs.90,664 crore in 2013-14 ( at 2004-05 prices) registering a Compound Annual Growth Rate (CAGR) of 8.08 per cent. Moreover, the growth rate of industrial GSDP during the period of 2005-06 and 2013-14 had been much oscillating from year to year. It ranged between the highest growth rate of 28.66 per cent in 2009-10 and the lowest of 0.60 per cent in 2007-08. -

TAMIL NADU STATE MARKETING CORPORATION LIMITED (A Government of Tamil Nadu Undertaking)

TAMIL NADU STATE MARKETING CORPORATION LIMITED (A Government of Tamil Nadu undertaking) Notice Inviting offers for registration of Imported Foreign Liquor brands for sale to TASMAC Tamil Nadu State Marketing Corporation Limited is a Company wholly owned by the State of Tamil Nadu having exclusive privilege of conducting wholesale and retail trade in IMFS and Beer in the whole State. It is also dealing in Imported Foreign Liquor (IFL) brands. The Corporation invites offers for registration of Imported Foreign Liquor (IFL) brands both ‘Duty paid’ and ‘Duty free’ for supply from the brand owners or their authorized distributors. They may submit offer form in the format given in Appendix – I. This invitation is for registration of IFL both ‘Duty paid’ and ‘Duty free’ brands for sale through TASMAC shops/sale to FL-2/FL-3 licensees. Registration of brands is a continuous process and can be done by the eligible persons at any time during the financial year. The persons who have registered their brands shall have no right vested in him to insist on TASMAC to purchase the goods offered by him. Price details are to be furnished in Appendix-II. Terms and Conditions and Additional Terms and Conditions for supply of IFL brands are given in Appendix- III and IV respetively. Special Fee rates in respect of Imported Foreign Liquor are given Appendix – V. Specimen price structure of imported foreign liquor brands (Duty paid items) for retail shops are given in Appendix – VI. Specimen price structure of imported foreign liquor brands (Duty paid and Duty free items) for FL2/F3 licencees are given in Appendix – VII and VIII respectively. -

High Court of Judicature at Madras Thursday 13 August 2020 Index

. HIGH COURT OF JUDICATURE AT MADRAS THURSDAY 13 AUGUST 2020 INDEX Sl. Video Conference Pages No. Court Sitting Arrangements / Coram 1 NOTIFICATION NO. 168 / 2020 1 - 4 2 NOTIFICATION NO. 169 / 2020 5 - 6 CHIEF JUSTICE & 3 VC 01 7 - 17 SENTHILKUMAR RAMAMOORTHY.J VINEET KOTHARI.J & 4 VC 02 18 - 20 KRISHNAN RAMASAMY.J R.SUBBIAH.J & 5 VC 03 21 - 25 C.SARAVANAN.J R.SUBBIAH.J & 6 VC 03 26 C.SARAVANAN.J N.KIRUBAKARAN.J & 7 VC 05 27 - 30 V.M.VELUMANI.J M.M.SUNDRESH.J & 8 VC 06 31 P.T.ASHA.J M.M.SUNDRESH.J & 9 VC 06 32 - 35 R.HEMALATHA.J M.M.SUNDRESH.J & 10 VC 06 36 - 38 R.HEMALATHA.J 11 VC 08 M.DURAISWAMY.J 39 - 40 12 VC 09 T.RAJA.J 41 - 43 13 VC 10 K.RAVICHANDRABAABU.J 44 - 48 14 VC 11 P.N.PRAKASH.J 49 - 51 15 VC 12 PUSHPA SATHYANARAYANA.J 52 - 55 16 VC 15 R.MAHADEVAN.J 56 - 60 17 VC 20 V.PARTHIBAN.J 61 - 68 18 VC 21 R.SUBRAMANIAN.J 69 - 74 19 VC 22 M.GOVINDARAJ.J 75 - 78 20 VC 23 M.SUNDAR.J (OS) 79 - 81 21 VC 26 M.S.RAMESH.J 82 - 88 22 VC 27 S.M.SUBRAMANIAM.J 89 - 90 23 VC 28 ANITA SUMANTH.J 91 - 96 24 VC 29 T.RAVINDRAN.J 97 - 98 25 VC 30 P.VELMURUGAN.J 99 - 103 26 VC 31 G.JAYACHANDRAN.J 104 - 106 27 VC 31 G.JAYACHANDRAN.J 107 - 109 28 VC 32 C.V.KARTHIKEYAN.J (OS) 110 - 115 29 VC 34 N.SATHISH KUMAR.J (OS) 116 - 122 30 VC 36 V.BHAVANI SUBBAROYAN.J 123 - 125 31 VC 37 A.D.JAGADISH CHANDIRA.J 126 - 137 32 VC 39 ABDUL QUDDHOSE.J 138 - 143 33 VC 40 M.DHANDAPANI.J 144 - 146 34 VC 41 P.D.AUDIKESAVALU.J 147 - 151 35 VC 47 P.T.ASHA.J (OS) 152 - 161 36 VC 47 P.T.ASHA.J (Advance List for 14.08.2020) (OS) 162 - 168 37 VC 48 M.NIRMAL KUMAR.J 169 - 174 38 VC 49 N.ANAND VENKATESH.J 175 - 181 39 VC 50 G.K.ILANTHIRAIYAN.J 182 - 184 40 VC 52 C.SARAVANAN.J 185 - 187 41 PROVISIONAL LIST 188 - 196 NOTIFICATION NO. -

