OFFICE SUITE

TO LET

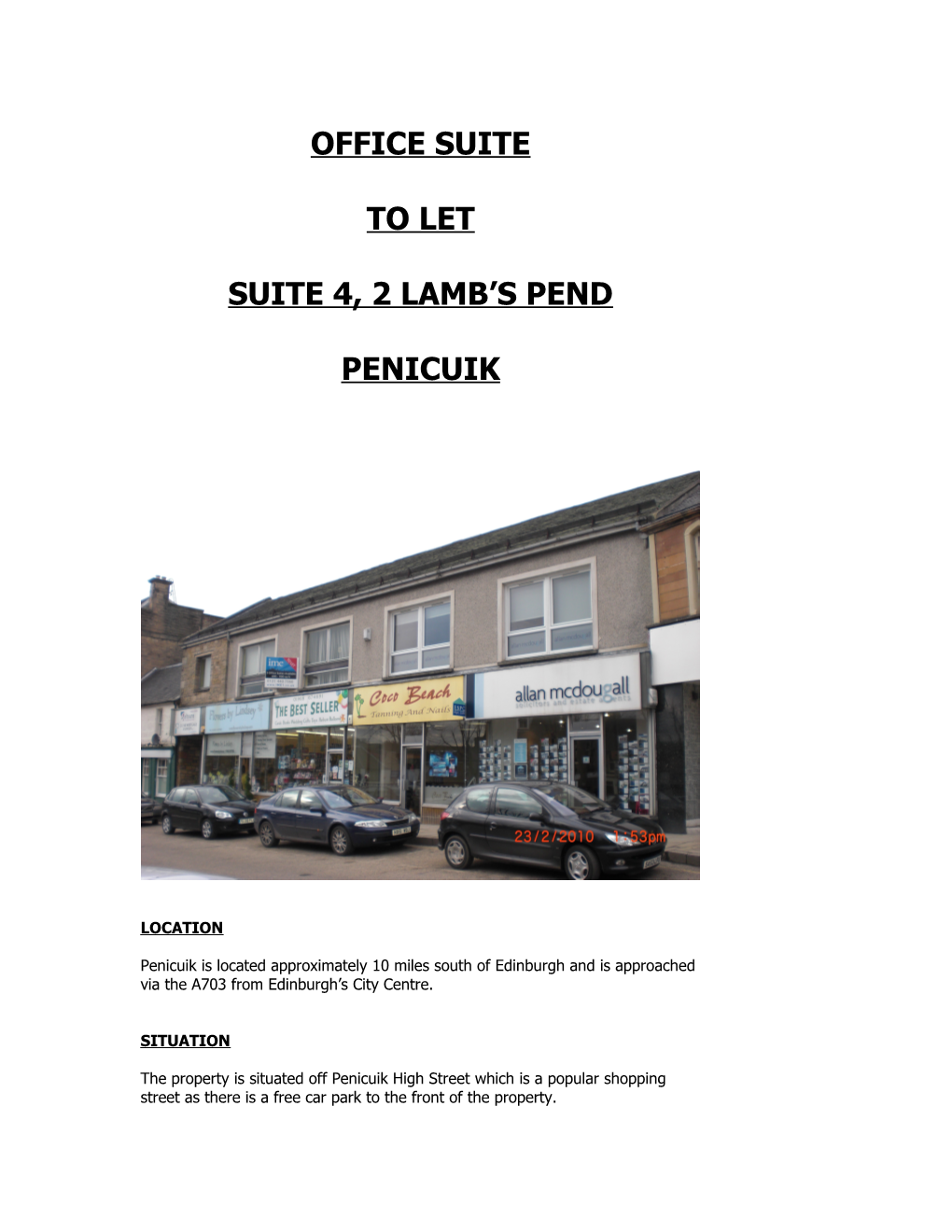

SUITE 4, 2 LAMB’S PEND

PENICUIK

LOCATION

Penicuik is located approximately 10 miles south of Edinburgh and is approached via the A703 from Edinburgh’s City Centre.

SITUATION

The property is situated off Penicuik High Street which is a popular shopping street as there is a free car park to the front of the property. DESCRIPTION

The property comprises first floor office suites being part of a 2 storey brick retail and office development. There are communal ladies and gents toilets together with a security system and fire alarm system. We calculate that the net internal floor area for the accommodation is as follows

Suite 4 34.9 sq.m. (367 sq.ft.)

The Suite benefits from night storage heating, suspended ceilings and fluorescent lighting.

RATEABLE VALUE

We have been informed by Lothian Regional Council that the property has been entered in the current valuation roll for 2010 as follows:-

RV

Suite 4 £2,200

LEASE TERMS

Our clients are seeking rental offers as follows:-

Suite 4 £2,500 per annum

Letting will be on the basis of a minimum 3 year full repairing and insuring lease.

The tenant will be responsible for payment of rates and the proportion of the common charges together with legal costs in connection with the lease.

VIEWING

Viewing arrangements by appointment with the sole letting agent:-

G2 Property Consultants, South Craighall Lodge, Jackton Road, Jackton, GLASGOW, G75 8RR.

Tel: 01355 301392

E-mail: [email protected] Property Misdescriptions Act 1991

1. The information contained within these particulars has been checked and, unless otherwise stated, is understood to be materially correct at the date of publication. After these details have been printed circumstances may change outwith our control. When we are advised of any changes we will endeavour to inform all enquirers at the earliest opportunity.

2. Date of publication: 20/12/11

3. Unless otherwise stated, all prices and rents are quoted exclusive of Value Added Tax. Prospective purchasers/lessees must satisfy themselves independently as to the incidence of VAT in respect of any transaction.

4. These particulars are not warranted and should not be taken to form part of any contract.