International Business, Update 2003 Cases

Harley-Davidson (B): Hedging Hogs

Harley-Davidson’s competitive comeback in the late 1980s is one of the few protectionist success stories. It is the story of a firm that used government protection to adjust to a changing competitive global market. But Harley’s success in the late 1980s brought along new problems that threatened to undermine much of the progress already attained. Harley’s primary problem was the same problem faced by many undiversified international firms: it produced its motorcycles, hogs,1 in only one country and exported its product to all foreign markets. But exchange rates change, and prices and earnings originally denominated in foreign currencies end up being worth very different amounts when finding their way back home to the dollar.2

Exporting Hogs

Harley’s sales in 1990 were more than $864 million. Of total sales, $268 million, or 31 percent, were international sales. Harley had been exporting for a very long time: for 50 years to Japan and more than 80 years to Germany. New markets were growing in countries such as Greece, Argentina, Brazil, and even the Virgin Islands. Although international sales were obviously very important to Harley’s present profitability, they also represented its future. The domestic market in the United States for motorcycles—any firm’s motorcycles—was beginning to decline. This was generally thought to be a result of changing consumer profiles and tastes. International market potential for Harley looked quite promising, but Harley had only 15 percent of the world market. It needed to do better, much better. Harley’s problem was that foreign distributors and dealers needed two things for continued growth and market share expansion: (I) local currency prices and (2) stable prices. First, local currency pricing, whether it be Japanese yen, German marks, Australian dollars, or Canadian dollars, would allow the foreign dealers to compete on price in same currency terms with all competitors. And this competition would not be hindered by the dealers and distributors adding currency surcharges to

