From PLI’s Course Handbook Acquiring or Selling the Privately Held Company 2009 #18988

5

ACQUIRING OR SELLING THE PRIVATELY HELD COMPANY--2009

Theodore B. Polk Citi Capital Strategies

© 2009 Citigroup Global Markets Inc.

1 Biographical Summary

Theodore (Ted) B. Polk Managing Director, Head of the Central Region

Mr. Polk has worked in the financial services industry for over 20 years and has been a Managing Director at Citi Capital Strategies since 1998. He has successfully managed strategic sale assignments and recapitalizations in a variety of industries and is a frequent public speaker on the topic of business exits, sales and recapitalizations of private and family-owned businesses.

Mr. Polk has completed transactions with prominent corporate buyers including, among others, The Boeing Company, General Dynamics, Illinois Tool Works, 3M, Akzo Nobel BV, and Cobham plc. He has also structured transactions involving leading private equity firms, such as TA Associates, Summit Partners, and The Riverside Company. In 2008, a transaction managed by Mr. Polk was recognized by The M&A Advisor as the Cross- Border Middle-Market Deal of the Year (below $100 million). This transaction was singled out for its excellence in dealmaking, and its demonstration of creativity and ingenuity, as well as adding value.

Prior to joining Citi Capital Strategies in 1994, Mr. Polk was employed by Valuemetrics, Inc., where he valued closely held businesses for legal- and tax- related requirements and, in particular, helped install Employee Stock Ownership Plans (ESOPs). He also worked at The Bank of New York in its Corporate Banking Group. Mr. Polk received his B.S.B.A. degree from Georgetown University and M.B.A. from The University of Chicago. He is a Chartered Financial Analyst (CFA) and is a member of The CFA Institute and The CFA Society of Chicago. Mr. Polk is a Series 7 and 63 Registered Securities Representative and a Series 24 Registered Securities Principal.

2 The views expressed herein are those of the author and do not necessarily reflect the views of Citigroup Global Markets Inc. or its affiliates. All opinions are subject to change without notice. Neither the information provided nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Past performance is no guarantee of future results.

This article references a sampling of transactions in which Citi Capital Strategies represented the sellers or other participants they are not indicative of future performance or success.

Citigroup Inc. and its affiliates do not provide tax or legal advice. To the extent that this material or any attachment concerns tax matters, it is not intended to be used and cannot be used by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Any such taxpayer should seek advice based on the taxpayer's particular circumstances from an independent tax advisor.

©2009 Citigroup Global Markets Inc. Member SIPC. Citi Capital Strategies is a division of Citigroup Global Markets Inc. Citi and Citi with Arc Design are trademarks and service marks of Citigroup Inc. and its affiliates, and are used and registered throughout the world.

3 The Current Market Environment

“The more things change, the more they are the same.” Jean Baptiste Alfonse Karr (1808-1890)

Borrowing from the wisdom expressed by this French editor and satirist, I think the best way to assess where the Mergers & Acquisitions (M&A) market is heading in 2009 is to first understand where things have recently been. Time has shown us that key M&A trends and the underlying drivers behind M&A activity are slow to change, making what we witnessed in 2008 a good prelude to what we should expect to experience this year. While several trends in 2008 did change course on us, these trends only changed for the negative and transactional volumes likewise declined too. As a result, there is now a slowdown in new deals entering into the market.

The slowdown in M&A activity was first evident with the largest and highest profile transactions. Earlier in 2008, higher profile, premium-priced strategic transactions, such as the acquisition of William Wrigley Jr. Company by Mars Inc., were completed as were several high profile distressed sale situations involving the financial services industry, such as the acquisition of Bear Stearns by JP Morgan Chase, and later the acquisition of Merrill Lynch by Bank of America and the acquisition of Wachovia Bank by Wells Fargo. More recent activity was also notable in the announced sale of the Chicago Cubs baseball team to the Ricketts family. In short, M&A activity has occurred and is occurring for many different reasons and in many different types of situations, but overall activity slowed in 2008 and that trend is continuing into 2009.

