UNO Template

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1332 Nippon Suisan Kaisha, Ltd. 50 1333 Maruha Nichiro Corp. 500 1605 Inpex Corp

Nikkei Stock Average - Par Value (Update:August/1, 2017) Code Company Name Par Value(Yen) 1332 Nippon Suisan Kaisha, Ltd. 50 1333 Maruha Nichiro Corp. 500 1605 Inpex Corp. 125 1721 Comsys Holdings Corp. 50 1801 Taisei Corp. 50 1802 Obayashi Corp. 50 1803 Shimizu Corp. 50 1808 Haseko Corp. 250 1812 Kajima Corp. 50 1925 Daiwa House Industry Co., Ltd. 50 1928 Sekisui House, Ltd. 50 1963 JGC Corp. 50 2002 Nisshin Seifun Group Inc. 50 2269 Meiji Holdings Co., Ltd. 250 2282 Nh Foods Ltd. 50 2432 DeNA Co., Ltd. 500/3 2501 Sapporo Holdings Ltd. 250 2502 Asahi Group Holdings, Ltd. 50 2503 Kirin Holdings Co., Ltd. 50 2531 Takara Holdings Inc. 50 2768 Sojitz Corp. 500 2801 Kikkoman Corp. 50 2802 Ajinomoto Co., Inc. 50 2871 Nichirei Corp. 100 2914 Japan Tobacco Inc. 50 3086 J.Front Retailing Co., Ltd. 100 3099 Isetan Mitsukoshi Holdings Ltd. 50 3101 Toyobo Co., Ltd. 50 3103 Unitika Ltd. 50 3105 Nisshinbo Holdings Inc. 50 3289 Tokyu Fudosan Holdings Corp. 50 3382 Seven & i Holdings Co., Ltd. 50 3401 Teijin Ltd. 250 3402 Toray Industries, Inc. 50 3405 Kuraray Co., Ltd. 50 3407 Asahi Kasei Corp. 50 3436 SUMCO Corp. 500 3861 Oji Holdings Corp. 50 3863 Nippon Paper Industries Co., Ltd. 500 3865 Hokuetsu Kishu Paper Co., Ltd. 50 4004 Showa Denko K.K. 500 4005 Sumitomo Chemical Co., Ltd. 50 4021 Nissan Chemical Industries, Ltd. 50 4042 Tosoh Corp. 50 4043 Tokuyama Corp. 50 WF-101-E-20170803 Copyright © Nikkei Inc. All rights reserved. 1/5 Nikkei Stock Average - Par Value (Update:August/1, 2017) Code Company Name Par Value(Yen) 4061 Denka Co., Ltd. -

Japan Monthly Highlights Product Manager MONTHLY

31 August 2015 Asia Pacific/Japan Equity Research Product Marketing Japan Monthly Highlights Product Manager MONTHLY Daisuke Takato 813 4550 9671 [email protected] August 2015 ■ August saw a rout in global equities triggered by concerns over China's economic stability. This came on the back of a prolonged commodities slump, an emerging markets slowdown, and increased currency fluctuations. It is precisely in times of volatility that investment opportunities are created, we highlight stocks that look to have been oversold despite solid fundamentals and that we think investors should hold. Examples include Lion (4912), Shinsei (8303), Nomura Real Estate (3231), Japan Airlines (9201), Fuji Heavy (7270), DaikyoNishikawa (4246), and Murata (6981). ■ The construction sector is poised for long-term growth, owing to the repatriation of Japanese manufacturing capacity amid a weaker yen, the rising need to renovate old buildings, and a slate of large infrastructure projects including the 2020 Summer Olympics. Construction order prices could also rise given the dearth of skilled workers. These factors should lift share prices for construction, cement and steel, writes analyst Masahiro Mochizuki in a Connection Series report with materials analyst Jun Yamaguchi and Shinya Yamada. We upgraded our stances on the construction and cement sectors from Market Weight to OVERWEIGHT and maintained our OVERWEIGHT on the steel sector. We added Shimizu (1803) and Taiheiyo Cement (5233) to the Japan Focus List. ■ Hideyuki Maekawa says semiconductor capacity utilization is at the lowest levels in the post-Lehman era, as additional production cutbacks have been made in August across all applications and process nodes. -

