Study of Consumer Perception of Credit Cards: An empirical investigation Prof Timira Shukla*

*Prof Timira Shukla* has over 22 years of experience to her credit in academics as well as industry. One of the founder faculty members of the Institute of Management Studies, Ghaziabad she has conducted several Management Development Programmes for the industry. A faculty in the field of Services Marketing, Marketing Research and Strategic Management she has over 22 publications to her credit in national and international refereed journals and conference proceedings.

1 Abstract

The credit card market in India, which started out in 1981, is on the verge of an unprecedented boom. Between 1987 and 2000, the market has virtually grown to over 3.8 million cards with almost 25-30 per cent growth in new card-holders. Currently, four major bishops are ruling the card empire - Citibank, Standard Chartered Bank, HSBC and State

Bank of India (SBI). While card-base and appends are growing at 25-30 per cent annually it is only 20 per cent of the card base, that is actually generating revenue, Nearly 45-50 per cent of the card-holders are estimated to be inactive. This is an area of major concern for the banks as it speaks volumes about the level of satisfaction derived from the bank/ credit card.

No bank or financial service provider can reap the benefits if they focus only on broadening the customer database. There seems to be a gap between what customers expect and what card issuers deliver. In other words the credit card issuers are not correctly focused on the service quality dimensions that matter to the customer. Citibank, SBI, HSBC, Bank of

Baroda are the dominant players in the credit card industry in India. The basic purpose of the study is to evaluate different banks on the basis of SERVQUAL model (service quality model also popularly referred to as GAP model) and study perceptual mapping of different banks with respect to credit cards.

Keywords: Consumer perception, SERVQUAL model, Credit cards

2 Introduction:

The word credit comes from Latin, meaning "trust”. In the early 1900s oil companies and

department stories issued their own proprietary cards. These cards had limited use; were

mainly developed as a means of creating customer loyalty and improving customer service

according to Sienkiewicz .The Diners Club Card was the next step in credit cards. Diners

Club and American Express launched the first ‘plastic money’ in USA in 1950. In 1951,

Diners Club issued the first credit card to 200 customers who could use it at 27 restaurants in

New York. These were mainly used for travel and entertainment purposes. But it was only

after the introduction of standards for magnetic stripe in 1970 that credit cards gained mass

acceptance. The concept of use now and pay later gained acceptance in India post

liberalistaion. There are various types of credit cards available in India. The table 1 given

below gives the performance measures of credit cards in India

TABLE 1

Performance measures (Credit Cards) Industry Citibank SBI HDFC ICICI Application & approval 60 60 64 62 58 process Verification process 57 56 60 59 54 Repayment process 57 58 55 64 53 Advertising & promotion 58 59 59 58 55 Comm. received on promotion 55 57 55 56 55 Call centre of bank FI 67 50 70 75 62 *Customer who rated performance as 'excellent' or 'very good'. Source CSMM-BW loyalty report.

Source:CSMM-BW loyalty report published in The Marketing Whitebook 2007-2008

3 Many definitions of service quality revolve around the identification and satisfaction of customer needs and requirements (Parasuraman et al., 1985 and 1988; and Cronin and

Taylor, 1992). Parasuraman et al. (1985) argue that service quality can be defined as the difference between predicted or expected service (customer expectations) and perceived service (customer perceptions). If expectations are greater than performance, then a service quality gap materializes. This does not necessarily mean that the service is of low quality but rather that the customer expectations have not been met. Pressure to provide quality services in order to remain commercially competitive has forced businesses to develop a better understanding of what service quality means to the customer, and how it could best be measured (Parasuraman et al., 1985 and 1988). It has also been argued that organizations make assumptions about what is important to the consumer, only to discover later that the customers' values are different from the organization's assumptions (Donnelly and

Wisniewski, 1996). Much of the discussion about service quality measurement revolves around the concept of dimensions of service quality, where dimensions refer to a set of attributes which consumers use in evaluating the quality of the service provided (Asubonteng et al., 1996). For the present study, the technique of Multidimensional Scaling has been used to compare ratings of seven banks in the credit card industry. The quality of service for both technical and functional aspects is the key ingredient in achieving customer satisfaction and in turn, the success of service organizations (Gronroos, 1984).

The widely used SERVQUAL model propounded by Zeithaml,Parasuraman and Berry(1990) has been taken as a basis for the study. It focuses on five pivotal gaps in delivering and marketing service. The model depicted in figure 1 below has been adopted to carry out gap

4 analysis of an organization’s service quality performances against customer’s service quality

expectations.