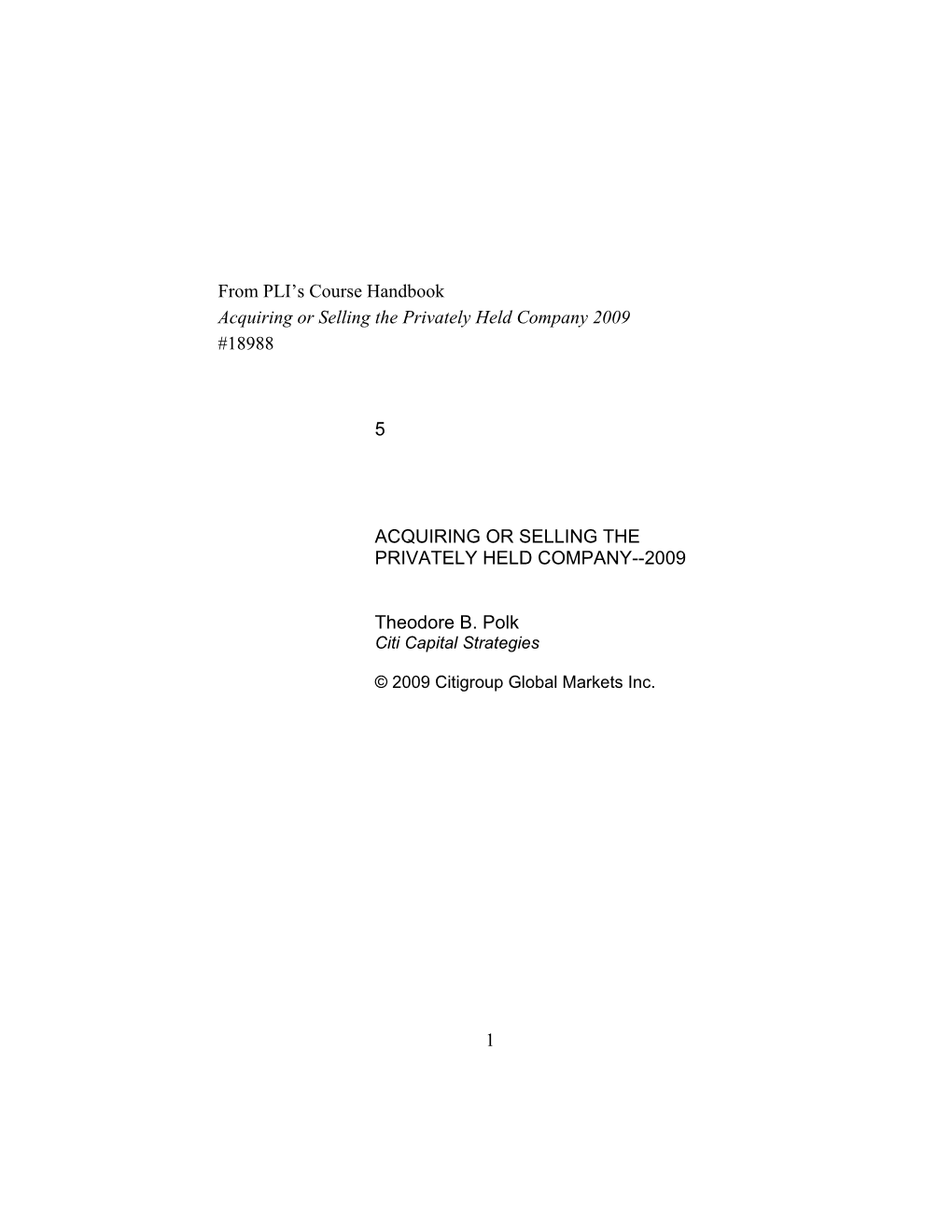

4 In varying degrees, the key drivers of a vibrant M&A market existed in 2008

M&A Activity

12,000

s 10,000 l a e D

d

e 8,000 c n u o n

n 6,000 A

f o

r e

b 4,000 m u N

2,000

0 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08

Source: 2008 Mergerstat Review; FactSet Mergerstat LLC database, 01/05/2009

but generally they weakened over the course of the year. They include the availability of the capital needed to finance transactions, a level of visibility regarding the expected near term performance of both target companies and their acquirers and a belief on the part of acquirers that the expected value created by acquiring assets exceeds the price paid for them. As evidenced in the above chart, the key transaction drivers must have existed to a greater degree in prior years, particularly for the larger deals, as the market was not able to hold-up.

