N

o

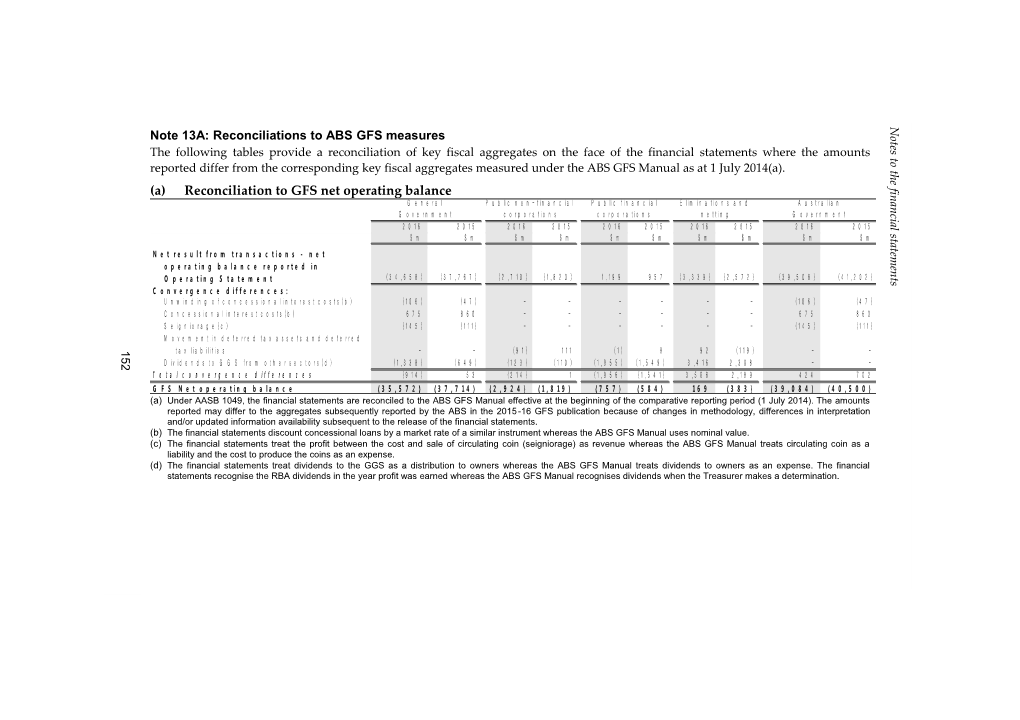

Note 13A: Reconciliations to ABS GFS measures t

e

s

The following tables provide a reconciliation of key fiscal aggregates on the face of the financial statements where the amounts t

o

t

reported differ from the corresponding key fiscal aggregates measured under the ABS GFS Manual as at 1 July 2014(a). h

e

f

i (a) Reconciliation to GFS net operating balance n

a

G e n e r a l P u b l i c n o n - f i n a n c i a l P u b l i c f i n a n c i a l E l i m i n a t i o n s a n d A u s t r a l i a n n

G o v e r n m e n t c o r p o r a t i o n s c o r p o r a t i o n s n e t t i n g G o v e r n m e n t c

i

a

2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 l

s

$ m $ m $ m $ m $ m $ m $ m $ m $ m $ m t

a

t

e

N e t r e s u l t f r o m t r a n s a c t i o n s - n e t m

e

o p e r a t i n g b a l a n c e r e p o r t e d i n n

( 3 4 , 6 5 8 ) ( 3 7 , 7 6 7 ) ( 2 , 7 1 0 ) ( 1 , 8 2 0 ) 1 , 1 9 9 9 5 7 ( 3 , 3 3 9 ) ( 2 , 5 7 2 ) ( 3 9 , 5 0 8 ) ( 4 1 , 2 0 2 ) t O p e r a t i n g S t a t e m e n t s C o n v e r g e n c e d i f f e r e n c e s : U n w i n d i n g o f c o n c e s s i o n a l i n t e r e s t c o s t s ( b ) ( 1 0 6 ) ( 4 7 ) ------( 1 0 6 ) ( 4 7 ) C o n c e s s i o n a l i n t e r e s t c o s t s ( b ) 6 7 5 8 6 0 ------6 7 5 8 6 0 S e i g n i o r a g e ( c ) ( 1 4 5 ) ( 1 1 1 ) ------( 1 4 5 ) ( 1 1 1 ) M o v e m e n t i n d e f e r r e d t a x a s s e t s a n d d e f e r r e d

