Accounting for a Merchandising Business Organized as a Partnership – Chapter 12 – Journalizing Sales & Cash Receipts

Seth and Steve are working on advertising, so they can get more customers into their shop. A CUSTOMER – is a person or businesses to whom merchandise or services are sold. The customers Seth and Steve are trying to target are teenagers who are interested in gaming. They have been passing out flyers at other game shops, the mall, other stores where teenagers shop, and the schools near their shop.

When customers come to the shop to buy games, play games or get beverages or snacks, they not only pay for the merchandise but are also required to pay SALES TAX. Sales tax is - Tax, a percentage of money that must be paid according to the price of merchandise or service, in addition to the original price of the merchandise or service. All stores, restaurants, gas stations, movie theaters, etc. charge tax. Every state has their own tax rate. Utah’s tax rate is currently 6.6%.

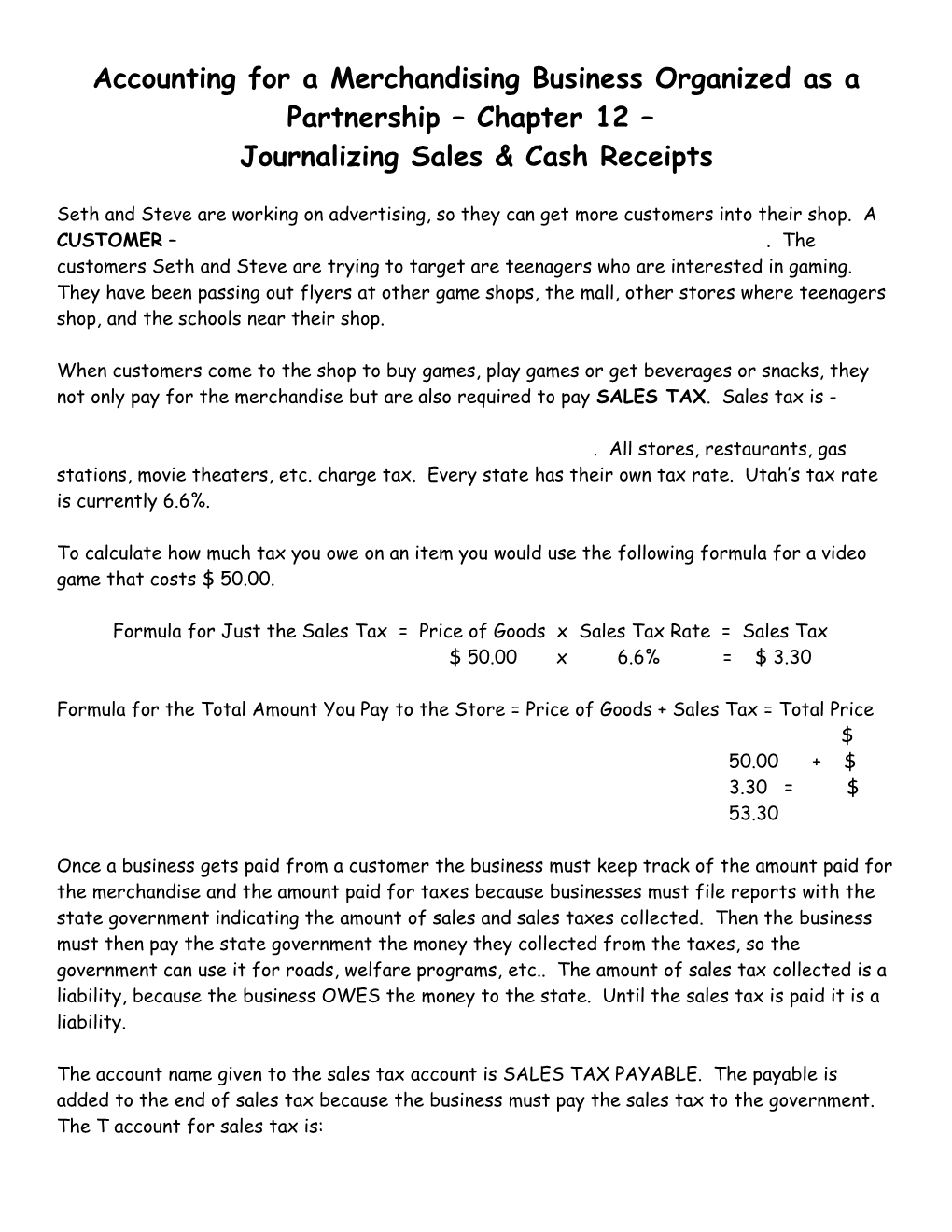

To calculate how much tax you owe on an item you would use the following formula for a video game that costs $ 50.00.

Formula for Just the Sales Tax = Price of Goods x Sales Tax Rate = Sales Tax $ 50.00 x 6.6% = $ 3.30

Formula for the Total Amount You Pay to the Store = Price of Goods + Sales Tax = Total Price $ 50.00 + $ 3.30 = $ 53.30

Once a business gets paid from a customer the business must keep track of the amount paid for the merchandise and the amount paid for taxes because businesses must file reports with the state government indicating the amount of sales and sales taxes collected. Then the business must then pay the state government the money they collected from the taxes, so the government can use it for roads, welfare programs, etc.. The amount of sales tax collected is a liability, because the business OWES the money to the state. Until the sales tax is paid it is a liability.

The account name given to the sales tax account is SALES TAX PAYABLE. The payable is added to the end of sales tax because the business must pay the sales tax to the government. The T account for sales tax is: Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - +

Liabilities – Sales Tax Payable

Left Side Right Side