While many issues helped to cause the fall-off in deal volumes, the primary culprit is the global credit crisis that began in 2007 and generally got worse throughout 2008. A reduction in the availability of leverage first limits the ability of buyers to be opportunistic and then forces them to be judicious in their use of third-party capital for any purpose other than to protect their core operations. For borrowers seeking to fund transactions, the impact of the credit crunch is twofold; it leads to a decrease in the availability of debt capital relative to the cash flows of target operations and to an increase in borrowing rates. These factors make deals more expensive to complete for buyers needing external funding and are now resulting in either greater equity contributions from investors, lower purchase prices, some combination of both or more likely, an inability to complete a transaction.

5 Average Equity Contribution to Leveraged Buyouts s e

c 45% r u

o 40% % S

l % 6 % . % a 6

t 35% % 0 2 . 5 . o . % 8 0 4 % . 0 T 9 7

% 30% 4 1 % f . 7 4 % 3 . % 3 o 9 5 3

1 . % 5 7 . . . 3

e 25% 3 0 3 2 2 . g 1 3 3 a 3 0 3

t 20% % 3 n 9 e .

c 15% 2 r e 2

P 10%

s

a 5%

y t i 0% u q

E 96 97 98 99 00 01 02 03 04 05 06 07 08

Source: Standard and Poor’s Leveraged Lending Review 4Q08, January 2009

With respect to privately held companies, the same trends and value drivers apply to the acquisition or sale of these often smaller businesses as apply to the headliners. However, there are noteworthy differences between public and private market activity. First, the smaller transactions, which are generally those involving privately held businesses, are less reliant on the availability of third-party capital because of their size. Second, one must keep in mind that with privately held companies, the owners are often the managers and thus sell decisions can be made on more factors than just the ‘pure’ numbers. While the former factor enables more M&A activity to occur involving smaller privately held concerns, the latter factor is the trump card and a significant amount of transactional activity involving privately held concerns will quickly stall once pricing metrics begin to deteriorate.

As previously noted, as a result of a lower reliance on debt capital to fund transactions, M&A activity involving privately held businesses seemed to hold-up longer in 2008 than was the case with the bigger deals 1, but, it has slowed over time along with deterioration of the credit markets and the overall economy. No doubt, many sellers will opt to not sell rather than accept a transaction that became harder to finance and consequently was priced lower than desired.

1 Murphy Carolyn, “Piper Jaffray: Middle-market M&A to hold its own in 2008,” The Deal.com, February 17, 2008. 6 Middle-Market* M&A Activity

3,000 s l a e

D 2,500

d e c

n 2,000 u o n

n 1,500 A

f o

r 1,000 e b m

u 500 N

0 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08

Source: FactSet Mergerstat LLC database, 02/26/2009 *Middle Market includes all deals valued from $1 million to $250 million

In our experience, 2008 also turned out to be a year that favored the strategic acquirer. Earlier in the year, with a weaker dollar, we noticed increased strategic interest coming from abroad, particularly from acquirers in Europe. As the currency differentials neutralized later in the year and the decline of the economy picked-up pace and spread globally, the dominant M&A players for us became those strategic buyers that were well capitalized, seasoned in the practice of acquisitions and were primarily domiciled in the United States.

As this piece was being written in February, deals are still getting done, but most are requiring extra effort to complete. While we remain hopeful that several other closings will soon occur, it is clear to us that the market environment has changed. The slowdown in deal activity that began in 2008 with the bigger transactions is continuing into 2009 and now is affecting all deals, regardless of size.

How does the M&A market change when the economy slows?

