NATIONAL ASSOCIATION OF MUNICIPALITIES IN THE REPUBLIC OF BULGARIA

1000 SOFIA, Alabin 16-20, tel: +359 2 9883763, 9800304, fax: +359 2 9879826, e-mail: [email protected]; web page: http://www.namrb.org

LOCAL FINANCE REFORM IN BULGARIA AND FORTHCOMING CHALLENGES (June 2005) 1. Background

The changes in Bulgaria over the last decade provided conditions for strengthening local self-government (free local elections, introduction of the principles of free-market economy, gradual expansion of local government competencies, etc.).

Currently, the only level of local government in Bulgaria is the municipal one. There are 264 municipalities with elected mayors and municipal councils. In fact, there are 28 districts with appointed district governors in Bulgaria, but they perform central government administrative functions, they do not provide any public services and do not have their own budgets.

Despite the positive administrative and political reforms, however, local finance system in Bulgaria stayed almost unchanged. Gradually, the gap between the existing system of local finance and the principles of market economy broadened. As a result, a consensus was reached that local finance reforms for decentralization should be implemented.

The “engine” of the lobbying for financial decentralization became the National Association of Municipalities in the Republic of Bulgaria (NAMRB) and in December 2001 the Association signed an Agreement for cooperation with the Bulgarian Government. That was the most important result of the Association’ efforts on the establishment of a durable relations and interaction with the central authorities. The document stated that one of the major goals of the joint work of the central and local governments will be “gradual implementation of the government decentralization and increasing the financial independence of municipalities.”

To the implementation of the commitments undertaken within the agreement, in March 2002 the Council of Ministers established a joint Working Group on Financial Decentralization with members representing the Government and the National Association of Municipalities in the Republic of Bulgaria. In June 2002 the Council of Ministers adopted a Financial Decentralization Concept and a Program for its implementation for the period 2002-2005. The adoption of the Program became the milestone for the introduction of the financial decentralization and municipal finance reforms in Bulgaria. As a result of the implementation of the Program and the joint efforts of the NAMRB and the Ministry of Finance, in 2003, a new ground was set for the local finance system.

One of the most important achievements in the Program implementation was that municipalities were given the powers to determine the local fees rates. They, however, still cannot determine the local tax rates, as a Constitutional amendment is necessary for that.

2. Structure of municipal finance in Bulgaria

2.1. Municipal functions

As the local finance system is currently in transition, an attempt was made to internally distinguish municipal functions into two groups: local tasks (such as waste management) and mandated tasks (such as primary and secondary schools). Expenditure standards have been developed for mandated tasks. This helped for updating the costs of public services provided by municipalities, and for identifying funding sources for the different functions. At the same time however this approach “internally segmented” the budget, which hinders the effective financial management.