Gray Portland Cement and Cement Clinker from Japan

Gray Portland Cement and Cement Clinker from Japan Investigation No. 731-TA-461 (Fourth Review) Publication 4704 June 2017 U.S. International Trade Commission Washington, DC 20436 U.S. International Trade Commission COMMISSIONERS Rhonda K. Schmidtlein, Chairman David S. Johanson, Vice Chairman Irving A. Williamson Meredith M. Broadbent F. Scott Kieff Catherine DeFilippo Director of Operations Staff assigned Carolyn Carlson, Investigator Gregory LaRocca, Industry Analyst Andrew Knipe, Economist Heng Loke, Attorney Fred Ruggles, Supervisory Investigator Address all communications to Secretary to the Commission United States International Trade Commission Washington, DC 20436 U.S. International Trade Commission Washington, DC 20436 www.usitc.gov Gray Portland Cement and Cement Clinker from Japan Investigation No. 731-TA-461 (Fourth Review) Publication 4704 June 2017 CONTENTS Page Determination .............................................................................................................................1 Views of the Commission .............................................................................................................3 Information obtained in the review ........................................................................................... I-1 Background ...................................................................................................................................... I-1 Responses to the Commission's notice of institution ..................................................................... -

Type of Dust Density Meter Advantage: Cheap ① Optical Disadvantage : the Detection Penetration Type Sensitivity Is Low, and Optical Axis Shifts

To whom it may concern Apr.24.2018 Light Scattering Method Dust Density Meter (Relative continuous measuring monitor system) Model DDM- f C Technical Introduction R&D , Manufacture , Sales , Maintenance Tanaka Electric Laboratory Co., Ltd. Table of contents • Corporate profile • Necessity of dust density meter for CEMS • Type of dust density meter • About our model : DDM-fC • Recent news! JIS B7996 • Installation photos • Customer list Corporate profile Established 17.Dec. in 1963 Capital 25,000,000 JPY Employee 35 Business Scope : 1. Dust density meter R&D, manufacture 2. Electronics instruments design & manufacture for industry use 3.PCB design , mounting & soldering. About CEMS (Continuous Emission Monitoring System) ■ CEMS is an equipment used to measure emissions discharged from stationary sources. ■ CEMS helps in the continuous assessment of pollutants discharged into the atmosphere in the form of exhaust gases from combustion or industrial processes. ■ Initially, CEMS was used to monitor oxygen, carbon dioxide, carbon monoxide. ■ Currently, CEMS including dust is used to adhere to air emission standards. CEMS Instruments Our Products HCl Gas analyzer Dust density meter DDM-fC NOx, SO2 , CO, CO2, O2 Gas analyzer A lot of dust from chimney ! The emitted dust exceeded the applicable limit concentrations, the residents in adjacent plants will complain to the relevant authorities. Type of dust density meter Advantage: Cheap ① Optical Disadvantage : The detection penetration type sensitivity is low, and optical axis shifts. ② Electrode type Advantage : Easy installation. Disadvantage : The moisture influences to the output signal. This type cannot be span-calibration under plant operation. Our system ! ③ Light scattering type Advantage: Low concentration can be measured. -