Tamil Nadu State Marketing Corporation Limited (TASMAC)

International Journal of Research in Management & ISSN : 2348-6503 (Online) Vol. 2 Issue 3 July - Sept. 2015 ISSN : 2348-893X (Print) Business Studies (IJRMBS 2015) Tamil Nadu State Marketing Corporation Limited (TASMAC) – An Overview Dr.S.Sivasankaran Associate Professor in Commerce, S.T.Hindu College, Nagercoil, Tamilnadu, India Abstract The Tamil Nadu State Marketing Corporation Limited (TASMAC) is a company incorporated under the Companies Act, 1956 on 23.05.1983 with Registered Office at Chennai. TASMAC is vested with the exclusive privilege of wholesale supply of IMFL for the whole State of Tamil Nadu as per Section 17 (C) (1-A) (a) of the Tamil Nadu Prohibition Act, 1937 (Tamil Nadu Act X of 1937). It has taken over the wholesale distribution of Indian Made Foreign Liquor from the Private Sector in the whole of Tamil Nadu during May 1983. The present study analyses the TASMAC in various aspects. Keywords TASMAC, Employees, Sales, History, Directors, Origin I. Introduction of C. Rajagopalachari. Between 1937 and 2001, it was lifted briefly The Tamilnadu State Marketing Corporation Limited (TASMAC) during 1971-74, 1981–87 and 1990-91. After 1983, TASMAC is a company incorporated under the Companies Act 1956 on 23- was in charge of wholesale liquor sales in the state whenever 05-1983with Registered Office at Chennai. TASMAC is vested prohibition was lifted. In 2001, prohibition was lifted again with the exclusive privilege of wholesale supply of IMFL for the and TASMAC became the wholesale monopoly for alcohol. whole State of Tamilnadu as per Section 17 (c) (1-A) (a) of the For retail vending, the state auctioned off licenses for running TamilnaduProhinition Act, 1937 (Tamilnadu Act X of 1937). -

Prefix Gpfno Name 06/96 04/98 09/13 07/03 02/12 04/93 01/15 08/10 11/91 11/09 03/99 09/91 07/91 09/92 07/91 10/91 03/97 05/13 01