1 t a x l i a b i l i t i e s - - ( 9 1 ) 1 1 1 ( 1 ) 8 9 2 ( 1 1 9 ) - -

5

2 D i v i d e n d s t o G G S f r o m o t h e r s e c t o r s ( d ) ( 1 , 3 3 8 ) ( 6 4 9 ) ( 1 2 3 ) ( 1 1 0 ) ( 1 , 9 5 5 ) ( 1 , 5 4 9 ) 3 , 4 1 6 2 , 3 0 8 - - T o t a l c o n v e r g e n c e d i f f e r e n c e s ( 9 1 4 ) 5 3 ( 2 1 4 ) 1 ( 1 , 9 5 6 ) ( 1 , 5 4 1 ) 3 , 5 0 8 2 , 1 8 9 4 2 4 7 0 2 G F S N e t o p e r a t i n g b a l a n c e ( 3 5 , 5 7 2 ) ( 3 7 , 7 1 4 ) ( 2 , 9 2 4 ) ( 1 , 8 1 9 ) ( 7 5 7 ) ( 5 8 4 ) 1 6 9 ( 3 8 3 ) ( 3 9 , 0 8 4 ) ( 4 0 , 5 0 0 ) (a) Under AASB 1049, the financial statements are reconciled to the ABS GFS Manual effective at the beginning of the comparative reporting period (1 July 2014). The amounts reported may differ to the aggregates subsequently reported by the ABS in the 2015-16 GFS publication because of changes in methodology, differences in interpretation and/or updated information availability subsequent to the release of the financial statements. (b) The financial statements discount concessional loans by a market rate of a similar instrument whereas the ABS GFS Manual uses nominal value. (c) The financial statements treat the profit between the cost and sale of circulating coin (seigniorage) as revenue whereas the ABS GFS Manual treats circulating coin as a liability and the cost to produce the coins as an expense. (d) The financial statements treat dividends to the GGS as a distribution to owners whereas the ABS GFS Manual treats dividends to owners as an expense. The financial statements recognise the RBA dividends in the year profit was earned whereas the ABS GFS Manual recognises dividends when the Treasurer makes a determination. N

(b) Reconciliation to GFS total change in net worth o

t

G e n e r a l P u b l i c n o n - f i n a n c i a l P u b l i c f i n a n c i a l E l i m i n a t i o n s a n d A u s t r a l i a n e

s

G o v e r n m e n t c o r p o r a t i o n s c o r p o r a t i o n s n e t t i n g G o v e r n m e n t t

o

2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 t

h

$ m $ m $ m $ m $ m $ m $ m $ m $ m $ m e

f

i T o t a l c h a n g e i n n e t w o r t h b e f o r e n

a t r a n s a c t i o n s w i t h o w n e r s i n t h e i r n

c

i

c a p a c i t y a s o w n e r s a s r e p o r t e d i n a

l

( 1 1 4 , 6 8 0 ) ( 3 8 , 4 2 4 ) ( 2 , 8 0 4 ) ( 1 , 6 7 8 ) 3 , 2 7 0 6 , 1 5 3 ( 4 8 1 ) ( 1 , 7 6 8 ) ( 1 1 4 , 6 9 5 ) ( 3 5 , 7 1 7 ) O p e r a t i n g S t a t e m e n t s

t C o n v e r g e n c e d i f f e r e n c e s : a

t

e

R e l a t i n g t o n e t o p e r a t i n g b a l a n c e ( 9 1 4 ) 5 3 ( 2 1 4 ) 1 ( 1 , 9 5 6 ) ( 1 , 5 4 1 ) 3 , 5 0 8 2 , 1 8 9 4 2 4 7 0 2 m

R e l a t i n g t o c h a n g e i n t r e a t m e n t o f e

n

t

d e f e n c e w e a p o n s a n d i n v e n t o r y ( a ) - 4 3 , 7 6 0 ------4 3 , 7 6 0 s R e l a t i n g t o o t h e r e c o n o m i c f l o w s 1 , 2 6 3 6 5 8 ( 4 , 0 1 7 ) ( 3 , 0 3 0 ) 1 , 9 7 9 ( 2 , 6 1 4 ) 7 1 5 2 , 2 8 8 ( 6 0 ) ( 2 , 6 9 8 ) R e l a t i n g t o t r a n s a c t i o n s w i t h o w n e r s - - 7 , 0 3 5 4 , 7 0 7 ( 3 , 2 9 3 ) ( 1 , 9 9 8 ) ( 3 , 7 4 2 ) ( 2 , 7 0 9 ) - - T o t a l c o n v e r g e n c e d i f f e r e n c e s 3 4 9 4 4 , 4 7 1 2 , 8 0 4 1 , 6 7 8 ( 3 , 2 7 0 ) ( 6 , 1 5 3 ) 4 8 1 1 , 7 6 8 3 6 4 4 1 , 7 6 4 G F S T o t a l c h a n g e i n n e t w o r t h ( 1 1 4 , 3 3 1 ) 6 , 0 4 7 ------( 1 1 4 , 3 3 1 ) 6 , 0 4 7 (a) Consistent with AASB 1049, the Australian Government elected not to apply Chapter 2 Amendments to Defence Weapons Platforms of the ABS publication