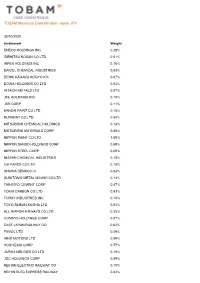

TOBAM Maximum Diversification Japan JPY

TOBAM Maximum Diversification Japan JPY 30/10/2020 Instrument Weight ENEOS HOLDINGS INC 0.28% IDEMITSU KOSAN CO LTD 0.51% INPEX HOLDINGS INC 0.16% DAICEL CHEMICAL INDUSTRIES 0.03% DENKI KAGAKU KOGYO K K 0.07% DOWA HOLDINGS CO LTD 0.04% HITACHI METALS LTD 0.07% JFE HOLDINGS INC 0.10% JSR CORP 0.11% KANSAI PAINT CO LTD 0.15% KURARAY CO LTD 0.04% MITSUBISHI CHEMICAL HOLDINGS 0.13% MITSUBISHI MATERIALS CORP 0.06% NIPPON PAINT CO LTD 1.09% NIPPON SANSO HOLDINGS CORP 0.59% NIPPON STEEL CORP 0.09% NISSAN CHEMICAL INDUSTRIES 0.18% OJI PAPER CO LTD 0.10% SHOWA DENKO K K 0.03% SUMITOMO METAL MINING CO LTD 0.13% TAIHEIYO CEMENT CORP 0.07% TOKAI CARBON CO LTD 0.83% TORAY INDUSTRIES INC 0.10% TOYO SEIKAN KAISHA LTD 0.04% ALL NIPPON AIRWAYS CO LTD 0.25% COMSYS HOLDINGS CORP 0.07% EAST JAPAN RAILWAY CO 0.02% FANUC LTD 0.49% HINO MOTORS LTD 0.05% HOSHIZAKI CORP 0.77% JAPAN AIRLINES CO LTD 0.16% JGC HOLDINGS CORP 0.09% KEIHAN ELECTRIC RAILWAY CO 0.10% KEIHIN ELEC EXPRESS RAILWAY 0.04% TOBAM Maximum Diversification Japan JPY 30/10/2020 Instrument Weight KEIO CORP 0.17% KINDEN CORP 0.05% KINTETSU CORP 0.20% KOMATSU LTD 0.06% KURITA WATER INDUSTRIES LTD 0.09% KYOWA EXEO CORP 0.06% KYUSHU RAILWAY COMPANY 0.08% LIXIL CORP 0.47% MABUCHI MOTOR CO LTD 0.05% MAKITA CORP 0.02% MITSUBISHI CORP 0.38% MITSUBISHI HEAVY INDUSTRIES 0.15% MIURA CO LTD 0.12% MONOTARO CO LTD 0.55% NAGOYA RAILROAD CO LTD 0.14% NIHON M&A CENTER INC 0.23% ODAKYU ELECTRIC RAILWAY CO 0.21% PARK24 CO LTD 0.48% SEIBU HOLDINGS INC 0.06% SEINO HOLDINGS CO LTD 0.05% SG HOLDINGS CO LTD 1.34% SHIMIZU -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd. -

Low-Activation Reinforced Concrete Design Methodology (9) - Low-Activation Concrete Based on Limestone Aggregates and White Cement-

Transactions, SMiRT 19, Toronto, August 2007 Paper # HW1/4 Low-Activation Reinforced Concrete Design Methodology (9) - Low-Activation Concrete Based on Limestone Aggregates and White Cement- Masaharu Kinno1), Norichika Katayose1), Ken-ichi Kimura1), Hirokazu Nishida1), Yusuke Fujikura1), Takao Tanosaki2), Masaki Takimoto2) and Akira Hasegawa3) 1) Technology Development Division, Fujita Corporation, Atsugi, Japan 2) Taiheiyo Cement Corporation, Tokyo, Japan 3) Tohoku University, Sendai, Japan ABSTRACT Manufacturing tests regarding the 1/30-low-activation concrete for a nuclear power plant were performed. Here, “1/30-low-activation” concrete denotes that the activity reduction rate to the ordinary concrete is designed to be 1/30. The detailed data regarding the concentrations of Co and Eu in limestone, white cement, silica fume, and limestone powder were obtained. The low-heat type of 1/30-low-activation concrete was developed by admixing with the low-activation limestone powder, and the low-heat type of 1/50-low-activation concrete was developed by admixing with the low-activation silica fume and/or the low-activation limestone powder. By admixing with the B4C of which concentration is from 1 to 2.5 w%, the total residual radioactivity reduction ratio of the above low-activation concrete to the ordinary concrete, in ΣDi/Ci unit, is estimated to be from 1/100 to 1/1,500. INTRODUCTION Concrete-widely used in a nuclear plant as a neutron shield because of its excellent shielding properties and low cost-includes a large quantity of residual radionuclide induced by neutron irradiation, and this concrete still remains to an enormous degree as radioactive waste after decommissioning. -

