STATEMENT OF CURRENT MONTHLY INCOME – FORM B22 i Angela M. Scolforo, Trustee Staff Attorney, and H. David Cox, Esquire December 1, 2007

I. Median Income a. Line 16: Median Income Figures for Virginia as of 10/15/2007 i. One: $44,780 ii. Two: $59,423 (only figure to increase) iii. Three: $67,788 iv. Four: $78,413 v. Five or more: add $6,900 for each additional person II. Allowable Living Expenses a. Line 24: National Standards as of 10/15/2007 – using income and family size to set standard deduction: These amounts already include school lunches, meals at home or away, recreation and entertainment. (and per UST) i. One: $621 IF income $3,334-$4,66 per month $703 IF income $4,167-$5,833 per month $916 IF income $5,823 and over per month ii. Two: $825 IF income $3,334-$4,66 per month $904 IF income $4,167-$5,833 per month $1,306 IF income $5,823 and over per month iii. Three: $937 IF income $3,334-$4,66 per month $1,017 IF income $4,167-$5,833 per month $1,368 IF income $5,823 and over per month iv. Four: $1,063 IF income $3,334-$4,66 per month $1,203 IF income $4,167-$5,833 per month $1,546 IF income $5,823 and over per month v. Extra Taken for Each Person Over 4: 1. $193 IF $3,334-$4,66 per month 2. $204 IF income $4,167-$5,833 3. $216 IF income $5,823 and over

