CHAPTER 4 THE INCOME STATEMENT, COMPREHENSIVE INCOME, AND THE STATE MENT OF CASH FLOWS

Overview The purpose of the income statement is to summarize the profit-generating activities that occurred during a particular reporting period. Comprehensive income includes net income as well as a few gains and losses that are not part of net income and are considered other comprehensive income items instead. The purpose of the statement of cash flows is to provide information about the cash receipts and c ash disbursements of an enterprise that occurred during the period. This chapter has a twofold purpose: (1) to consider important issues dealing with the content, pres entation, and disclosure of net income and other components of comprehensive income and (2) to pr ovide an overview of the statement of cash flows, which is covered in depth in Chapter 21.

Learning Objectives LO4-1 Discuss the importance of income from continuing operations and describe its components. LO4-2 Describe earnings quality and how it is impacted by management practices to manipulate earnings. LO4-3 Discuss the components of operating and nonoperating income and their relationship to earnings quality. LO4-4 Define what constitutes discontinued operations and describe the appropriate income statement presentation for these transactions. LO4-5 Define earnings per share (EPS) and explain required disclosures of EPS for certain income statement components. LO4-6 Explain the difference between net income and comprehensive income and how we report components of the difference. LO4-7 Describe the purpose of the statement of cash flows. LO4-8 Identify and describe the various classifications of cash flows presented in a statement of cash flows. LO4-9 Discuss the primary differences between U.S. GAAP and IFRS with respect to the income statement, statement of comprehensive income, and statement of cash flows.

Lecture Outline Part A: The Income Statement and Comprehensive Income

I. Income from Continuing Operations A. Income from continuing operations includes the revenues, expenses, gains, and losses that will probably continue in future periods. 1. Income tax expense always is shown as a separate expense. 2. A distinction often is made between operating and nonoperating income. (T4-1) 3. A single-step income statement format groups all revenues and gains together and all e xpenses and losses together. (T4-2)

Instructors Resource Manual 4-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. 4. A multiple-step income statement format includes a number of intermediate subtotals b efore arriving at income from continuing operations. (T4-3) 5. There are more similarities than differences between income statements prepared accor ding to U.S. GAAP and those prepared applying IFRS. (T4-4)

II. Earnings Quality A. Earnings quality refers to the ability of reported earnings (income) to predict a company’s future earnings. 1. To enhance predictive value, analysts try to separate a company’s transitory earnings effects from its permanent earnings. 2. Many believe that corporate earnings management practices reduce the quality of earni ngs. Two major methods used by managers to manipulate income are (1) income shift ing and (2) income statement classification. B. Not all items included in operating income should be considered indicative of a company’s permanent earnings. (T4-5) 1. Restructuring costs include costs associated with shutdown or relocation of facilities o r downsizing of operations. GAAP requires these costs to be expensed in the period(s) incurred. 2. Asset impairment losses, inventory write-down charges, losses from natural disasters s uch as earthquakes and floods, and gains and losses from litigation settlements are oth er operating expenses that call into question the issue of earnings quality. 3. Earnings quality is affected by revenue issues as well. C. Some nonoperating items have generated considerable discussion with respect to earnings quality, notably gains and losses generated from the sale of investments. (T4-6)

III. Discontinued operations A. Discontinued operations involve the disposal or planned disposal of a component of an ent ity. 1. Discontinued operations must be reported separately, below income from continuing operations. (T4-7) 2. The objective is to report all of the income effects of a discontinued operation separately. That’s why we include the income tax effect in this separate presentation rather than report it as part of income tax expense related to continuing operations. The process of associating income tax effects with the income statement components that create those effects is referred to as intraperiod tax allocation. B. What constitutes a component of an entity? (T4-8) 1. A component is any part of the company, such as an operating segment or subsidiary, that includes operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the company. 2. A component or group of components that has been sold or disposed of in some other way, or is considered held for sale is reported as a discontinued operation if the disposal represents a strategic shift that has, or will have, a major effect on a company’s operations and financial results. C. Reporting discontinued operations,

4-2 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. 1. When the component has been sold, the income effects of a discontinued operation inc ludes (1) the operating income or loss of the component from the beginning of the repo rting period to the disposal date, and (2) the gain or loss on disposal. (T4-9) 2. When the component is considered held for sale, the income effects of a discontinued operation includes (1) operating income or loss of the component from the beginning o f the reporting period to the end of the reporting period, and (2) an impairment loss if t he book value, sometimes called carrying value or carrying amount, of the assets of th e component is more than fair value minus cost to sell. (T4-10) 3. The assets and liabilities of a component considered held for sale are reported separate ly in the balance sheet at the lower of their book value or fair value minus cost to sell.