Figure 1

CUSTOMER

Expected Service GAP 5

Perceived Service

Service Delivery External COMPANY Communications GAP 3 GAP 4 to Customer GAP 1

Customer-driven service design and standards

GAP 2

Company perceptions of Consumer expectations

GAP model of service quality

The SERVQUAL method is widely used in service industry to understand employee’s

perceptions of target customers regarding the service needs and to provide a measurement of

the service quality of the organization. It is also applied internally to understand employee’s

perceptions of service quality. The methods involve the development of an understanding of

the perceived service needs of target customers. These measured perceptions of service

quality of the organization in question, are then compared against an organization that is

5 “excellent”. The resulting gap analysis may then be used as a driver for service quality improvement. It also takes into account the perception of the customers of the relative importance of service attributes. This allows the organization to prioritize and to use its resources to improve the most critical service attribute. SERVQUAL based on customer’s assessment was conceptualized as a gap between the customer’s expectation from a class of service provider and their evaluation of their performance of a particular service provider.

Presented as a multidimensional construct in their original formulation it is widely used in variety of studies that include public service, higher education, hotel, banking, consulting, marketing etc. The RATER scale given below identifies the important dimensions:

Tangibles: These are defined as the appearance of physical facilities, equipment,

personal and communication material.

Reliability: Reliability is defined as the ability to perform the promised service

dependably and accurately. Reliability means that the company delivers on its

promises about delivery, service provisions, problem resolution and pricing..

Responsiveness: it is the willingness to help customers and to provide prompt

service. This dimension emphasizes attentiveness and promptness in dealing with

customers request, questions, complains and problem.

Assurance: it is defined as employee’s knowledge of the firm and its employee’s

capacity to inspire trust and confidence to the customer. This dimension is

particularly important for services that the customer perceives as it involves high risk

and/or about which they feel uncertain about their ability to evaluate outcomes.

6 Empathy: it is defined as the caring individualized attention the firm provides its

customer. The essence of empathy is conveying, through personalized or customized

service, that customers are unique and social.

It has been observed that banks should constantly monitor the level of satisfaction among their customers for fulfilling their needs .Ennew et al. (1990) indicated that a comparison of mean scores on the importance of service attributes provides a very effective method of measuring the ability of services to meet the needs of the customers. Moreover, the degree of success in the implementation of enterprise mobilization in the credit card industry is positively correlated to the management performance of external aspects like providing increased customer satisfaction. Customer satisfaction and the salesperson's relation orientation significantly influences the future business opportunities and as the salespersons are able to enhance their relationships with the clients, clients are more satisfied and are more willing to trust, and thus secures the long-term demand for the services (Tam and Wong,

2001). The company and agent's service quality as well as recommendations of friends are factors that significantly affect decisions of purchasing credit cards

Purpose of the study

The study was focused on conducting a sample survey of customers so that their perceived service needs are understood. Customers are asked to answer numerous questions within each dimension that determines

The relative importance of each dimension and the factors within the dimension.

7 A measurement of performance expectation that would relate to an “excellent”

company.

A measurement of the perceptions of the customers for the company

An exploratory study was carried out wherein all the credit card holders were surveyed for collecting the data regarding factors influencing their attitude towards credit cards offered by different banks. Purposive sampling was used to collect data from the respondent belonging to the NCR region (the customer database with the bank was used). The primary data has been collected by personal visit; the sample size is 120. The questionnaire used for the sample survey is a structured and non-disguised questionnaire and consisted of two major sections. The first section intended to collect the various demographic factors; the second section intended to collect the various opinions containing questions about the various factors affecting the consumer attitude towards banks issuing credit cards. A five point rating scale was used to capture the consumers responses ranging from strongly agree to strongly disagree. The different statements regarding the various factors affecting the consumer attitude towards life insurance companies were generated based on literature review as well as expert opinion in an iterative manner. MDS (Multi dimensional scaling) is used to obtain a perceptual map of different banks offering platinum cards.

Analysis and Discussion

Frequency distribution of the sample data was carried out to obtain a demographic profile of the respondents owning the bank credit cards. The figures 2, 3, 4 and 5 show the demographic details of the respondents.

