Special Audit Reports - - 5 Performance Audit Reports - - 6 Other Reports (Relating to Uas) -

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Muzaffargarh

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !! ! ! ! ! ! Overview - Muzaffargarh ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! Bhattiwala Kherawala !Molewala Siwagwala ! Mari PuadhiMari Poadhi LelahLeiah ! ! Chanawala ! ! ! ! ! ! ! Ladhranwala Kherawala! ! ! ! Lerah Tindawala Ahmad Chirawala Bhukwala Jhang Tehsil ! ! ! ! ! ! ! Lalwala ! Pehar MorjhangiMarjhangi Anwarwal!a Khairewala ! ! ! ! ! ! ! ! ! Wali Dadwala MuhammadwalaJindawala Faqirewala ! ! ! ! ! ! ! ! ! MalkaniRetra !Shah Alamwala ! Bhindwalwala ! ! ! ! ! Patti Khar ! ! ! Dargaiwala Shah Alamwala ! ! ! ! ! ! Sultanwala ! ! Zubairwa(24e6)la Vasawa Khiarewala ! ! ! ! ! ! ! Jhok Bodo Mochiwala PakkaMochiwala KumharKumbar ! ! ! ! ! ! Qaziwala ! Haji MuhammadKhanwala Basti Dagi ! ! ! ! ! Lalwala Vasawa ! ! ! Mirani ! ! Munnawala! ! ! Mughlanwala ! Le! gend ! Sohnawala ! ! ! ! ! Pir Shahwala! ! ! Langanwala ! ! ! ! Chaubara ! Rajawala B!asti Saqi ! ! ! ! ! ! ! ! ! BuranawalaBuranawala !Gullanwala ! ! ! ! ! Jahaniawala ! ! ! ! ! Pathanwala Rajawala Maqaliwala Sanpalwala Massu Khanwala ! ! ! ! ! ! Bhandniwal!a Josawala ! ! Basti NasirBabhan Jaman Shah !Tarkhanwala ! !Mohanawala ! ! ! ! ! ! ! ! ! ! Basti Naseer Tarkhanwala Mohanawala !Citiy / Town ! Sohbawala ! Basti Bhedanwala ! ! ! ! ! ! Sohaganwala Bhurliwala ! ! ! ! Thattha BulaniBolani Ladhana Kunnal Thal Pharlawala ! ! ! ! ! ! ! ! ! ! ! Ganjiwala Pinglarwala Sanpal Siddiq Bajwa ! ! ! ! ! Anhiwala Balochanwala ! Pahrewali ! ! Ahmadwala ! ! ! -

Citizens' Budget Dera Ghazi Khan.Cdr

30% 50% 75% 60% 90% Citizens' Budget District Dera Ghazi Khan Year 2020-21 www.cpdi-pakistan.org Centre for Peace and Development Iniaves (CPDI) would welcome reproducon and disseminaon of the contents of this Cizens’ Budget with due acknowledgments. Disclaimer: Every effort has been made to ensure the accuracy of the contents of this publicaon. The organizaon does not accept any responsibility of any omission as it is not deliberate. Nevertheless, we will appreciate provision of accurate informaon to improve our work. ISBN: Table of Contents What is Cizens' Budget? 1 i. Budget 1 ii. Government Budget 1 iii. Ciz ens' Budget 1 iv. Cizens' Budget by CPDI 1 Budget Making Process 2 District Development Summary 4 Why Cizens Must Pay Taxes? 4 Sector-Wise Allocaons for Service Delivery 5 Allocaon in Educaon Sector 5 Major Development Projects in Educaon 6 Allocaon in Health Sector 8 Major Development Projects in Health 9 Allocaon for Water Supply and Sanitaon 11 Major Development Projects in Water Supply and Sanitaon 12 Allocaon for Roads 14 Major Development Projects in Roads 15 Allocaon for Agriculture 17 Major Development Projects in Agriculture 18 Allocaon for Social Welfare 19 Major Development Projects in Social Welfare 20 Allocaon for Women Development 21 Major Development Projects in Women Development 22 Cizens’ Budget Budget: A budget is an esmate of income and expenditure over a specific period. Government A government budget is a document presenng the esmated income from taxes and other sources and the esmated spending Budget: of government over a specific financial year. In Pakistan the financial year spans between July and June. -