IV. Accounting Changes A. Accounting changes fall into one of three categories: (1) a change in an accounting princip le, (2) a change in estimate, or (3) a change in reporting entity. B. Most voluntary changes in accounting principles are accounted for retrospectively by revis ing prior years’ financial statements. (T4-11) 1. The comparative financial statements are revised. 2. The appropriate accounts are adjusted. 3. A disclosure note provides clear justification that the change is appropriate. The note a lso indicates the effects of the change on items not reported on the face of the primary statements, as well as any per share amounts affected for the current period and all prio r periods presented. C. A change in depreciation, amortization, or depletion method is considered to be a change i n accounting estimate that is achieved by a change in accounting principle. These changes are accounted for prospectively, exactly as we would account for any other change in esti mate. D. A change in accounting estimate is reflected in the financial statements of the current perio d and future periods. (T4-12)

V. Correction of Accounting Errors A. Errors discovered in the same year they are made are simply corrected by journal entry. B. Treatment of errors discovered in a year subsequent to the year the error is made depends on whether the error is material. 1. If the error is not material, it is simply corrected in the year discovered. 2. If the error is material, the correction is considered a prior period adjustment which req uires an addition to or reduction in beginning retained earnings and a restatement of pr evious years' financial statements.

VI. Earnings per Share Disclosures A. Earnings per share (EPS) is the amount of income reported during a period for each share of common stock outstanding. B. All corporations whose common stock is publicly traded must disclose EPS. C. The EPS for (a) income from continuing operations, (b) discontinued operations, and (3) n et income, must be disclosed. (T4-13)

VII.Comprehensive Income

Instructors Resource Manual 4-3 Copyright © 2015 McGraw-Hill Education. All rights reserved. A. The purpose of the income statement is to summarize the profit-generating activities that o ccurred during a particular reporting period. B. Comprehensive income is the total change in equity for a reporting period other than from transactions with owners. C. The information in the income statement and other comprehensive income items can be pr esented either (1) in a single, continuous statement of comprehensive income or (2) in two separate, but consecutive statements, an income statement and a statement of comprehensi ve income. (T4-14) D. Both U.S. GAAP and IFRS allow companies to report comprehensive income in either a si ngle statement of comprehensive income or in two separate statements. (T4-15)

Part B: The Statement of Cash Flows

I. Usefulness of the Statement of Cash Flows A. The purpose of the statement of cash flows (SCF) is to provide information about cash rec eipts and cash disbursements that occurred during a period. B. A SCF is presented for each period in which results of operations are provided.

II. Classifying Cash Flows A. The SCF classifies all transactions affecting cash into one of three categories: (T4-16) 1. Operating activities are inflows and outflows of cash related to the transactions enterin g into the determination of net operating income. (T4-17) a. The Direct Method b. The Indirect Method 2. Investing activities involve the acquisition and sale of (1) long-term assets used in the business and (2) nonoperating investment assets. 3. Financing activities involve cash inflows and outflows from transactions with creditors (excluding trade creditors) and owners. B. Significant investing and financing transactions not involving cash also are reported. C. The classification of certain cash flows differs between U.S. GAAP and international acco unting standards. (T4-18)

Appendix4: Interim Reporting A. Interim reports are issued for periods of less than a year, typically as quarterly financial sta tements. B. With only a few exceptions, the same accounting principles applicable to annual reporting are used for interim reporting. C. Complete financial statements are not required for interim reporting, but certain minimum disclosures are required: 1. Sales, income taxes, and net income. 2 Earnings per share. 3 Seasonal revenues, costs, and expenses. 4. Significant changes in estimates for income taxes. 5. Discontinued operations and unusual items.

4-4 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. 6. Contingencies. 7. Changes in accounting principles or estimates. 8. Significant changes in financial position.

PowerPoint Slides A PowerPoint presentation of the chapter is available in the Connect library.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or y ou can first modify them to suit your particular needs or preferences. In addition, a ll illustrations in the chapter are separately available in the Connect library.