8 Figure 2: Gender Composition

GENDER

FEMALE 31%

MALE 69%

MALE FEMALE

Out of 120 respondents, 69% are male and 31% are female

Figure 3:Occupation-wise profile

OCCUPATION

HOUSEWIFE 13%

SERVICE PROFESSION ALS 49% 23%

BUSINESS 15%

SERVICE BUSINESS PROFESSIONALS HOUSEWIFE

Out of the 120 respondents, 49% were into service, 23% were professional, 15% were having business and 13% were housewives.

9 Figure 4: Education background

EDUCATIONAL BACKGROUND

HIGH SCHOOL POST 13% GRADUATE 34%

GRADUATE 53%

HIGH SCHOOL GRADUATE POST GRADUATE

Out of the 120 respondents, 53% were Graduate, 34% Post Graduate and remaining 13%

High School.

\Figure 5: Income-wise distribution

INCOME

LESS THAN MORE THAN Rs 1.50,000 Rs 3,00,000 23% 32%

BETWEEN Rs1,50,000- 3,00,000 45%

LESS THAN Rs 1.50,000 BETWEEN Rs1,50,000-3,00,000 MORE THAN Rs 3,00,000

Out of 120 respondents, 35% were having income between Rs.1,50,000-3,00,000, 32% respondents were having income of more than Rs.3,00,000 and 23% having income less than

Rs.1,50,000.

10 A two-dimensional aggregate solution has been using INDSCAL.Aggregate solution has

been used as the main purpose is to obtain an overall evaluation of the banks and the

dimensions used in obtaining the respondents’ evaluation. After inputting the 49 column and

120 rows (by using SPSS) a table of responses of 120 respondents’ perception about 7 banks

and their 7 attributes is obtained. A weighted mean of every parameter (like AMEX Fuel

Surcharge Waiver AMEX Cash Back, HSBC Cash Back, HDFC Entertainment Programs

etc)is calculated and to generate a 7*7 matrix. This matrix is used to generate the final

solution given below in Table 2.

Table 2: Respondent-Specific Measures using Ratings for 7 banks

PARAMETERS / Deutsc AMEX HSBC HDFC Stan c ICICI ABN BRANDS he bank AMRO

FUEL 4.2475 4.5551 3.696 3.5468 3.9609 4.0975 2.7358 SURCHARGE WAIVER CASH BACK 2.9527 4.3137 3.539 3.555 3.2574 3.3819 2.8824

WELCOME 2.88 4.3084 3.418 3.4706 3.2791 3.4051 2.8545 GIFTS

ENTERTAINMEN 2.8101 4.3137 3.539 3.8282 2.8101 3.4356 2.7778 T PROGRAMS

SECURITY 2.1745 4.4269 3.279 3.7123 2.6498 3.349 2.4468 FEATURES TRAVEL 2.1441 4.7923 3.814 3.555 3.057 3.117 2.7429 PROGRAMS CREDIT LIMIT 2.679 4.0513 3.279 3.5385 2.8698 3.4051 2.7836

Note: These ratings have been obtained using a five-point Rating scale. (1 denotes Poor and 5 denotes Very Good).To establish the Overall Model Fit and determine the appropriate dimensionality the index of fit or R-square and stress has been computed. Thus R-square indicates goodness of fit, whereas stress value represents badness of fit. So for any research higher value of R-square and lower value of Stress is expected. The high

11 R-square value represents MDS model is well fitted to obtain a perceptual map( refer Table 3).

Table 3: The Lower Triangular matrix Optimally scaled data (disparities) for subject 1

1 2 3 4 5 6 7

1 .000 2 4.217 .000 3 2.240 2.215 .000 4 2.524 2.011 .285 .000 5 1.008 3.292 1.233 1.518 .000 6 1.790 2.459 .580 .836 .836 .000 7 1.518 4.153 1.940 2.149 1.281 1.886 .000

Reliability and Validity

In this case, Stress = .00043 RSQ = .99876.The iteration is given below in Table 4 (Young's S-stress formula 1 is used). Iteration S-stress Improvement

1 .00028 Iterations stopped because S-stress improvement is less than .005000

Table 4: Configuration derived in 2 dimensions

Stimulus Coordinates Dimension

Stimulus Stimulus 1 2 Number Name

1 Deutsche 1.6056 .7226 2 Amex -2.5794 .2045 3 HSBC -.4117 -.2516 4 HDFC -.6589 -.3925 5 STAN C .7125 .2559 6 ICICI -.1207 .2506

