Lecture #1: A Survey of the American Economy (February 2014)

I. The Importance of the Constitution to US Economic Policy

The US economy is the world's largest national economy. It is also one of the most complicated. The US is of course composed of fifty different states (and the city of Washington DC, which is not a state) and each state has its own laws and regulations and economic activities and goals. Instead of one uniform nation, the US is really a federated system where the federal government maintains the national interest, with the states maintaining their own narrower interests. As you might expect, with fifty sets of state laws and one set of federal laws there is much that can go wrong and much opportunity for confusion.

There is no doubt that considerable tension exists between the states and the federal government. But, as a principle, the US federal government does not usually intervene in the affairs of a particular state unless the action bears some relation to the nation as a whole. In the early history of the US, this separation was strictly maintained. It was why there was not a sizeable national income tax until 1913. It is why today some banks are chartered by the state and not by the federal government. It is why that voting rules and regulations, even in federal elections, are different in different states. In addition, doctors and lawyers are typically licensed to practice medicine in one state and not in another. The rules and regulations governing economic activity in one state may be quite different in another state. Incorporating a business is a very different affair from one state to another, as are tax laws and environmental regulations.

To guarantee that a contract in one state is honored in another, the founders wrote Article IV, Section I of the US Constitution, which quite clearly states

"Each State to Honor all others Full Faith and Credit shall be given in each State to the public Acts, Records, and judicial Proceedings of every other State. And the Congress may by general Laws prescribe the Manner in which such Acts, Records and Proceedings shall be proved, and the Effect thereof."

Another important part of the Constitution deals specifically with Congress' right to regulate economic affairs and is called the Commerce Clause of the US Constitution. The Commerce Clause contains enumerated powers listed in the United States Constitution (Article I, Section 8, Clause 3). The clause states that the United States Congress shall have power

"To regulate Commerce with foreign Nations, and among the several States, and with the Indian Tribes"

In the past, Congress and the courts interpreted the clause very narrowly. However, beginning in the 1930's with President Franklin D. Roosevelt, the Commerce Clause was used to justify massive intrusion of the federal government into the private affairs of citizens within a state. Today the federal government is extensively involved in the regulation of business throughout the US regardless of the how much interstate or foreign trade is taking place. Article IV, Section I and the Commerce Clause of the US Constitution have become important focal points of legal issues surrounding problems with the US economy — from gay marriage, to regulating greenhouse gases, to President Obama's health care legislation. It is important to recognize this continuing conflict in the American system of government in order to better understand US federal economic policies. Not every economic problem has its basis in purely economic roots. A major recurring problem in the US is the appropriate legal relation between the federal government and the state and local governments. No doubt the same problems plague other countries, as well.

II. Recent US Economic Performance

What are the facts about the US economy? Here we can be less subjective and more quantitative. Let’s focus now on real growth, unemployment and inflation. A great deal can be discussed by looking closely at three economic indicators — the real economic growth rate, the unemployment rate, and the inflation rate.

Real Economic Growth in the US:

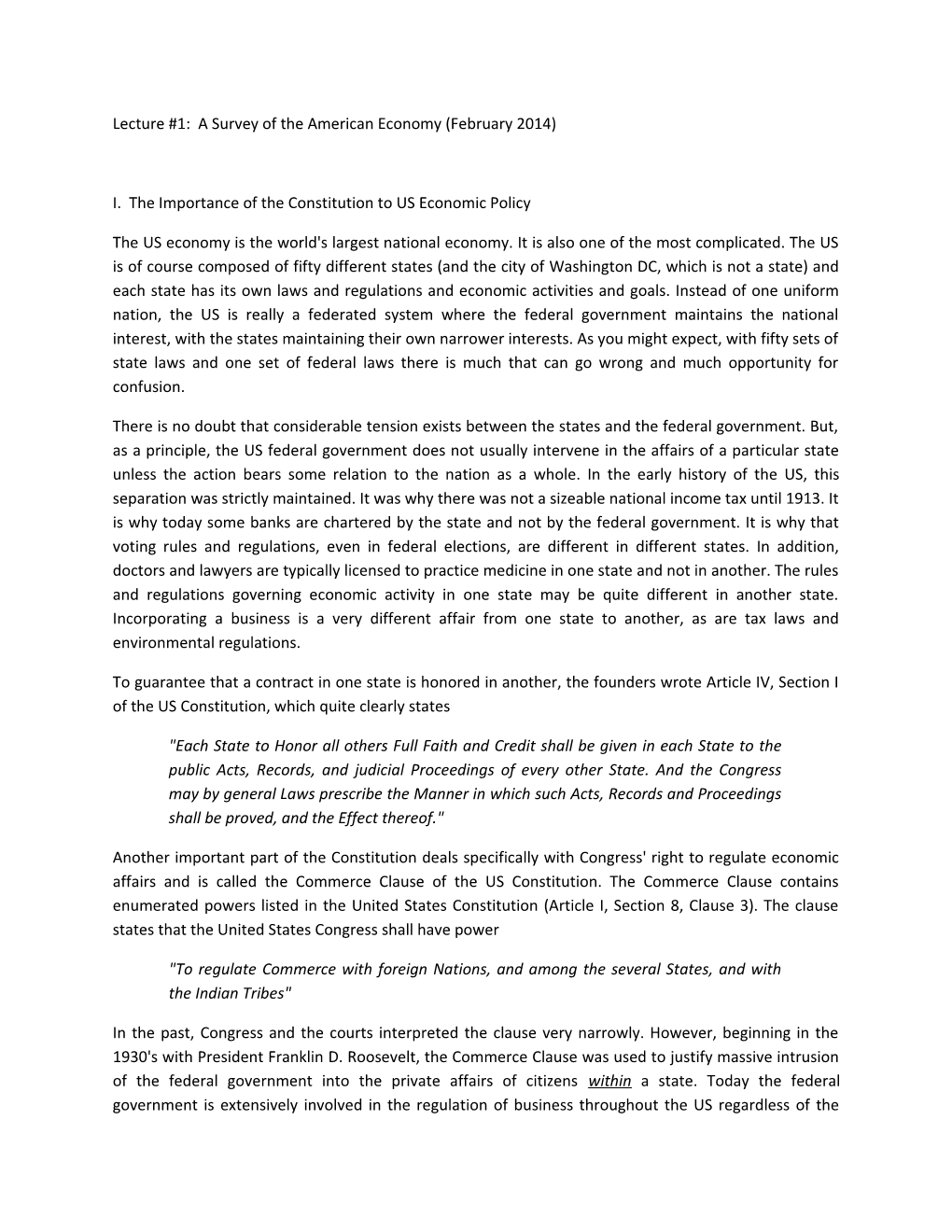

Figure 1 below shows the time series record for US economic growth over the period 1975-2013. The recessions of 1975, 1982, 1991, 2001, and 2008 are clearly evident from the figure. Average real growth over the period was 2.75%, which is very nearly equal to the natural rate of growth of the economy of 2.85%, using potential output estimates. The figure also indicates that the recent recession has been more severe than most of those that went before, if we use growth as a criterion. Highest prolonged growth appears to be in the range of 3.7%. This gives us a basic handle on how quickly the economy can grow for a period of a few years under the most ideal conditions.

The 1984 recovery growth rate of over 7% could not be sustained. A better estimate for sustained growth is 2.5%. This is the standard on which we can measure current and future performance of the US economy. The last three quarters of estimates on QoQ annualized growth that we have are

2013Q2 2.5% 2013Q3 4.1% 2013Q4 3.2%

which shows a much healthier economic condition than 2012.