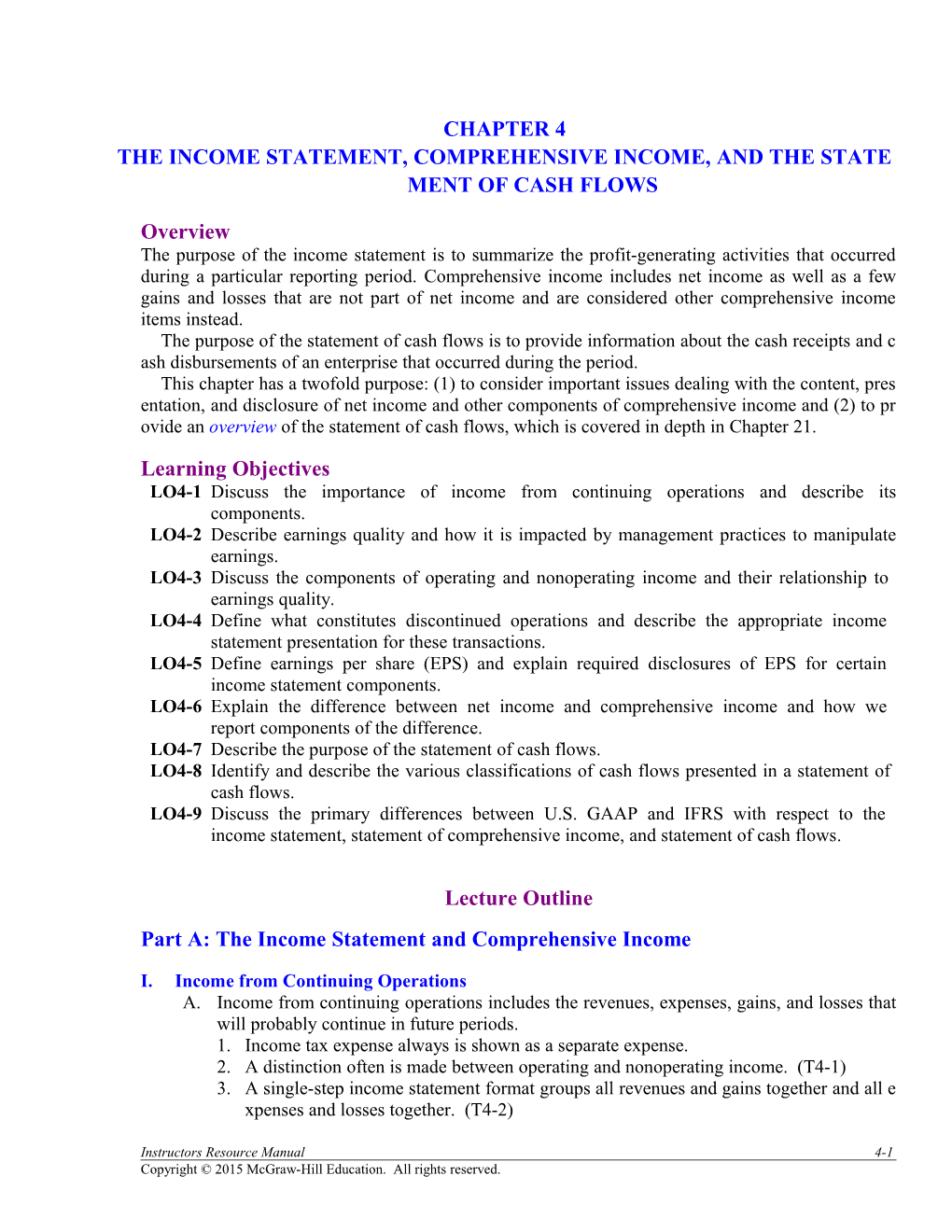

INCOME STATEMENTS — . Consolidated Statements of Income (In thousands, except per share data) Fiscal Year Ended January 31 2014 2013 2012 Net salesURBAN OUTFITTERS$3,086,608 IN$2,794,925 $2,473,801 Cost of sales 1,925,266 1,763,394 1,613,265 Gross profit C. 1,161,342 1,031,531 860,536 Selling, general and administrative expenses 734,511 657,246 575,811 Operating income 426,831 374,285 284,725 Interest income 2,713 2,126 5,120 Other income 1,088 862 553 Other expenses (3,114) (1,701) (1,567) Income before income taxes 427,518 375,572 288,831 Income tax expense 145,158 138,258 103,580 Net income $ 282,360 $ 237,314 $ 185,251

Earnings per common share: Basic $1 .92 $1 .63 $1 .20 Diluted $1 .89 $1 .62 $1 .19

Illustration 4-2

Instructors Resource Manual 4-5 Copyright © 2015 McGraw-Hill Education. All rights reserved. T4-1 SINGLE-STEP INCOME STATEMEN An adv T ant age of the single-step format is its simplicity.