Debit Side Credit Side Normal Balance - + In order to journalize selling merchandise with tax, you need to know whether the customer paid with cash, credit card or bought the merchandise on account. A CASH SALES - is when a customer pays with cash or a check for the total amount of the merchandise (merchandise + tax) on the day they buy it. A CREDIT CARD SALES - is when a customer pays with a credit card for the total amount of the merchandise (merchandise + tax) on the day they buy it.

When paying with a credit card, the store gets the money from the credit card that day, so a credit card purchase is journalized the same way as a cash purchase. The reason a credit card works the same way as cash is because the bank who issued the credit card pays the store for the total amount of the merchandise (merchandise + tax), and the customer promises to pay the bank back at a certain time for the amount of the merchandise. If the customer chooses not to pay the bank back when they said they would (the grace period), the customer is charged an interest rate in addition to the amount of the merchandise until the entire amount of the merchandise is paid.

The store must however keep track of all of the credit card payments. To do this the company does the following: at the end of each week, the business prepares a credit card slip for each credit card sale the businesses bank accepts the credit card slips the same way it accepts checks and cash for deposit the bank increases the businesses bank account by the total amount of the credit card sales deposited the bank that issues the credit card then bills the customer and collects the amount owed the bank that accepts and processes the credit card slips for a business charges a fee to the business for the time and paper work for billing the credit card company. (This fee is included on the businesses monthly bank statement)

The amount of money the business gets from either a cash or credit card sale is considered revenue to the business, because it increases the amount of money the business makes. The account used to journalize a sale is Sales. To journalize a cash sales or a credit card sale the source document or Doc. No. with either be a C if the customer paid with a check or a T (register tape) if the customer paid with cash or credit card.

To record and journalize a cash and credit card sales from a customer for a game that costs $50.00 it would look like this: November 7, 20–. Recorded cash and credit card sales $ 50.00, plus sales tax, $ 3.30; total, $ 53.30. Cash Register Tape No. 7.

