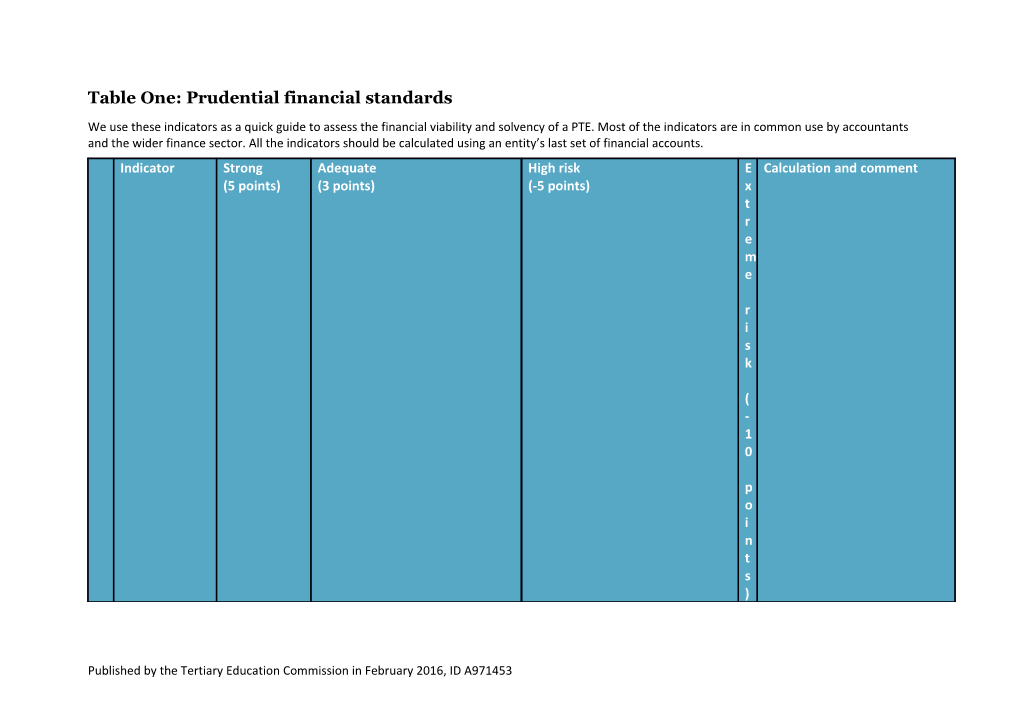

Table One: Prudential financial standards

We use these indicators as a quick guide to assess the financial viability and solvency of a PTE. Most of the indicators are in common use by accountants and the wider finance sector. All the indicators should be calculated using an entity’s last set of financial accounts. Indicator Strong Adequate High risk E Calculation and comment (5 points) (3 points) (-5 points) x t r e m e

r i s k

( - 1 0

p o i n t s )

Published by the Tertiary Education Commission in February 2016, ID A971453 1 Net tangible 10%+ of total 5% to 10% of total revenue Less than $50,000 or less than 2% of Z Total equity less intangible assets ratio revenue total revenue e assets/Total revenue r o

o r l e s s 2 Liquid assets ratio 16%+ 8%+ Less than 5% Z Cash + bank + readily liquefiable e investments-bank overdrafts/ Annual r cash outflow from operations o Readily liquefiable investments include financial assets that can be o liquidated within 90 days without r materially affecting operations n The assessment may include TEC e approved undrawn committed g borrowing facilities with a term a greater than one year and TEC t approved investments with a Group i central treasury v e 3 Working capital 120%+ 100% to 120% Less than 75% or where the working L Current assets/Current liabilities ratio capital deficit exceeds annual net e cashflow from operations s s t h a n

2

Published by the Tertiary Education Commission in February 2016, ID A971453 0 % 4 Profitability ratio 8%+ (i.e. 0 to 8% Loss>8% of total revenue or >30% of S Net surplus after tax/Total revenue generates a total equity i commercial z return) e

o f l o s s p r e c l u d e s P T E

f r o m

m e e t i

Published by the Tertiary Education Commission in February 2016, ID A971453 n g i t s b il l s a s t h e y f a ll d u e 5 Net cash flow 111%+ 108% to 111% Ratio<100% S Annual cash inflow from from operations i operations/Annual cash outflow ratio g from operations n s t h e