Inevitably, when credit tightens and concern grows over the outlook for the economy, the criteria used by sellers to assess offers changes. While in a bullish M&A market valuation is almost exclusively considered, in a slower market sellers more heavily assess the financial wherewithal of the buyer and the buyer’s proven willingness to complete a transaction not only in a timely manner, but also without changes in proposed terms. In our case, well known acquirers such as Berkshire Hathaway and Illinois Tool Works acquired client 7 companies which we advised over the past few months and succeeded in buying businesses at fair prices by being able to execute in a professional manner as promised. These deals were completed because the buyers took advantage of their superior access to capital and welcomed the opportunity to buy well-run operations at a time when others were struggling to do so.

When the visibility of the future business outlook declines, as is presently the case, the urgency for most parties to either sell or buy declines too. In the case of the buyer, we have found that many, unlike ITW or Berkshire Hathaway, are prone to seek a greater ‘incentive’ to complete transactions during this period and thus are quicker to lower valuations in down-markets than are the owners of privately held concerns. As for sellers, again we find that most owners do not view their ownership in such businesses as just another investment. The opportunity to have your family’s name on the business, to pay you and your family members at rates you determine, to lease real estate you own for use by the company, and so on, often makes the hold alternative just too attractive to consider accepting a sale price that is lower than desired. These differing perspectives help ensure that there will be fewer ‘meetings of the minds’ when it comes to valuation and also helps explain why there are fewer sales of privately held concerns in down-markets.

Keep in mind that absent bankruptcy sales or sales being forced by creditors, all completed transactions by definition require an exchange of consideration between a ready and willing buyer and a ready and willing seller. In fact, fair market value is defined as just that – the cash or cash-equivalent price at which property would exchange hands between a willing buyer and a willing seller, both being adequately informed of the facts, and neither being compelled to buy or sell2. And, if the perspectives of the transacting parties do not overlap with respect to valuation, we will not be able to establish fair market value and we will simply witness fewer transactions getting completed.

In light of the current market environment, what types of owners are most likely to sell today?

The most likely sellers today are those that can best take advantage of the M&A market or those that have decided, for whatever reason, that they will be better off with more liquidity today. They include:

2 Pratt, Shannon A., “Valuing a Business – The Analysis and Appraisal of Closely Held Companies,” page 22-23. 8 The owner of a ‘bulletproof’ business. Regardless of the state of the economy, there always seems to be another Google Inc. out there that has figured out how to do something a little bit different or a little bit better than its competitors and is an extremely attractive acquisition target for a wide range of acquirers. While businesses like this are few and far between, they do exist and, given the inevitable breadth of interest in acquiring them, they will command premium valuations at all points of an economic cycle.

The owner of a counter cyclical operation. As awkward as it may sound, let’s face it – the problems encountered by parties operating in one sector of the economy may well create opportunities for those operating elsewhere. As an example, in 2008 only two companies listed as components of the Dow Jones Industrial Average posted increases in their stock price. Those companies were McDonald’s Corporation and Wal-Mart Stores, both of which are known for their price-competitive product offerings and both of which become more valuable when consumers are tightly managing their money. These businesses are weathering the economic storms better than most as could businesses operating in areas such as healthcare, consumer staples, credit services and even repossessions. Just because the overall economy is under-performing, it certainly does not mean that every business is performing poorly too and it may mean that certain sectors of the economy may be better suited for M&A activity in a down-market than in a growing one.

Those seeking to secure liquidity. For some sellers, while the current market is not great, it may well be good enough. In situations involving businesses that have had strong growth to date, but may need help growing to the next level or those that, for whatever reason, do not seem able to dramatically improve their position over the near term, maybe a sale today is the best alternative. This could include businesses which are underperforming, those whose owners or executives have health issues, those with owners that no longer have interest in staying involved with operations or even those that fear future changes in tax policy and would like to take advantage of today’s favorable capital gains rates.

It does not include everybody. Outperforming businesses, burned out owners, or those with owners needing to sell represent just a small portion of the universe of privately held enterprises. Again, in our experience the prototypical business owner is a value optimizer at

9 heart and in the absence of bull market pricing that allows for premium valuations, many business owners will gladly sit on the sidelines and not sell. And, if you have fewer sellers, you have fewer transactions.

How do deals get done in today’s markets?