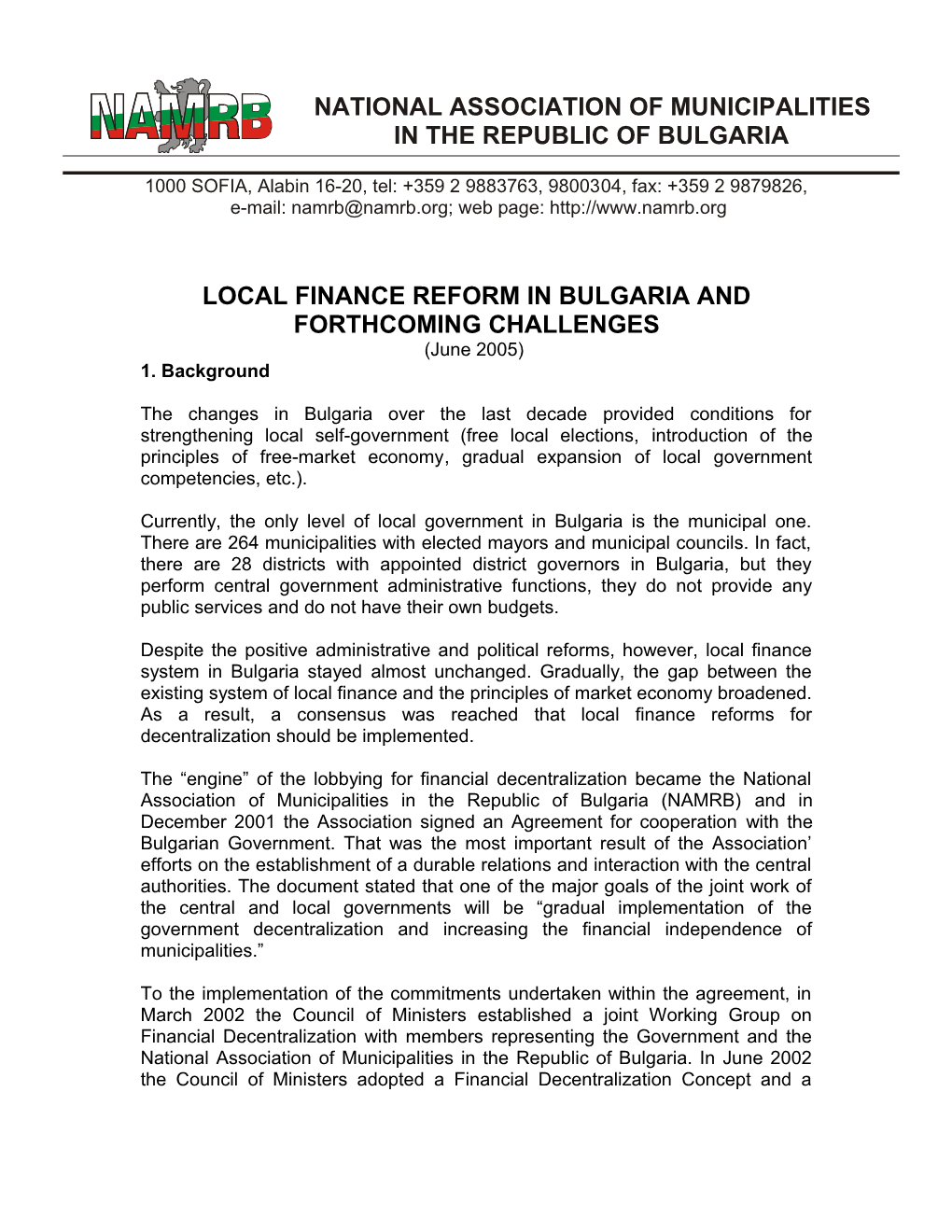

The mechanism for financing municipal functions is shown in Scheme 1.

Scheme 1. Municipal finance system

Bulgarian municipal finance system

Revenues for mandated Revenues for local functions functions Ceded PIT; Own revenues General supplementing General equalizing subsidy subsidy

Mandated functions Local functions (expenditure standards)

As seen from the above scheme, mandated functions are financed by the proceeds of Personal Income Tax, which are generated within the territory of the municipality. If the estimated revenues are more than the expenditures, according to the standards, the respective municipality receives only a percentage of the PIT proceeds. If the estimated revenues are less than the expenditures, according to standards, the municipality receives also a supplementing general subsidy to “fill in the gap”.

2 Local functions are financed by own-source revenues (local taxes, local fees and revenues from municipal property management). However, according to law, municipalities are also entitled to receive general equalizing subsidy to fund those services. The minimum amount of the subsidy is set in the Municipal Budgets Act, and the mechanism of allocation among municipalities is annually negotiated between the Minister of Finance and NAMRB. The purpose of the subsidy is to decrease the discrepancy in the taxation capacities of municipalities. The mechanism however is quite imperfect and is to be improved through development of a system of horizontal equalization.

Municipalities also receive target capital subsidy. The total amount of the subsidy is subject to annual negotiations between the Ministry of Finance and NAMRB, as well as the criteria for its distribution among municipalities.

The Annual State Budget Act also regulates what other transfers municipalities will receive from the state, but those are targeted funds, and usually related to expenses reimbursement.

Naturally, municipalities are allowed to use bank loans or bond issues to finance projects, as well as to benefit from different donor funds through project implementation.