P T E

i s

Published by the Tertiary Education Commission in February 2016, ID A971453 n o t g e n e r a t i n g e n o u g h

c a s h

t o

m e e t b il l s

Published by the Tertiary Education Commission in February 2016, ID A971453 a s t h e y f a ll d u e 6 Debt equity ratio Less than 20% 20% to 33% 50% to 80% 8 Debt/Debt plus net tangible assets 0 Debt excludes accounts payable, % student fees in advance, and current + liabilities unlikely to result in a cash outflow. Debt includes shareholder o current accounts where these are a r liability of the PTE n e g a t i v e

r a t i o

Published by the Tertiary Education Commission in February 2016, ID A971453 Table Two: Further financial indicators used

Where there are concerns with the financial health of a PTE then we use this wider set of risk indicators; supplement these with additional financial and educational performance information, and follow up with a discussion with the PTE and its financial advisors to inform the assessment.

Indicator Strong Adequate High Risk Extre Calculation and comment (5 points) (3 points) (-5 points) me Risk (-10 poin ts) 7 Net surplus pre 8%+ 0 to 8%+ Loss>8% of total revenue or >30% of Size Total surplus + shareholder shareholder total equity of loss wages + directors fees + wages and preclu subvention payments/Total directors fees des revenue PTE from meeti ng its bills as they fall due 8 Variability in Refer Variability in earnings table below This indicator looks at both the earnings year on variability in earnings and the year direction of travel 9 Shareholders’ 75%+ 60% to 75% Less than 40% Zero Total equity minus funds ratio or intangibles/Total assets minus less intangibles and pre-paid fees (liability) Trust funds may need to be excluded from total tangible assets if the amounts are material

Published by the Tertiary Education Commission in February 2016, ID A971453 Equity excludes Shareholder current accounts 10 Going concern Confirmation of Confirmation of going concern status Auditor or reviewing independent Audit Measures the outcome of the attestation by going concern by auditor or reviewing independent accountant questions aspects of the or or assessment auditor or status by auditor accountant (must be for the latest “going concern” test; e.g. “fundamental revie reviewing of Big 10 accounts) uncertainty” or “emphasis of matter” or wing independent international notes inability to assess – or the TEC indep accountant accounting firms considers there is evidence the PTE may enden (include: not be a going concern currently or in t Deloitte, PWC, future accou E&Y, Grant ntant Thornton, BDO) consi or OAG through ders an external audit the opinion (must PTE be for the latest not to accounts) be a going conce rn Failur e of one or more of the solve ncy tests in the Comp anies Act 11 Other factors None Indications there may be factors with Concerns expressed by a government Evide The factor considered must be a negative bearing on the PTE’s agency, TEC IM, or TEC reviewer of nce of verifiable, objective, evidence financial viability. This includes “going concern” issues or other factors insolv based and material. This does

Published by the Tertiary Education Commission in February 2016, ID A971453 possible future funding reductions likely to have a material impact on the ency not exclude commercial PTE’s solvency. Includes entities that (see judgements made by suitably receive a “zero allocation” letter Comp qualified accountants anies Act defini tion) 12 Meets funding 99% to 105% of 97% to 99% Need for borrowing or TEC deferment of Risk Funding dollars commitments contracted/ recovery to continue to operate or of delivered/funding dollars (prior year & allocated delivers less than 90% of allocated failur allocated. Across all TEC funds current year) provision at the funding at start of year e to start of the year compl ete tuitio n to all stude nts 13 Change in roll EFTS increase EFTS increase in current year over EFTS decline year on year over the last EFTS EFTS figures are from your last size (measured year on year previous year three years declin December full year SDR. by EFTS) over the last e by The TEC may use prospective three years over year information if there is a 30% risk of EFTS enrolment on underachievement prior year and/o r TEC consi dering disco ntinui ng fundi ng 14 Total revenue Increases year Increases in current year over Total revenue declines year on year Total Total revenue from all sources.