One of our favorite investment maxims is that ‘cash is king.’ In the context of M&A, that means that those who have money in-hand today are infinitely more valuable as buyers than those parties whose offers come with a financing contingency. It also means that since investment capital is scarcer today than is typically the case, there can be draconian differences in the valuations of highflying businesses compared to those of more modest performers. These factors change the normal dynamics for both buyers and sellers, both in terms of targeting buyers as well as structuring the transactions.

Talk to the groups with money. In 2005, 50% of our deals were completed with strategic acquirers. In 2008, this figure increased to 70% and this trend is likely to continue over the near term. If you want the highest certainty of closing, there is no better place to look than here.

Presently, companies in the S&P 500 report $2.67 trillion in cash on their Balance Sheets, figures that are up 19% from a year ago. 3 While this does not mean that all these funds are available for acquisitions, it does give sell-side advisors good direction as to whom they should be first contacting on behalf of their clients today.

Be precise in your dealings with Private Equity Groups (PEGs). As for the private equity community, many funds are flush with cash and those with committed funding are under pressure to make investments. However, the typical PEG relies heavily on leverage (debt financing) to generate the high internal rates of return sought by investors in this asset class. With a desire to deploy capital but a limited ability to procure significant leverage to fund transactions, many PEGs are presently in a bind. Inevitably, those seeking to complete transactions with PEGs today will find interested parties, but parties that are more likely to offer lower prices and/or require more creative transaction structures than

3 Flashwire Weekly, “U.S. Market Report,” February 17, 2009, page 2.

10 were common over the past few years. Our recommendation is to very closely assess the financing plans supporting PEG acquisition proposals today and to obtain a thorough understanding of and comfort with any financing contingencies before going too deep into the final stages of a sale. Those that do not do so may get unwelcome surprises just before closing. Over the past few years, PEGs have grown accustomed to being able to generate decent returns simply by de- leveraging the businesses they purchased and now that credit is tight, they will be forced to generate returns in other ways, with a lower price often being the ‘lowest hanging fruit’ for them.

Focus on those situations where it will be easiest to obtain financing on the target business. Keep in mind that those target businesses that are asset-heavy will be easier to finance that those that are asset-light, businesses with a diversified customer base will be easier to finance than those with customer concentrations, those with a contracted backlog of business will be easier to finance than those without, and those businesses that have historically had consistent performance will be easier to finance than those whose operations have been more volatile. No doubt, transactional activity today will favor those situations that are easiest to finance.

Bridge valuation gaps using more creative transaction structures. The transaction we most recently completed involved the sale of a closely held business to two private equity groups and the pivotal element that made the transaction acceptable to both parties was a twenty five percent ownership interest in the go-forward business that was retained by the sellers. It gave the sellers the opportunity to participate in the future success of the business and lowered the cash outlay required of the buyers at the time of the transaction closing. While the need for a creative financing solution that was just noted involved PEG buyers, the need for creative financing could also be required by strategic acquirers too. That is, while the limited availability of debt capital particularly hurts the typical approach to transaction structuring that is employed by Private Equity Groups, both PEGS and strategic acquirers alike may also be impacted by a lack of visibility related to target company operations. To the extent required, buyers may seek to include earn-outs or other forms of consideration that are more contingent in nature to offset the risk that newly acquired businesses under perform following a sale.

11 Conventionally, the form of consideration most likely to be used in a market with limited available credit is seller financing. This occurs when the seller steps in to bridge the financing of any gaps that may exist between the debt available to the buyer relative to the desired purchase price and the seller receives payment of the principal portion of these loans over time.

For sellers, agreeing to the use of seller financing can be double-edged. On the positive side, its use may result in a valuation that is higher relative to the other alternatives that currently exist and tax recognition on the portion of the sale price tied to the loan is tax deferred until principal payments are received. Further, interest is earned on the pre- tax face value of the loans which increases the amount of interest that is earned. On the other hand, sellers receive less capital up-front relative to an all-cash sale and carry continued risk associated with the future success of the sold business.

Agree on a lower price. If parties are interested in selling their privately held business and the best opportunities are those with lower prices than desired, obviously the only way deals will be completed is by acceptance of one of the lower offers.