FTSE Publications

2 FTSE Russell Publications 20 May 2020 FTSE Japan Indicative Index Weight Data as at Closing on 31 March 2020 Constituent Index weight (%) Country Constituent Index weight (%) Country Constituent Index weight (%) Country 77 Bank 0.03 JAPAN Denso Corporation 0.45 JAPAN Isetan Mitsukoshi Holdings 0.06 JAPAN ABC-Mart 0.04 JAPAN Dentsu Inc 0.13 JAPAN Isuzu Motors 0.1 JAPAN Acom 0.05 JAPAN DIC 0.06 JAPAN Ito En 0.09 JAPAN Advantest Corp 0.24 JAPAN Disco 0.17 JAPAN Itochu Corp 0.87 JAPAN Aeon 0.48 JAPAN DMG Mori Seiki 0.03 JAPAN Itochu Techno Solutions 0.08 JAPAN AEON Financial Service 0.04 JAPAN Dowa Holdings 0.04 JAPAN Itoham Yonekyu Holdings 0.02 JAPAN Aeon Mall 0.05 JAPAN East Japan Railway 0.84 JAPAN Iyo Bank 0.04 JAPAN AGC 0.14 JAPAN Ebara 0.06 JAPAN Izumi Co Ltd 0.03 JAPAN Aica Kogyo 0.05 JAPAN Eisai 0.6 JAPAN J Front Retailing 0.06 JAPAN Ain Pharmaciez 0.05 JAPAN Electric Power Development 0.1 JAPAN Japan Airlines 0.06 JAPAN Air Water 0.08 JAPAN Ezaki Glico 0.07 JAPAN Japan Airport Terminal 0.06 JAPAN Aisin Seiki Co 0.13 JAPAN FamilyMart 0.13 JAPAN Japan Aviation Electronics 0.02 JAPAN Ajinomoto Co 0.28 JAPAN Fancl Corp 0.05 JAPAN Japan Exchange Group 0.29 JAPAN Alfresa Holdings 0.1 JAPAN Fanuc 0.8 JAPAN Japan Petroleum Exploration 0.02 JAPAN Alps Alpine 0.06 JAPAN Fast Retailing 0.65 JAPAN Japan Post Bank 0.12 JAPAN Amada 0.08 JAPAN FP Corporation 0.05 JAPAN Japan Post Holdings 0.32 JAPAN Amano Corp 0.05 JAPAN Fuji Electric 0.09 JAPAN Japan Post Insurance 0.07 JAPAN ANA Holdings 0.08 JAPAN Fuji Media Holdings 0.01 JAPAN Japan Steel -

Making Concrete Change: Innovation in Low-Carbon Cement and Concrete

Chatham House Report Johanna Lehne and Felix Preston Making Concrete Change Innovation in Low-carbon Cement and Concrete #ConcreteChange Chatham House Report Johanna Lehne and Felix Preston Energy, Environment and Resources Department | June 2018 Making Concrete Change Innovation in Low-carbon Cement and Concrete The Royal Institute of International Affairs Chatham House 10 St James’s Square London SW1Y 4LE T: +44 (0) 20 7957 5700 F: + 44 (0) 20 7957 5710 www.chathamhouse.org Charity Registration No. 208223 Copyright © The Royal Institute of International Affairs, 2018 Chatham House, the Royal Institute of International Affairs, does not express opinions of its own. The opinions expressed in this publication are the responsibility of the author(s). All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical including photocopying, recording or any information storage or retrieval system, without the prior written permission of the copyright holder. Please direct all enquiries to the publishers. ISBN 978 1 78413 272 9 A catalogue record for this title is available from the British Library. Printed and bound in Great Britain by Latimer Trend. The material selected for the printing of this report is manufactured from 100% genuine de-inked post-consumer waste by an ISO 14001 certified mill and is Process Chlorine Free. Typeset by Soapbox, www.soapbox.co.uk Cover image: Staircase, Benesse Museum House, Naoshima, Japan. Copyright © Education Images/UIG via Getty Images -

