1

The Capital to Labor Ratio and the Long Run Cost Function

Questions: 1. What is the long run cost function? If a firm uses only capital and labor, what is the ratio of the two inputs that minimizes cost? Be sure to define the terms.

2. Describe returns to scale and relate to long run average costs.

3. Given appropriate information, calculate the capital/labor ratio that minimizes costs.

4. Given appropriate information, find the long run cost function.

The Economically Efficient Combination of Inputs If a firm chooses to use more capital, its short run cost function will change. The result will generally be a change in marginal revenue and in the utilization of labor. And that will in turn change the marginal revenue product of capital This implies that a little more work needs to be done to determine how much capital should be used. In general, a firm should use an amount of each and every input such that the marginal revenue product of each input is equal to the price of the input (or rental rate.) In the short run, this determines the proper combination of the variable inputs. In the long run, it determines the proper combinations of all inputs. To keep things simple, we have dealt with only two inputs, labor and capital. In the long run, both vary. Still, the marginal revenue product of capital must equal the implicit rental rate on capital and the marginal revenue product of labor must equal the wage rate. This allows one to find the proper capital/labor ratio.

MRPl = MR * MPl = w And MRPk = MR*MPk = Kr

So, MR = MPl /w and MR = MPk/Kr

But that means MPl/w = MPk/Kr or MPl /MPk = w/Kr

In words, the ratio of the marginal products to the prices (or rentals) of every input must be equal. For any two, the ratios of their marginal products must be equal to the ratios of their prices (or rentals.)

Why is this the economically efficient combination of labor and capital? Because it produces the output at least cost, and as long as the prices of the inputs signals their opportunity costs, that implies the least sacrifice of other goods. Why do these relationships hold when the combinations of inputs allow for minimum cost? The best way to see this is to consider an example. Suppose that the wage rate and the rental rate for capital were the same. If one unit of capital is used to replace one unit of labor, then total cost remains the same. If the marginal product of capital is greater than the marginal product of labor, then output increases, so the cost per unit decreases. That is because the marginal product of capital is how much extra output one more unit of capital can produce and the marginal product of labor is how much output will decrease when one less unit of labor is used. So as long as the marginal product of capital is greater than the marginal product of labor, the firm will get more and more output at the same total cost by replacing labor with capital. Of course, pretty soon there won’t be enough workers to operate all the machinery, so the marginal product of capital will fall. And the marginal product of labor will rise because a bit more labor could be put to good use with all of the machinery. Eventually, the marginal product of capital and the marginal product of labor will be equal--just like their prices. Suppose the prices (or rentals) are not equal? Then the marginal products won’t be equal either. Suppose the rental rate on capital is twice the wage rate. If the marginal products of capital and labor were equal, then using one less unit of capital and one more unit of labor would leave output the same, but costs would fall. The capital good not used would save twice as much money as the extra unit of labor would cost. The firm could lower cost by using less capital and more labor. But as less capital is used and more labor, each worker would have fewer tools, tending 2 to reduce his or her marginal product. And more capital would be very useful to those additional workers. So the marginal product of labor would fall and the marginal product of capital would rise. Still, the firm could save money until the amount of output sacrificed by using one less unit of capital is twice the amount of output obtained by one more unit of labor.

Capital to Labor Ratio Calculating the capital to labor ratio is simple. Suppose your production function is:

Q = .1L.5K.5

The MPk is the first derivative of the production function with respect to capital. Just treat labor as a constant!

.5 .5-1 MPk = .5*.1L K

.5 -.5 MPk = .05L K

Now, do the exact same for labor. Take the first derivative of the production function with respect to labor and treat capital as a constant.

.5-1 .5 MPl = .5*.1L K

-.5 .5 MPl = .05L K

The ratio of the marginal products is equal to the ratio of the prices, so:

MPl / MPk = w/Kr

With the wage being 5 and the rental of capital 2000, that results in:

.05L-.5 K.5/.05L.5K-.5 = 5/2000

That simplifies to:

L-.5-,5K.5--.5 = .0025

L-1K1 = .0025

K/L = .0025

That means for each man hour of labor used, you use .0025 units of capital.

K = .0025L

L = 400K

Long Run Cost Function The long run cost function determines the cost of producing a given output with the minimum cost combination of both fixed and variable inputs. In the long run, all inputs can be adjusted. If capital is fixed and labor is variable, the both labor and capital can be adjusted. Finding the long run cost function is simple with just two inputs. Use the long run production function and 3 the capital to labor ratio.

Q = .1L.5K.5 K = .0025L

Q = .1L.5(.0025L).5

Q = .1 * (.0025) .5 L.5*L.5

Q = .1* .05 *L .5+.5

Q = .005L

L = 200Q

K = .0025*200Q

K = .5Q

TC = wL + KrK = 5*200Q + 2000*.5Q

= 1000Q + 1000Q

TC = 2000Q

Profit Maximization in the Long Run

Finding the long run profit maximum is no different than in the short run. Marginal revenue must equal marginal cost.

TC = 2000Q

MC = 2000

MR = 3253- .1Q

MR = MC

3253 - .1 Q = 2000

-.1Q = 2000-3253

-.1Q = -1253

Q = -1253/-.1

Q = 12,530

To find the amount of capital and labor to be used the relationships used for the long run cost function.

L = 200Q L = 200(12530) 4

L = 2,506,00

K = .5Q

K = 6256

Total cost, price, revenue, profit, and average cost are found in the usual way. There is no such thing as average variable cost in the long run (or rather since everything is variable, it is the same as average cost.)

Returns to Scale and Long Run Average Costs

Returns to scale describes what happens to production when all inputs are changed in strict proportion. Constant returns to scale means that if all inputs are changed in proportion, output changes in the same proportion. For example, if all inputs double, output doubles as well. The production functions used in the example has constant returns to scale. On a Cobb-Douglas production function, so long as the exponents in the production function add up to one, there are constant returns to scale.