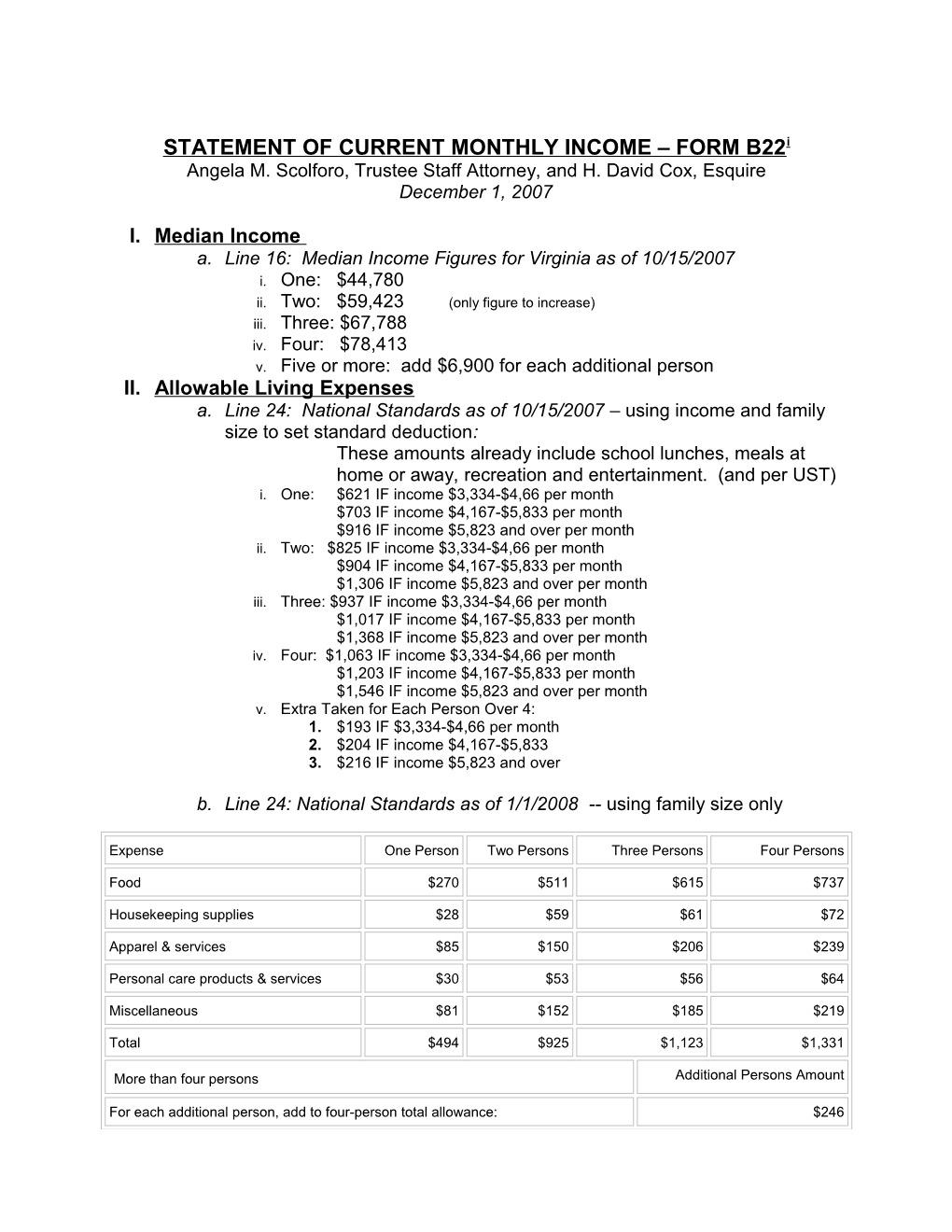

b. Line 24: National Standards as of 1/1/2008 -- using family size only

Expense One Person Two Persons Three Persons Four Persons

Food $270 $511 $615 $737

Housekeeping supplies $28 $59 $61 $72

Apparel & services $85 $150 $206 $239

Personal care products & services $30 $53 $56 $64

Miscellaneous $81 $152 $185 $219

Total $494 $925 $1,123 $1,331

More than four persons Additional Persons Amount

For each additional person, add to four-person total allowance: $246 III. Local Housing and Utilities a. Effective 10/15/2007 - See Exhibit 1 attached hereto i. Line 25A: first column of the chart based upon family size and county ii. Line 25B: second column of the chart based upon family size and county – deduct the mortgage payment, as also shown on Line 47 b. Effective 1/1/2008 -- See Exhibit 2 attached hereto –

IV. Transportation Deductions a. Line 27: Operating Expenses i. Vehicle Operating Expense as of 10/15/2007 1. No Car: $203 2. One Car: $260 3. Two Cars: $343 4. Culpeper: ($299, $350, $433) ii. Vehicle Operating Expense as of 1/01/2008 1. No Car: $163 2. One Car: $181 3. Two Cars: $362 4. Culpeper: ($208, $416) b. Lines 28 and 29: Ownership Expenses i. Vehicle Ownership Expense as of 10/15/2007 1. First Car: $471 2. Second Car: $332 ii. Vehicle Ownership Expense as of 1/01/2008 1. One Car: $478 2. Two Cars: $956 (show ½ this amount on Line 28 and ½ on Line 29)

V. Deductible Expenses –reasonable and necessary for health and welfare and production of income of debtors and their dependents a. Line 30: Taxes – actual tax expense owed over prior 6 months – 1/12th of the prior year tax refunds received by debtors must be deducted from amounts withheld on the pay advices so this amount shows actual tax obligation – b. Line 32: Life Insurance – can only take life insurance deduction for term life insurance on the debtors’ life, not the whole life portion of policy payment (and per UST) c. Line 33: Child Support Expense Deduction – deduct for court-ordered payments only -- do not include the arrearage amount because it comes out on Line 49, so make sure you determine what portion, if any, of the ordered support payment is for an arrearage – agreed to amounts for which there is no order may be taken on Line 57 d. Line 35: Childcare Expense: actual expense for daycare, babysitting, or preschool which amount must be documented with statement from the caregiver e. Line 36: Health Care Expense - this is the actual amount expended and must be documented and justified carefully