6 RMS (Carlos Cabrera)

Industrial Facilities and Business Interruption Carlos Cabrera Lead Catastrophe Risk Modeler Risk Management Solutions, Inc. Preliminary Briefing on Japan’s Tohoku Earthquake April 28, 2011 Outline Direct vs. Contingent Business Interruption Mitigation: Business Continuity Plan (BCP) Field Reconnaissance Process Field Observations: Light and Heavy Industrial Facilities Large Commercial Facilities Key Drivers of Business Interruption Types of Business Interruption Direct BI: A property sustains damage that interrupts its ability to conduct business Tohoku Semiconductor Sendai-Miyagi Manufacturing Plant; north side of Sendai City; (38.355, 140.855) Produced microcontrollers, analog integrated circuits and sensors products; 600 employees Sustained extensive equipment and infrastructure damage on March 11 and in the April 7 aftershock Hazardous chemical spills made repairs especially difficult Its parent company, Freescale Semiconductor, announced on April 5th that it would permanently close the facility Production is being transferred to other Freescale facilities in Texas and Arizona $90 Million USD is the total loss as of April 20th; $49M non-cash asset impairment, $15M non-cash damaged inventory, $26M cash employee and contract termination Types of Business Interruption Direct BI: A property sustains damage that interrupts its ability to conduct business Source: www.nytimes.com Image: Clean room in the Renesas Electronics Microcontroller Manufacturing Facility; Naka factory, Hitachinaka, Ibaraki Prefecture Two weeks to complete -

Low-Activation Reinforced Concrete Design Methodology -Fundamental Investigation for Various Types of Low-Activation Concrete

Fujita Technical Research Report No.43 2007 Low-Activation Reinforced Concrete Design Methodology -Fundamental Investigation for various Types of Low-Activation Concrete- Ken-ichi Kimura, Masaharu Kinno, Hirokazu Nishida, Noritcika Katayose, Mikihiro Nakata2), Katsumi Hayashi3), Mikio Uematsu4) and Akira Hasegawa1) Abstract Concrete is very useful and inexpensive material. However after long-term use in a nuclear powerplant it can become both expensive and difficult. One possible solution to this problem is the use of low-activation concrete, which has much less residual radioactivity even after many years of operation. In this paper, we evaluated fifty raw materials by radiochemical analyses, which assessed the quantities of dominant trace elements for the activation under specific conditions. From these investigations, three kinds of aggregates (fused alumina ceramics, silica sand and limestone) and two kinds of cements (high alumina cement and white cement) were selected as raw materials for the low–activation concrete. Finally, six types of low-activation concrete and two mortars were proposed and their mix proportions described so as to make them suitable for different areas within nuclear plants. Areas of investigation for further improvements were also identified. §1. Introduction to the decommissioning of nuclear power plants. The Concrete enveloping a nuclear reactor retains key areas of programme include; investigation of residual radioactivity after decommissioning. Disposal residual radionuclides in construction materials of such radioactive concrete is very costly and requires around a reactor, improvement and development of strict supervision. From this point of view, we have low-activation materials, and establishment of developed a new concrete that retains little residual low-activation design method for the reduction of the radioactivity – i.e. -

Moving to Aggregate Taiheiyo Cement Group Companies’ Technologies Owned by Group Companies

GLOBAL NETWORK Net Sales Holding Company ………………………… TAIHEIYO CEMENT GROUP MAIN BUSINESS LOCATIONS Representative Ofce …………………… Cement Plant ……………………………… Clinker Grinding Plant …………………… SUSTAINABILITY Distribution Terminal ……………………… CORPORATE PROFILE The Taiheiyo Cement Group aspires to leadership in pioneering a sustainable future for our planet. Committed to doing business in ways that contribute to economic development, are environmentally efficient, and make a positive difference to society, we are working to be a leader of our industry in the Pacific Rim region. Ordinary Income In line with this, we aim to maximize our corporate value by making efficient use of managerial resources in an integrated fashion to minimize costs and risks as we strengthen our overall earnings capacity and financial structure. We are simultaneously committed to fulfilling our corporate social responsibilities and the cement industry’s mission of ensuring DOMESTIC MAIN BUSINESS LOCATIONS plentiful supplies of cement and concrete, both materials that are indispensable for building and maintaining social infrastructure that secures the safety and assets of the population. We are also committed to helping protect the environment and advancing a new socioeconomic order built on closed loop materials sourcing by putting our cement plants and home-grown recycling capabilities and technologies to work to reduce, recycle, and reuse large volumes of waste material and by-products. CONTENTS FINANCIAL HIGHLIGHTS Net Income (Millions of yen) (Thousands of U.S. dollars)