K = 100, L = 400

Q = .1(400).5 (100).5

Q = 20

K = 200, L = 800

Q = .1(200).5 (800).5

Q = 40

With constant returns to scale, long run average cost are constant. The long run cost function found in the example was:

TC = 2000Q

AC = TC/Q = 2000Q/Q = 2000

Since average cost is always 2000, that means that average cost are constant. If long run average costs are constant, then small firms can compete effectively with large firms.

Increasing returns to scale means that increasing all inputs in proportion increases output more than in proportion. If all inputs are doubled, output will more than double. With a Cobb-Douglas production function, if the sum of the exponents on all the inputs is greater than one, then there will be increasing returns to scale. Since average cost is total cost divided by output, and cost rises in proportion to input use, then if output rises more than in proportion in input use, average cost must fall. Increasing returns to scale implies that long run average costs fall as output rises. This means that the larger a firm’s operation, the lower its average cost. Increasing returns to scale make it impossible for small firms to compete with large firms. The small firms have excessively high unit costs.

Decreasing returns to scale means that increasing all inputs in proportion increases output less than in proportion. If all inputs double, output increases, but it doesn’t double. Decreasing returns to scale implies that 5 long run average costs first. The larger the scale of operations the higher the average costs.

Economists have found that most firms have increasing returns to scale at first and then begin to face constant returns to scale. That means that long run average costs decline at first, but then become constant. The result is that very small firms have excessively high costs, but quite small firms have similar unit costs to large firms and compete effectively. Some economists argue that extremely large firms become so difficult to manage that they are begin to suffer decreasing returns to scale and rising long run average costs.

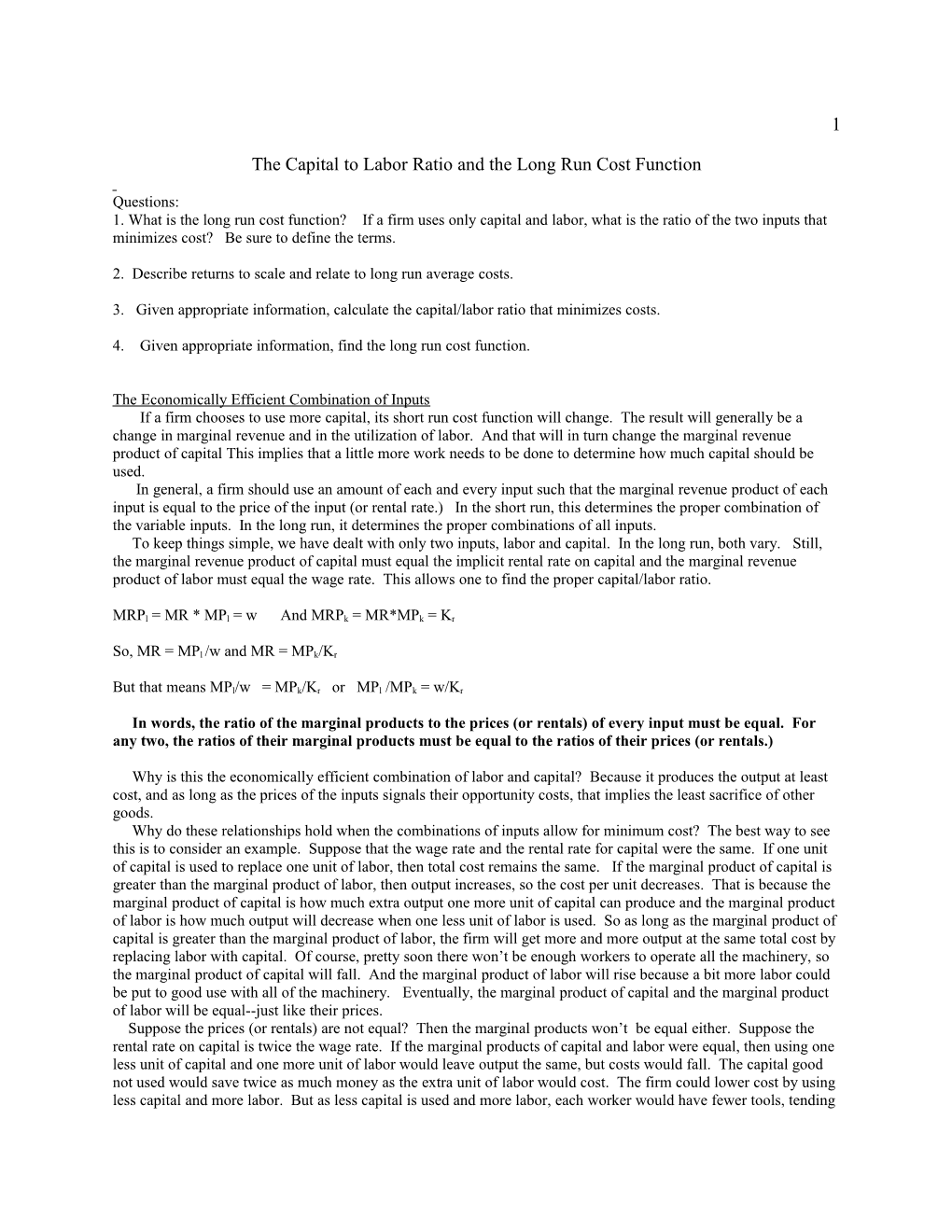

LRAC

Q

When LRAC is falling at the beginning, there are increasing returns to scale. When it is constant in the middle range, there are constant returns to scale. And at the end, when it rises again, there are diminishing returns to scale for gigantic dinosaur firms.