Project Completion Report

Project Completion Report Project Name : Provision of Healthcare Services to Flood affected Women and Children in two Union Councils of Tehsil D.G. Khan Funded by : Concern worldwide Location : Union Councils: Haji Ghazi and Jakhar Imam Shah, Tehsil and District D G Khan Implemented by: Al-Asar Development Organization, D.G.Khan CONTENTS Page Background information 1 Project Output 1 Achievements 6 Overall Impact of the Project 11 Case Studies 12 Recommendations 13 Awareness Publications 14 Picture Gallery 17 ANNEXURES A, B & C Background Information Dera Ghazi Khan (D. G. Khan) District is situated in southwestern part of Pakistan. The district covers an area of 11922 square kilometers. According to the 1998 Census of Pakistan, the district had a population of 1,643,118 persons and estimated current population is 2,165,708. The district is divided into 3 tehsils including main tehsils of D.G Khan and Taunsa. Of 59 total union councils, 51are located in rural, while 8 union councils are located in urban part of the district. Geographically D.G Khan is divided into two regions i.e. the western half of the district is covered by Sulaimain Mountains and other is plane in the east. The cultivation and livestock breeding are main source of income for rural population. Heavy monsoon rains and floods caused devastation on a massive scale in district D.G Khan. The road contact of Dera Ghazi Khan to Multan, Muzaffargarh and the rest of Punjab was suspended as national highway was flooded at various locations and some key bridges collapsed. Flood water caused severe damage to houses, public infrastructures, crops, roads and bridges. -

Study of the Quality of Under Ground Water of District Dgkhan, Southern

Global Journal of Science Frontier Research: D Agriculture and Veterinary Volume 14 Issue 3 Version 1.0 Year 2014 Type : Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA) Online ISSN: 2249-4626 & Print ISSN: 0975-5896 Study of the Quality of under Ground Water of District D. G. Khan, Southern Punjab (Pakistan) By Muhammad Yousuf, Muhammad Bilal, Muhammad Aslam, Muhammad Arif, Shahid Munir, Muhammad Ejaz, Abdul Latif, Muhammad Rafiq, Abdul Rauf, Zafar Abbas & Muhammad Sabir Khan Directorate of Rapid Soil Fertility Survey and Soil Testing Institute, Pakistan Abstract- To analyzing the EC (μS/cm), RSC (meq/L) and SAR for assessing the quality of ground water of District Dera Ghazi Khan Southern Punjab (Pakistan). About 16555 water samples from D. G. Khan Tehsil and 5500 water samples from Tehsil Taunsa Sharif were collected. On the basis of RSC water samples show highly fitness. In Tehsil D. G. Khan it was 99% fit, correspondingly same result were drown from Taunsa Sharif. However on SAR basis ground water quality were noted that 98% from D.G. Khan and 97% from Taunsa Sharif were fit. Finally classifying the water samples on the three quality parameters EC (μS/cm), RSC (meq/L) and SAR in Tehsil D. G Khan and Taunsa Sharif following result were set up in (Table 6) that point out 60.60% water samples were consider fit, 5.65% marginally fit and 33.75% unfit, respectively. In Tehsil Taunsa Sharif, 29.07% samples were fit, 4.02% were marginally fit and 66.91% were unfit. Keywords: ground water, electrical conductivity, SAR, RSC, fit, marginally fit, unfit. -

Rapid Assessment Report of Flood-Affected Communities in D.G. Khan District, Punjab, Pakistan