1

5 Amendments to Australian System of Government Finance Statistics: Concepts, Sources and Methods, 2005 (ABS Catalogue No. 5514.0.55.001) — published on 4 the ABS website on 5 April 2011 — until the 2014-15 reporting period. The 2013-14 period was prepared on the previous basis and impacts the 2014-15 comparative. (c) Reconciliation to GFS net lending / (borrowing) G e n e r a l P u b l i c n o n - f i n a n c i a l P u b l i c f i n a n c i a l E l i m i n a t i o n s a n d A u s t r a l i a n G o v e r n m e n t c o r p o r a t i o n s c o r p o r a t i o n s n e t t i n g G o v e r n m e n t 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 $ m $ m $ m $ m $ m $ m $ m $ m $ m $ m N e t l e n d i n g / ( b o r r o w i n g ) a s r e p o r t e d i n O p e r a t i n g S t a t e m e n t ( 3 7 , 5 0 8 ) ( 4 0 , 4 7 3 ) ( 7 , 3 9 9 ) ( 4 , 7 4 9 ) 1 , 1 3 0 9 7 4 ( 3 , 5 3 4 ) ( 2 , 5 5 9 ) ( 4 7 , 3 1 1 ) ( 4 6 , 8 0 7 ) C o n v e r g e n c e d i f f e r e n c e s : R e l a t i n g t o n e t o p e r a t i n g b a l a n c e ( 9 1 4 ) 5 3 ( 2 1 4 ) 1 ( 1 , 9 5 6 ) ( 1 , 5 4 1 ) 3 , 5 0 8 2 , 1 8 9 4 2 4 7 0 2 A u c t i o n s a l e s o f s p e c t r u m ( a ) - ( 1 , 9 6 5 ) ------( 1 , 9 6 5 ) T o t a l c o n v e r g e n c e d i f f e r e n c e s ( 9 1 4 ) ( 1 , 9 1 2 ) ( 2 1 4 ) 1 ( 1 , 9 5 6 ) ( 1 , 5 4 1 ) 3 , 5 0 8 2 , 1 8 9 4 2 4 ( 1 , 2 6 3 ) G F S N e t l e n d i n g / ( b o r r o w i n g ) ( 3 8 , 4 2 2 ) ( 4 2 , 3 8 5 ) ( 7 , 6 1 3 ) ( 4 , 7 4 8 ) ( 8 2 6 ) ( 5 6 7 ) ( 2 6 ) ( 3 7 0 ) ( 4 6 , 8 8 7 ) ( 4 8 , 0 7 0 ) (a) The financial statements recognise the disposal of spectrum licences at the point of issue whereas the ABS GFS Manual recognises spectrum licences at the time of auction and the proceeds from their sale at the point of auction, reflected on the balance sheet as a receivable.

1

5

5

N

o

t

e

s

t

o

t

h

e

f

i

n

a

n

c

i

a

l

s

t

a

t

e

m

e

n

t

s N

(d) Reconciliation to GFS net worth o

t G e n e r a l P u b l i c n o n - f i n a n c i a l P u b l i c f i n a n c i a l E l i m i n a t i o n s a n d A u s t r a l i a n e

s

G o v e r n m e n t c o r p o r a t i o n s c o r p o r a t i o n s n e t t i n g G o v e r n m e n t t

o

2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 2 0 1 6 2 0 1 5 t

h

$ m $ m $ m $ m $ m $ m $ m $ m $ m $ m e

f

i ( 4 1 3 , 5 1 4 ) ( 2 9 9 , 3 0 2 ) 1 9 , 8 9 0 1 5 , 6 3 9 2 4 , 7 8 2 2 4 , 8 0 2 ( 4 5 , 1 8 4 ) ( 4 0 , 9 5 5 ) ( 4 1 4 , 0 2 6 ) ( 2 9 9 , 8 1 6 ) n N e t w o r t h a s r e p o r t e d i n B a l a n c e S h e e t a

