Bo Sjö 2012-10-08

What is the interest rate?1

Interest rates are often referred to as the cost of waiting. When you save money you take a part of your present income and wait with consumption until some future date. As compensation you receive interest on your savings. An economist would say it like this; you receive a yield or a return on your savings so that you feel compensated for giving up some of your consumption today. In this memo, and in the one that follows, we will try to fill the need for a more formal treatment of “the interest rate”, since it plays such an important role in our lives.

Consider the basic identity between production, income and spending in a country,

Total production = total income = consumption + savings

Total production or more often Gross national Income (GNI) = Wages + capital income (interest and dividends) = consumption + savings.

By definition what is not consumption (C ) must be savings (S). Saving is by definition equal to investments (I).

In term of national accounts we have Y = C + I Where Y - C = S

On the margin, between what people chose to consume and save (invest), is the interest rate. The interest rate measures the alternative cost of consumption today compared with consumption in the future. The flow of funds analysis below illustrates this in terms of supply and demand for loanable funds.

It follows from the there can never be an economy without an interest rate. Only if all income is consumed immediate, without any savings, would you get an economy without interest rates. Thus, trying to ban interest rates only means that people have to invent (costly) ways to get around the ban to protect their wealth.2

How do we measure and define interest rates?

When we talk about interest rates in economics we refer the yield (=Yield to maturity YTM) on zero-coupon government bonds. In a more general way of speaking interest rates refers to the YTM on government bonds of all maturities including also coupon paying government bonds. However, the later can lead to confusions. The difference is between interest rates and yields.

1 Still preliminary but a substantially updated version from before. Spelling and grammar errors can still persist. 2 If you want o see how it working (or rather not working for ordinary people) visit Iran a country where the rules have banned interest rates but at the same time run inflation rates around 30%.

1 In the general speech interest rates are often used to imply discount rates, coupon rates, YTM:s and various yields. When analysing bonds and all sorts of debt instruments it is important to separate between the yield of a bond and the interest rate.

The price of a bond is present value of the expected cash flows the bond is offering. A zero coupon government promises a payment of a principal/face value/nominal value at a specific future date. The face value is often a round number such as 100, 1000 or 1m (say in euros, dollars, kronor etc).

The government borrows by issuing the bonds of different maturities on an auction market. Bidders decide on much they want to pay for receiving say €1000 a year from now. These bonds, once they are issued, can then be bought and sold on a second-hand market. For bonds with a maturity up and including one-year the market is called the money-market. It is on the money market that interest rates are determined.

The price (P0) of a one-year zero-coupon paying bond is therefore determined by the following formula,

FVT P0 , 1 y

where FVT is the face value to be paid out at time T. The yield (to maturity) of this bond (y) is the one-year interest rate. When bidding for the bond buyers must calculate what interest they demand for giving their money away in exchange for promise to get a nominal value paid out at a future time T. The mechanism is the same as going to the bank and save in a deposit account, or borrow by use credit on your account. The difference is that the bank account is an over-the-counter market (OTC-market) while the bonds we talk about are bought and sold on regular markets.

Though the price is easy to calculate, prices for government bonds are usually quoted in per cent of the face value.

Money market bonds, i.e. bonds with maturity are usually referred to as ‘bills’ or “treasury bills” in English. In Sweden the instrument is called Statsskuldväxlar SSKV.

In Sweden the face value is SEK1 000 000, which is the minimum amount one can invest. Prices on bonds are quoted in per cent of the nominal value. If the price of a one-year so- called SSKV (Statsskuldväxel) is 998 000, the price quotation is 99.8. However, price quotations are quite complex. We need a special lecture on quotation only.

To know the one-year interest rate simply divide the face value with the price,

FV y T 1. P0

The yield on this government bill is the yield you get if you buy the bond today and keep it until maturity. If you sell the price before maturity you will receive the going price at that particular time and the yield will be different.

2 If the face value is €100 and the price is €99.01, the yield (and the interest rate) is

FV €100 y T 1 => 1 0.02030 or 2.03% P0 €98.01

Since the government, in most cases, can be assumed to be fully solvent and fulfil the promise to pay out the face value at maturity, government bonds are often assumed to be risk-free meaning that they are without default risk.

Referring to government bonds as “risk-free” simply refers to default free. Other risk remains when purchasing government bonds such as market risk and inflation risk.

The government will typically issue bond zero-coupon bonds with maturities one-month, three-months, six-months and one-year. Often the most liquid markets are for three and six- months bonds. When bonds are issued with longer maturities they come with coupon payments.