Subscribers with one or two missing credits upto February 2015 18-JAN-21 05:32 PM (Press Ctrl+F and type your gpf number to identify your record in this list) Send recovery amount of subs/refund and month of encashment for clearance of missing credit(s) PREFIX GPFNO NAME DRAWING AND DISBURSING OFFICER MISSING MONTHS AGRI 23136 SENTHIL M SUPDT ENGR AE)LAND DEVELOPMENT O/O THE CHIEF ENGR(AE) CH 35 06/96 , 27131 JOHN DURAIRAJ S ADMN OFFICER O\O THE JOINT DIR OF AGRICULTURE TIRUVALLUR 04/98 , 09/13 , 27365 BALAN S DY DIR OF AGRI WATER MGT TRAINING CENTRE VINAYAGAPURAM MDU 07/03 , 28080 PARTHIBAN K ASST DIR OF AGRI SARKARSAMAKULAM COIMBATORE DIST 02/12 , 28216 AGALYASAMUNDESWARI C JOINT DIRECTOR OF AGRI COIMBATORE 04/93 , 28244 SELVARAJU S ASST DIR OF AGRI PAVINJUR KANCHEEPURAM DIST 01/15 , 08/10 , 28620 VINAYAGAMOORTHY K ASST DIR OF AGRI RAJAPALAYAM 11/91 , 28651 MOHAN DOSS M ASST EXE ENGR (AE) TANJORE 11/09 , 28748 RAVICHANDAR A K ASST EXE ENGR (AE) KUMBAKONAM 03/99 , 09/91 , 28820 MANI R ASST DIR OF AGRI MELBHUVANAGIRI CUDDALORE DIST 07/91 , 09/92 , 28832 BALASUBRAMANIAN T ASST DIR OF AGRI VALANGAIMAN TIRUVARUR 07/91 , 10/91 , 28957 EMMANUEL RAJAA D DY DIR OF AGRI PA TO COLLECTOR (AGRI) COIMBATORE 03/97 , 05/13 , 28960 SAMPATH KUMAR V ADMN OFFICER DIR OF AGRL CHEPAUK CHENNAI - 5 01/95 , 11/91 , 29126 CHANDRANAGAR T DY DIR OF AGRI (AGRI BUSINESS) VIRUDHUNAGAR 11/91 , 29258 RAMASWAMY K ASST EXE ENGR (AE) KRISHNAGIRI 05/93 , 29317 DEVARAJ I ASST EXE ENGR AGRL ENGINEERAING DEPT UDUMALPET TIRUPPUR DIST 09/00 , 29447 KUMARASAMI D DY DIR OF AGRI -

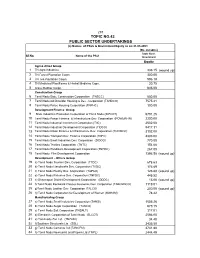

Annexure Topic No.42

297 TOPIC NO.42 PUBLIC SECTOR UNDERTAKINGS (a) Names of PSUs & Government Equity as on 31.03.2003 (Rs. in lakhs) State Govt. Sl.No. Name of the PSU Investment Equity Agri & Allied Group 1 TN Agro Industries 333.15 (wound up) 2 TN Forest Plantation Corpn. 300.00 3 TN Tea Plantation Corpn. 596.18 4 TN Medicinal PlantFarms & Herbal Medicine Copn. 20.75 5 Arasu Rubber Corpn. 845.00 Construction Group 6 Tamil Nadu State Construction Corporation (TNSCC) 500.00 7 Tamil Nadu Adi Dravidar Housing & Dev . Corporation (TAHDCO) 7575.41 8 Tamil Nadu Police Housing Corporation (TNPHC) 100.00 Development Finance Group 9 State Industries Promotion Corporation of Tamil Nadu (SIPCOT) 5791.25 10 Tamil Nadu Power Finance & Infrastructure Dev. Corporation (POWERFIN) 2200.00 11 Tamil Nadu Industrial Investment Corporation (TIIC) 2502.00 12 Tamil Nadu Industrial Development Corporation (TIDCO) 9417.31 13 Tamil Nadu Urban Finance & Infrastructure Dev. Corporation (TUFIDCO) 3102.00 14 Tamil Nadu Transport Dev. Finance Corporation (TDFC) 4303.00 15 Tamil Nadu Small Industries Dev. Corporation (SIDCO) 770.00 16 Tamil Nadu Textiles Corporation (TNTC) 154.00 17 Tamil Nadu Handloom Development Corporation (TNHDC) 267.00 18 Tamil Nadu Film Development Corporation 1396.50 (wound up) Development - Others Group 19 a) Tamil Nadu Tourism Dev. Corporation (TTDC) 678.63 20 b) Tamil Nadu Handicrafts Dev. Corporation (THDC) 176.69 21 c) Tamil Nadu Poultry Dev. Corporation (TAPCO) 126.68 (wound up) 22 d) Tamil Nadu Fisheries Dev. Corporation (TNFDC) 445.52 23 e) Dharmapuri District Development Corporation (DDDC) 15.00 (wound up) 24 f) Tamil Nadu Backward Classes Economic Dev. -