To this point, statistics indicate that declines in market pricing have been occurring for some time. According to FactSet Mergerstat LLC, a firm that tracks middle-market sized deals, the average buyout multiples of transactions dropped from the 7.5x EBITDA range in 2007 to 7.0x EBITDA in 20084, a level not seen since our last recession in 2002. Our research also indicates a significant decrease in the use of debt leverage on deals. As was noted in a prior chart using Standard and Poor’s data, the average equity contribution to leveraged buyouts increased from 32.9% in 2007 to 42.6% in 2008. And, according to GF Data Resources, a firm that tracks middle market acquisitions involving private equity groups, total debt used in middle market sized deals decreased from 3.4x adjusted EBITDA in the first half of 2008 to 2.4x in the fourth quarter of 2008.5

4 FactSet Mergerstat database involving private U.S. targets and announced transactions with enterprise values of $1mm to $500mm, 1/05/2009. 5 “The resilient middle market delivers again: Deal volume and valuations held steady in Q4,” GF Data Resources, February 19, 2009 12 AverageAverage Enterprise Enterprise Value/EBITDA Value/EBITDA 10 9.1 9.0 9 8.2 8.1 7.9 8.1 7.5 8 7.0 7.0 7

s 6 e 5 m i

T 4 3 2 1 0 2000 2001 2002 2003 2004 2005 2006 2007 2008

Source: FactSet Mergerstat LLC database, 01/05/2009 Includes private U.S. targets; announced transactions with Enterprise Values of $1 million to $500 million. Considered ratios from 0 to 25.

What sectors will likely be the most vibrant?

The sectors of the M&A market for privately held businesses that we expect to be the most vibrant in 2009 will come from two distinct camps; they will include those industries that offer the greatest predictability for near term performance and have at least decent growth prospects, and industries that have had cataclysmic downturns and require rapid consolidation.

Some of the stronger industry sectors where M&A activity should continue include:

Healthcare industry. The growth drivers for many sectors of healthcare are not closely correlated with those of the overall economy and can make such markets more stable and predictable than most others. In fact, demographic trends and government policies are more critically important to discerning demand than is the expected growth in GDP. For these reasons, including the Obama Administration’s interest in expanding health care coverage to include more Americans, the expectation is that healthcare M&A activity should remain resilient in 2009. However, it should be noted that some of the changes in the new Administration’s budget have caused fears of industry price controls, a situation that has yet to play out. From an M&A perspective, the sector benefits from its large size as well as from the numerous niches that exist within it. The different niches keep it fragmented and thus a great source of M&A activity involving privately held businesses. Within the healthcare

13 industry, much of the M&A activity is likely to come from higher growth sectors like healthcare IT products and services or from pharmaceutical or biotech activity. Notably, the healthcare IT field is also expected to benefit from the government’s recently announced spending initiatives.

Technology industry. The technology sector, year-in and year-out, is a vibrant source of M&A transactions involving privately held concerns. In general, this is because of the higher rates of growth associated with the sector which makes it an attractive place for investment. It is also because tech businesses often find it easier to ‘buy rather to than to build’ when seeking to expand given the more rapid pace of change in these markets and the preference to invest in proven rather than untested technologies. Further, it is also an active area for M&A activity because the industry is more fragmented than most, with plenty of privately held concerns that can represent attractive takeover targets. A notable subcategory of the tech sector, which should be more vibrant than most, involves businesses that provide services to the government. The particular attractiveness of government IT providers is that their businesses are more predictable than most and their customer base (i.e. the government) is unquestioned in its demand for products and services. In addition to government IT providers, the “clean tech” segment may see particular strength, as the U.S., and the rest of the world, continues to put a premium on initiatives that contribute to the health of the environment.

In contrast to these defensible industries, the present challenges in several market sectors may also act as catalysts for M&A activity. Likely areas include:

Auto industry. This sector is presently experiencing unprecedented contraction. Significant levels of excess capacity exist throughout the globe and assets may well need to be divested in order to provide needed liquidity to OEMs or as part of a forced sale. This may well also occur with parts suppliers in these markets too. It is in this latter category where privately held M&A activity will occur.