MAXWELL GEAR CORPORATION Income Statement For the Year Ended December 31, 2016 Revenues and gains: Sales ...... $573,522 Interest and dividends ...... 26,400 Gain on sale of investments ...... 5,500 Total revenues and gains ...... 605,422 Expenses and losses: Cost of goods sold ...... $302,371 Selling ...... 47,341 General and administrative ...... 24,888 Research and development ...... 16,300 Interest ...... 14,522 Total expenses and losses ...... 405,422 Income before income taxes ...... 200,000 Income tax expense ...... 80,000 Net income ...... $120,000

Illustration 4-3

4-6 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. T4-2

Instructors Resource Manual 4-7 Copyright © 2015 McGraw-Hill Education. All rights reserved. MULTIPLE-STEP INCOME STATEMENT An advantage of the multiple-step format is that it separately r eports operating and nonoperating activities.

MAXWELL GEAR CORPORATION Income Statement For the Year Ended December 31, 2016 Sales revenue ...... $573,522 Cost of goods sold ...... 302,371 Gross profit ...... 271,151 Operating expenses: Selling ...... $47,341 General and administrative ...... 24,888 Research and development ...... 16,300 Total operating expenses ...... 88,529 Operating income ...... 182,622 Other income (expense): Interest and dividend revenue ...... 26,400 Gain on sale of investments...... 5,500 Interest expense ...... (14,522) Total other income, net ...... 17,378 Income before income taxes ...... 200,000 Income tax expense ...... 80,000 Net income ...... $120,000

Illustration 4-4

T4-3

4-8 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. INTERNATIONAL FINANCIAL REPORTING STANDARDS

Income Statement Presentation. There are more similarities than differ ences between income statements prepared according to U.S. GAAP and t hose prepared applying international standards. Some of the differences a re:

International standards require certain minimum information to be r eported on the face of the income statement. U.S. GAAP has no mini mum requirements.

International standards allow expenses to be classified either by f unction (e.g., cost of goods sold, general and administrative, etc), or b y natural description (e.g., salaries, rent, etc.). SEC regulations requir e that expenses be classified by function.

In the U.S., the “bottom line” of the income statement usually is c alled either net income or net loss. The descriptive term for the botto m line of the income statement prepared according to international sta ndards is either profit or loss.

T4-4

Instructors Resource Manual 4-9 Copyright © 2015 McGraw-Hill Education. All rights reserved. OPERATING INCOME AND EARNINGS QUALITY

Operating income could include some unusual items that may or may not continue in the future.

Income Statements – GameStop Corp.

Income Statements (in part) ($ in millions) Year Ended February 1, February 2, 2014 2013 Net sales $9,039.5 $8,886.7 Cost of sales 6,378 .4 6,235 .2 Gross profit 2,661.1 2,651.5 Selling, general and administrative expenses 1,892.4 1,835.9 Depreciation and amortization 166.5 176.5 Goodwill impairments 10.2 627.0 Asset impairments and restructuring costs 18 .5 53 .7 Operating income (loss) 573 .5 (41 .6)

Illustration 4-5

T4-5

4-10 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. NONOPERATING INCOME AND EARNINGS QUALITY

Some nonoperating items have generated considerable discuss ion with respect to earnings quality, notably gains and losses f rom the sale of investments.

Income Statements – Intel Corporation

Income Statements (in part) Years Ended December 30 (in millions) 2000 1999 Operating income 10,395 9,767 Gains on investments, net 3,759 883 Interest and other, net 987 578 Income before taxes 15,141 11,228

Illustration 4-6

T4-6

Instructors Resource Manual 4-11 Copyright © 2015 McGraw-Hill Education. All rights reserved. DISCONTINUED OPERATIONS

► Discontinued operations must be reported separately, below income from continuing operations.

Income from continuing operations before income taxes XXX Income tax expense XX Income from continuing operations XXX Discontinued operations, net of $xx tax (expense)/benefit XX Net income $XXX

The income tax effect of discontinued operations is included in the separate presentation rather than as part of the amount reported as i ncome tax expense. This is referred to as intraperiod tax allocati on.