Home, Prohibition and Excise Department Policy Note Demand No. 37 Prohibition and Excise 2018

HOME, PROHIBITION AND EXCISE DEPARTMENT POLICY NOTE DEMAND NO. 37 PROHIBITION AND EXCISE 2018 – 2019 P. THANGAMANI Minister for Electricity, Prohibition and Excise © Government of Tamil Nadu 2018 INDEX Sl. Subject Pages No. 1. Introduction 1-3 2. Prohibition and Excise – 3 Organisational Set up and Functions 3. Commissionerate of Prohibition and 3-25 Excise 4. Prohibition Enforcement Wing 26-32 5. Tamil Nadu State Marketing 33-40 Corporation Limited 6. Narcotic Intelligence Bureau (NIB) 41-49 CID 7. Conclusion 50 8. Annexures I – VI 51-65 HOME, PROHIBITION AND EXCISE DEPARTMENT Demand No. 37 PROHIBITION AND EXCISE Policy Note 2018-2019 1. INTRODUCTION 1.1 The Constitution of India, by virtue of Entries 8 and 51 of the State List in the Seventh Schedule empowers the Legislature of any State to make laws with respect to the production, manufacture, possession, transport, purchase and sale of intoxicating liquors and for levying duties of excise on alcoholic liquors for human consumption manufactured in the State. Sale of toddy, arrack and country liquor was banned in this State. Sale of Indian Made Foreign Spirits, Beer and Imported Foreign Liquor is only permitted in Tamil Nadu. 1.2 This Government, as a first step towards achieving total prohibition, has ordered to reduce the working hours of TASMAC retail vending liquor shops and the bars attached thereto and also to reduce the number of liquor shops. Accordingly, from 24.05.2016 onwards, the TASMAC retail vending liquor shops and the bars attached thereto are functioning from 12 noon to 10 pm as against the earlier working hours of 10 am to 10 pm. -

Postedlist.Pdf

TAMIL NADU EXSERVICEMEN CORPORATION LIMITED POSTED LIST AS ON 19-09-2018 REG TEXCO SERVICE NO RANK NAME MOBILE NO REGION DISTRICT PROJ PROJ NAME CAT NO NO NO 13 142830 14388133L HAV A MUTHUSAMY 9942389649 MADURAI MADURAI 0545NP JOINT TRANSPORT COMMISSIONER, MADURAI SG 19 142831 1492553X NK RAJESH KUMAR N 8300868655 TIRUNELVELI TIRUNELVELI 1165 NPCIL, KUDANKULAM SG 20 142833 JC279036F NB SUB G VELUCHAMY 9487649138 RAMNAD VIRUDHUNAGAR 1822G TNCSC, VIRUDHUNAGAR SG 25 142834 JC769557K NB SUB G RAMAR 8699251209 RAMNAD SIVAGANGAI 1937H TNSTC, MOFFUSIL BRANCH, RAMNAD SG 27 142835 2484586K HAV P MUNIANDI 9159627216 TIRUNELVELI TUTICORIN 14016 AGRICULTULRAL COLLEGE, KILLIKULAM SG 30 142867 1379266A NK A RAJENDIRAN 8940511547 SOUTH CHENNAI 25049 TNEB, MAMBAKKAM SG 34 142836 14424821X HAV P MUTHUMANI 9629685634 MADURAI MADURAI 0545NP JOINT TRANSPORT COMMISSIONER, MADURAI DVR 37 137678 15762151A NK N VELMURUGAN 9445897721 CENTRAL CHENNAI 22117 IOCL, SOUTHERN REGION PIPILINES, CHENNAI SG 41 137329 7241063H DFR VIJAYAN P 9095299108 THANJAVUR THIRUVARUR 6137 CENTRAL UNIVERSITY, TIRUVARUR SG 44 142837 6484987X NK CHINNAPPA R 8754956496 TRICHY TRICHY 12099 TAMIL NADU NATIONAL LAW SCHOOL, TRICHY SG 46 141123 1380308N NK G SUNDARARAJAN 8825404085 THANJAVUR TIRUVARUR 6137 CENTRAL UNIVERSITY, TIRUVARUR SG 49 120328 13898057K NK DURAIRAJ K 9443645556 TRICHY TRICHY 7075 TREASURIES & ACCOUNTS, TRICHY DVR 51 142838 14366748W NK R MANNARSAMY 8940736748 NORTH CHENNAI 2486C TNSCB, VYASARPADI SG 53 142858 JC299284Y SUB NARAYANASAMY G 9500010542 SALEM SALEM 3406 AAVIN, -