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 53.30 $ 3.30 $ 50.00

Journal Page 1 Post. Date Account Title Doc. Sales Sales Tax Cash Ref. No. Payable

Credit Debit Credit Credit

1 Nov 7 T7 50.00 3.30 53.30 Because all of the accounts have special amount columns a is placed in the Account Title to tell people reading the journal that both accounts have special amount columns and put a in the Post Ref. to tell people reading the journal that the amounts are not to be posted individually to their own accounts, the amounts will be added in with all of the amounts in its special amount column to get a total amount, which the total will then be posted to the account. Date, written in date column 20-, Nov. 7 Account Title

Check Mark (all account titles have their own column) Doc No., Cash Register Tape 7 T7 Post. Ref.

Check Mark (don’t post individually) Sales Credit, Credit amount (special amount column) $ 50.00 Sales Tax Payable, Credit amount (special amount column) $ 3.30 Cash, Debit amount (special amount column) $ 53.30

There are times when Seth and Steve have customers who want to buy beverages or snacks, and they don’t have enough money, so they allow the customers to buy the beverages and snacks on account, this is called a sale on account. A SALE ON ACCOUNT - is when cash for the total amount of sales is collected at a later date, it is also called a charge sale.

The total amount of money that needs to be collected is put in an Asset account called ACCOUNTS RECEIVABLE. The accounts receivable affects cash, because the business is not collecting money at that time – it is a debit to Accounts Receivable because it decreases cash (they’re giving merchandise for nothing in return). When the customer pays the business – it is a credit to Accounts Receivable because it increases cash. The T account for accounts receivable is:

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Accounts Receivable Left Side Right Side Debit Side Credit Side Normal Balance + -

The source document or Doc. No. for a sale on account will be a S for SALES INVOICE. A sales invoice is - an invoice form showing what has been sold on account, the quantity of items and the price of each item. The sales invoices are numbered in sequence 1, 2, 3, 4, and also referred to as a sales ticket or a sales slip.

When a sales invoice is prepared, it is prepared in duplicate, the original goes to the Customer, and the carbon copy is used as the source document.

To record and journalize a sale on account for snacks that add up to $5.33 it would look like this: November 3, 2---, Sold merchandise (snacks) on account to Brady Flemm, $5.00, plus sales tax, $ .33; total, $ 5.33. Sales Invoice No. 72. Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Accounts Receivable Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 5.33 $ .33 $ 5.00

Journal Page 1 Post Accounts Sales Sales Date Account Title Doc. Tax . Payable No. Receivable Ref. Debit Credit Credit Credit 2 Nov 3 Brady Flemm S72 5.33 5.00 .33 Date, written in date column 20-, Nov. 3 Account Title

Brady Flemm Doc No., Sales Invoice No. 72 S72 Accounts Receivable, Debit amount (special amount column) $ 5.33 Sales Credit, Credit amount (special amount column) $ 5.00 Sales Tax Payable Credit, amount (special amount column) $ .33

To record and journalize another cash and credit card sales from merchandise that cost $500.00 it would look like this: November 8, 20–. Recorded cash and credit card sales $ 500.00, plus sales tax, $ 33.00; total, $ 533.00. Cash Register Tape No. 8.

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 533.00 $ 33.00 $ 500.00 Journal Page 1 Post. Date Account Title Doc. Sales Sales Tax Cash Ref. No. Payable

Credit Debit Credit Credit

3 Nov 8 T8 500.00 33.00 533.00 Because all of the accounts have special amount columns a is placed in the Account Title to tell people reading the journal that both accounts have special amount columns and put a in the Post Ref. to tell people reading the journal that the amounts are not to be posted individually to their own accounts, the amounts will be added in with all of the amounts in its special amount column to get a total amount, which the total will then be posted to the account. Date, written in date column 20-, Nov. 8 Account Title

Check Mark (all account titles have their own column) Doc No., Cash Register Tape 8 T8 Post. Ref.

