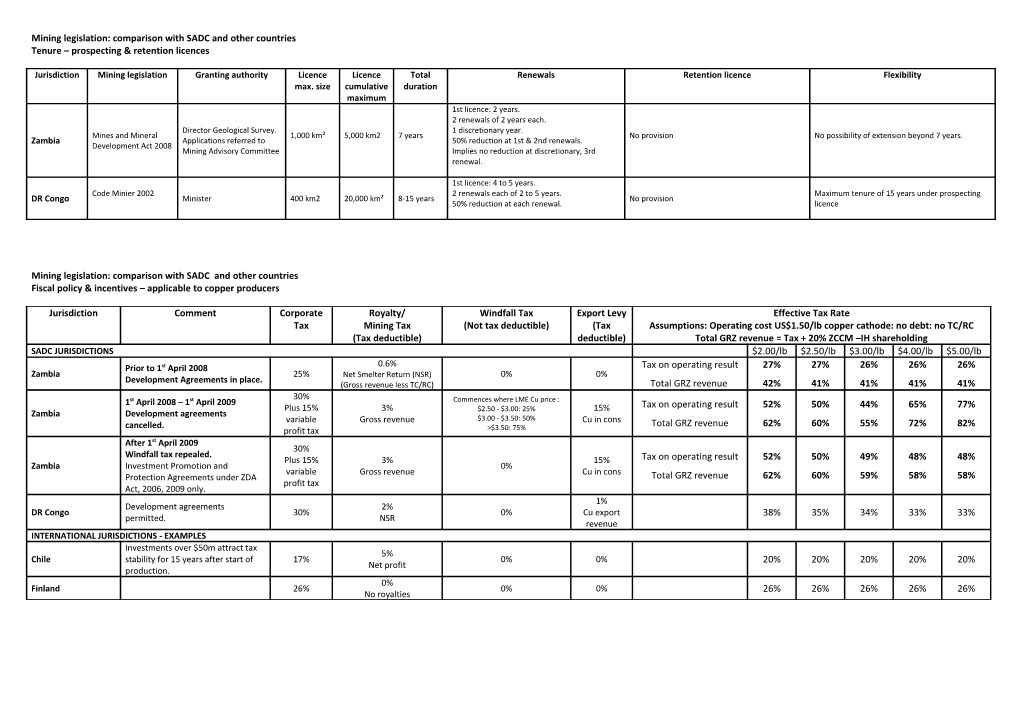

Mining legislation: comparison with SADC and other countries Tenure – prospecting & retention licences

Jurisdiction Mining legislation Granting authority Licence Licence Total Renewals Retention licence Flexibility max. size cumulative duration maximum 1st licence: 2 years. 2 renewals of 2 years each. Director Geological Survey. 1 discretionary year. Mines and Mineral 1,000 km² 5,000 km2 7 years No provision No possibility of extension beyond 7 years. Zambia Applications referred to 50% reduction at 1st & 2nd renewals. Development Act 2008 Mining Advisory Committee Implies no reduction at discretionary, 3rd renewal.

1st licence: 4 to 5 years. Code Minier 2002 2 renewals each of 2 to 5 years. Maximum tenure of 15 years under prospecting DR Congo Minister 400 km2 20,000 km² 8-15 years No provision 50% reduction at each renewal. licence

Mining legislation: comparison with SADC and other countries Fiscal policy & incentives – applicable to copper producers

Jurisdiction Comment Corporate Royalty/ Windfall Tax Export Levy Effective Tax Rate Tax Mining Tax (Not tax deductible) (Tax Assumptions: Operating cost US$1.50/lb copper cathode: no debt: no TC/RC (Tax deductible) deductible) Total GRZ revenue = Tax + 20% ZCCM –IH shareholding SADC JURISDICTIONS $2.00/lb $2.50/lb $3.00/lb $4.00/lb $5.00/lb Prior to 1st April 2008 0.6% Tax on operating result 27% 27% 26% 26% 26% Zambia 25% Net Smelter Return (NSR) 0% 0% Development Agreements in place. (Gross revenue less TC/RC) Total GRZ revenue 42% 41% 41% 41% 41% 30% 1st April 2008 – 1st April 2009 Commences where LME Cu price : Plus 15% 3% $2.50 - $3.00: 25% 15% Tax on operating result 52% 50% 44% 65% 77% Zambia Development agreements variable Gross revenue $3.00 - $3.50: 50% Cu in cons cancelled. Total GRZ revenue 62% 60% 55% 72% 82% profit tax >$3.50: 75% After 1st April 2009 30% Windfall tax repealed. Plus 15% 3% 15% Tax on operating result 52% 50% 49% 48% 48% Zambia Investment Promotion and 0% variable Gross revenue Cu in cons Protection Agreements under ZDA Total GRZ revenue 62% 60% 59% 58% 58% profit tax Act, 2006, 2009 only. 1% Development agreements 2% DR Congo 30% 0% Cu export 38% 35% 34% 33% 33% permitted. NSR revenue INTERNATIONAL JURISDICTIONS - EXAMPLES Investments over $50m attract tax 5% Chile stability for 15 years after start of 17% 0% 0% 20% 20% 20% 20% 20% Net profit production. 0% Finland 26% 0% 0% 26% 26% 26% 26% 26% No royalties