Rapid Assessment Report of Flood-Affected Communities in D.G. Khan District, Punjab, Pakistan A house amid flood water in UC Sheroo, Tehsil D.G.Khan Monitoring, Evaluation and Accountability Unit August 19, 2010 Acknowledgements We would like to acknowledge support and cooperation by our field staff members in D.G Khan district particularly Dr. Shafiq-ur-Rehman, Mr. Khurram Khosa and Mr. Sajid. Sincere thanks to our Team Leader, Allison Zelkowitz, who showed keen interest in this assessment and provided every possible support to finish this study in time. We thank our colleague Mr. Omar Aijzi and Mr. Musa Hunzai who provided their valuable inputs during the course of study. We appreciate hard work of our data enumerators who showed great commitment and dedication throughout this exercise. Finally we extend our deepest thanks to flood affected communities who provided us vital information to compile this report. Report by: Sajjad Akram Monitoring, Evaluation & Accountability Manager Muhammad Hassan Monitoring, Evaluation & Accountability Coordinator Save the Children, Malakand Response Program, Pakistan © Photo by Khurram Khusa, a house amid flood water in UC Sheroo, D. G. Khan District, Punjab Province Save the Children Federation Inc. 2010 2 List of Abbreviations and Acronyms BHU Basic Health Unit CD Civil Dispensary CH Civil Hospital D. G. Khan Dera Ghazi Khan DHQ District Headquarter Hospital HHs Households Km Kilometers MNCH Maternal, Neonatal, and Child Health NFIs Non Food Items NGO Non Government Organization SPSS Statistical Package -

Matric Annual 2019

BOARD OF INTERMEDIATE AND SECONDARY EDUCATION DERA GHAZI KHAN 1 SCHOOL WISE PASS PERCENTAGE EXCEPT RESULT LATER ON CASES SECONDARY SCHOOL CERTIFICATE (ANNUAL) EXAMINATION 2019 APPEARED PASSED PASSED% 323201 LOAH-O- QALAM GIRLS SECONDARY SCHOOL KOT ADU M.GARH SCIENCE 23 20 86.96 GENERAL 1 1 100.00 TOTAL 24 21 87.50 32110007 GOVT. GIRLS HIGH SCHOOL, CHOTI ZAREEN (DERA GHAZI KHAN) SCIENCE 176 147 83.52 GENERAL TOTAL 176 147 83.52 32110008 GOVT.GIRLS HIGHER SECONDARY SCHOOL, KOT CHHUTTA (DERA GHAZI KHAN) SCIENCE 217 178 82.03 GENERAL 38 24 63.16 TOTAL 255 202 79.22 32110046 GOVT. GIRLS HIGH SCHOOL, SARWAR WALI (DERA GHAZI KHAN) SCIENCE 81 63 77.78 GENERAL TOTAL 81 63 77.78 32110047 GOVT. GIRLS HIGH SCHOOL, SHADAN LUND (DERA GHAZI KHAN) SCIENCE 96 86 89.58 GENERAL TOTAL 96 86 89.58 32110048 GOVT.GIRLS HIGH SCHOOL, JHOKE UTTRA (DERA GHAZI KHAN) SCIENCE 68 67 98.53 GENERAL TOTAL 68 67 98.53 32110049 GOVT.GIRLS HIGHER SECONDARY SCHOOL, MANA AHMADANI (DERA GHAZI KHAN) SCIENCE 179 177 98.88 GENERAL TOTAL 179 177 98.88 32110050 GOVT. GIRLS HIGH SCHOOL NO.1, DERA GHAZI KHAN SCIENCE 362 320 88.40 GENERAL 140 103 73.57 TOTAL 502 423 84.26 32110051 GOVT.GIRLS HIGH SCHOOL, MULLA QUAID SHAH, DERA GHAZI KHAN SCIENCE 335 277 82.69 GENERAL 39 32 82.05 TOTAL 374 309 82.62 BOARD OF INTERMEDIATE AND SECONDARY EDUCATION DERA GHAZI KHAN 2 SCHOOL WISE PASS PERCENTAGE EXCEPT RESULT LATER ON CASES SECONDARY SCHOOL CERTIFICATE (ANNUAL) EXAMINATION 2019 APPEARED PASSED PASSED% 32110052 CENTER OF EXCELLENCE GOVT. -