Check Mark (don’t post individually) Sales Credit, Credit amount (special amount column) $ 500.00 Sales Tax Payable, Credit amount (special amount column) $ 33.00 Cash, Debit amount (special amount column) $ 533.00

To record and journalize another cash and credit card sales from merchandise that cost $1500.00 it would look like this: November 20, 20–. Recorded cash and credit card sales $ 1500.00, plus sales tax, $ 99.00; total, $ 1599.00. Cash Register Tape No. 9.

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 1599.00 $ 99.00 $ 1500.00

Journal Page 1 Post. Date Account Title Doc. Sales Sales Cash Ref. No. Tax Payable

Credit Debit Credit Credit

4 Nov 20 T9 1500.00 99.00 1599.00 Because all of the accounts have special amount columns a is placed in the Account Title to tell people reading the journal that both accounts have special amount columns and put a in the Post Ref. to tell people reading the journal that the amounts are not to be posted individually to their own accounts, the amounts will be added in with all of the amounts in its special amount column to get a total amount, which the total will then be posted to the account. Date, written in date column 20-, Nov. 20 Account Title

Check Mark (all account titles have their own column) Doc No., Cash Register Tape 9 T9 Post. Ref.

Check Mark (don’t post individually) Sales Credit, Credit amount (special amount column) $ 1500.00 Sales Tax Payable, Credit amount (special amount column) $ 99.00 Cash, Debit amount (special amount column) $ 1599.00

To record and journalize another cash and credit card sales from merchandise that cost $ 600.00 it would look like this: November 27, 20–. Recorded cash and credit card sales $ 600.00, plus sales tax, $ 39.60; total, $ 639.60. Cash Register Tape No. 10.

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 639.60 $ 39.60 $ 600.00

Journal Page 1 Post. Date Account Title Doc. Sales Sales Tax Cash Ref. No. Payable

Credit Debit Credit Credit

5 Nov 27 T10 600.00 39.60 639.60 Because all of the accounts have special amount columns a is placed in the Account Title to tell people reading the journal that both accounts have special amount columns and put a in the Post Ref. to tell people reading the journal that the amounts are not to be posted individually to their own accounts, the amounts will be added in with all of the amounts in its special amount column to get a total amount, which the total will then be posted to the account. Date, written in date column 20-, Nov. 27 Account Title

Check Mark (all account titles have their own column) Doc No., Cash Register Tape 10 T10 Post. Ref. Check Mark (don’t post individually) Sales Credit, Credit amount (special amount column) $ 600.00 Sales Tax Payable, Credit amount (special amount column) $ 39.60 Cash, Debit amount (special amount column) $ 639.60

When it comes time for the customer to pay Seth and Steve back for the $5.33 they borrowed for the beverages and snacks, the business will prepare a receipt to show that the customer paid. The receipts are pre-numbered so that the business can keep track of the receipts and who paid. The original receipt toes to the customer, and the carbon coy is used as a source document for the cash received (Accounts Receivable). The account Accounts Receivable will be decreased, because the customer is paying off (decreasing the amount) what they owe.

To record and journalize a cash payment from a customer for a previous sale on account for snacks that added up to $5.33 it would look like this:

December 3, 2---, Received cash on Account from Brady Flemm for (snacks), $ 5.33, covering S 72. Receipt No. 86

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Assets - Accounts Receivable Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance + - + - $ 5.33 $ 5.33 Journal Page 1 Date Account Title Doc Post Accounts Cash . . Receivable No. Ref. Debit Credit Debit Credit 6 De 3 Brady Flemm R86 5.33 5.33 c Date, written in date column 20-, Dec. 3 Account Title

Brady Flemm Doc No., Sales Invoice No. 86 R86 Accounts Receivable, Credit amount (special amount column) $ 5.33 Cash, Debit amount (special amount column) $ 5.33

To record and journalize another cash and credit card sales from merchandise that cost $ 2000.00 it would look like this: December 5, 20–. Recorded cash and credit card sales $ 2000.00, plus sales tax, $ 132.00; total, $ 2132.00. Cash Register Tape No. 11.