Financial Services industry. The level of M&A activity that occurred in the financial services industry during 2008 was extraordinary. As it is unclear when credit market conditions will cease to deteriorate, the potential for more forced consolidation remains, and it could just as easily affect privately held institutions as it could the big institutions.

14 What are the key drivers behind a market turnaround?

As is often the case, we will know the market is turning after it has done so. This will, no doubt, coincide with more stable capital markets and a more vibrant economy.

Along the way, we first will likely see some temporary and minor spikes that may help pave the way for a resumption of more normal M&A activity. They include:

Opportunistic acquiring. Weaker economies make certain acquirers very active. In addition to parties like Illinois Tool Works and Berkshire Hathaway that we previously mentioned as actively acquiring businesses recently, we believe there are many large corporations that are prepared to ‘seize the moment.’ Among others, 3M recently publicly announced that it is prepared to step up acquisitions in the current environment and acquire several competitors that are now a little weaker. 3M also noted that it is prepared to use its cash reserves or its own stock to complete transactions.

Selling before Uncle Sam increases his take. All indications are that the Obama Administration intends to proceed with plans to increase the capital gains rate from 15% to 20%. At the time of this writing, it looks like the new tax rates are being targeted for 2010 and beyond. As a rational seller will be more concerned with their after-tax proceeds as opposed to their pretax proceeds, 2009 may be the right time to sell for many. As the chart below indicates, the current capital gains rates are at historic lows, and our instinctive guess is that they may not return to these levels for many years to come.

15 Capital Gains Tax Rate s l a

u 35% d i v i

d 30% n I

r o

f 25%

e t a 20% R

s n i

a 15% G

l a

t 10% i p a

C 5%

l a r

e 0% d e

F 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 8 8 8 8 8 8 8 8 9 9 9 9 9 9 9 9 9 9 0 0 0 0 0 0 0 0 0

Source: Tax Foundation, Special Report No. 148, November 2006 (latest change)

The Federal Stimulus package may give us a boost. The American Recovery and Reinvestment Act of 2009 is making $787 billion available to help revive the United States economy. Parties looking to take advantage of funding might seek to make acquisitions in areas of the economy, such as the infrastructure market, which are expected to directly benefit.

As for the turnaround itself, an increased willingness to lend is likely to result from the stabilization of lending portfolios and improved economic conditions. And, an increased willingness to borrow should result from increased visibility and confidence in the near term outlook. Here are some items to watch that may indicate these factors are occurring and that the downturn in M&A activity will be ending:

Financial institutions cease to have large write-downs of their assets. Once their asset base stops shrinking from write-downs, the equity cushion of financial institutions should stop contracting too and logically this will alleviate one of the constraints preventing banks from actively seeking to add new loans to their books.

Emerging markets resume their growth. Given the significant portion of global manufacturing that has been outsourced to emerging market partners in places like China or India, a growth

16 in their output could be a strong indicator of increases in global demand and a resumption of more normal global trading activity.

Watch the leading economic indicators. A pick-up in economic activity is often evident in increased business for players in the transportation industry, among others. Increased trucking, rail, ship and air freight activity, as well as increased logistics activities for shipments could all serve as an early radar system for us on a pick-up in economic activity. Watch the stock market as its pricing is based on expected future performance. The stock market in some ways is also a leading economic indicator. It is a more speculative measure, as it just reflects the consensus views of investors regarding future economic activity, but it is important as it also captures the level of confidence expressed by the investing public in the economy. When it starts to again increase, we should soon also see increases in consumer and corporate spending and both should help support the overall economic recovery.

In closing, while it is safe to say that these times are not reflective of a “normal adjustment,” but rather something much bigger, it is also worth noting that M&A activity has suffered to one degree or another during every period of a slow or declining economy in the past 30 years. We continue to expect that when the economy and the market improve, M&A activity will likely rebound as well. In fact, looking back 30 years, M&A activity has always bounced back very strong, usually setting new activity records within 1-2 years of the end of the contraction.6

6 2008 Mergerstat Review; Factset Mergerstat LLC database, 01/05/2009; Department of Commerce, Bureau of Economic Analysis

17