(13) Govt. Girls Degree College

BOARD OF INTERMEDIATE & SECONDARY EDUCATION, D.G.KHAN. A1 COLLEGE/INSTITUTE WISE PASS PERCENTAGE INTERMEDIATE (PART-I FRESH) ANNUAL EXAMINATION 2019 NAME OF INSTITUTE FROM RNO TO RNO APPEARED PASSED PASSED % (13) GOVT. GIRLS DEGREE COLLEGE MODEL TOWN, DERA GHAZI KHAN PRE-MEDICAL 297 184 61.95 PRE-ENGINEERING 40 27 67.50 HUMANITIES AND OTHER 132 90 68.18 GENERAL SCIENCE 26 3 11.53 TOTAL: 495 304 61.41 (17) GOVT. GIRLS HIGHER SECONDARY SCHOOL MANA AHMADANI ( DERA GHAZI KHAN ) PRE-MEDICAL 60 43 71.66 PRE-ENGINEERING 18 10 55.55 HUMANITIES AND OTHER 63 47 74.60 GENERAL SCIENCE 7 1 14.28 TOTAL: 148 101 68.24 (49) GOVT. HIGHER SECONDARY SCHOOL MANA AHMADANI ( DERA GHAZI KHAN ) PRE-MEDICAL 69 55 79.71 PRE-ENGINEERING 49 43 87.75 HUMANITIES AND OTHER 69 57 82.60 GENERAL SCIENCE 20 4 20.00 TOTAL: 207 159 76.81 (107) GOVT. GIRLS COMMUNITY HIGHER SECONDARY SCHOOL KHAN GARH ( MUZAFFARGARH ) PRE-MEDICAL 93 62 66.66 PRE-ENGINEERING 16 12 75.00 HUMANITIES AND OTHER 21 13 61.90 GENERAL SCIENCE 18 8 44.44 TOTAL: 148 95 64.18 (111) GOVT.GIRLS COMMUNITY MODEL HIGHER SECONDARY SCHOOL MEHMOOD KOT ( MUZAFFARGARH ) PRE-MEDICAL 85 53 62.35 PRE-ENGINEERING 16 12 75.00 HUMANITIES AND OTHER 37 13 35.13 GENERAL SCIENCE 11 7 63.63 TOTAL: 149 85 57.04 (321101) GOVT. COLLEGE FOR WOMEN CHOTI ZAREEN ( DERA GHAZI KHAN ) PRE-MEDICAL 67 21 31.34 PRE-ENGINEERING 11 9 81.81 BOARD OF INTERMEDIATE & SECONDARY EDUCATION, D.G.KHAN. -

Weekly Epidemiological Bulletin Disease Early Warning System and Response in Pakistan