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 21322.00 $ 132.00 $ 2000.00

Journal Page 1 Post. Date Account Title Doc. Sales Sales Cash Ref. No. Tax Payable

Credit Debit Credit Credit 7 Dec 5 T11 2000.00 132.00 2132.00 Because all of the accounts have special amount columns a is placed in the Account Title to tell people reading the journal that both accounts have special amount columns and put a in the Post Ref. to tell people reading the journal that the amounts are not to be posted individually to their own accounts, the amounts will be added in with all of the amounts in its special amount column to get a total amount, which the total will then be posted to the account. Date, written in date column 20-, Dec. 5 Account Title

Check Mark (all account titles have their own column) Doc No., Cash Register Tape 11 T11 Post. Ref.

Check Mark (don’t post individually) Sales Credit, Credit amount (special amount column) $ 2000.00 Sales Tax Payable, Credit amount (special amount column) $ 132.00 Cash, Debit amount (special amount column) $ 2132.00

To record and journalize another cash and credit card sales from merchandise that cost $ 800.00 it would look like this: December 12, 20–. Recorded cash and credit card sales $ 800.00, plus sales tax, $ 52.80; total, $ 852.80. Cash Register Tape No. 12. Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 852.80 $ 52.80 $ 800.00

Journal Page 1 Post. Date Account Title Doc. Sales Sales Tax Cash Ref. No. Payable

Credit Debit Credit Credit

8 Dec 12 T12 800.00 52.80 852.80 Because all of the accounts have special amount columns a is placed in the Account Title to tell people reading the journal that both accounts have special amount columns and put a in the Post Ref. to tell people reading the journal that the amounts are not to be posted individually to their own accounts, the amounts will be added in with all of the amounts in its special amount column to get a total amount, which the total will then be posted to the account. Date, written in date column 20-, Dec. 12 Account Title

Check Mark (all account titles have their own column) Doc No., Cash Register Tape 12 T12 Post. Ref.

Check Mark (don’t post individually) Sales Credit, Credit amount (special amount column) $ 800.00 Sales Tax Payable, Credit amount (special amount column) $ 52.80 Cash, Debit amount (special amount column) $ 852.80

To record and journalize another cash and credit card sales from merchandise that costs $ 1300.00 it would look like this: December 20, 20–. Recorded cash and credit card sales $ 1300.00, plus sales tax, $ 85.80; total, $ 1385.80. Cash Register Tape No. 13. Assets = Liabilities + Owner’s Equity

Assets Liabilities Owner’ Equity Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance Normal Balance + - - + - + Assets – Cash Sales Tax Payable Sales Left Side Right Side Left Side Right Side Left Side Right Side Debit Side Credit Side Debit Side Credit Side Debit Side Credit Side Normal Balance Normal Balance

+ - - + - + $ 1385.80 $ 85.80 $ 1300.00

Journal Page 1 Post. Date Account Title Doc. Sales Sales Tax Cash Ref. No. Payable

Credit Debit Credit Credit

9 Dec 20 T13 1300.00 85.80 1385.80 Because all of the accounts have special amount columns a is placed in the Account Title to tell people reading the journal that both accounts have special amount columns and put a in the Post Ref. to tell people reading the journal that the amounts are not to be posted individually to their own accounts, the amounts will be added in with all of the amounts in its special amount column to get a total amount, which the total will then be posted to the account. Date, written in date column 20-, Dec. 20 Account Title

Check Mark (all account titles have their own column) Doc No., Cash Register Tape 13 T13 Post. Ref.

Check Mark (don’t post individually) Sales Credit, Credit amount (special amount column) $ 1300.00 Sales Tax Payable, Credit amount (special amount column) $ 85.80 Cash, Debit amount (special amount column) $ 1385.80

Seth and Steve’s computer gaming business has a lot of merchandise and customers to keep track of. They feel that using the expanded 11 column is very helpful for keeping track of their money. They see a good future for their business and know that the information they are learning in their accounting class is really helping them be professionals. However, besides journalizing the transactions they will also need to prove and rule the journal pages when all of the lines on the journal page are full or it is the end of the month.