The recovery from the most recent recession began in Q3 of 2009 and average growth over the period from the start of the recovery until now has been about 2.4%. This has been indeed a slow recovery. Figure 1: Actual growth and potential or full employment growth

For most of the past four years, growth of the US economy has been weak...very weak...too weak to produce enough jobs to substantially reduce the unemployment rate. Compare 2009 with 1982 and note how that the earlier period had strong and sustained growth. The population of the US is about 300 million people. The labor force is roughly 50% of this, meaning that the labor force is about 150 million (actually 155,460,000 for 2014 January's civilian labor force). If the unemployment rate is 6.6%, then a reduction of the rate to 5.6% requires the net creation of more than 1.55 million new stable jobs for the year.1 It is doubtful that this can be accomplished by the federal government spending more. Large increases in job creation require a change of perception on the part of business. Business must become much more optimistic and willing to take risks if there is to be large scale job creation. Figure 2 and Figure 3 show the differences in recoveries between 1982 and 2009. If policy is to be effective, it must

1 Note that these new jobs can be concentrated in part-time, low-paying entry-level jobs. In July of 2013 half of the jobs created during the month were in low-paying jobs. This is one reason why the unemployment rate can fall, but there is very little growth in GDP. This has important ramifications to Okun's Law, which shows the relation between the economic growth rate and the unemployment rate. Also, note that the current unemployment rate is 6.6% and that to reduce this to 5.6% in 2014, given likely circumstances of a stable labor force of 155 million people, there would have to be a NET increase of about 130,000 new jobs per month for the year. We will show this calculation later in this lecture. Figure 2: Recovery in 1982 -- Quick

Figure 3: Recovery in 2009 --Slow

be aimed at recovering both business and consumer confidence. None of the policies tried thus far have been successful at restoring confidence to levels that can be maintained. Consumer confidence is influenced heavily by the general conditions of the economy, the housing market in particular. Much of the increase in business confidence came with a continued fall in long term interest rates, movements in the stock market, and a general rise in US manufacturing exports. However, raising consumer and business confidence is not an easy task, as you might expect. Human social psychology is enormously complicated. Of course, thing may get better over time. "Hope springs eternal in the human breast". But, that is of no comfort to politicians who are seeking to retain their office. Unemployment in the US

Cursory examination of Figure 4 shows that the US unemployment rate has been quite variable over the business cycles of 1982, 1991, 2001, and 2008. Over the entire period from 1980 to 2009 the unemployment rate averaged 6.2%. This is close to the 5-6% range many economists take as the US natural unemployment rate (or NAIRU – the non-accelerating inflation rate of unemployment). The current rate of unemployment remains stubbornly high 6.6%. Looking at the severe recession of 1982, it took over two years to pull the unemployment rate down from its high. When it did drop, it fell from about 10.5% to 7.5%. However, it has been over four years since the US recovery began in 2009 Q3 and the unemployment rate has yet to return to the NAIRU. The slowness of the fall is unlike 1982 and is more like that of 1991 and 2002 with less steeply sloping declines. In the past, these were referred to as "jobless recoveries".

Figure 4: Comparison of the Unemployment Rate and the NAIRU

This thought-provoking fact (i.e. stylized fact) builds confidence in the proposition that recessions require between two and three years to see large scale reduction in unemployment. Embedded in the cyclical ups and downs shown in Figure 4 is a long run downward trend in the unemployment rate beginning in the late 1970's. From the 1980s until 2008 we see a long run trend taking the US economy's natural unemployment rate to increasingly lower average values. The average value of the unemployment rate between 2000 and 2008 was only 5.1%. This is an important stylized fact that needs to be explained. US trended performance on unemployment over the last 30 years has been exemplary, especially when compared with the EU and Japan. Note how that the NAIRU has been estimated to be slightly rising after 2009. The days of low unemployment for the US may be gone.

Inflation in the US Figure 5 shows that since the mid-1980s the US has had quite stable inflation. There is certainly a cyclical movement to inflation, but it is quite muted nevertheless. The average rate of inflation in the US from 1985 onwards was roughly 2.5%. The rate seldom rose above 4% or fell below 2%. Recently, inflation has been running below 2%. Such low and predictable inflation does not impose much cost on society.

Figure 5: Compounded Annual Change in CPI

Indeed, it is a pittance compared to the losses that occurred due to higher unemployment. Some people have been arguing that the US and other countries must create higher inflation to get people to quit holding money and start spending.

One of the problems with using inflation as a measure of price stability is that it ignores changes in asset prices. For example, housing prices and stock prices may be rising very quickly while the general price level or consumer prices are rising very slowly. This can be confusing to the central bank which is charged with maintaining price stability.