Weekly Bulletin Epidemiological Disease early warning system and response in Pakistan Volume 3, Issue 17, Wednesday 2 May 2012 Highlights Priority diseases under surveillance Epidemiological week no. 17 (22 to 28 April 2012) in DEWS Acute (Upper) Respiratory Infection • In week 17, 2012, total 87 districts including 2 agencies provided surveillance data to the Pneumonia DEWS on weekly basis from around 1,958 health facilities. Data from mobile teams is reported Suspected Diphtheria through sponsoring BHU or RHC. Suspected Pertussis Acute Watery Diarrhoea Bloody diarrhoea • A total of 758,579 consultations were reported through DEWS of which 17% were acute Other Acute Diarrhoea respiratory infections (ARI); 9% were acute diarrhoea; 5% were suspected malaria; while 4% were Suspected Enteric/Typhoid Fever Skin disease. Suspected Malaria Suspected Meningitis Suspected Dengue fever • A total of 246 alerts reported while 25 outbreaks were identified in week 17, 2012: Alto‐ Suspected Viral Hemorrhagic Fever gether 130 alerts for Measles; 25 for Leishmaniasis; 18 each for AWD and Typhoid; 17 for Acute Pyrexia of Unknown Origin diarrhoea; 11 for NNT and tetanus; 9 for Pertussis; 8 for Bloody diarrhoea; 3 each for acute jaun‐ Suspected Measles Suspected Acute Viral Hepatitis dice syndrome and Scabies; 2 for DF; while 1 each for Malaria and ARI. Chronic Viral Hepatitis Neonatal Tetanus • In this week no new polio cases was reported. As of 30 April 2012, the total number of polio Acute Flaccid Paralysis cases confirmed by the laboratory is 15 from 10 districts/towns/tribal agencies and areas. Scabies Cutaneous Leishmaniasis Others Figure‐1: Weekly trend of Acute diarrhoea, Bloody diarrhoea, ARI and Suspected malaria in Pakistan, Week‐1, 2011 to week‐17, 2012. -

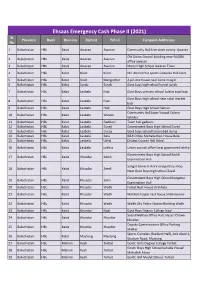

UPDATED CAMPSITES LIST for EECP PHASE-2.Xlsx

Ehsaas Emergency Cash Phase II (2021) Sr. Province Bank Division Distrcit Tehsil Campsite Addresses No. 1 Balochistan HBL Kalat Awaran Awaran Community Hall Live stock colony Awaran Old Union Council building near NADRA 2 Balochistan HBL Kalat Awaran Awaran office awaran 3 Balochistan HBL Kalat Awaran Awaran Model High School Awaran Town 4 Balochistan HBL Kalat Kalat Kalat Mir Ahmed Yar sports Complex Hall kalat 5 Balochistan HBL Kalat Kalat Mangochar A private house near Jame masjid 6 Balochistan HBL Kalat Surab Surab Govt boys high school hostel surab 7 Balochistan HBL Kalat Lasbela Hub Govt Boys primary school Adalat road hub Govt Boys high school near sabzi market 8 Balochistan HBL Kalat Lasbela Hub hub 9 Balochistan HBL Kalat Lasbela Hub Govt Boys High School Sakran Community Hall Jaam Yousuf Colony 10 Balochistan HBL Kalat Lasbela Winder Winder 11 Balochistan HBL Kalat Lasbela Gaddani Town hall gaddani 12 Balochistan HBL Kalat Lasbela Dureji Government Boys High School Dureji 13 Balochistan HBL Kalat Lasbela Dureji Govt boys school hasanabad dureji 14 Balochistan HBL Kalat Lasbela Bela B&R Office Mohalla Rest House Bela 15 Balochistan HBL Kalat Lasbela Uthal District Council Hall Uthal 16 Balochistan HBL Kalat Lasbela Lakhra Union council office local goverment lakhra Government Boys High School Karkh 17 Balochistan HBL Kalat Khuzdar Karkh Examination Hall Sangat General store and poltary shop 18 Balochistan HBL Kalat Khuzdar Zeedi Near Govt Boys high school Zeedi Government Boys High School Norgama 19 Balochistan HBL Kalat Khuzdar Zehri Examination Hall 20 Balochistan HBL Kalat Khuzdar Wadh Forest Rest House Drakhala 21 Balochistan HBL Kalat Khuzdar Wadh Mohbat Faqeer rest house Shahnoorani 22 Balochistan HBL Kalat Khuzdar Wadh Wadh City Police Station Building Wadh 23 Balochistan HBL Kalat Khuzdar Naal Govt Boys Degree College Naal Social Welfare Office Hall, Hazari Chowk 24 Balochistan HBL Kalat Khuzdar Khuzdar khuzdar. -