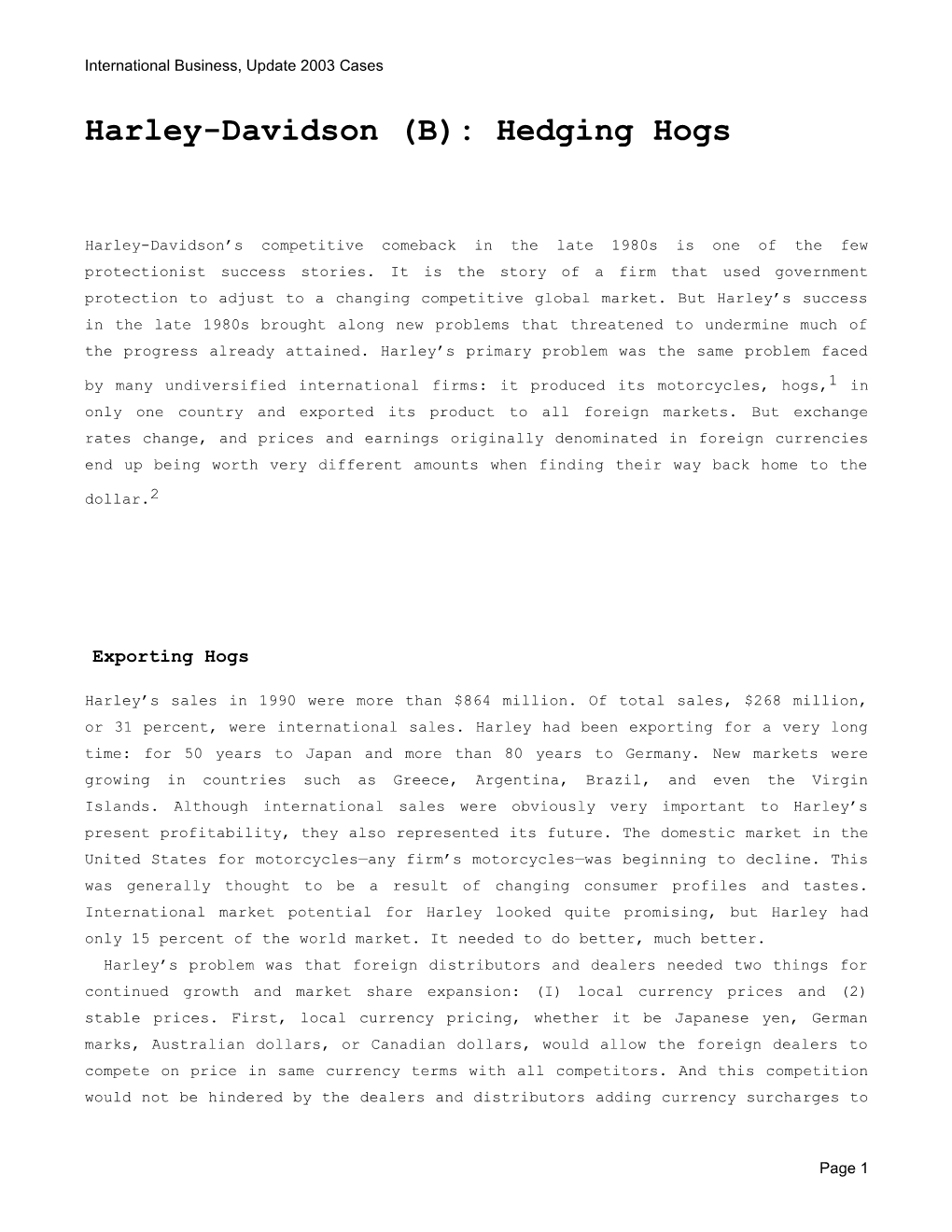

Page 1 International Business, Update 2003 Cases sticker prices as a result of their own need to cover currency exposure.3 Harley needed to sell its hogs to foreign dealers and distributorships in local currency, but that would not really solve the problems. First, Harley itself would now be responsible for managing the currency exposure. Second, it still did not assure the foreign dealers of stable prices, not unless Harley intended to absorb all exchange rate changes itself. Figure I illustrates the foreign currency pricing issue for sales of Harleys in Australia and Japan. Australian consumers shop, compare, and purchase in Australian dollars. Starting at the opposite end, however, is the fact that Harley hogs are produced and initially priced in U.S. dollars. Someone must bear the risk of currency exchange, either the parent, the distributor, or the consumer; it rarely will be the consumer.

Currency Risk Sharing at Harley

John Hevey, manager of international finance, instituted a system that Harley calls “risk sharing.” The idea is not new, but it has not been fashionable for some time. The idea is fairly simple: as long as the spot exchange rate does not move a great distance from the rate in effect when Harley quotes foreign currency prices to its foreign dealers, Harley will maintain that single price. This allows the foreign dealers and distributors, both those owned and not owned by Harley, to be assured of predictable and stable prices. The stable prices needed to be denominated in the currency of the foreign dealer and distributor’s operations. Harley would then be responsible for managing the currency exposures. A typical currency risk-sharing arrangement specifies three bands or zones of exchanges: (1) neutral zone, (2) sharing zone, and (3) renegotiation zone. Figure 2 provides an example of how the currency zones may be constructed between a U.S. parent firm and its Japanese dealers or distributors. The neutral zone in Figure 2 is constructed as a band of 1/25 percent change about the central rate specified in the contract, ¥130.00/$. The central rate can be determined a number of ways, for example, the spot rate in effect on the date of the contract’s consummation, the average rate for the past three-month period, or a moving average of monthly rates. In this case, the neutral zone’s boundaries are ¥136.84/$ and ¥123.81/$.4 As long as the spot exchange rate between the yen and dollar remains within this neutral zone, the U.S. parent assures the Japanese dealers of a constant price in yen. If a particular product line was priced in the United States at $4,000, the yen-denominated price would be ¥520,000. This assures the Japanese dealers a constant supply price in their own

Page 2 International Business, Update 2003 Cases currency terms. The predictability of costs reduces the currency risks of the Japanese dealers and allows them to pass on the more predictable local currency prices to their customers. If, however, the spot rate moves out of the neutral zone into the sharing zone, the U.S. parent and the Japanese dealer will share the costs or benefits of the margin beyond the neutral zone rate. For example, if the Japanese yen depreciated against the dollar to ¥140.00/$, the spot rate will have moved into the upper sharing zone. If the contract specified that the sharing would be a 50y50 split, the new price to the Japanese dealer would be

$4,000 x 3 ¥130.00/$+ (¥140.00/$2¥136.84/$)/24

= $4,000 x ¥131.58/$ = ¥526,320.

Although the supply costs have indeed risen to the Japanese dealers, from ¥520,000 to ¥526,320, the percentage increase is significantly less than the percentage change in the exchange rate.5 The Japanese dealer is insulated against the constant fluctuations of the exchange rate and subsequent fluctuations on supply costs. Finally, if the spot rate were to move drastically from the neutral zone into the renegotiation zone, the risk-sharing agreement calls for a renegotiation of the price to bring it more in line with current exchange rates and the economic and competitive realities of the market.