For a three-month government bond (or bill) the price is determined as a function of the yield as

FVT P0 1 y / 4

Notice that yield and interest rates are always expressed on an annual basis, which explains the y/4 conversion factor.

The conversion factor, in this context, is usually determined as n/360, where n is set to 30 days a month. There three conventions

Practice Day count in period Days /Year February International Exact number of days 360 28 (28/360)x0.045= British Exact number of days 365 28 (28/365)x0.045= Swiss Assumed 30/month 360 30 (30/360)x0.045=

Thus, you have USD 10m and an interest rate set to 4.5%, how much interest do you get for the month of February? Depending on the convention used you get

With the short-term interest rate of a country we usually refer to the yield on a 3-month treasury bill. The long-run interest rate is usually represented by the YTM on a ten-year government bond.3 To get a quick overview of rates and how they change across countries see The Economist.

The value of a ten-year annual coupon paying government bond is the present value of the expected cash flows the bond is offering. The following formula, where FV = face value, C =

3 Depending on the country is could be five-year government bond. Sweden for a long time used a five-year rate to represent the long-run interest rate.

3 coupon payment, T is the number of periods (in this case years) until maturity and y is yield to 4 maturity (YTM). P0 defines the price today ,

T C FVT P0 t T . t1 1 y 1 y

The coupon payment C is determined by the coupon rate c multiplied with the face value C = c x FV. The coupon payments are the same for all periods. Hence there is no time subscript on C.

The annuity solved by using the annuity formula,

T C T 1 1 t Ar% C T C t1 (1 y) r r(1 r) where in the formula r represents the value of y (YTM).

Some countries issues government bonds that pay coupons semi-annually. For semi-annual coupon the formula is

2xT C / 2 FVT P0 t 2xT t1 y y , 1 1 2 2 where T is the number of years to maturity. Thus, 2xT equals the number of periods to maturity.

The yield to maturity (y) is the return on the bond if it is kept to maturity. Given the price, the coupon payments and the face value it is possible to solve for the YTM. The YTM can be seen as an average discount rate over the whole investment horizon, up to time T.

The YTM of a zero coupon government bond is called the interest rate y = r. If you buy a bond today it means that you abstain from consumption today, to be able to consume in the future. The compensation for waiting with your consumption is time value of money, a fundamental concept in all investment and savings calculations.