SED Verified Sites, Phase-VI, November,2014 Site No# District Tehsil UC Name UN No

SED Verified Sites, Phase-VI, November,2014 Site No# District Tehsil UC Name UN No. Chack/Moza Name Address 1 BWP Yazman Derawer Chack No. 118/DNB Chack No. 118/DNB, Yazman, BWP 2 BWP BWP 4/BC Basti Fazil Wali, Chack 4/BC Basti Fazil Wali, Chack No. 4/BC, P.O Dera Bakkha, BWP 3 Lodhran Lodhran Khanwan Basti Tibbi Ghalwan Basti Tibbi Ghullwan, P.O Qureshiwali, Tehsil/Distric Lodhran 4 Multan Jalalpur Lalwan Chak No.64/M Chak No.64/M 5 Okara Okara UC, Chak No 37/4A.L 41 Chak No. 39/4A.L Chak No. 39/4A.L, Gamabar,Okara 6 Okara Okara UC, Chak No 40/4A.L 42 Chak No. 41/4A.L Chak No. 41/4A.L, Gamabar,Okara Basti HABIB UR Rehman chandia 7 R.Y.Khan Khan pur Din pur sharif Basti HABIB UR Rehman chandia markaz zahir pir markaz zahir pir 8 BWN Chishtian Kalia Shah Ada Mari Shock Shah Ada Mari Shock Shah, BWN Road, Chishtian Basti Bashi, Moza Shahbaz, Boys Degree College Road, Near 9 BWN Minchinabad Minchinabad II 2 Basti Bashir Petrol Pump, Minchinabad 10 BWN Minchinabad Said Ali 114 Ada Feeder Ada Feeder, BWN Road, Minchinabad 11 BWN Minchinabad Meclod Gunj 106 Ahmad Pur Ahmad pur meclod gunj Minchinabad 12 BWN Minchinabad Mirzika 111 Tara Cheena Tara cheena mirzika minchinabad 13 BWN Minchinabad Bunga akhtar Nehal 112 Mahraj khurd Mehraj khurd mari akhtar nehaal 14 Gujrat Kharian Warichanwala 93 Soli wind Soli wind , Via Mangowal Road Dinga, Tehsil Kharian 15 Chiniot Chiniot 153 /JB 19 143 Chak 143 Chak No Jhoke Kalra Chiniot 16 Chiniot Chiniot Harsa Sheikh 11 Masoor Ke Masoor Ke Near Mal Ke Asiyan Chiniot Chak Gangi pur, Adda Rang Shah, Pakpattan Road, Arifwala, 17 Pakpattan Arifwala Chak No 13/EB 44 Chak Gangi pur Pakpattan 18 Khanewal Khanewal 74/15-L / No. -