T4-7

4-12 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. DISCONTINUED OPERATION

► A component is any part of the company, such as an operating segment or subsidiary, that includes operations and cash flows that can be clearly distinguished, operationally and for financi al reporting purposes, from the rest of the company. ► A component or group of components that has been sold or di sposed of in some other way, or is considered held for sale is r eported as a discontinued operation if the disposal represents a strategic shift that has, or will have, a major effect on a com pany’s operations and financial results.

T4-8

Instructors Resource Manual 4-13 Copyright © 2015 McGraw-Hill Education. All rights reserved. DISCONTINUED OPERATIONS — When the component has been sold

When the component has been sold, the income effects of a di scontinued operation includes: 1. Operating income or loss (revenues, expenses, gains and losses) of the component from the beginning of the reporting period to t he disposal date. 2. Gain or loss on disposal.

The Duluth Holding Company has several operating divisions. In October 2016, management dec ided to sell one of its divisions that qualifies as a separate component according to generally accep ted accounting principles. The division was sold on December 18, 2016 for a net selling price of $ 14,000,000. On that date, the assets of the division had a book value of $12,000,000. For the peri od January 1 through disposal, the division reported a pre-tax loss from operations of $4,200,000. The company’s income tax rate is 40% on all items of income or loss. Duluth generated after-tax p rofits of $22,350,000 from its continuing operations.

Duluth’s income statement for the year 2016, beginning with income from continuing operation s, would be reported as follows:

Income from continuing operations $22,350,000 Discontinued operations: Loss from operations of discontinued component (including gain on disposal of $2,000,000*) $(2,200,000) † Income tax benefit 880,000 ‡ Loss on discontinued operations (1,320,000) Net income $21,030,000

* Net selling price of $14 million less book value of $12 million † Loss from operations of $4.2 million less gain on disposal of $2 million ‡ $2,200,000 x 40%

Illustration 4-7 T4-9

4-14 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. DISCONTINUED OPERATIONS — When the component is considered held for sale

When the component is considered held for sale, the income e ffects of a discontinued operation includes: 1. Operating income or loss (revenues, expenses, gains and losses) of the component from the beginning of the reporting period to t he end of the reporting period. 2. An “impairment loss” if the book value, sometimes called carryi ng value or carrying amount, of the assets of the component is more than fair value minus cost to sell.

The Duluth Holding Company has several operating divisions. In October of 2016, management d ecided to sell one of its divisions that qualifies as a separate component according to generally acc epted accounting principles. On December 31, 2016, the end of the company’s fiscal year, the divi sion had not yet been sold. On that date, the assets of the division had a book value of $12,000,00 0 and a fair value, minus anticipated costs to sell, of $9,000,000. For the year, the division reporte d a pre-tax loss from operations of $4,200,000. The company’s income tax rate is 40% on all item s of income or loss. Duluth generated after-tax profits of $22,350,000 from its continuing operatio ns. Duluth’s income statement for 2016, beginning with income from continuing operations, would be reported as follows: Income from continuing operations $22,350,000 Discontinued operations: Loss from operations of discontinued component (including impairment loss of $3,000,000*) $(7,200,000) † Income tax benefit 2,880,000 ‡ Loss on discontinued operations (4,320,000) Net income $18,030,000 * Book value of $12 million less fair value net of cost to sell of $9 million † Operating loss of $4.2 million plus impairment loss of $3 million ‡ $7,200,000 x 40%

Illustration 4-8 T4-10

Instructors Resource Manual 4-15 Copyright © 2015 McGraw-Hill Education. All rights reserved. CHANGE IN ACCOUNTING PRINCIPLE ► Most voluntary changes in accounting principles are accounte d for retrospectively by revising prior years’ financial stateme nts. ► The steps used to account for changes are as follows: 1. The comparative financial statements are revised. 2. The appropriate accounts are adjusted. 3. A disclosure note provides clear justification for the chan ge along with the effects of the change on items not repo rted on the face of the primary statements, as well as any per share amounts affected for the current period and all prior periods presented. ► A change in depreciation, amortization, or depletion method i s considered to be a change in accounting estimate that is achi eved by a change in accounting principle. We account for the se changes prospectively, exactly as we would any other chan ge in estimate.

T4-11

4-16 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. CHANGE IN ACCOUNTING ESTIMATE

► A change in accounting estimate is reflected in the financial st atements of the current period and future periods.