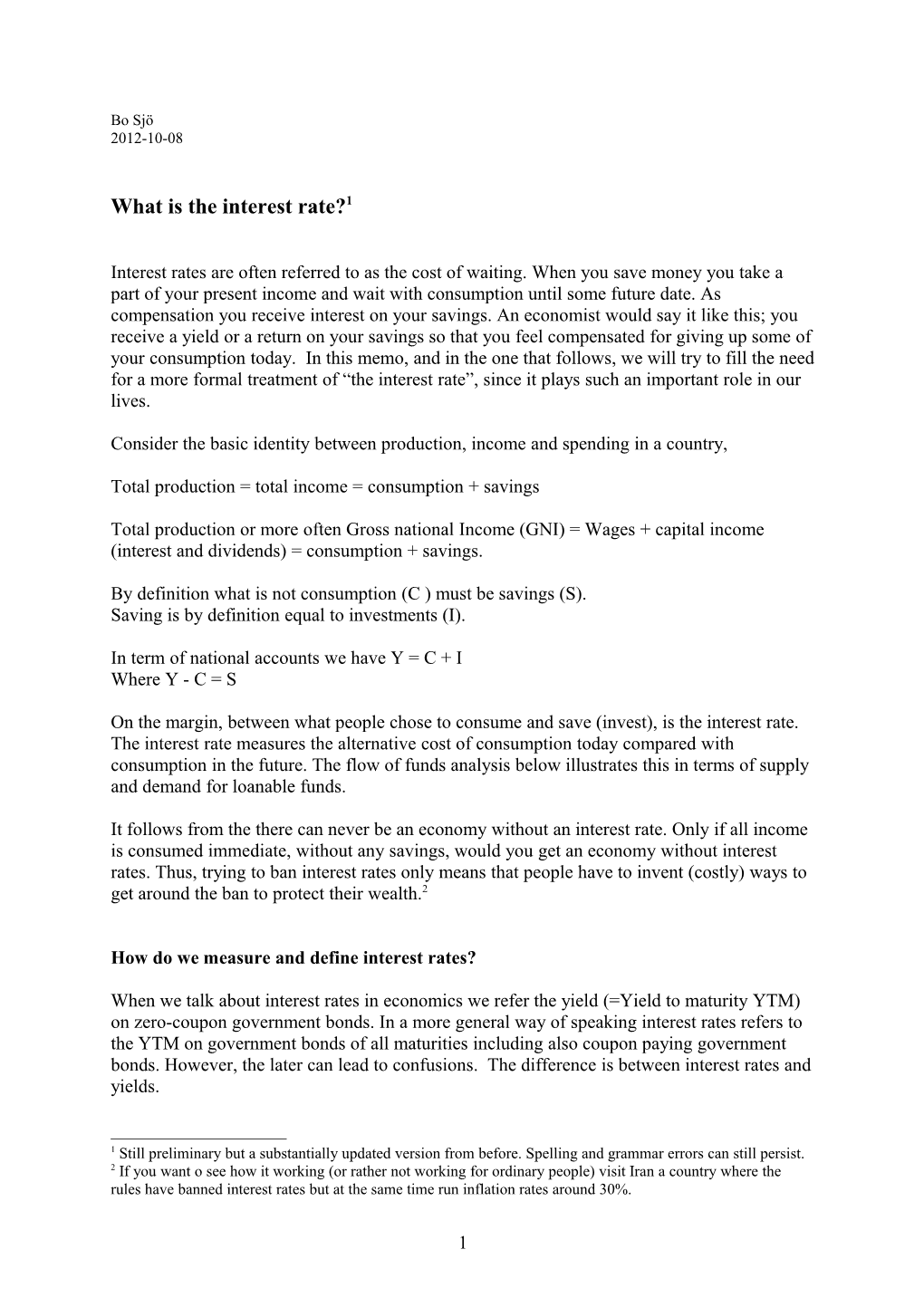

The relationship between bond prices and yields (interest rates) is negative and convex, as the bond pricing formulas shows above and the following graph is illustrating.

Figure 1. The relation Between Bond Prices and Yields.

4 Please notice the use of sum sign to avoid writing out all individual discounted coupons.

4 r

P

Since there exist a number of zero-coupon risk-free bonds with different maturities, at each moment, there are several interest rates at the same time. We refer to the interest rates that exist at a point in time as spot interest rates. These spot interest rates over different maturities are linked through the terms structure of interest rates, in such a way that we can talk about one interest rate in the economy. It is important to understand how this link works.

What determines the interest rate?

1. The loanable funds theory. Demand and supply of loanable funds.

The yield to maturities on risk-free (or rather default free to be exact) bonds define the interest rates. The next question is what determines the level of the interest rates. For that purpose we set up figure of demand and supply of loanable funds. The conclusion is that the interest rate, like any price, is determined by demand and supply. In this case it is the demand and supply for loanable funds (say the supply of savings that goes to the bond markets. The following Figure 2 (below) illustrates the concept.

As the interest rate goes up more people wants to save and the supply of loanable funds (savings) goes up. As the interest rate goes up people would like to borrow less. Thus, demand for loanable funds goes down. The equilibrium interest rate balances demand and supply for loanable funds.

In this graph, we can let the interest rate be the nominal or the real interest rate depending on the analysis we are aiming at. You find this graph in many text books, and for real rate of interest.

5 Figure 2. The interest rate and loanable funds.

r

SupplyDemand

DemandSupply

Supply of Loanable Funds

The figure illustrates how the interest rate is determined by demand and supply. Households supply loanable funds (they save). The industry and the government demands loanable funds (they invest).

The central bank will be an important player. The central bank have tools for affecting bank and credit institutions demand and supply and thereby affect the interest rate.

By analysing the main macro factors that move demand and supply (shifts the behaviour of households, industry and the government) we can understand how interest rates moves. Typical macro factors are changes in inflation, business cycle, return on investments and government borrowing.

The demand and supply can be decomposed into the private sector net demand and public sector net demand. At the short end of market, the central bank is often an important actor and can therefore influence short term (money market) interest rates. Typically the banking sector as a whole has excess liquidity at the end of the day. Central banks buy this excess liquidity and thereby determine (or have a strong influence over) short-term interest rates, given the net demand and supply by the private sector. Short term rates are important for consumer credits. However, controlling long term capital market interest rates, important for investment decisions are more difficult.

All interest rates, yields and returns are linked. First, the risk-free government bond yields over different maturities are linked through the yield curve. Given the yield curve other yields are linked over different maturities through the term structure of interest rates.

6 As the interest rate goes up more people wants to save and the supply of loanable funds (savings) goes up. As the interest rate goes up people would like to borrow less. Thus, demand for loanable funds goes down. The equilibrium interest rate balances demand and supply for loanable funds.