12 7 ABN AMRO 1.4526 -.7895

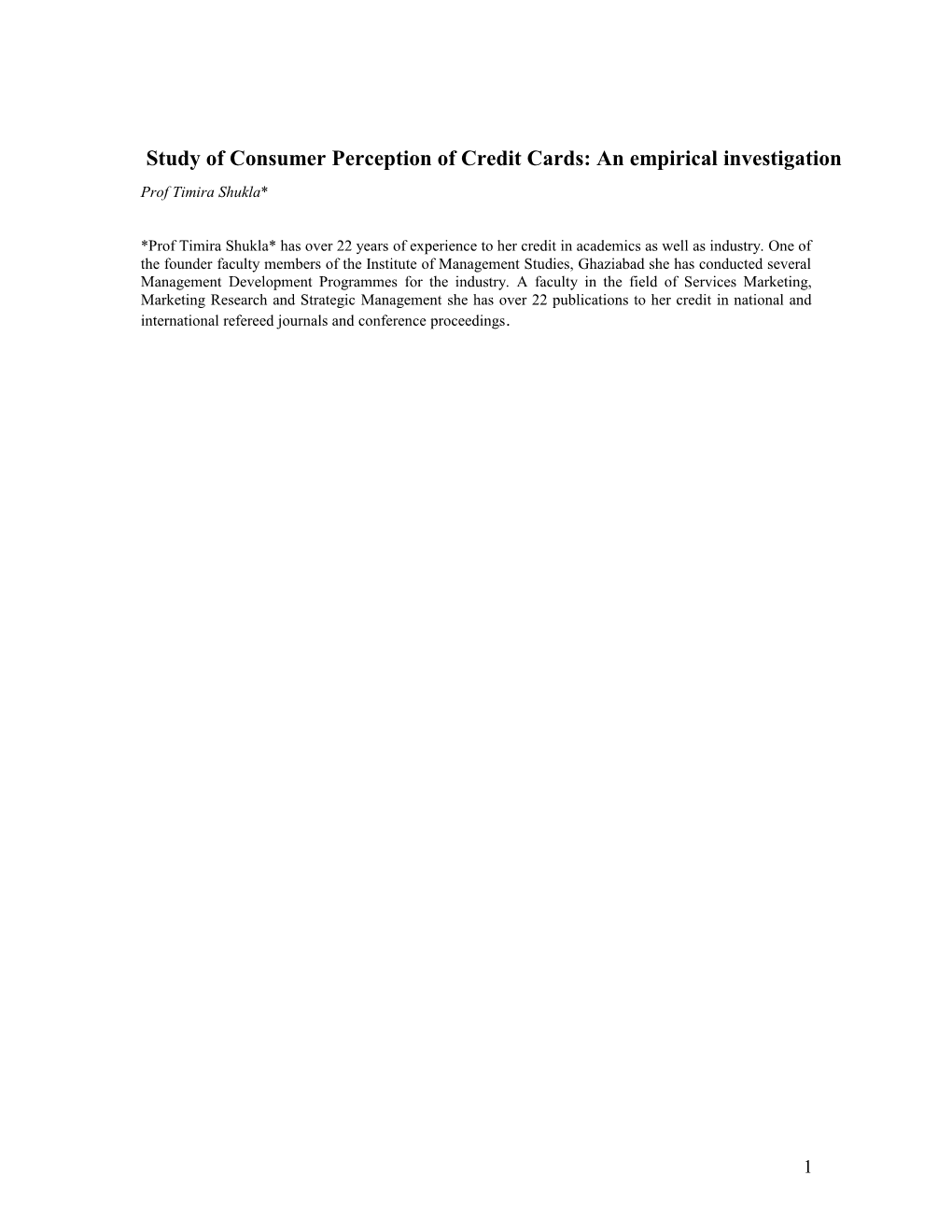

As the dimensionality has been established a perceptual amp (refer Figure 6) has been obtained for the seven banks included in the study.

Figure 6: Derived Stimulus Configuration

Conclusion:

From the above perceptual map it can be inferred that the consumers’ perception about the brands HDFC and HSBC is negative. American Express has no competition with the other banks, as there is no brand near by them. As visible from the graph there is a competition between Deutsche & Standard Chartered. So, in the mind of consumers these 2 banks have shared the same place probably. There is no competition between Deutsche, Amex & ABN

AMRO. The three banks have stayed in three different places in different quadrants. Amex

13 and ABN AMRO have no competition with other banks. There is tough competition between

HSBC and HDFC. ICICI and Standard Chartered is also the competitor of these two banks.