T4-12

Instructors Resource Manual 4-17 Copyright © 2015 McGraw-Hill Education. All rights reserved. EARNINGS PER SHARE Earnings per share (EPS) is the amount of income reported ex pressed on a per share basis. In its simplest form, EPS is computed by dividing income availab le to common shareholders (net income less any preferred stock d ividends) by the weighted-average number of common shares out standing. All corporations whose common stock is publicly traded must dis close EPS. The EPS for (a) income from continuing operations, (b) discontin ued operations, and (3) net income, must be disclosed.

T4-13

4-18 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. EARNINGS PER SHARE (continued)

BIG LOTS, INC. Consolidated Statements of Operations (in part)

Thirteen Weeks Ended (In thousands, except per share amounts) May 3, 2014 May 4, 2013 Income from continuing operations $28,581 $37,065 Loss from discontinued operations, net of tax (25,233) (4,732) Net income $ 3,348 $32,333

Earnings per common share – basic: Continuing operations $0.50 $0.65 Discontinued operations (0 .44) (0 .08) Net income $0 .06 $0 .57

Earnings per common share – diluted: Continuing operations $0.50 $0.64 Discontinued operations (0 .44) (0 .08) Net income $0 .06 $0 .56

Illustration 4-10

T4-13 (continued)

Instructors Resource Manual 4-19 Copyright © 2015 McGraw-Hill Education. All rights reserved. COMPREHENSIVE INCOME

► Comprehensive income is the total nonowner change in equity for a period.

($ in millions) Net income $xxx Other comprehensive income: Net unrealized holding gains (losses) from investments (net of tax)* $xx Gains (losses) from and amendments to postretirement benefits plans (net of tax)† (x) Deferred gains (losses) from derivatives (net of tax) ‡ (x) Gains (losses) from foreign currency translation (net of tax) § x xx Comprehensive income $xxx

* Changes in the market value of certain investments (described in Chapter 12). † Gains and losses due to revising assumptions or market returns differing from expectations and prior service cost from amending the plan (described in Chapter 17). ‡ When a derivative designated as a cash flow hedge is adjusted to fair value, the gain or loss is deferred as a component of comprehensive income and included in earnings later, at the same time as earnings are affected by the hedged transaction (described in the Derivatives Appendix to the text). § Gains or losses from changes in foreign currency exchange rates. The amount could be an addition to or reduction in shareholders’ equity. (This item is discussed elsewhere in your accounting curriculum.)

Illustration 4-11 The information in the income statement and other comprehen sive income items can be presented either (1) in a single, cont inuous statement of comprehensive income or (2) in two separ ate, but consecutive statements, an income statement and a sta tement of comprehensive income. T4-14

4-20 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. INTERNATIONAL FINANCIAL REPORTING STANDARDS

Comprehensive Income. Both U.S. GAAP and IFRS allow companies to report comprehensive income in either a single statement of comprehensive income or in two separate statements. Other comprehensive income items are similar under the two sets of standards. However, an additional OCI item, changes in revaluation surplus, is possible under IFRS. In Chapter 11 you will learn that IAS No. 16 permits companies to value property, plant, and equipment at (1) cost less accumulated depreciation or (2) fair value (revaluation). IAS No. 38 provides a similar option for the valuation of intangible assets. U.S. GAAP prohibits revaluation. If the revaluation option is chosen and fair value is higher than book value, the difference, changes in revaluation surplus, is reported as other comprehensive income and then accumulates in a revaluation surplus account in equity.

T4-15

Instructors Resource Manual 4-21 Copyright © 2015 McGraw-Hill Education. All rights reserved. STATEMENT OF CASH FLOWS

► OPERATING ACTIVITIES Inflows and outflows of cash that result from activities repor ted in the income statement. Includes most of the elements of net income, but reported o n a cash basis rather than an accrual basis.

► INVESTING ACTIVITIES Inflows and outflows of cash related to the acquisition and d isposition of long-term assets (such as property, plant and e quipment, and intangible assets) and investment assets (exce pt those classified as cash equivalents and trading securities). The purchase and sale of inventories are not considered inve sting activities.

► FINANCING ACTIVITIES Cash inflows and outflows from transactions with creditors (excluding trade creditors) and owners.