2.2. Structure of municipal revenues and expenditures*

The structure of municipal revenues is displayed in Graph 1. Although the share of own-source revenues has been increasing for the last 3 years, municipalities still are largely dependent on state subsidies.

Graph 1. Municipal revenues structure

loans 1% own-source revenues 34%

state transfers 65%

* Based on the budget reports for 2004.

3 Local taxes are property taxes (real estate tax, heritage tax, vehicle tax, tax on acquiring property, road tax). In 2004 road tax was abolished due to the introduction of the vignette system. Tax revenues amount to just 27% of own revenues and 8.3% of total municipal revenues and their share is slightly decreasing.

The local fees revenues are increasing steadily, since municipalities were given the right to determine the rates. They do not have the right however to introduce new fees for services provided, as Constitutional amendment is needed. The share of local fees in the own-source revenues is 39%. The main local fees are for waste collection and management (64% of all fees), for kindergartens (9%), followed by social home care for elderly and tourist fee.

Other non-tax revenues of municipalities are generated mainly by municipal property management (34% of own-source revenues), which also are increasing.

State transfers were explained in part 2.1. They present 65% of municipal revenues and the share has decreased over the last three years.

Graph 2 shows the expenditure structure of municipal budgets by sectors. The share of local functions in the budget is 44% (slightly increasing due to national health care policy implementation), and the one of mandated functions is 56%.

Graph 2. Municipal expenditures structure by sectors

culture health s ocial care 4% 8% 5%

adm inis tratio education n 40% 12%

public utilities and urban developm ent 31%

4 The tendency of municipal expenditures is of increasing the share of education and urban development, and decreasing the share of healthcare and social services and welfare.

3. Primary concerns and challenges related to local finance in Bulgaria

The above mentioned changes made the budget relations between the state and the municipalities more transparent, and to a great extent provided for stabilization of the financial situation of municipalities.

The reform, however, has not yet achieve the desired level of decentralization of resources and has not expanded the powers of municipalities in service provision and budget management. The primary concerns of local finance are listed below: Municipal budgets are still used as “buffer” for state deficits. In the beginning of the fiscal year, the Parliament usually adopts a deficit macro-framework of the state budget, including for local governments, and in the end of the year, additional resources are allocated to municipalities. The decrease of municipal budgets‘ share in the consolidated state budget (14.37%) and the GDP (5.69%) continues. Some legislative amendments deprive municipalities of own-source revenues (a local tax was abolished in 2004 without being replaced by another own reliable own revenue source). Still the local tax proceeds are very low and their share in the budget revenue is only 9%. Local taxes generated only 1.7% of the total tax revenues of the state. The taxation base, however, has not been updated for years, and now the tax evaluation of property in some municipalities is several times below the market price. Each year, with the Annual State Budget Act, restrictions are set to municipalities on spending the funds from the PIT and the supplementing subsidy, which turn the general subsidy into a targeted one. Local governments should be allowed to spend the general subsidy funds on their own discretion and according to the local needs and priorities. A problem still exists with the so called “unfunded mandates”. Central government adopts laws and regulations entailing additional tasks for municipalities without the respective financial provision. This leads to overdue liabilities of municipalities and threatens their financial stability. The level of municipal investments is also very low (11% of total expenditures). If the tendency of “shrinking own-source revenue base” continues, Bulgarian municipalities might not fully absorb the potential EU funds through project implementation.

5 The above concerns related to municipal finance predetermine the challenges that both central and local government should face in the near future: Expanding the own-source revenue base of municipalities – reordering the tax system in Bulgaria and providing “space” for introduction of new local taxes; giving taxation powers to municipalities. For the latter, Constitutional amendment is necessary and public support has already been achieved; Increasing the local governments’ freedom to manage their budgets according to the local needs and priorities; Improving the equalization mechanism of subsidies; Developing a new law on local finance, which will set a better base for municipal budgets; Municipal capacity development for assuming taxation powers and creating own tax administrations; Developing expert and financial capacity for EU funds absorption and supporting the municipal co-financing contribution for projects.

All those challenges will be on the agenda of the National Association of Municipalities in the joint work with the newly elected Parliament and the new Government.

6