In this graph, we can let the interest rate be the nominal or the real interest rate depending on the analysis we are aiming at. You find this graph in many text books, and for real rate of interest.

The demand and supply can be decomposed into the private sector net demand and public sector net demand. At the short end of market, the central bank is often an important actor and can therefore influence short term (money market) interest rates. Typically the banking sector as a whole has excess liquidity at the end of the day. Central banks buy this excess liquidity and thereby determine (or have a strong influence over) short-term interest rates, given the net demand and supply by the private sector. Short term rates are important for consumer credits. However, controlling long term capital market interest rates, important for investment decisions are more difficult.

The interest rate (r) can be defined as from investing $ at time t, with maturity at time t+1 in a default- free asset. Thus, we have that one dollar today is equal to the future value of a dollar at maturity t, $1t = $1(1+r)t+1.

The nominal interest rate can decomposed as

(1+r) = (1+rr)(1+%pe) where r is the nominal risk-free interest rate, rr is the real interest rate and %pe is the expected rate of inflation. It follows that we can write the real interest rate as,

(1+rr) = (1+r)/ 1+%pe).

Changes in the interest rate reflect people’s expectations about the future business cycle. If people expect the economy to go down, they save more to compensate for the coming bad times. The supply of loanable fund increases and the interest goes down. (Supply curve shifts outward as consequence of changing expectations.) If people believe the economy is going up, they save less, and spend more today. The supply of loanable fund decreases, the supply curve shifts inwards, and the interest rate goes up. Below we will return to this discussion.

2. Analysing Bond Markets and Bond Prices more Explicit

The interest rate is not the primary variable in the bonds markets; it is the price of bonds which comes first. Thu, instead of looking at the interest rate let us look at the price of bonds as a function of the demand and supply of bonds.

On the vertical axis we write P for the bond price. Instead of loanable funds we write Q for the quantity of bonds on the market. The quantity of bonds (demand for investment capital) is the opposite of the supply of loanable funds (savings). The result is the following figure, were we put in the inverted interest rate (the yield on bonds) on the right hand side. An increase in the interest rate is associated with moving down along the right most arrow.

7 Figure 3. Bond Prices and Yields.

P 0

Supply

Demand r

Q Quantity of Bonds

The demand and supply for bonds can be used to analyse the effect on the interest rate and bond prices. First we will study the most important demand factors, which if they change will move the demand curve and establish a new level of prices and yields. Second, we will look at the most important supply factors, which will make the supply curve shift and lead to new prices and yield.

The Demand Side

What are the important demand factors? We state the following, not necessary in any order,

1) The wealth effect 2) Expected return on the bond – the expected inflation rate 3) The risk of holding bonds 4) The liquidity of the bond market. 5) Changes in the expected growth of income (business cycle & consumption smoothing).

Notice that the price of the bond is not a demand factor. The price is something that is solved as a combination of the demand and supply of bonds.

8 These demand factors move the demand curve, and thereby bond prices and interest rates in predictable ways.

The Supply Side

Next, consider the most important supply factors.

1) The expected return on real investment (changes in the business cycle or productivity). 2) The expected inflation 3) The impact of economic policy

Conclusion: Expectations are important. Inflation and future growth of the economy. This of course also reflected in the changing slope of the yield curve (yield on long run bonds – yield on short term bonds) [rlr – rsr]. And, pay special attention to the expected inflation. It has clear and strong effect.

We are now ready to move deeper into the nature of interest rates, and stochastic discount rates, Part II – Intertemporal asset pricing.

The Money Market – to be completed.

Instruments on the money market

- Tbills (SSKV) - CD:s - Commercial papers - Repos and reversed repos (Anyone can use the instrument, but central baks does to smooth out liquidity) - Eurocurrency

Central bank tools -Repos - Intervention buy and sell government bills and bonds - Change the interest rate that the banking sector pays on reserves held in the central. (Alternative the rate on borrowed reserves) This is the main instrument. Direct controls over reserve quotas will not work anymore, see Eurocurrency markets

Central banks typically have two targets: 1) Inflation target, and 2) stabilise output growth around full employment output growth.

The interbank market How the central bank is controlling the bank rates on the short term market.

What is the interest rate? How are interest rates determined? Interest conventions Money market instruments How can the central bank affect

9 Government bonds vs. corporate bonds International bonds, Global bonds Bond yield differences Yield curve, terms structure of interest rates, and theories about the terms structure of interest rates.

10