It provides a primary assessment of the position occupied by the bank in the mind of the customer; together with a ranking of the importance of the service criteria. This allows the banks in the credit card business to focus its resources on those parameters which are significant for the customer.

Limitations:

It is an exploratory study and therefore not appropriate for hypothesis testing. A small number of parameters have been included in the study to facilitate the respondents’ task. The respondents’ i.e. the customers of credit cards of different banks may vary in the dimensionality they use. There may be variations over time for said parameters included in the study. The small sample size taken for the study is also a limitation for broader generalization. The study is limited to Noida and Delhi region only. A large area was not covered so the perceptual mapping difference may be there.. In the current research, the method of data collection being self-administered questionnaire, data is limited to the extent of data generation available through this method.

14 References Asubonteng,P McCleary, K.J.Swan,J(1996).”Servqual revisited: a critical review of service quality”, Journal of Services Marketing, 10(6) 62-81

Chang, J.J.and J. Douglas Carroll. 1969. How to Use INDSCAL, A Computer Program for

Individual Differences in Multidimensional scaling. Unpublished paper, Bell Laboratories,

Murray Hill, NJ

Cronin J, Taylor, S. A (1992),” Measuring service quality: a reexamination and extension”,

Journal of Marketing, 58(1), 125-31

Donnelly M and Wisniewski M (1996), "Measuring Service Quality in the Public Sector: The

Potential for SERVQUAL", Total Quality Management, Vol. 7, No. 4, pp. 357-365.

Ennew C and M Wright (1990), “Retail Banks and Organisational Change evidence from

UK” International Journal of Bank Marketing, Vol 8,1 pp4-9

Green, P.E. 1975. On the Robustness of Multidimensional Scaling Techniques, Journal of

Marketing Research 12 (February): 73-81

Groonroos C (1984), “A service quality model and marketing implications” European

Journal of Marketing, 18(4), 36-44

Malhotra Naresh (1999). Marketing Research : An Applied Orientation, 3rd ed. Prentice Hall Inc.

15 Parasuraman A, Berry L and Zeithaml V (1985” A Conceptual Model of service Quality and its Implications for future research” Journal of Marketing, 49 (Fall), 41-50

Parasuraman A, Berry L and Zeithaml V (1991), "Refinement and Reassessment of the

SERVQUAL Scale", Journal of Retailing, Vol. 67 No. 4, pp. 420-450.

Parasuraman A, Zeithaml V and Berry L (1994), "Alternative Scales for Measuring Service

Quality: A Comparative Assessment Based on Psychometric and Diagnostic Criteria",

Journal of Retailing, Vol. 70, No. 3, pp. 193-194.

Parasuraman A, Zeithaml V and Berry L (1995),Delivering Quality Service:Balancing

Customer Perceptions and Expectations (New York:The Free Press,1990)

The Marketing Whitebook 2007-2008 published by Businessworld

Websites

www.creditcards-india.com www.economictimes.com www.creditcards.com

16 Annexure 1: Questionnaire

Name …………………………………………………………………..

Age …………………………………………………………………….

Gender - MALE FEMALE

Occupation …………………………………………………………….

Educational Background………………………………………………. a) High School: b) Graduate: d) Post graduate: d) any other please specify:

Income…………………………………………………………………. a) Less than 1, 50,000 b) between 1, 50,000-3, 00,000 c) More than 3, 00,000

Number of Family Members…………………………………………… a) Two b) Three c) More than three

1) Do you have a credit card? a) Yes b) No

2) Which Bank’s platinum card do you have? a) Deutsche Bank b) American Express c) HSBC d) HDFC e) Standard Chartered bank f) ICICI Bank g) ABN AMRO

17 3) Rank the following brands on the scale of 1-5

1-Poor 5- very good

BANKS / DEUTSCH AMERICAN HSBC HDFC STANDARD ICICI ABN PARAMETER E EXPRESS CHARTERE BANK AMRO S BANK D BANK FUEL SURCHARGE WAIVER CASH BACK / REWARD POINTS WELCOME GIFTS ENTERTAIN- MENT PROGRAMS SECURITY FEATURES TRAVEL PROGRAMS CREDIT LIMIT

18