2 i. Do not include health insurance or health savings plan amounts here – use Line 39. ii. effective 1/1/2008 there will be a standard deduction of $54 per person under 65 years old and $144 per person 65 years old or older f. Line 37: Telecommunications Services – this amount should approximate the deduction on J for necessary “cell phones, pagers, special long distance, internet” - not a deduction for regular phone service, whether that is a land or cell phone, because it is already included in Line 25. g. Line 39 : Health and Disability Insurance -- health and disability insurance deduction for actual cost, probably same amount on Schedule J (and per UST) h. Line 42: Home Energy Costs – amount by which your actual cost exceeds the IRS standards – must document this additional expense and the justification for it -- there is no cap on this expense (and per UST) i. Line 43 : Deduction for Education Expense – this does NOT include preschool or college expenses – this may include private or home schooling expenses – i. maximum deduction is $125 per child pursuant to Code §707(b)(2) (A)(ii)(IV) (and per UST) ii. See, In re Cleary, 357 B.R. 369 (Bankr. S.C. 2006)(allowing private school expense in light of family’s sacrifice of other basic expenses to fund private school tuition and strongly held religious convictions) j. Line 44 : Additional Food & Clothing Costs – amount by which your actual cost exceeds the IRS standards – must document this additional expense and the justification for it (i.e. – special dietary or medical needs) – there is a 5% cap on this additional expense pursuant to Code §707(b)(2)(A)(ii)(I) (and per UST) k. Line 45 : Charitable Expense Deduction – limited to 15% of gross income – you should expect to demonstrate level of gifting in current and one (1) prior year to support current expense l. Lines 47 and 48: Deduction for Secured Debt Payments – i. Pro rate the contractual payments over 60 months ii. If debt payments exceed 60 months, use the monthly payments iii. If interest rate is adjustable – use the rate on the filing date iv. If loan balloons within 60 months, include 1/60th of the entire v. Leased vehicle payments may not be deducted here vi. Arrearage: Deduct 1/60th of the secured debt arrearage amounts to be paid in the Plan – NOT on luxury items -- only on “primary residence, motor vehicle, or other property necessary for the support of the debtor and the debtor’s dependents” pursuant to 707(b)(2)(A)(iii)(II) (and per UST) vii. Surrendered Collateral: you cannot take any deduction for payments on property which will be surrendered See, In re Ball, 06-70154 (Bankr. W.D. VA 5/17/2006) viii. Crammed Down Collateral: if you are valuing the collateral in the Plan, you must deduct 1/60th of the total amount being paid on the secured portion of the claim in the Plan, and not the contractual 3 amount owed on the filing date See, In re McPherson, 06-60243 (Bankr. W.D. VA 2006) ix. Good Faith: the Code still contains a good faith analysis - “the unsecured creditors are better off than they would be if the asset is excluded and the monthly payments on the secured debt are added into a monthly plan payment.” In re Hylton, 07-70320, page 12 fn 8 (Bankr. W.D. VA 8/22/07) m. Line 49: Priority Debts -- deduction for 1/60th of priority tax, alimony and child support payments in the Plan – be careful not to duplicate the arrearage amounts which may be in court-ordered support payments on Line 33. n. Line 50 : Trustee Commission – this should reflect the Trustee’s commission on the actual monthly plan payment – currently 6.8%; however, see the UST website referenced in the endnote below because this figure changes regularly o. Line 54 : Child Support Income -- income shown on Line 7 for child support may be deducted here to determine disposable income p. Line 55 : Qualified Retirement Deduction – i. Includes expenses for retirement, 401K, etc -- actual contributions ii. Includes 1/60th of the balance of debt to be repaid during the Plan term, including interest q. Line 57 : Miscellaneous -- may be used for other expenses i. Examples of expenses may be: extraordinary gas expense, substantial change in employment, adjustments for extraordinary circumstances, etc. ii. Student loans may not be taken as a deduction for calculating disposable income iii. IRS has discretionary allowance of $100 per person plus $25 for each family member, See, I.R.M. [5.15.1.10] (05-1-2004) – we will not allow this deduction without documentation and justification iv. All expenses must be “reasonably necessary to be expended … for the maintenance or support of the debtor or a dependent of the debtor” pursuant to §1325(b((2)

VI. Disposable Income a. Line 59: amount which must be paid to unsecured non-priority claims and attorney fees in the Plan

4 i The opinions and policies expressed herein are those of Herbert L. Beskin, and Rebecca Connelly, the Chapter 13 Trustees for the Western District of Virginia, as of this date in light of the cases decided and the policies adapted from other jurisdictions. These policies may change as the case law develops. Where these policies are supported or governed by the United States Trustee we have specified by indicating “per the UST.”

The UST website for means testing information, policies, and income and expense figures, can be found at: www.usdoj.gov/ust/eo/bapcpa/meanstesting.htm. These figures change several times each year and counsel should check the site regularly.