Currency Management at Harley

Harley’s risk-sharing program has allowed the firm to increase the stability of prices in foreign markets. But this stability has come about by the parent firm’s accepting a larger proportion of the exchange rate risk. Harley’s approach to currency management is conservative, both in what it hedges and how it hedges. The “what,” the exposures that Harley actually manages, are primarily its sales, which are denominated in foreign currencies. Although Harley does import some inputs, the volume of imports denominated in foreign currencies (accounts payable) are relatively small compared to the export sales (the accounts receivable). Harley is a bit more aggressive in its exposure time frame than many other firms, however. Harley will hedge sales that will be made in the near future, anticipated sales, extending about twelve months out. The ability of the

Page 3 International Business, Update 2003 Cases firm to hedge sales that have not yet been “booked” is a result of the firm’s consistency and predictability of sales in the various markets. Like most firms that hedge future sales, however, Harley will intentionally leave itself a margin of error, therefore hedging less than 100 percent of the expected exposures. Presently Harley is rather conservative in the “how,” the instruments and methods used for currency hedging. Harley uses currency forward contracts for all hedging. Harley will estimate the amount of the various foreign currency payments to be received per period and sell those foreign currency quantities forward (less the percentage margin for error). Like many other firms expanding international operations, Harley is now studying the use of additional currency management approaches, such as the use of foreign currency options. At present, however, Harley executives are satisfied with their currency management program.

Financial Management’s Growing Responsibilities

A third dimension of the new financial/currency management program at Harley is the increased role of financial management with sales. The finance staff keeps in touch with the sales and marketing staffs to work toward the most competitive combinations and packages of pricing. Financial staff also attempts to keep information lines open between its foreign dealers and distributors to help them maintain price competitiveness. Harley-Davidson is a firm that continues to be unique in many ways. Not only is it one of the true “success stories” for American protectionism, but it has continued to work to improve its international competitiveness by responding to the needs of not only its customers, but also its distributors and dealers.

Questions for Discussion 1. Why is it so important for Harley-Davidson to both price in foreign currencies in foreign markets and provide stable prices? 2. How effective will “risk sharing” be in actually achieving Harley’s stated goals? Is there a better solution? 3. Who is bearing the brunt of the costs of the financial risk management program?

References

Page 4 International Business, Update 2003 Cases

Hufbauer, Gary Clyde, Diane T. Berliner, and Kimberly Ann Elliot. Trade Protection in the United States: 31 Case Studies. Washington, D.C.: The Institute for International Economics, 1986. Pruzin, Daniel R. “Born to be Verrucht.” World Trade 5, Issue 4 (May 1992): 112–117. Quinn, Lawrence R. “Harley Uses ‘Risk Sharing’ to Hedge Foreign Currencies.” Business International Money Report, March 16, 1992, 105–106. ———, “Harley: Wheeling and Dealing.” Corporate Finance (April 1992): 29–30.

Source: This case was written by Michael H. Moffett, the University of Michigan, March 1993. The case is intended for class discussion purposes only and does not represent either efficient or inefficient financial management practices. Do not quote without prior permission.

1The motorcycles produced and sold by Harley-Davidson have traditionally been known as hogs. The nickname is primarily in reference to their traditional large size, weight, and power.

2This case draws upon several articles including “Harley Uses ‘Risk Sharing’ To Hedge Foreign

Currencies,” by Lawrence R. Quinn, Business International Money Report (March 16, 1992): 105 – 106; and “Harley: Wheeling and Dealing,” by Lawrence Quinn, Corporate Finance (April 1992): 29–30.

3For example, an independent Australian dealer who sells and earns Australian dollar revenues but must pay for the Harley hogs shipped from the United States in U.S. dollars will be accepting currency risk. If the Australian dealer then adds a margin to the hog price to cover currency-hedging costs, the product is less competitive.

FIGURE 1

Harley-Davidson’s Foreign Pricing Flow

4The upper and lower exchange rates of the band are calculated as:

(insert formula) x 100 = -5.0%. and

(insert formula) x 100 = +5.0%.

5The yen price has risen only 1.22 percent while the Japanese yen has depreciated 7.14 percent versus the U.S. dollar.

FIGURE 2

Page 5 International Business, Update 2003 Cases

Currency Risk Sharing Note: Percentage changes are in the value of the Japanese yen versus U.S. dollar. For example, a “15%” is a 5 percent appreciation in the value of the yen, from ¥130.00/$ to ¥123.81/$.

Page 6