T4-16 CASH FLOWS FROM OPERATIONS ACTIVITIES

4-22 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. Under the direct method, the cash effect of each operating ac tivity is reported directly in the statement. By the indirect method, we arrive at net cash flow from oper ating activities indirectly by starting with reported net income and working backwards to convert that amount to a cash basis

T 4-17

Instructors Resource Manual 4-23 Copyright © 2015 McGraw-Hill Education. All rights reserved. CASH FLOWS FROM OPERATIONS ACTIVITIES (continued)

Arlington Lawn Care (ALC) began operations at the beginning of 2016. ALC’s 2016 income statement and its year-end balance sheet are shown below ($ in thousands).

ARLINGTON LAWN CARE Income Statement For the Year Ended December 31, 2016

Service revenue $90 Operating expenses: General and administrative $32* Depreciation 8 Total operating expenses 40 Income before income taxes 50 Income tax expense 15 Net income $35

* Includes $6 in insurance expense.

ARLINGTON LAWN CARE Balance Sheet At December 31, 2016

Assets Liabilities and shareholders’ equity Current assets: Current liabilities: Cash $54 Accounts payable** $ 7 Accounts receivable 12 Income taxes payable 15 Prepaid insurance 4 Total current liabilities 22 Total current assets 70 Shareholders’ equity: Equipment 40 Common stock 50 Less: Accumulated depreciation (8) Retained earnings 30*** Total assets $102 Total liabilities and shareholders’ equity $102

** For general and administrative expenses *** Net income of $35 less $5 in cash dividends paid

Illustration 4-14 T4-17 (continued)

4-24 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved. CASH FLOWS FROM OPERATIONS ACTIVITIES (continued) ARLINGTON LAWN CARE Statement of Cash Flows For the Year Ended December 31, 2016 ($ in thousands) Cash Flows from Operating Activities Cash received from customers* $78 Cash paid for general and administrative expenses** (29) Net cash flows from operating activities $49

* Service revenue of $90 thousand, less increase of $12 thousand in accounts receivable. **General and administrative expenses of $32 thousand, less increase of $7 thousand in accounts payable, plus increase of $4 thousand in prepaid insurance.

Illustration 4-14A

ARLINGTON LAWN CARE Statement of Cash Flows For the Year Ended December 31, 2016 ($ in thousands) Cash Flows from Operating Activities Net income $35 Adjustments for noncash effects: Depreciation expense $ 8 Changes in operating assets and liabilities: Increase in prepaid insurance (4) Increase in accounts receivable (12) Increase in accounts payable 7 Increase in income taxes payable 15 14 Net cash flows from operating activities $49

Illustration 4-14B

T4-17 (continued)

Instructors Resource Manual 4-25 Copyright © 2015 McGraw-Hill Education. All rights reserved. INTERNATIONAL FINANCIAL REPORTING STANDARDS

Classification of Cash Flows. Like U.S. GAAP, international standards also require a statem ent of cash flows. Consistent with U.S. GAAP, cash flows are classified as operating, investi ng, or financing. However, the U.S. standard designates cash outflows for interest payments and cash inflows from interest and dividends received as operating cash flows. Dividends pai d to shareholders are classified as financing cash flows. IAS No. 7, on the other hand, allows more flexibility. Companies can report interest and dividends paid as either operating or financing cash flows and interest and dividends received as either operating or investing cash flows. Interest and dividend payments usually are report ed as financing activities. Interest and dividends received normally are classified as investing activities.

Typical Classification of Cash Flows from Interest and Dividends

U.S. GAAP IFRS Operating Activities Operating Activities Dividends received Interest received Interest paid Investing Activities Investing Activities Dividends received Interest received

Financing Activities Financing Activities Dividends paid Dividends paid Interest paid Siemens AG, a German company, prepares its financial statements according to IFRS. In its stateme nt of cash flows for the first three months of the 2014 fiscal year, the company reported interest and divi dends received as operating cash flows, as would a U.S. company. However, Siemens classified interest paid as a financing cash flow.

Siemens AG Statement of Cash Flows (partial) For the First Three Months of Fiscal 2014 (€ in millions) Cash flows from financing activities: Transactions with owners (6) Repayment of long-term debt (5) Change in short-term debt and other financing activities 1,138 Interest paid (78) Dividends paid (4) Financing discontinued operations (107) Cash flows from financing activities-continuing operations 938

T 4-18

4-26 Intermediate Accounting, 8/e Copyright © 2015 McGraw-Hill Education. All rights reserved.