To View NSP QAT Schedule

EMIS CODE New QAT Program Sr. No Shift Time SCHOOL NAME Address TEHSIL DISTRICT REGION QAT Day /SCHOOL CODE Date Name 12.30 pm NEW AGE PUBLIC UC Name Dhurnal, UC # 39, Moza FATEH 1 B ATK-FJG-NSP-VIII-3061 ATTOCK North 14 18.12.18 NSP to 2.30 pm SCHOOL Dhurnal, Chak / Basti Dhurnal Ada, JANG Tehsil Fateh Jung District Attock 12.30 pm Village Bai, PO Munnoo Nagar, Tehsil HASSANAB 2 B ATK-HDL-NSP-IV-210 Sun Rise High School ATTOCK North 11 14.12.18 NSP to 2.30 pm Hassan Abdal, District Attock DAL 12.30 pm Science Secondary Thatti Sado Shah, Po Akhlas, Tehsil PINDI 3 B ATK-PGB-NSP-IV-214 ATTOCK North 16 20.12.18 NSP to 2.30 pm School Pindi Gheb, District Attock GHEB 12.30 pm Al Aziz Educational Village Gangawali, Teshil Pindi Gheb, PINDI 4 B ATK-PGB-NSP-IV-216 ATTOCK North 17 09.01.19 NSP to 2.30 pm School System District Attock GHEB Basti Haider town(Pindi Gheb), Mouza 12.30 pm PINDI 5 B ATK-PGB-NSP-VII-2477 Hamza Public School Pindi Gheb, UC Name Chakki, UC # 53, ATTOCK North 17 09.01.19 NSP to 2.30 pm GHEB Tehsil Pindi Gheb, District Attock. Mohallah Jibby. Village Qiblabandi, PO 12.30 pm Tameer-e-Seerat Public 6 B ATK-HZO-NSP-IV-211 Kotkay, Via BaraZai, Tehsil Hazro, HAZRO ATTOCK North 12 15.12.18 NSP to 2.30 pm School District Attock 9.00 am to Stars Public Elementary 7 A ATK-ATK-NSP-IV-207 Dhoke Jawanda, Tehsil & District Attock ATTOCK ATTOCK North 12 15.12.18 NSP 11.00 School 12.30 pm Muslim Scholar Public Dhoke Qureshian, P/O Rangwad, tehsil 8 B ATK-JND-NSP-VI-656 JAND ATTOCK North 15 19.12.18 NSP to 2.30 pm School Jand 12.30 pm Farooqabad -

DERA-GHAZI-KHAN-Rend60.Pdf

Renewal List S/NO REN# / NAME FATHER'S PRESENT ADDRESS DATE OF ACADEMIC REN DATE NAME BIRTH QUALIFICATION 1 39939 ZAFAR PEER BUKHSH CHAK TOPI WALA MOUZA KHAKHI P/O SAMEDISTT. 7-10-1984 MATRIC 13/7/2014 HUSSAIN D.G. KHAN , DERA GHAZI KHAN, PUNJAB 2 37693 ABDUL RASHID ELAHI BAKHSH IDREES TOWN GADAI SHUMALI P/O SAMIN TEH & 1-10-1970 MATRIC 14/7/2014 DISTT. D.G. KHAN , DERA GHAZI KHAN, PUNJAB 3 21707 ABID HUSSAIN KHADIM CHOTI ZARIN BASTI MARI WALAP.O. HASSAN ABAD, 10/5/1978 MATRIC 14/07/2014 HUSSAIN DERA GHAZI KHAN, PUNJAB 4 32701 SAAD ULLAH MUHAMMAD H/NO. 92 BLOCK NO. 15 EID GAH ROAD D, G, KHAN , 26-12- MATRIC 15/07/2014 SAFDAR SAFDAR DERA GHAZI KHAN, PUNJAB 1975 5 47704 GHULAM ALLAH WASAYA VILL, BAQIR WALA P/O NUTKANI TEH, TAUNSA 7-7-1978 MATRIC 19/07/2014 MUSTAFA SHARIF DISTT,, DERA GHAZI KHAN, PUNJAB 6 31539 MUNIR AHMED MOLVI BASHIR MORAH P/O NANKANI TEH, TOUNSAH DISTT, D G 28-5-1973 MATRIC 04/09/2014 AHMED KHAN, DERA GHAZI KHAN, PUNJAB 7 22237 SALEEM MIRZA H.N.82BLOCK G, DERA GHAZI KHAN, PUNJAB 1/4/1974 MATRIC 20/09/2014 AKHTAR MUHAMMAD RAFIQ 8 37680 MUHAMMAD MUHAMMAD HOUSE NO. 92, BLOCK -9, , DERA GHAZI KHAN, 31-8-1968 MATRIC 23/9/2014 SALEEM SHARIF PUNJAB SHARIF 9 40134 MUHAMMAD MUHAMMAD H NO. 102 BLOCK F D G KHAN, DERA GHAZI KHAN, 24-2-1984 MATRIC 27/9/2014 ALI ANSARI RIAZ ANSARI PUNJAB 10 40135 MUHAMMAD MUHAMMAD BLOCK NO.