If all of the lines of the journal are filled up, the total amounts from the journal page must be written on the next page of the journal. When the amounts have been written on the next page, the page will continue to be used until the end of the month.

To rule and journal page to carry the total amounts to the next page, the columns of the first page are proved and ruled so that the column totals can be carried forward from the page filled up and brought (moved) forward to the next page. The following five steps show you how to prove a journal. 1- Individually add each of the amount columns up to get a total. 2- Add all of the debit column totals together to get a total amount for all debit columns. 3- Add all of the credit column totals together to get a total amount for all credit columns. 4- Check to make sure the total debit amount equals the total credit amount

Once you’ve proved that the debit totals equal the credit totals you can rule (finish with) the fill up journal page and start a new journal page to keep journalizing transactions 1- Rule (draw) a single line across all amount columns directly below the last entry. 2- On the next line, write the date you are closing the page in the date column. 3- On the same line, write Carried Forward in the Account Title Column. (A is used in the Post. Ref. column to show that nothing on this line needs to be posted at this time. At the end of the month you will post amounts). 4- On the same line, add up the column amounts and write the total amount directly below the single line. 5- If you’ve proved the page and all debit columns amounts equal all credit column amounts, rule (draw) double (two) lines below the column totals across all amount columns to tell people reading the journal that all of the amount totals have been verified as correct.

To starting a new journal page you, follow the next four steps 1- On the top of the page, where it as the page number, write the new page number, 2. 2- On the first journal entry line, write the same date as the carried forward date on the previous page in the date column. 3- On the same line, write Brought Forward in the Account Title. (A is placed in the Post. Ref. column to tell people reading the journal that nothing on this line needs to be posted, until the page is filled up or it is the end of the month). 4- On the same line, write in the column total amounts from the previous page.

You will ALWAYS complete a journal at the end of the month, even if all of the lines are not full by the end by proving all of the debit and credit amount columns, ruling the journal pages and proving the cash.

You will need to prove all of the amount columns of each journal page (page one, page two, etc.). You will prove Page 2 of a Journal just as you did Page 1. 1- Individually add each of the amount columns up to get a total. 2- Add all of the debit column totals together to get a total amount for all debit columns. 3- Add all of the credit column totals together to get a total amount for all credit columns. 4- Check to make sure the total debit amount equals the total credit amount

You will need to rule all of the journal pages at the end of the month, just as you did page 1. 1- Rule (draw) a single line across all amount columns directly below the last entry. 2- On the next line, write the date you are closing the page in the date column. 3- On the same line, write Totals in the Account Title Column. 4- On the same line, add up the column amounts and write the total amount directly below the single line. 5- If you’ve proved the page and all debit columns amounts equal all credit column amounts, rule (draw) double (two) lines below the column totals across all amount columns to tell people reading the journal that all of the amount totals have been verified as correct.

You will also need to prove the cash you started out with at the beginning of the month with the cash you have at the end of the month. PROVING CASH is - determining that the amount of cash agrees with the accounting records. Use the following to help you prove cash: 1- Calculate the cash balance Write down the amount of cash you had on hand at the begin of the month (Some months you will start with $ 0 cash) Add + the total cash received during the month (Cash Debit Total Amount) Equals = the money you gained Minus – the total cash you paid during the month (Cash Credit Total Amount) Equals = the cash balance you have at the end of the month

2- Check to make sure that the cash balance is the same as the balance in the check book on the next unused check stub. If the amounts are the same, cash has been proved!

Wow after completing and ruling the journal, proving the amount columns of the journal and proving cash, Julie feels she is truly becoming an accountant. The next step Julie and her classmates need to learn is how to take the journal entries and post (put) the account amounts into their own separate accounts.