n

C o n v e r g e n c e d i f f e r e n c e s : c

i

P r o v i s i o n f o r d o u b t f u l d e b t s ( a ) 2 8 , 3 7 4 2 5 , 0 7 6 1 8 1 5 1 1 ( 1 ) - 2 8 , 3 9 2 2 5 , 0 9 2 a

l

C o n c e s s i o n a l i t y o n l o a n s a n d i n v e s t m e n t s ( b ) 7 , 1 5 0 9 , 4 3 5 ------7 , 1 5 0 9 , 4 3 5 s

t I n v e s t m e n t i n o t h e r s e c t o r e n t i t i e s ( c ) ( 1 , 0 0 7 ) ( 7 0 7 ) - - - - 1 , 0 0 7 7 0 7 - - a

t

e

D e f e r r e d t a x a s s e t s ( d ) - - ( 8 2 0 ) ( 9 0 9 ) ( 5 ) ( 4 ) 8 2 5 9 1 3 - - m

S e i g n i o r a g e ( e ) ( 4 , 0 0 6 ) ( 3 , 8 6 1 ) ------( 4 , 0 0 6 ) ( 3 , 8 6 1 ) e

n

D e f e r r e d t a x l i a b i l i t y ( d ) - - 4 6 8 6 4 8 - - ( 4 6 8 ) ( 6 4 8 ) - - t

s D i v i d e n d s ( f ) ( 1 , 3 3 8 ) ( 6 4 9 ) - - 1 , 3 3 8 6 4 9 - - - - S h a r e s a n d o t h e r c o n t r i b u t e d c a p i t a l ( g ) - - ( 1 9 , 5 5 6 ) ( 1 5 , 3 9 3 ) ( 2 6 , 1 1 6 ) ( 2 5 , 4 4 8 ) 4 3 , 8 2 1 3 9 , 9 8 3 ( 1 , 8 5 1 ) ( 8 5 8 ) T o t a l c o n v e r g e n c e d i f f e r e n c e s 2 9 , 1 7 3 2 9 , 2 9 3 ( 1 9 , 8 9 0 ) ( 1 5 , 6 3 9 ) ( 2 4 , 7 8 2 ) ( 2 4 , 8 0 2 ) 4 5 , 1 8 4 4 0 , 9 5 5 2 9 , 6 8 5 2 9 , 8 0 7 G F S N e t w o r t h # # # # # # # # # # # # # # ------( 3 8 4 , 3 4 1 ) ( 2 7 0 , 0 0 9 ) (a) The financial statements treat provisions for doubtful debts as an offset to the asset in the balance sheet. The ABS GFS Manual does not consider the creation of a 1 provision to be an economic event and therefore excludes it from the balance sheet.

5

4 (b) The financial statements discount concessional loans by a market rate of a similar instrument whereas the ABS GFS manual uses nominal value. (c) The financial statements apply AASB 13 to the valuation of the GGS’s investment in public corporations whereas the ABS GFS Manual values public corporations at their net assets unless the shares in a public corporation are publicly traded. A convergence difference arises where the application of AASB 13 results in a valuation other than net assets. (d) Deferred tax assets and deferred tax liabilities are reported in the financial statements whereas the ABS GFS Manual does not recognise these items. (e) The financial statements treat the profit between the cost and sale of circulating coin (seigniorage) as revenue whereas the ABS GFS Manual treats circulating coin as a liability and the cost to produce the coins as an expense. (f) The financial statements recognise the RBA dividends in the year profit was earned whereas the ABS GFS Manual recognises dividends when the Treasurer makes a determination. (g) The financial statements treat shares and other contributed capital in public corporations as part of net worth whereas the ABS GFS Manual deducts shares and other contributed capital in the calculation of net worth (with net worth calculated as assets less liabilities less shares and other contributed equity). Notes to the financial statements

The ABS GFS Manual measures inventory at market value (rather than the lower of cost and net realisable value). It also does not recognise the provision for decommissioning/restoration costs. The above reconciliation has not been adjusted for these items on the basis of materiality and information availability.

Reconciliation to GFS cash surplus/(deficit) is disclosed on the face of the cash flow statement.

Note 13B: Reconciliation to original budget The following tables provide a comparison of the original 2015-16 Budget to the final actual results for the GGS. Explanations are provided for major variances, which are typically those amounts greater than $1 billion.

The Australian Government does not present budgets at the whole of government level, and therefore, only the GGS is presented in this note. The Budget is not audited.

N

o

t

e

s

t

o

t

h

e

f

i

n

a

n

c

i

a

l

s

t

a

t

e

m

e

n

t

s

156