Published by the Tertiary Education Commission in February 2016, ID A971453 on year over the previous year over the last three years reven Based on the most recent last three years ue annual financial accounts declin The TEC reserves the right to es by use prospective information if over there is a risk of total revenue 30% materially declining on prior year or TEC consi dering disco ntinui ng fundi ng 15 Interest coverage Greater than Greater than 3.0:1 but less than Less than 1.5:1 but greater than 1.0:1 Less Earnings before interest ratio 12.0:1 or “Divide 12.0:1 than expense and tax divided by by zeros” or 1.0:1 interest expense interest costs under $10,000

Published by the Tertiary Education Commission in February 2016, ID A971453 Earnings variability

The following table looks at how the Net surplus to Total revenue financial indicator has changed over time. The risk category and score assigned in column 1 depends upon the observable characteristics in the further columns.

Net Surplus Financial results Ratio Variability Direction of travel Comment Strong Positive net surplus Previous two years of Less than 300 Improving ratio Must have all (score 5) surplus and outlook is a percentage points characteristics surplus Latest net surplus above 20% Previous year in surplus Less than 500 Positive or negative Must have all percentage points characteristics Adequate Positive net surplus Previous year in surplus Less than 500 Improving ratio Must have all (score 3) percentage points characteristics Latest net surplus above 20% Previous year in surplus Less than 700 Positive or negative Must have all percentage points characteristics Positive net surplus Previous two years in Less than 500 basis Positive or negative Must have all surplus points characteristics Poor Positive net surplus Previous year in surplus or Less than 700 Positive or negative Choose best description (score 1) loss percentage points of characteristics here or below Net loss Previous year in surplus or Less than 300 basis Positive or negative Choose best fit loss points Latest net surplus above 20% Previous year in surplus or Less than 1000 Positive or negative Choose best fit loss percentage points Positive net surplus Previous two years of Above 500 percentage Positive or negative Choose best fit surplus points High risk Positive net surplus Previous year in surplus or Above 700 percentage Positive or negative Choose best fit (score -5) loss points Net loss Previous year in surplus or Above 300 percentage Positive or negative Choose best fit loss points Net loss greater than 50% of previous Previous year is a loss Not a factor Not a factor Choose best fit year’s total equity Net loss Previous two years of Not a factor Not a factor Choose best fit losses Extreme risk Net loss greater than the previous Not a factor Not a factor Not a factor Must have characteristic. (score -10) year’s or the existing year’s net If met then use this

Published by the Tertiary Education Commission in February 2016, ID A971453 tangible assets category Two years of losses and forecast loss Not a factor Not a factor Not a factor Must have characteristic. for current budget year If met then use this category

Published by the Tertiary Education Commission in February 2016, ID A971453 Table Three: Calculating the overall financial viability risk score

For each financial indicator used, including the prudential financial standards, a score is assigned. By summing the scores and dividing by the number of indicators it is possible to assign a PTE an overall score (ranging from -10 to 5). The higher the score the stronger the financial viability is.

A PTE’s overall risk classification is then determined two ways:

1. PTEs that fail the minimum prudential financial standards for their last set of accounts or current budget automatically receive either a High (D) or Extreme (E) risk grade. If a PTE does not meet the minimum prudential financial standards, but its overall risk indicator score is calculated as a (C) or better then the PTE will be assigned a High risk (D) category, otherwise the PTE is categorised as Extreme risk (E).

2. In all other cases a PTE’s classification is determined as follows:-

Overall average (mean) score Overall assessment Greater than 4.5 Strong (A); Between 3 and 4.5 Adequate (B) Between 2.5 and 3 Poor (C) Between 1.0 and 2.5 High risk (D) Less than 1.0 Extreme risk (E)

If information is not available to calculate some indicators the inability to assess will be noted for future follow-up and the average will be calculated as the average of the available scores.

Published by the Tertiary Education Commission in February 2016, ID A971453