People Oppose Beach-Link Road the Madras HC on February 21 Ordered a Study on Extending Marina Loop Road

Edition 6 Page 1_Layout 1 2/28/2020 4:29 PM Page 1 Volume No 20 Issue No 6 February 28, 2020 LAB JOURNAL OF THE ASIAN COLLEGE OF JOURNALISM Effects of farm Polluted metro Fighting online protection law water a concern child abuse Page 2 Page 3 Page 4 People oppose beach-link road The Madras HC on February 21 ordered a study on extending Marina Loop Road PHURPA LHAMO ter J. Jayalalithaa scrapped the plan S. Rajendiran of the Buildings and in 2011, it has been revived be - Bridges Department of the GCC, Fishermen, environmentalists, and cause of the court order. the road would mean less travel and people residing along the Besant The members of the Save Chen - less fuel consumption. Nagar Beach stretch are unhappy nai Beaches Campaign said that a “We know that there will be im - with the Madras High Court’s di - letter would be submitted to the pact on the environment. That can - rection to the Government urging it High Court and a press meet would not be avoided,” he said. to consider reconstructing a road be conducted at Urur Olcott Kup - With regard to the CRZ, he said from the Loop Road to Besant pam to show the impact of the that because the Broken Bridge had Nagar. construction on fishermen and en - been constructed prior to when the The order passed on February 21 vironment. CRZ was issued in 1991, the regu - by Justice Vineet Kothari and Jus - Naturalist M.Yuvan said that the lations didn't apply to the project. -

Public Sector Undertakings, Government of Tamil Nadu

Report of the Comptroller and Auditor General of India on Public Sector Undertakings for the year ended March 2016 Government of Tamil Nadu Report No.7 of 2016 Report of the Comptroller and Auditor General of India on Public Sector Undertakings for the year ended March 2016 Government of Tamil Nadu Report No.7 of 2016 TABLE OF CONTENTS Particulars Reference to Paragraph Page Preface (v) Overview (vii) – (xii) CHAPTER-I Functioning of State Public Sector Undertakings Introduction 1.1 1 Accountability frame work 1.2 - 1.4 2-3 Stake of Government of Tamil Nadu 1.5 3 Investment in State PSUs 1.6 - 1.7 3-5 Special support and returns during the year 1.8 5-7 Reconciliation with Finance Accounts 1.9 7 Arrears in finalisation of accounts 1.10 - 1.12 7-8 Impact of non-finalisation of accounts 1.13 9 Performance of PSUs as per their latest finalised 1.14 - 1.17 9-12 accounts Winding up of non-working PSUs 1.18 12 Comments on Accounts 1.19-1.20 12-13 Response of the Government to Audit 1.21 13 Follow-up action on Audit Reports 1.22 - 1.24 14-16 Coverage of this Report 1.25 16 Disinvestment, Restructuring and Privatisation of 1.26 - 1.27 16-17 PSUs and any reforms in power sector CHAPTER-II Performance Audit relating to Government Company Performance Audit on Industrial Development 2.1 21 Activities of Tamil Nadu Industrial Investment Corporation Limited Executive Summary 21-22 Introduction 2.1.1 - 2.1.2 23 Organisational setup 2.1.3 23 Scope and Audit methodology 2.1.4 23-24 i Audit Report (Public Sector Undertakings) for the year ended 31 March